Artificial Intelligence in the German Chemical and Pharmaceutical Industry: A Comparative Analysis of Empirical Survey Results from 2020 and 2025

This study presents a comparative analysis of survey data collected from 124 companies in the German chemical and pharmaceutical industry in 2020 and 2025. The findings reveal a clear upward trend in digitalization: in 2025, 91% of companies rated digitalization as “relevant” or “very relevant”, up from 75% in 2020. Over this period, digital initiatives shifted from a focus on basic IT infrastructure and communication tools to a more consistent integration of artificial intelligence (AI). The adoption of AI grew substantially, with active use expanding from 34% of companies in 2020 to 76% in 2025. Generative AI tools, such as ChatGPT and customized enterprise assistants, are increasingly embedded in daily operations, particularly in large firms and a rising number of SMEs. AI’s relevance is highest in research & development and customer service, likely reflecting new generative AI capabilities. Main obstacles to AI shifted from organizational and budget issues in 2020 to technical and regulatory challenges, particularly IT security, in 2025. Mid-sized companies (50-999 employees) report the greatest difficulties in keeping pace with digital transformation. Overall, the sector is transitioning from isolated pilot projects to broad, multi-functional use of AI technologies.

1 Introduction

The chemical and pharmaceutical industries are undergoing rapid digital transformation, driven by advances in automation, data analytics, and increasingly, artificial intelligence (AI). AI applications have moved beyond niche uses in process optimization and forecasting to become integral tools in day-to-day business operations. The broad potential of AI in these sectors is well established (Henstock, 2019; Baum, 2021; Mowbray, 2022; Womack, 2022; Laska, 2023; Toniato, 2023; Konrad, 2024; Ananikov, 2024). Key areas of application include research and development (Ulbrich, 2021; Womack, 2020; Laska, 2023; Konrad, 2024), drug development (Mak, 2018; Kulkov, 2021; Patel, 2022; Vora, 2023; Maharjan, 2023), production (Womack, 2020; Kulkov, 2021; Chiang, 2022; Laska, 2023; Maharjan, 2023; Konrad, 2024), supply chain management (Womack, 2020; Kulkov, 2021; Chiang, 2022; Laska, 2023; Konrad, 2024), sales and customer service (Womack, 2020; Kulkov, 2021; Konrad, 2024), regulatory affairs (Walsh, 2021), sustainable chemistry (Toniato, 2023), quality assurance (Kulkov, 2021; Laska, 2023), and innovation in start-ups (Dreiling, 2025). Despite extensive documentation of AI’s relevance, comprehensive research on its actual implementation and changing significance over time remains limited. Existing studies include a global survey of 400 executives in the chemical industry (Womack, 2020), qualitative interviews with executives in pharmaceutical firms (Kulkov, 2021), and sector-specific reviews (Chiang, 2022; Patel, 2022). However, there is no systematic analysis focusing on the German chemical and pharmaceutical industry. This study addresses this gap by presenting and comparing survey results from German chemical and pharmaceutical companies in 2020 and 2025. The analysis covers company demographics, digitalization strategies, adopted measures, AI uptake and understanding, and perceived barriers to implementation. By examining changes over time, the study offers new insights into evolving trends and challenges in digitalization and AI adoption within these sectors.

2 Methods

This study uses a mixed-methods design, combining quantitative and qualitative survey approaches to assess the development of digitalization and artificial intelligence (AI) in the German chemical and pharmaceutical industry. Data were collected via standardized online questionnaires, distributed to industry professionals in two survey waves, in 2020 and 2025.

2.1 Survey Design

The questionnaires covered three core areas: (1) company and respondent demographics (industry sector, role, and employee count), (2) digitalization practices and obstacles, and (3) AI understanding, usage, and obstacles. Both closedended (single-choice and Likert-scale) and open-ended questions were used to ensure data depth and comparability. Closed questions assessed topic relevance and obstacles, while open questions captured detailed experiences and perspectives on digitalization and AI. Company size was benchmarked against the categories defined by the German Chemical Industry Association (VCI) to assess sample representativeness.

2.2 Sampling and Data Collection

Respondents included employees from companies of various sizes, roles, and functions within the chemical and pharmaceutical sectors. Recruitment took place through professional and alumni networks, email invitations, and LinkedIn outreach, targeting both SMEs and large enterprises. Participation was voluntary and all responses were anonymized.

