After COVID, What’s Next for Pharma Supply Chains?

If the world’s dependence on pharmaceutical technology wasn’t already obvious, COVID-19 brought a dramatic reminder as companies like Moderna, Pfizer, BioNTech, and Johnson & Johnson delivered needed vaccines. Now, pharma executives are seeing the success tempered by reality as significant new risks challenge the global supply chain and the industry.

While recent, pandemic-induced disruptions have focused attention on global supply chain vulnerabilities for pharmaceuticals and other industries, the challenges facing pharmaceutical companies are broader and deeper than these. The reason is a convergence of complications, including substantial environment, sustainability and governance (ESG) issues and a rising wave of government scrutiny, that are landing squarely on the sector’s supply chain vulnerabilities.

The impact is real and already visible. COVID-19-related breakdowns have affected pharmaceutical companies, with manufacturing interruptions that have caused suspension of clinical drug trials in some cases and even delayed introductions of new key drugs. Key concerns are blocked supplies of needed medicines, and, as a second order, foregone revenue.

These kinds of pressures have refocused attention on potential vulnerabilities in healthcare’s global supply chains and with it a kind of economic nationalism that is pushing manufacturers to bring their far-flung factories, processes, and jobs back onshore, or establish a presence in certain markets.

The impact becomes even more profound when set against climate and sustainability concerns that are putting real pressure on pharmaceuticals and biotechs to decarbonize their supply chains.

To safeguard their achievements and remain competitive, pharmaceutical and biotech organizations must protect the ongoing viability of product supply networks against the growing risks by increasing resiliency and reducing their carbon footprints.

Have pharmaceuticals overcommitted to a global model?

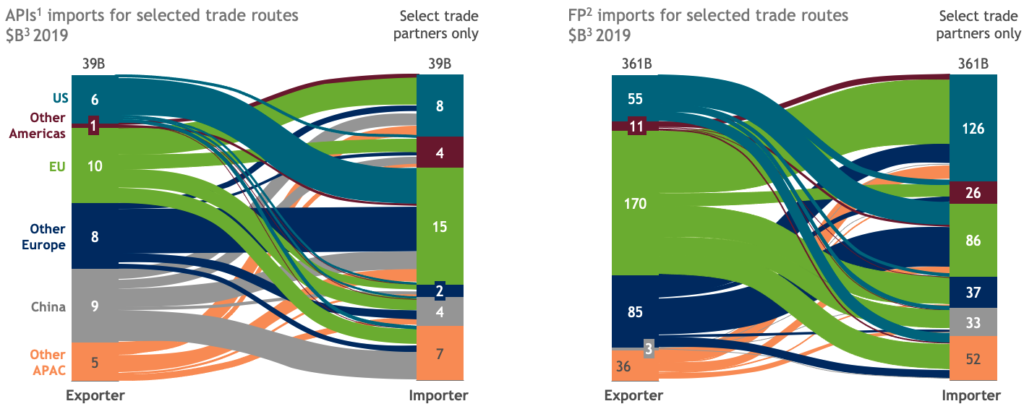

Pushed by costs, talent shortages, and the growing availability of overseas contract manufacturing organizations (CMOs), companies in recent years have embraced biopharma supply chains that rely on suppliers in all parts of the world. The resulting network is a highly interconnected global supplychain,with significant dependency on certain countries — not only China, but Eastern Europe, and others — now established for active pharmaceutical ingredients (APIs), while Europe has become the major exporter of finished products (Figure 1).

The complexity of this growing network brings management challenges: international trade issues, increasing margin and cost pressures, demand uncertainty, high volatility, and increasingly complex technologies to manage, all in a highly regulated environment.

What were seen as savvy outsourcing moves that increased sourcing flexibility and lowered costs are now cause for concern as companies are witnessing the greater risks of extreme globalization. This naturally differs from company to company. Generics players, for example, typically have more exposure to lower-cost country sourcing and production than innovative pharma companies.

Figure 1 Highly globalized biopharma supply chains rely heavily on internatiobal trade (IHS Markit; Global Trade Atlas; BCG analysis).

A pre-pandemic movement in the United States and Europe to encourage companies to shift supply chains back onshore has become stronger in recent months from governments that see increased urgency to secure supplies of essential medicines and reduce dependence on China. The result is increasing protectionist sentiments and growing pressure to localize supply chain footprints.

