Biomedical research and development in the Indian therapeutic drug industry

Health is a key issue in the development of a stable global social, political and economic structure in the 21st century. Better and reasonable health is a global goal. Great progress has been made during the past decades in the biomedical fields in the understanding of diseases, developing new diagnostic technologies and new medicines for better prevention and treatment of illness. The emergence of new diseases directly and indirectly affecting human activity through environmental changes is a new major scientific challenge. Research and development (R&D) is the heart of all advances and has the capacity to solve problems facing humanity. The paper aims to explore the biomedical R&D in the therapeutic segments of the pharmaceutical drug industry in India. The paper also highlights factors influencing the growth of biomedical R&D in therapeutic areas, the market and investments, and elaborates on the R&D pipeline of firms and public research for biomedical drugs in the current healthcare system in India.

1 Introduction

Biomedical research is a broad aspect of science that looks for ways to prevent and treat diseases that cause illness and death of people as well as animals. It is an evolutionary process requiring careful experimentation by many scientists, including biologists and chemists. Discovery of new medicines and therapies requires careful scientific experimentation, development, and evaluation (New Jersey Association for Biomedical Research, 2014). Therapeutics refers to treatment and care of a patient for the purpose of both preventing and combating disease or alleviating pain or injury. In a broader sense, it means, serving and caring for the patient in a comprehensive manner, preventing disease as well as managing specific problems (Rakel, 2014). Biomedical research is conducted in pharmaceutical, biotechnology and medical device firms. The paper addresses the therapeutic segments in the pharmaceutical industry, not all biomedical industries. Reducing the disease burden of the population has emerged as a major development challenge in several developing countries. R&D has always been the backbone and the underlying strength of biomedical innovation in the pharmaceutical industry. In the past decades, the Indian pharmaceutical industry has delivered multiple life-saving medicines contributing to new treatment options for several biomedical needs. Currently, it is playing a major role in medical needs and R&D investments in neuroscience, cardiovascular, endocrine, gastrointestinal, respiratory and genitourinary research.

The Indian pharmaceutical industry was valued at US$ 12 billion in the year 2013. Globally, India ranks 3rd in terms of volume and 14th in terms of value (Business Standard, 2014). The top 10 therapy areas (anti-infective, cardiac, gastrointestinal, respiratory, pain/analgesics, vitamins/nutrients, anti-diabetic, gynecology, central nervous system and derma) of the Indian pharmaceutical contribute to approximately 90% of the Indian pharmaceutical sales. The contribution of chronic therapies to the Indian pharmaceutical industry has raised from 27% in 2010 to 30% in 2013. Chronic therapies (cardio, gastro, central nervous system and anti-diabetic) have outperformed the market for the past four years and are growing at a rate of 14%, faster than the acute therapies (anti-infective, respiratory, pain and gynecology) which grew at 9.6% (PWC, 2013). Within the domestic formulations market the major therapeutic categories are anti-infective, gastrointestinal, cardiac, gynecology and dermatology. The leading drug classes were Cephalosporin, anti‐peptic ulcers, oral anti‐diabetic and Ampicillin or Amoxycillin, etc. (DOP, 2013).

In this backdrop, the present paper is an attempt to analyze the biomedical R&D in the therapeutic drug industry in India. The paper is divided into six sections. Section one deals with the introduction and the current market scenario of biomedical industry in therapeutic segments. Section two deals with the methods used for data collection. The third section presents the factors influencing growth of biomedical industry. Section four presents Indian biomedical firms in the therapeutic segments, and section five deals with the role of public sector units and research institutes in the biomedical R&D. Finally, section six deals with discussion and conclusion.

2 Research method

The research study is based on a quantitative research method. A quantitative method is generally used in order to collect statistical data and conduct statistical analyses (Yin, 2003). In this paper, quantitative indicators for R&D expenditure, net sales, profits, market share and registered patents have been collected. Details of R&D and innovation activities of Indian pharmaceutical firms, particularly in the therapeutic segments, were picked out through various sources such as authentic internet resources, annual reports, newspaper clippings, websites, etc. Data is mainly collected from companies’ websites and annual reports: www.lupin. com, www.sunpharma.com, www.cipla.com, www.zyduscadila.com, www.torrentpharma.com and www.ipcalabs.com. We also analyzed these facts from the peer-reviewed literature and books published by academia.

We have chosen the six largest Indian pharmaceutical companies in terms of revenue from worldwide pharmaceutical sales in therapeutic segments: Lupin, Sun Pharma, Cipla, Zydus Cadila, Torrent Pharma, and Ipca. These leading Indian companies examined here have been selected on the following basis:

- They are highly profitable and fast growing.