2.3 Data Processing and Analysis

Closed-ended responses were analyzed quantitatively using descriptive statistics and visualized with bar charts. Openended answers were grouped into thematic categories. Results from the two survey waves were compared side by side to identify trends and changes over time. This comparative approach enabled analysis of key developments and ongoing challenges in digitalization and AI within the industry.

3 Results

3.1 Sample Characteristics

In the 2020 survey, 68 questionnaires were returned, with 66 completed and included in the analysis. In 2025, 81 questionnaires were returned, 57 of which were complete and analyzed. The total number of companies in the sector was 4,013 in 2020 (VCI 2022) and is currently (latest data refer to 2023) around 2,000 (VCI 2024). Given the small survey sample compared to the industry total, results should be viewed as exploratory rather than representative. We compared the distribution of survey respondents to VCI employee size classes (Fig. 1). Both surveys included companies of varying sizes. In 2020, respondents from the 50-249 and 1000+ employee segments were proportionally similar to the sector average, but those from <50 employees were overrepresented and those from 250-999 employees underrepresented, potentially biasing results toward smaller and larger companies.

Figure 1 Comparison of the distribution of survey respondents by company size (number of employees) in 2020 (left, N=66) and 2025 (right, N=57) with the overall industry distribution according to VCI classification.

In the 2025 survey, respondents from companies with 1000+ employees were overrepresented compared to the industry average, while the share from <50 employees was closer to industry proportions. Respondents from the 50-249 and 250- 999 employee categories were underrepresented, though still sufficient for analysis. This distribution (see Fig. 1) should be considered when interpreting results, as it may introduce bias. Regarding industry sectors, both surveys showed similar distributions (Fig. 2). Most respondents work in chemical and pharmaceutical companies, including sectors such as distribution and biotechnology/diagnostics. Other mentioned sectors include plant engineering, consumer goods, coatings, contract research, manufacturers/suppliers of additives/ auxiliaries, analytical service providers, and consulting.

Figure 2 Distribution of survey respondents by industry sector in 2020 (N=66) and 2025 (N=57).

Since most respondents work in the targeted industry sectors, the survey results for this category are considered valid for addressing the research question. A similar pattern is seen in the organizational positions of respondents in both surveys (Fig. 3). Most work in R&D, reflecting its importance in the chemical and pharmaceutical industry. Around 14–15% are in Marketing and Sales, often covering technical sales and service in B2B.

Other relevant functions represented include management, Quality Management (QM), and Production, covering key stages of the value chain. The “Other” category includes roles such as Procurement/Purchasing, Business Development, Supply Chain, Digitalization, Project Management, Product Stewardship, and Application Engineering. The respondents’ positions in both surveys are both comparable and relevant to our research question.

Figure 3 Distribution of survey respondents by organizational position in 2020 (N=66) and 2025 (N=57).

3.2 Digitalization in the Chemical and Pharmaceutical Industry

Digitalization is a prerequisite for AI. Therefore, we first surveyed the status of digitalization in the chemical and pharmaceutical industries. Figure 4 shows responses to the question: „How relevant is digitalization in your company?“

Figure 4 Relevance of digitalization in the 2020 and 2025 surveys. Total numbers and breakdown by company size

The results show that digitalization was already highly relevant in 2020, and its relevance has increased since then. This reflects a clear awareness of digitalization’s importance and suggests that the digital competence of companies has grown. This trend may have been accelerated by the Covid-19 pandemic – the 2020 survey (February-June 2020) took place during the first lockdown – as well as the introduction of large language models (LLMs) since 2022. Breaking down these findings by company size provides further detail (Fig. 4, lower part). The increased importance of digitalization was observed across all size categories, with the exception of companies with 250-999 employees, where there was a slight decrease. In the 2025 survey, digitalization was not rated as „not relevant“ by any respondent, which highlights its growing significance. The relevance of digitalization has especially increased in small companies (<50 employees) and large corporations (1000+ employees). For companies with 50-999 employees, digitalization is somewhat less prominent but remains important. While digitalization’s importance decreased with smaller company size in 2020, the results from 2025 present a more nuanced picture. Nonetheless, it aligns with studies showing that SMEs are generally less advanced in digitalization than larger companies (Fraunhofer ISI and IW Consult, 2024), although those studies were not focused specifically on the chemical and pharmaceutical industry. Analysis of open-ended responses to „What concrete measures related to digitalization have already been implemented in your company?“ provided further insight (Tab. 1). The data in Table 1 should be interpreted carefully, since categorizing open-ended responses relies on subjective judgment. However, this overview offers an indication of the relevance of individual topics.