While specific legislation and regulations are evolving with the changing environment, the primary concern for pharmaceutical and biotech companies today is governments that are imposing or considering various carrot-and-stick policies that apply indirect pressure, such as procurement bans, trade restrictions, and access incentives.

In the US, the Biden Administration and lawmakers are developing policies to strengthen domestic manufacturing in several critical industries. In 2021, Biden signed an executive order to review supply chains to reduce foreign dependence on key technologies, including pharmaceuticals (Tankersleyand Swanson, 2021).

Likewise, EU leaders have expressed similar concern in the wake of the pandemic and subsequent supply chain disruption. “The crisis has shown that we must continue to produce in our country and on our continent“, French President Emmanuel Macron said in June 2020, announcing measures aimed at relocating pharmaceutical factories to France (Teller Report, 2020).

1 Active pharmaceutical ingredient; international harmonized system (IHS) codes 2924, 2930, 2931, 2936, 2937, 2941.

2 Finished Product; codes 3002, 3003, 3004, 3006.

3 Figures represent trade volumes between selected geographies only calculated based on reported imports for countries. Excludes intraregion trade (e.g. within EU).

Increasing focus on supply chain sustainability

In the wake of the pandemic, the climate discussion that has been brewing for a decade or so is taking on sudden urgency, with increasing stakeholder pressure on companies to take action on supply chain decarbonization.

Although pharmaceuticals are not commonly grouped, in the public’s perception, among heavy-polluting smokestack industries, environmental watchdogs are calling them out, like other chemicals companies, as a significant contributor to global carbon emissions. A study by Belkhir and Elmeligi(2019) published in the Journal of Cleaner Production found that the pharmaceutical industry’s carbon emission intensity is 55% higher than the automotive industry’s. The key point is the increased attention to the pharmaceutical industry’s carbon footprint. Companies’ emission levels range widely, as they are driven by company size, technology, and the overall product supply set up. For example, pharma companies that are producing mainly small-molecule drugs (based on active pharmaceutical ingredients that are made via chemical synthesis) have, other things being equal, higher emission levels than biologics.

Investors are taking it seriously. BlackRock, Inc., the world’s largest asset management company, has set the ambitious goal of having all of the assets it manages (over $10 trillion worth) reach net zero emissions by 2050. It punished 53 companies in 2020 for climate inaction, voting at annual meetings against the re-election of directors. Chief executive Larry Fink reaffirmed Wall Street’s changing attitudes in his annual letter to CEOs in January 2022, explaining that companies must “focus on sustainability not because we’re environmentalists, but because we are capitalists andfiduciaries to our clients.” (Fink, 2022).

“Most stakeholders – from shareholders, to employees, to customers, to communities, and regulators – now expect companies to play a role in decarbonizing the global economy,” Fink wrote.

Regulators and the public have sustainability in their sights as well. The EU proposed tougher 2030 emissions targets, with potential impacts for chemicals and pharmaceutical manufacturers, (European Commission, 2021) and polls show growing numbers of consumers are demanding positive change from the companies they buy from (Nielsen IQ, 2019).