- Their initial technical skills have been in chemistry and low cost manufacturing.

- These companies are mainly active in the generics sector and produce generics to be sold in India.

- They have significant levels of international business, including products on sale in the highly regulated markets in the western countries. They obtain approval for and market generic drugs in the USA and Europe.

- They develop in-house skills in drug discovery and developing new patented drugs including biopharmaceuticals.

These six companies have diverse roots. Some were founded many years ago, e.g. Cipla in 1935, Zydus Cadilla in 1952, Torrent Pharma in 1959, Lupin in 1968 and some comparatively recently, e.g. Ipca in 1976, 1983 Sun Pharma in 1983. The vision of these companies is to make India self-sufficient in healthcare, a leader in the pharmaceutical industry, deliver world class products and services, and make quality medicine more accessible and affordable to the common man globally.

3 Factors influencing growth of biomedical industry

3.1 Growing and ageing population

The current world population of 7.2 billion is projected to increase by over 1 billion in the next 12 years and reach 9.6 billion by 2050 (UN News, 2013). Between 2000 and 2050, the proportion of the world’s population over 60 years will double from about 11% to 22%. The absolute number of people aged over 60 years is expected to increase from 605 million to 2 billion over the same period (WHO, 2014a). Most of the older people die of non-communicable diseases such as heart disease, cancer and diabetes, rather than from infectious and parasitic diseases. The growing ageing population will drive the demand for medicines and increase pharmaceutical spending.

3.2 Changing lifestyle

Rising prevalence of lifestyle diseases like hypertension, diabetes mellitus, dyslipidaemia and overweight or obesity are the major risk factors for the development of cardiovascular diseases. Cardiovascular diseases (CVD) continue to be the major cause of mortality representing about 30% of all deaths worldwide (Pappachan, 2011). With rapid economic development and increasing westernization of lifestyle in the past few decades, prevalence of these diseases have reached alarming proportions among Indians in the recent years (Pappachan, 2011).

3.3 The rising incidence of non-communicable diseases

Non-communicable diseases are the top cause of death worldwide, killing more than 36 million people in 2008. Cardiovascular diseases were responsible for 48% of these deaths, cancer 21%, chronic respiratory diseases 12%, and diabetes 3% (WHO, 2014b). World Health Organization (WHO) forecasts that by 2020, the non-communicable diseases will account for 44 million deaths a year, increasing by 15% from 2010 (WHO, 2010).

3.4 Prevalence of communicable diseases

Although disease patterns change constantly, communicable diseases remain the leading cause of mortality and morbidity in less developed countries. According to WHO, low-income countries currently have a relatively high share of deaths from: (i) HIV infection, tuberculosis and malaria, (ii) other infectious diseases, and (iii) maternal, perinatal and nutritional causes compared with high and middle income countries (Gupta and Guin, 2010; WHO, 2004).

3.5 Rising spend on healthcare

The healthcare sector in India is expected to grow at a CAGR of 15% and touch US$ 158.2 billion in 2017 from US$ 78.6 billion in 2012 (IBEF, 2014a). India is a country with a growing population, its per capita healthcare expenditure has increased at a CAGR of 10.3% from US$ 43.1 in 2008 to US$ 57.9 in 2011, and going forward it is expected to reach US$ 88.7 by 2015 (IBEF, 2014a). The factors behind the growth of the sector are rising incomes, easier access to high quality healthcare facilities and greater awareness of personal health and hygiene.

3.6 Growth in healthcare financing products

Development in the Indian financial industry has eased healthcare financing with the introduction of products such as health insurance policy, life insurance policy and cashless claims. This has resulted in an increase in healthcare spending, which in turn, has benefitted the pharmaceutical industry.

3.7 Health insurance is growing

Health insurance in India is a growing segment of India’s economy. It is expected to grow at a CAGR of 15% over the next five years and nearly 650 million people will enjoy health insurance coverage. Around 80% healthcare is financed out of pocket (PWC, 2010). The private healthcare facilities grew rapidly and insurance coverage increased. The small percentage of Indian who has some insurance and government run insurance company is the main provider. The government sponsored programmes largely focused on the below poverty line (BPL) segment and are expected to provide coverage to nearly 380 million people by 2020 (Bhadoria et al., 2012).