Table 1 Classification of open-ended responses to the question “What concrete measures related to digitalization have already been implemented in your company?”.

In 2020, most digitalization measures taken by companies focused on establishing IT infrastructure, improving internal and external communication, process and production automation, and data analytics. This is not surprising, given the chemical and pharmaceutical industries’ traditional focus on process optimization, which makes digitalization in production and automation a logical step. The emphasis on communication can also be attributed to the timing of the survey, conducted during the first Covid-19 lockdown, when virtual communication – both internally (among employees) and externally (with suppliers and customers) – became essential. The landscape changed in 2025. While IT systems and infrastructure, data management and analytics, and process digitization/automation remained important, communication was mentioned less frequently than in 2020. This likely reflects the normalization of virtual communication and reduced necessity compared to the lockdown period. Notably, “AI, Innovation & Research” emerged as one of the most prominent topics in 2025, whereas it was only sporadically mentioned in 2020. This is particularly striking because the questionnaire did not explicitly prompt respondents to discuss AI. When respondents rated predefined digitalization topics, an increase was observed across all areas (Fig. 5).

Figure 5 Assessment of relevance of digitalization topics in the 2020 and 2025 surveys.

All specified topics were rated at least moderately relevant – at least 40% of respondents assessed them as “very relevant” or “relevant” – and most topics reached high relevance, with over 70% of respondents giving these ratings in the chemical and pharmaceutical industries. Importantly, all topics have become more relevant since 2020 (dark green and green bars in Fig. 6). IT security and data protection ranked highest in relevance, likely reflecting the impact of European legislation such as the GDPR (DSGVO), in effect since 2018.

Topics directly or indirectly related to analytical AI also increased substantially in relevance. This is most notable in the rising importance of machine and deep learning between 2020 and 2025. These technologies require large data volumes stored in databases – on local servers or in the cloud – which is reflected in the growing relevance of these topics. The increased relevance of harmonizing IT systems, a prerequisite for efficiently creating companywide data lakes, is consistent with these trends.

Augmented and virtual reality were rated least relevant overall but held greater importance in large companies (1,000+ employees), with about 60% rating them as “very relevant” or “relevant” in 2020 and 80% in 2025; however, SMEs saw these topics as less important. Further research is needed to better understand this observation.

The obstacles to digitalization in chemical and pharmaceutical companies are similar in both 2020 and 2025 (data not shown; details are provided in the supplementary materials). The main challenge continues to be the complex change process associated with digitalization. This includes (a) a lack of mindset, where employees may not recognize the necessity for change, (b) a lack of strategy and coordination, suggesting that management does not always provide clear direction, and (c) a complex change process, even once the need for change is acknowledged by both employees and management. Additional obstacles identified include limited budgets and resources, as well as insufficient skills to facilitate and support the change process.

The complexity of the IT landscape is also frequently mentioned as a major obstacle. Harmonizing IT systems proves difficult, especially when companies use a variety of incompatible systems for functions such as accounting, HR, and CRM. When comparing the survey results from 2020 and 2025, it appears that implementation-oriented obstacles – such as lack of skills and the complexity of the change process – have become more significant, while foundational issues like lack of mindset and limited budgets or resources are less prominent. This may indicate that companies in the chemical and pharmaceutical industries are progressing towards the practical implementation of digitalization and are moving beyond preliminary debates.

3.3 Artificial Intelligence in the Chemical and Pharmaceutical Industry

Before exploring the use of AI in chemical and pharmaceutical companies, survey participants were asked, “What do you understand by artificial intelligence (AI)?” This question aimed to assess whether respondents had a thorough understanding of the topic or only a superficial view. The results are presented in Table 2.

Table 2 Classification of open-ended responses to the question “What do you understand by artificial intelligence (AI)?”.

It is evident that most survey participants had a wellinformed and nuanced understanding of AI in both the 2020 and 2025 surveys. The most prominent responses in 2020 related to key areas of AI application, such as “Data analysis, Pattern recognition & prediction” and “Process Control & Decision Support.” While data analysis remained the leading answer in 2025, process control and decision support were mentioned less frequently. Notably, the category “Creation of new content” appeared only in the 2025 survey, likely due to the growing presence of generative AI, such as LLM-based systems. Similarly, a larger proportion of responses in 2025 focused on specific software or tools, reflecting greater familiarity and hands-on experience with AI, as generative tools have become more widely used both professionally and privately. The category “Self-learning and evolving systems,” though not an incorrect definition, is rather vague, and its relative importance declined from 2020 to 2025 as AI became more mainstream. However, some unclear or incorrect notions of AI persist, as indicated by this category in both surveys. Overall, the answers confirm that survey participants generally have a sound understanding of AI, which supports the validity of the study’s results.