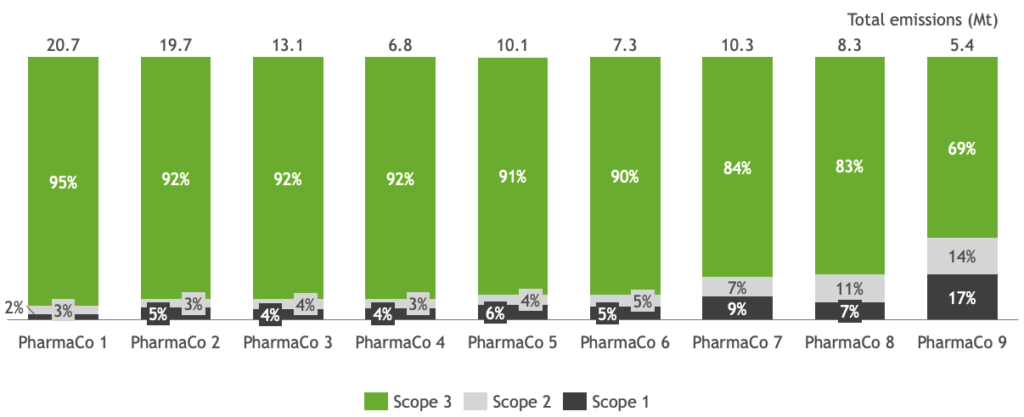

And the goals will become harder, not easier, to achieve, as more companies attempt to address Scope 3 carbon emissions. According to the Greenhouse Gas (GHG) Corporate Protocol, part of the global carbon emissions framework on climate change, Scope 1 refers to emissions created directly by the organization; Scope 2 emissions are those created by power companies and utilities that supply a company’s energy. Scope 3 emissions designate pollution created by an organization’s extended network of suppliers and customers. Because the organization doesn’t directly control these emissions, identifying, measuring, and reducing them is much more difficult. But to environmentalists— and, increasingly, investment leaders like BlackRock—it is becoming an important area of focus because the vast majority of emissions (percentages in the 80s and 90s are typical) fall under Scope 3 (Figure 2; BCG analysis4). While the GHG Protocol requires companies to identify and report Scope 1 and 2 emissions, more companies are trying to identify Scope 3 emissions as part of their carbon reduction planning.

Figure 2 Majority of emissions in pharma fall under Scope 3 (Company Annual Reports; BCG analysis).

Companies are clearly taking the issue to heart as well— and that, in turn, puts pressure on peers that lag behind. Corporate commitments are growing significantly. Over 2,000 companies, across industries, have pledged to meet science-based targets, as of the end of 2021, roughly double compared to a year earlier (Eckart et al., 2022).

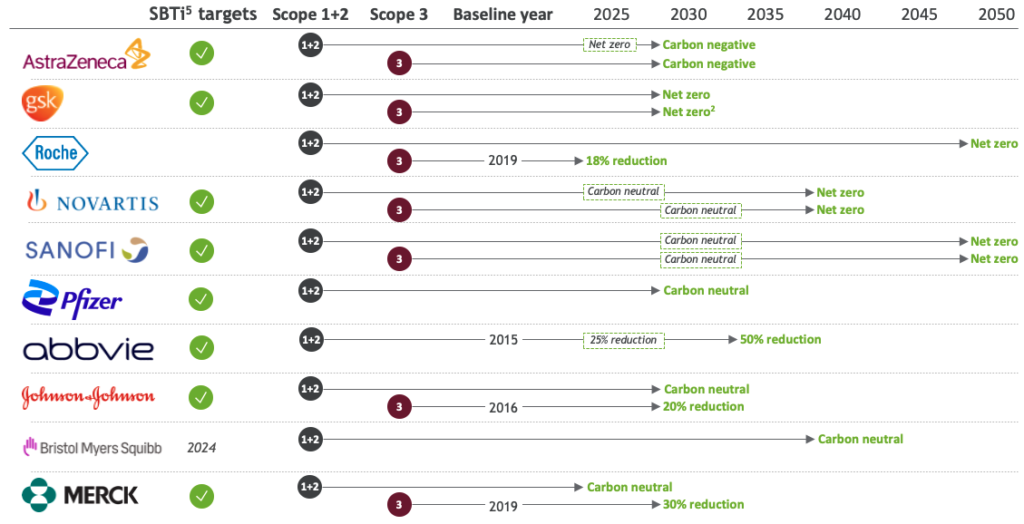

Several pharmaceutical companies (e.g., Abbvie, AstraZeneca, BMS, GSK, Johnson & Johnson, Merck, Novartis and others) have committed to science-based, carbon-neutral, and net-zero targets, for both Scope 1-2 emissions (targets ranging from 2025 to 2040) and also Scope 3 emissions (2030 to 2050), see Figure 3.

Figure 3 PharmaCos set ambitious targets, including Scope 3. Net zero emissions across full value chain for Biopharma (AstraZeneca, 2025; GSK, 2030; Roche, 2050; Novartis, 2040; Sanofi, 2050; BCG analysis).

Figure 3 PharmaCos set ambitious targets, including Scope 3. Net zero emissions across full value chain for Biopharma (AstraZeneca, 2025; GSK, 2030; Roche, 2050; Novartis, 2040; Sanofi, 2050; BCG analysis).

A study by My Green Lab (2021) concludes that just 4% of the world’s largest publicly-traded pharmaceutical and biotech companies have adopted climate commitments that align with the UN’s Intergovernmental Panel on Climate Change (IPCC) to limit global warming to 1.5 °C.