3.8 Increase in domestic demand

More than half of India‘s population does not have access to advanced medical services and is mainly depending on traditional medicine practices. However, with the increase in awareness levels, rising per capita income, change in lifestyle due to urbanization and increase in literacy levels, demand for advanced medical treatment is expected to rise. Moreover, growth in the middle class population would further influence demand for pharmaceutical products.

3.9 Rise in outsourcing activities

Increase in the outsourcing business in India would accelerate the growth of Indian pharmaceutical industry. Some of the factors that are likely to influence clinical data management and bio-statistics markets in India in the near future include: 1) cost efficient research 2) highly-skilled labour base 3) cheaper or low cost of skilled labour 4) presence in end-to-end solutions across the drug-development spectrum and 5) robust growth in the IT industry.

3.10 High R&D expenditures

The government of India is committed to supporting the expansion of R&D in the pharmaceutical and biotechnology industries and has taken a direct role in funding R&D in both, public and private sectors. The total biomedical R&D expenditure by both public and private sectors was US$ 10.4 billion between the year 2007 and 2012 in India (Chakma et al., 2014). This R&D expenditure included expenditures by government agencies, educational or research institutions, and charitable organizations, whereas for the industries it included expenditures by biotechnology, medical-device, and pharmaceutical firms.

4 Indian biomedical firms in therapeutic segments

4.1 Overview of the major players

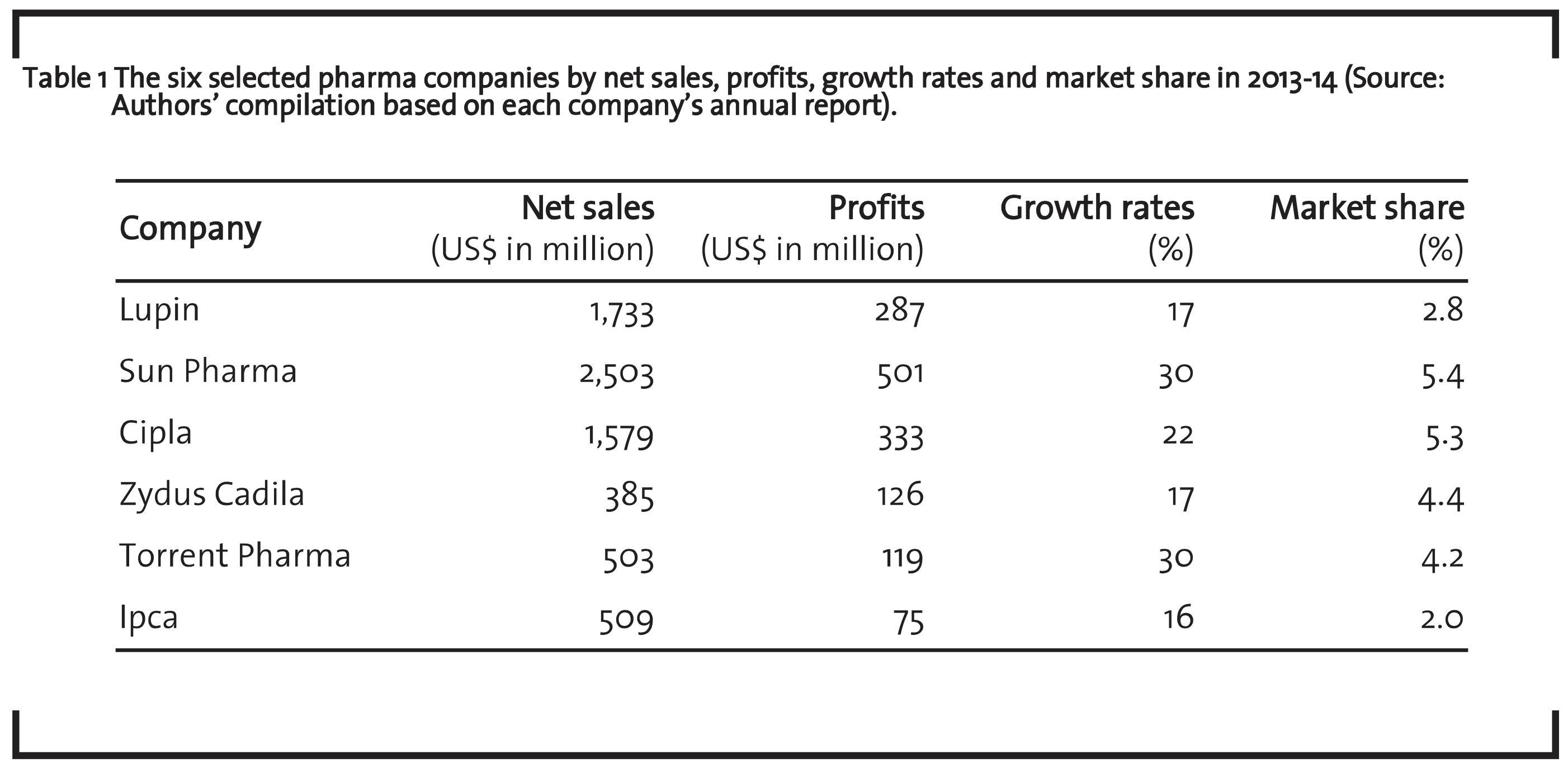

Biomedical innovation in the pharmaceutical industry in India is one of the largest and most advanced among the developing countries. The industry produces an entire range of products belonging to all major therapeutic segments. In the pharmaceutical world, India’s opportunities are significant in the context of medicinal development in the 21st century (Kumar and Satish, 2007). India has an existing generic based drug industry with an increasing focus on discovery. Antibiotic, cardiovascular, analgesic and antipyretic, antacids and anti-ulcerants, respiratory and anti-tuberculosis are the major therapeutic segments which account for over 