When asked whether AI is used in their company, participants reported a clear shift towards more intensive AI adoption in 2025 compared to 2020 (see Fig. 6).

Figure 6 Visualization of results to the question “Is AI used in your company?”, 2020 and 2025. Total numbers and breakdown by company size.

In 2025, most companies either already use AI or plan to do so in the future. This marks a stark contrast to 2020, when only about one third of companies had implemented AI and more than half of survey participants indicated that AI usage was not even planned within their organizations. While some bias cannot be ruled out – such as different awareness levels among respondents depending on their position (e.g., an R&D employee may not know of management-level AI initiatives) – the significant increase in positive responses in 2025 compared to 2020 demonstrates that AI has firmly established itself in the chemical industry.

This upward trend in AI adoption since 2020 is reflected across different company sizes, although the situation is more nuanced. AI uptake is particularly high among large companies (1,000+ employees) and small companies (<50 employees), while companies in the 50-999 employee range appear to lag behind in terms of actual implementation. Despite their plans to use AI in the future, these mid-sized companies have not adopted AI to the same extent yet.

Survey participants were then asked, “How exactly is AI used in your company?” (data not shown; details are provided in the supplementary materials). In 2020, AI initiatives were primarily limited to individual pilot projects or focused on automating repetitive tasks, especially in the areas of data analysis and forecasting. Some applications in research and development were also mentioned. By 2025, the landscape had evolved significantly: generative AI became a major driver of adoption within chemical and pharmaceutical companies.

Solutions such as ChatGPT, Copilot, company-specific GPTs, assistants, and chatbots were either firmly integrated into daily operations or actively tested and implemented. Alongside its “traditional” role in data analysis, AI is now increasingly regarded as a tool for supporting work and expanding communication – for example, in marketing. We complemented this analysis by asking, “How relevant is the use of AI along the value chain in your company?” and specifying individual steps within the corporate value chain. The results are presented in Figure 7.

Figure 7 Visualization of results to the question “How relevant is the use of AI along the value chain in your company?”, 2020 and 2025.

It is evident that AI is relevant to all the mentioned steps in the value chain, with at least 50% of survey participants in both 2020 and 2025 rating all steps as “very relevant” or “relevant.” The greatest increase in relevance was observed in Research & Development (+25 percentage points for “very relevant” or “relevant”) and Customer Service (+29 percentage points). These two areas are where generative AI is expected to have the highest impact, which also aligns well with the results shown in Table 4. For all other value Solutions such as ChatGPT, Copilot, company-specific GPTs, assistants, and chatbots were either firmly integrated into daily operations or actively tested and implemented. Alongside its “traditional” role in data analysis, AI is now increasingly regarded as a tool for supporting work and expanding communication – for example, in marketing. We complemented this analysis by asking, “How relevant is the use of AI along the value chain in your company?” and specifying individual steps within the corporate value chain. The results are presented in Figure 7. chain steps, there is a slight overall increase in the importance of AI, although the 2025 results are similar to those from 2020. This may be explained by the fact that most of these steps are related to the direct material flow within the company and are thus more closely tied to the production process. In these areas, analytical AI is expected to play a larger role than generative AI. It is likely that analytical AI was already widely adopted in the chemical and pharmaceutical industry by 2020, which could explain the lack of major developments in these areas over the last five years.

We then asked survey participants, based on the current use of AI, “How relevant are the AI topics listed below for your company now compared to the future?” The topics included a range of AI-related areas such as “predictive analytics,” “intelligent automation,” and “knowledge management.” In the survey, “future” referred to the year 2025 for the 2020 survey and the year 2030 for the 2025 survey, which enabled us to compare the 2020 forecast with the actual results from the 2025 survey. The results are shown in Figure 8.

Figure 8 Visualization of results to the “How relevant are the AI topics listed below for your company now compared to the future?”, 2020 and 2025. The dark green bars correspond to current values in 2020 (bar on the left) and 2025 (bar on the right). The light green bars with the dashed line correspond to the forecast of the 2020 survey (bar on the left) and the forecast of the 2025 survey (bar on the right).