4 BCG analysis refers to internal, non-disclosed analyses based on client data and company information.

5 Science Based Targets initiative. This is a list of representative companies that have publicly announced SBTi targets (approved and committed to be approved within 24 months). The list is non-exhaustive by nature and does not mean that companies that are not listed here do not have set targets.

The way forward for pharmaceutical supply chains

Pharmaceutical companies must take action to cope with increasing threats from political and natural risks as well as global climate requirements, and network resiliency and sustainability must be top priorities. If there is a silver lining in this, it is that the global supply chain is a vector for numerous risks, and companies may be able to address multiple threats—climate, government pressure, business resiliency—through improvements in this one critical area of the business.

To be sure, it is a very complicated task, and it requires an end-to-end view along the whole supply chain. Given the range of disruptions and company product supply setups, prioritized and tailored strategies are required—there is no one-size-fits-all solution.

An appropriate, strategic approach will entail identifying areas with the highest risks, evaluating risk tolerances, establishing redundancies, installing risk mitigation strategies, and actively engaging suppliers and customers regarding carbon emissions.

Companies must begin with appropriate assessments of supply chain risks, for the improvement of resiliency, and of emissions challenges, to enhance sustainability.

Next, companies should view steps to build resilience and sustainability through a double lens of a) impetus to change, and b) ease of adjustment. Impetus to change requires an assessment of the magnitude of supply chain risks, how essential a product is for patients as well as company revenue, and current and future regulatory requirements. The other requirement, ease of adjustment, demands an understanding of the comparative difficulty involved in adjusting the current product supply setup. This includes numerous inputs, such as technical feasibility, capabilities and skills, regulatory factors, costs, and interdependencies and redundancies in the production network.

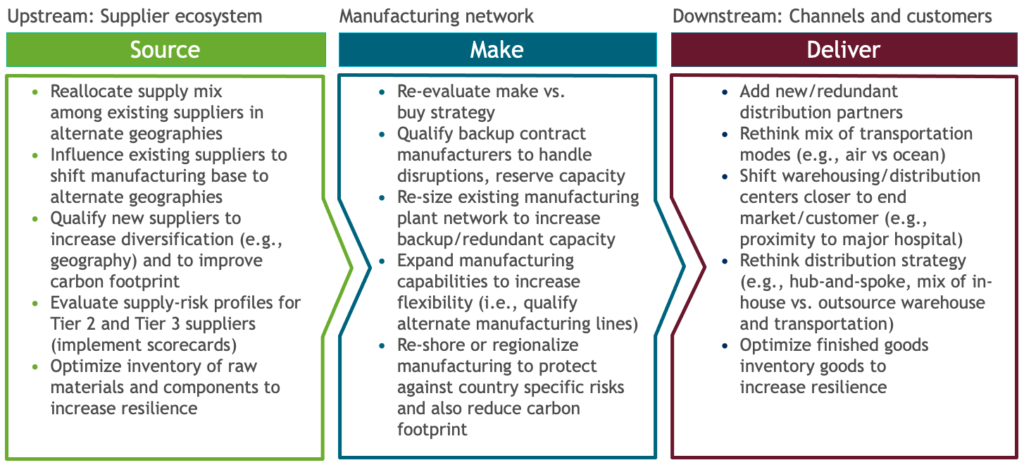

While each organization’s approach will depend on its particular circumstances, companies have a range of levers they can use. To improve resiliency, options range from reevaluating the make-versus-buy strategy to reshoring part of the manufacturing footprint to protect against country risks (Figure 4). To address Scope 3 emissions, companies can work with existing API suppliers or qualify new suppliers to shift the manufacturing base to improve overall carbon emissions. In downstream areas they can reconsider the distribution strategy, such as the mix of transportation modes or moving distribution centers closer to end markets.

Figure 4 Levers across the supply chain (BCG analysis).

The time horizons for different steps vary widely. For example, we see more and more companies discussing a region-to-region, product supply-network approach. Changing supply routes, building new sites, and the like, takes time—years rather than months, and might not be economically feasible for every product given the regulatory requirements. Fundamentally adjusting global supply networks will be a multi-year journey, and an important part of a coherent strategy to promote a resilient and sustainable product supply network.