90% of the domestic formulation market (Kumar and Satish, 2007). Other important therapeutic segments are anti-parasitic and antifungal products, non-steroidal anti-inflammatory drugs (NSAID) drugs, anti-anaemic, anti-diabetes, anti-malarial, anti-tuberculosis, central nervous system (CNS) and psychiatric products, gynaecology, nutrients and mineral supplements. Table 1 presents the figures of the six selected Indian pharmaceutical companies revealing their net sales, profit, growth rates and market share during the financial year 2013-14.

Sun Pharma has the largest share and has a strong positioning in chronic segments like central nervous system (CNS), cardiovascular and diabetology, together accounting for more than 50% of India formulation revenues. Torrent Pharma posted the highest growth in revenue; growth was primarily driven by cardiology, diabetology, CNS in chronic and gastroenterology in acute segments. The company is ranked number four in cardiovascular segment and in neuro-psychiatry therapies.

Lupin is one of the fastest growing players in high growth therapy segments like cardiology, central nervous system, diabetology, anti-asthma, and gynaecology, anti-infective, gastro intestinal and oncology. The company is the second largest player in India’s respiratory (anti-asthma) segment, third largest player in the cardiovascular segment and seventh largest player in diabetes segment. Cipla holds the second largest share and it has a leading position in various therapeutic categories, including respiratory and urology, and reinforces the potential to strengthen its presence in India across other therapies. It continues to increase its focus on CNS, oncology, dermatology and gastroenterology. The company holds a dominant position in the respiratory therapy segment and grasps 70% market share in this segment.

Zydus Cadila is one of the largest market players with leading positions in key therapy areas. It has strong leadership positions in the represented markets of cardiology, gynaecology, gastrointestinal and respiratory therapy areas. The company has gained second position in the dermatology segment and shifted from the sixth rank in 2013 to the fourth rank in 2014. Ipca is a therapy leader in India for anti-malarial and it focuses on chronic therapy segments such as cardiovascular, anti-diabetics and non-steroidal anti-inflammatory drugs (NSAID)