The relevance of all AI-related topics listed in the questionnaire increased between 2020 and 2025. The largest increases were observed for topics related to or influenced by generative AI, such as voice assistants/chatbots, intelligent assistance systems, and knowledge management. For voice assistants and chatbots specifically, participants in the 2020 survey underestimated the actual relevance of this topic by 18 percentage points. However, participants in the 2020 survey generally overestimated the relevance of AI for most other topics, particularly those related to material flow, production, or analytical AI with a focus on well-structured data (including intelligent automation, optimized resource management, predictive analytics, and quality control). This may reflect the inherent challenges in further optimizing production processes, where AI can certainly assist, but is often just one tool among several. We further observe that participants in the 2025 survey expect the importance of most of these topics to increase markedly by 2030. The estimated increases for most topics are similar in magnitude to those predicted for the period 2020-2025. Based on the comparison between the 2025 forecast and actual data, we speculate that the actual increase by 2030 may not fully match these expectations.

To gain a better understanding of the obstacles to further AI implementation in companies, we asked survey participants the open-ended question, “What obstacles do you see for the use of AI in your company?” (data not shown; details are provided in the supplementary materials). Analysis of the open-ended responses indicates that all categories previously identified as obstacles to digitalization were also considered barriers to AI adoption. Six additional categories specific to AI were mentioned: (1) IT security/ data protection, (2) lack of trust/control, (3) insufficient digitalization, (4) lack of data, (5) missing knowledge about applications, and (6) not in line with company philosophy. Interestingly, the latter two categories were absent from the 2025 survey results, which may be attributed to the rise of generative AI since 2022. This shift appears to have prompted more intensive engagement with AI within companies, leading to sufficient knowledge regarding its use (at least for generative AI) and a changing perception – AI is no longer seen as an “impurity”, to use a chemical term, in company philosophy, though it has certainly not yet become a core part of every company’s identity. The most prominent obstacle reported by survey participants in 2025 was IT security and data protection. This points to an increased sensitivity around balancing the need to protect confidential information with the large data requirements of AI applications. This heightened awareness is further reflected in the emergence of the category „lack of trust/control“ in 2025, which was not mentioned in 2020.

We complemented this analysis by asking the question, „How relevant are the following obstacles for the use of AI in your company?“ and specifying different topics we anticipated would be relevant in this context. The results are presented in Figure 9.

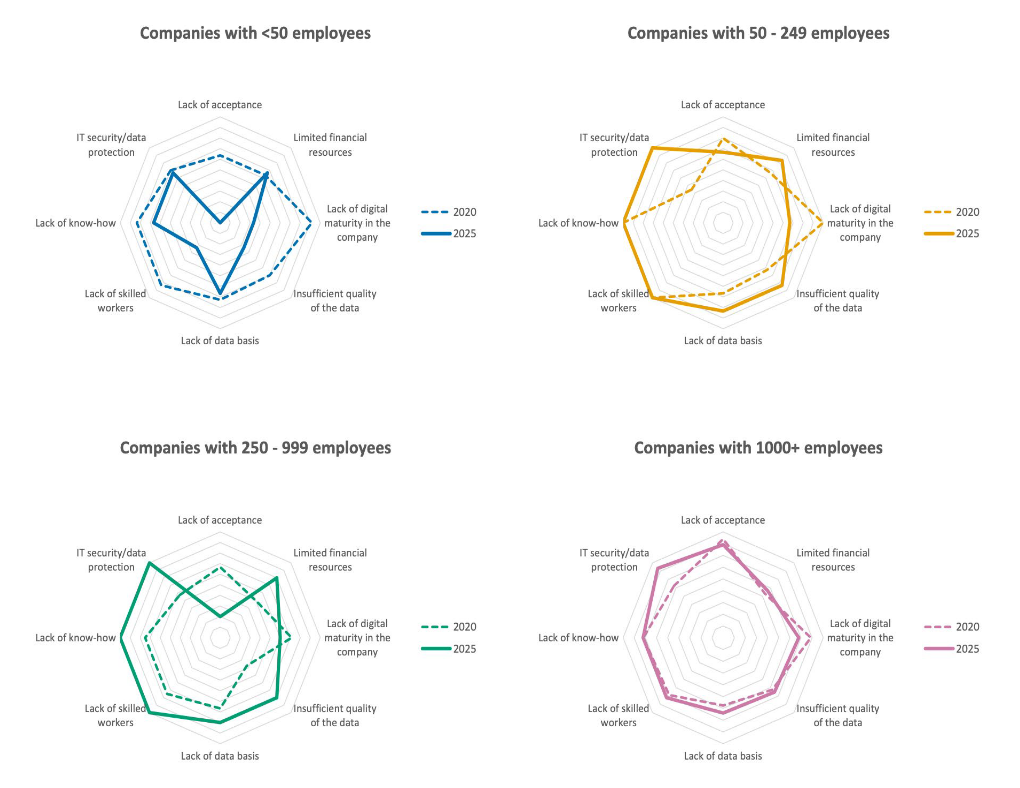

Figure 9 Visualization of results to the question “How relevant are the following obstacles for the use of AI in your company?”, 2020 and 2025.