References

Abbvie (2021): Celebrating Our Employees, available at https://investors.abbvie.com/static-files/91cf9d6a-8e6f- 4059-9575-eda83b7e4623, accessed 13 April 2022.

Astra Zeneca (2021): What science can do available at https://www.astrazeneca.com/content/dam/az/Investor_ Relations/annual-report-2021/pdf/AstraZeneca_AR_2021. pdf, accessed 18 June 2022.

Belkhir, L., Elmeligi, A. (2019) Carbon footprint of the global pharmaceutical industry and relative impact of its major players, Journal of Cleaner Production, 214, pp. 185-194.

Bristol Myers Squibb (2021): 2021 Annual Report, available at https://annual-report.bms.com/assets/bms-ar/ documents/2021-annual-report.pdf, accessed 18 June 2022.

Eckart, J., Gawel, A., Burchardt J., Fagan S., Frédeau, M., Herhold, P., Inovaara, S., Lesser, R., Pieper, C., Salomon, N. (2022): Winning the Race to Net Zero: The CEO Guide to Climate Advantage, World Economic Forum, Geneva, Switzerland, pp. 2-36.

European Commission (2021): ‘Fit for 55‘: delivering the EU‘s 2030 Climate Target on the way to climate neutrality, available at https://eur-lex.europa.eu/legal-content/EN/ TXT/?uri=CELEX:52021DC0550, accessed 13 April 2022.

Fink, L (2022): Larry Fink’s 2022 letter to CEOs, The power of capitalism, available at https://www.blackrock.com/ corporate/investor-relations/larry-fink-ceo-letter, accessed 13 April 2022.

GlaxoSmithKline (2021): Annual Report 2021, available at https://www.gsk.com/media/7462/annual-report-2021.pdf, accessed 13 April 2022.

IHS Markit: Global Trade Atlas, available at https://ihsmarkit. com/products/global-trade-atlas-data-lake.html, accessed 18 June 2022.

Johnson & Johnson (2021): 2021 Annual Report, available at https://www.investor.jnj.com/annual-meeting- materials/2021-annual-report, accessed 13 April 2022.

Merck (2021): Form 10-K, available at https://s21.q4cdn. com/488056881/files/doc_financials/2021/q4/Form-10-K- 2021-Final.pdf, accessed 13 April 2022.

My Green Lab (2021): New Study Finds That Just 4%of Biotech & Pharma Companies Currently on Track to Meet Paris 2030 Climate Goals, available at https://www. mygreenlab.org/blog-beaker/my-green-lab-measures- carbon-impact-of-biotech-and-pharma, accessed 13 April 2022.

Nielsen IQ (2019): A ‘natural’ rise in sustainability around the world, available at https://nielseniq.com/global/en/ insights/analysis/2019/a-natural-rise-in-sustainability- around-the-world/, accessed 13 April 2022.

Novartis (2021): Annual Report 2021, available at https:// www.novartis.com/sites/novartis_com/files/novartis- annual-report-2021.pdf, accessed 13 April 2022.

Pfizer (2021): Environmental, Social & Governance Report, available at https://s28.q4cdn.com/781576035/files/ doc_financials/2021/ar/Pfizer_ESG_Final-(2).pdf, accessed 13 April 2022.

Roche (2021): Annual Report 2021, available at https:// www.roche.com/investors/reports/#0c02f4c4-daa1-48f6- a506-c75a59b1a4dc, accessed 13 April 2022.

Sanofi (2021): Corporate Social Responsibility 2021, Chapter 4 of 2021 Document d’enregistrement universel, available at https://www.sanofi.com/-/media/Project/ One-Sanofi-Web/Websites/Global/Sanofi-COM/ Home/en/our-responsibility/docs/documents-center/ brochures/Declaration-of-Extra-Financial-Performance. df?la=en&hash=463A22969391C0FCAC98E2398C80DD0C, accessed 13 April 2022.

Tankersley, J; Swanson, A (2021): Amid Shortfalls, Biden Signs Executive Order to Bolster Critical Supply Chains, available at https://www.nytimes.com/2021/02/24/ business/biden-supply-chain-executive-order.html, accessed 13 April 2022.

Teller Report (2020): Emmanuel Macron announces measures to relocate factories in France, available at https://www.tellerreport.com/life/2020-06-16-emmanuel- macron-announces-measures-to-relocate-factories-in- france.rkpHqWLITI.html, accessed 13 April 2022.