According to survey participants, all of the specified topics are obstacles for the further expansion of AI within companies. IT security and data protection was identified as the most significant obstacle, with 88% of respondents stating it was very relevant or relevant. Notably, the importance of this obstacle has increased by 28 percentage points since 2020. Other categories, while still important, have generally remained at a similar level or decreased slightly when considering the combined “very relevant” and “relevant” responses. Most interestingly, there was a modest decrease in the obstacles “lack of acceptance” (from 77% in 2020 to 64% in 2025) and “lack of digital maturity in the company” (from 84% in 2020 to 65% in 2025). This aligns well with the results shown in Table 1 and the observation that companies have increased their digitalization efforts since 2020, likely influenced by the Covid-19 pandemic as well as the gradual adoption of generative AI.

When examining the obstacles by company size (see Fig. 10), we observe that companies with fewer than 50 employees considered most obstacles less significant in 2025 compared to 2020. For companies with more than 1,000 employees, the average assessment of individual obstacles remained largely unchanged between 2020 and 2025, with a slight increase reported for “IT security/data protection” and a slight decrease for “lack of digital maturity in the company.”

Figure 10 Share of answers with “very relevant” and “relevant” of total number of answers to the question “How relevant are the following obstacles for the use of AI in your company?” for different company sizes, 2020 (dashed line) and 2025 (solid line)

Companies with 50-999 employees considered most obstacles to be more important in 2025 compared to 2020, particularly regarding financial resources, lack of skilled workers/know-how, and a lack of sufficiently high-quality data. They also reported that IT security/data protection had increased in importance. Conversely, lack of acceptance was less of an obstacle in 2025 than in 2020. Comparing the results between company sizes shows that the pattern in 2020 was quite similar across all companies (see Fig. 11).

Although there are some deviations from the average, the overall pattern remains comparable between different company sizes. We believe this may be due to the fact that, in 2020, AI applications were primarily focused on process optimization, process automation, and data analysis – activities that are central to chemical and pharmaceutical companies. It is therefore not surprising to see a similar assessment across companies of different sizes during that period.

Figure 11 Comparison of “obstacle pattern” between different company sizes from survey 2020 and 2025.

When looking at the results of the 2025 survey, we observe a greater variation in the assessment of obstacles between companies of different sizes. Companies with fewer than 50 employees and those with more than 1,000 employees reported a comparable or even lower relevance for most obstacles. In contrast, companies with 50-999 employees appear to face greater challenges in adopting AI.

4 Discussion

4.1 Evolution of Digitalization and AI Adoption

Results show a steady rise in the use and importance of digital technologies. By 2025, 91% of companies rated digitalization as “relevant” or “very relevant”, up from 75% in 2020. This reflects broader industry trends catalyzed by the Covid-19 pandemic and improved digital infrastructure. AI adoption also increased markedly, from 34% to 76%, indicating a shift from pilot projects in analytics and automation to broad integration of generative AI tools. AI is now seen not only as a tool for data analysis, but increasingly as a facilitator of everyday tasks and communication. These findings match previous reports of widespread AI use in the sector (Chiang, 2022; Patel, 2022).

4.2 Trajectory and Momentum: Short-term Overestimation and Long-term Potential

The survey reveals that respondents in 2020 overestimated the short-term operational impact of several AI topics for 2025. This pattern is consistent with Amara’s Law: “We tend to overestimate the effect of a technology in the short run and underestimate the effect in the long run” (Amara, 2007). The underlying tendency for experts to misjudge technology adoption rates is well documented (Rahal et al., 2021; Naudé, 2021; Bonaccorsi et al., 2020) and highlights persistent cognitive biases in technology foresight. Early predictions about AI relevance in areas like predictive analytics, automation, resource, and knowledge management were only partially realized; meanwhile, disruptive generative AI applications, barely considered in 2020, have become central by 2025. These findings suggest that current forecasts for 2030 may also be overestimated, underscoring the need for ongoing, data-driven monitoring of technological trends.

4.3 Sectoral Differences and the “Mittelstand Challenge”

A key finding is the heterogeneity of digital and AI adoption by company size. Large enterprises and some small firms (<50 employees) show advanced digitalization and AI use, while medium-sized companies (“Mittelstand”, 50-999 employees) lag behind and face more obstacles, including limited financial resources, lack of qualified staff, data quality issues, and technical challenges like IT security and system integration. This aligns with previous research (Fraunhofer ISI and IW Consult, 2024). The persistence – and in some cases intensification – of these challenges suggests that the “Mittelstand”, a key part of Germany’s industrial base, risks structural disadvantages in digital transformation. Without action, this divergence may reduce overall sector competitiveness and innovation. Possible causes include budget constraints, shortage of skilled workers, and lower strategic prioritization of digital initiatives compared to larger corporations. If these hypotheses hold, our findings highlight the need for targeted support measures, best-practice sharing, and further research to develop tailored solutions for medium-sized companies.

4.4 Barriers to Further Implementation: Technical, Organizational, and Cultural Factors

The landscape of obstacles has shifted: while earlier barriers focused on mindset, budgets, and digital literacy, by 2025 technical and organizational issues predominate. IT security and data protection are now the leading concerns (cited by 88% of respondents), reflecting both the complexity and data demands of advanced AI, and evolving regulations such as DSGVO. Reluctance caused by lack of acceptance or digital maturity is decreasing. Organizations seem to be more ready to embrace digital change.

4.5 Implications and Future Directions

The sector is in transition: digitalization and AI have shifted from isolated experiments to integrated, business-critical roles, with generative AI – especially large language models and assistants – acting as a major catalyst from 2020 to 2025, notably in R&D and customer engagement. Despite progress, major barriers persist, particularly for mediumsized enterprises, and expert forecasts remain vulnerable to short-term overoptimism.

Ongoing empirical research is needed to track these trends and challenges. Enhanced collaboration among industry, academia, and policymakers is crucial to drive inclusive digital transformation. Given the importance of SMEs in the sector, we hope our results will prompt targeted support, upskilling, and practical solutions for overcoming obstacles. Future studies – including a potential follow-up in 2030 – will be important to validate forecasts and deepen understanding of the ongoing technological change.

5 References

Ananikov, V. P. (2024): Top 20 influential AI-based technologies in chemistry. Artif. Intell. Chem., 2, 100075. https://doi.org/10.1016/j.aichem.2024.100075

Baum, Z.J.; Yu, X.; Ayala, P.Y.; Zhao, Y.; Watkins, S.P.; Zhou, Q. (2021): Artificial Intelligence in Chemistry: Current Trends and Future Directions. J. Chem. Inf. Model., 61, 3197-3212. Bonaccorsi, A., Apreda, R., and Fantoni, G. (2020): Expert biases in technology foresight. Why they are a problem and how to mitigate them. Technol. Forecast. Soc. Change, 151, 119855.

Chiang, L.H.; Braun, B.; Wang, Z.; Castillo, I. (2022): Towards artificial intelligence at scale in the chemical industry. AIChE J., 68, e17644. https://doi.org/10.1002/aic.17644

Dreiling, A. (2025): The Impact of Artificial Intelligence on Innovation Speed in Startups. J. Bus. Chem., 22(2), 128-136.

DSGVO, Verordnung (EU) 2016/679 des Europäischen Parlaments und des Rates vom 27. April 2016 zum Schutz natürlicher Personen bei der Verarbeitung personenbezogener Daten, zum freien Datenverkehr und zur Aufhebung der Richtlinie 95/46/EG (DatenschutzGrundverordnung), available at: https://eur-lex.europa.eu/ eli/reg/2016/679/oj/deu?locale=de, accessed August 14th, 2025.

Fraunhofer ISI, IW Consult (2024), Zukünftige Unterstützungsbedarfe des Mittelstandes in der digitalen Transformation, available at: https://projekttraeger. dlr.de/sites/default/files/2024-07/documents/ BedarfsanalyseZuk3%C3%BCnftigeUnterst%C3%BCtzung sBedarfeMittelstand.pdf, accessed August 14th, 2025.

Henstock, P. V. (2019): Artificial Intelligence for Pharma: Time for Internal Investment. Trends Pharmacol. Sci., 40(8), 543-546.

Konrad, A. (2024): How artificial intelligence can be used in the chemical industry. J. Bus. Chem., 21(2), 67-70.

Kulkov, I. (2021): The role of artificial intelligence in business transformation: A case of pharmaceutical companies. Technol. Soc., 66, 101629. https://doi.org/10.1016/j.techsoc.2021.101629

Laska, M.; Karwala, I. (2023): Artificial Intelligence in the Chemical Industry – Risks and Opportunities. Sci. J. Sil. Univ. Technol., 172, 403-416.

Maharjan, R.; Lee, J.C.; Lee, K.; Han, H.-K.; Kim, K.H.; Jeong, S.H. (2023): Recent trends and perspectives of artificial intelligence‑based machine learning from discovery to manufacturing in biopharmaceutical industry. J. Pharm. Investig., 53, 803-826. https://doi.org/10.1007/s40005-023- 00637-8

Mak, K.-K.; Pichika, M.R. (2018): Artificial intelligence in drug development: present status and future prospects. Drug Discov. Today, 24(3), 773-780.

Mowbray, M.; Vallerio, M.; Perez-Galvan, C.; Zhang, D.; Del Rio Chanona, A.; Navarro-Brull, F.J. (2022): Industrial data science – a review of machine learning applications for chemical and process industries. React. Chem. Eng., 7, 1471-1509. DOI: 10.1039/d1re00541c

Naudé, W. (2021): Artificial intelligence: neither Utopian nor apocalyptic impacts soon. Econ. Innov. New Technol., 30(1), 1-23.

Patel, V.; Shah, M. (2022): Artificial intelligence and machine learning in drug discovery and development. Intell. Med., 2, 134-140. https://doi.org/10.1016/j.imed.2021.10.001

Rahal, C., Verhagen, M., and Kirk, D. (2021): Machine Learning in the Social Sciences: Amara‘s Law and an inclination across Foster‘s S-Curve?, available at: https://www.researchgate. net/publication/ 3355016055_Machine_Learning_in_the_Social_Sciences_ Amara‘s_Law_and_an_inclination_across_Forster‘s_SCurveww, accessed August 14th, 2025.

Toniato, A.; Schilter, O.; Laino, T. (2023): The Role of AI in Driving the Sustainability of the Chemical Industry. CHIMIA, 77(3), 144-149.

Ulbrich, M.; Hammann, J.; Sommerhuber, P. (2021): From disruption to maturity: The evolution of digital R&D in chemicals. Available at: https://www.accenture.com/ content/dam/accenture/final/a-com-migration/r3-3/pdf/ pdf-158/accenture-digital-research-and-development-chemicals.pdf, accessed August 15th, 2025.

VCI (2022): Chemiewirtschaft in Zahlen 2022, Verband der Chemischen Industrie e.V. VCI (2024): Chemiewirtschaft in Zahlen 2024, Verband der Chemischen Industrie e.V.

Vora, L.K.; Gholap, A.D.; Jetha, K.; Thakur, R.R.S; Solanki, H.K.; Chavda, V.P. (2023): Artificial Intelligence in Pharmaceutical Technology and Drug Delivery Design. Pharmaceutics, 15, 1916. https://doi.org/10.3390/pharmaceutics15071916

Walsh, P.; Ringnalda, L. (2021): Innovation in regulatory – Accelerating drugs to market with AI. Available at: https:// www.accenture.com/content/dam/accenture/final/a-commigration/pdf/pdf-165/accenture-innovation-in-regulatory. pdf, accessed August 15th, 2025.

Womack, D.; Krishnan, V.; Lin, S. (2020): Optimizing the chemicals value chain with AI. AI champions are creating more business value and outperforming their peers. Available at: https://www.ibm.com/downloads/documents/ us-en/10a99803f92fdaa2, accessed August 15th, 2025.

Supplementary Material

This section contains detailed information about three openended questions from the 2020 and 2025 surveys that are not included in the main article:

1. “What major obstacles do you see in your company with regard to digitalization?”

2. “How exactly is AI used in your company?”

3. “What obstacles do you see for the use of AI in your company?”

This information complements the data in the main article and the interested reader can find additional information on the mentioned subjects.

Table S1 Classification of open-ended responses to the question “What major obstacles do you see in your company with regard to digitalization?”.

Table S2 Classification of open-ended responses to the question “How exactly is AI used in your company?”

Table S3 Classification of open-ended responses to the question “What obstacles do you see for the use of AI in your company?”.