4.2 Investments into R&D

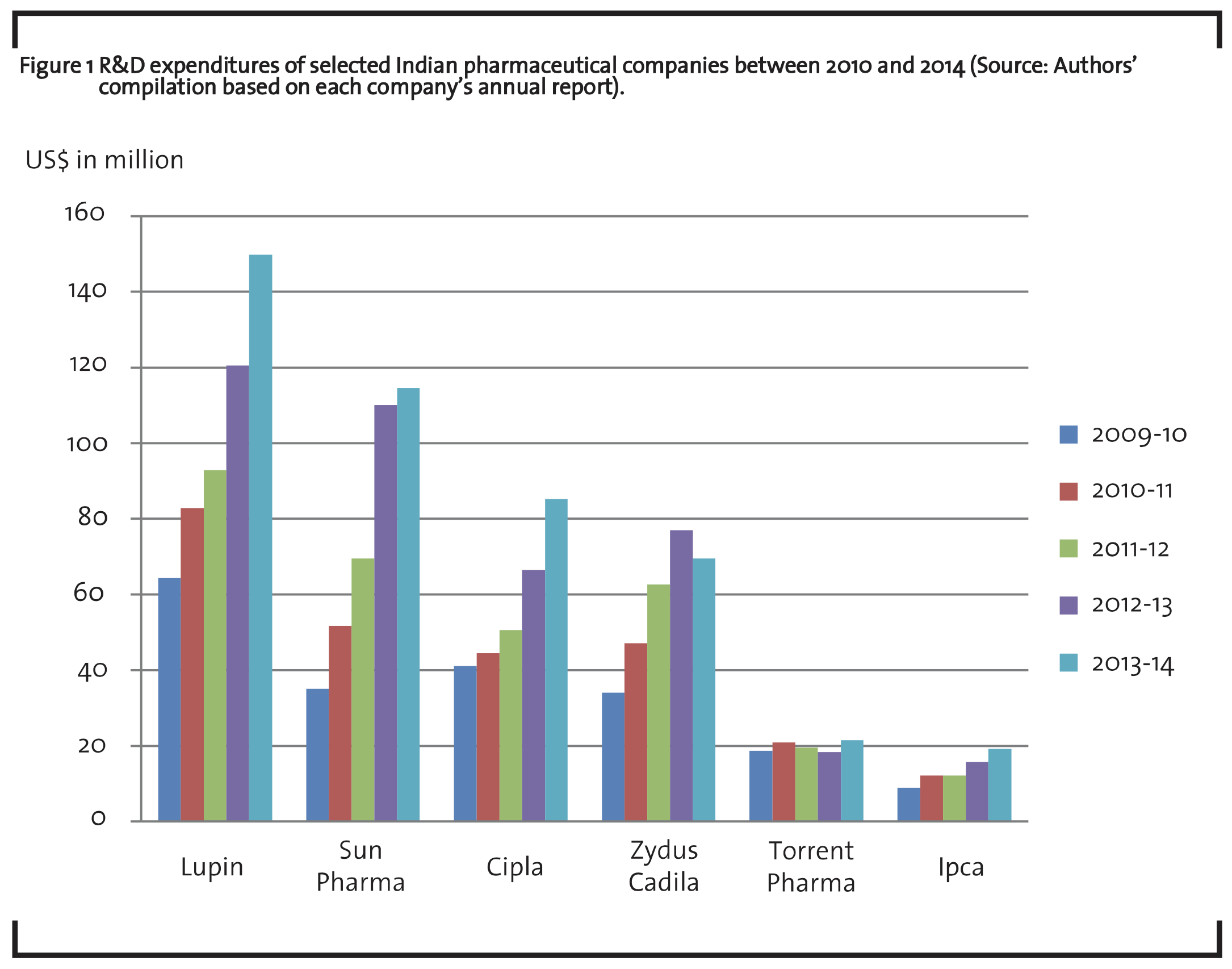

The pharmaceutical industry is knowledge intensive and R&D investment plays a crucial role in the growth of this industry (Shah et al., 2010). R&D in pharmaceutical industry includes directional search solutions to existing medical problems and unmet medical requirements. The pharmaceutical R&D may be concentrated in the New Chemical Entities (NCE), Novel Drug Delivery Systems (NDDS) or in generic products. R&D is a comparatively recent phenomenon for Indian pharmaceutical firms which gained momentum only after the year 1995. India introduced the product patent regime in accordance with the Trade Related Aspects of Intellectual Property Rights (TRIPs) agreement, in January 2005 with an amendment to the patent act. The allowance of product patents supported the confidence of innovator pharmaceutical companies in the Indian market (IBEF, 2014b). The cumulative figure for the top 30 companies is about US$ 837.9 million in 2012-13. This works out to be about 7.8% of the net sales of these companies (Rao, 2014). Figure 1 shows the R&D expenditures of selected pharmaceutical companies over the past five years.

The R&D expenditure of these pharma companies has steadily increased. In the financial year 2013-14, the total R&D expenditure by these six pharmaceutical companies was US$ 460.70 million. Currently, Lupin is the top pharma company spending for its R&D in the biomedical innovation in India. The company invested 8.6% of its net sales in R&D and related expenditure amounting to US$ 149.80 million in the financial year 2014. The company Novel Drug Discovery and Development (NDDD) program focuses on the discovery, development and commercialization of new drugs for new therapies and various diseases that include metabolic and endocrine disorders, pain and inflammation, autoimmune diseases, CNS disorders, cancer and infectious diseases. The R&D of Sun Pharma in India focuses on the chronic segments like diabetes, central nervous system, hypertension etc. The company spends around 6% of its net sales in the R&D, and has four modern R&D centres, expert scientist teams who are engaged in complex developmental research projects in process chemistry and dosage forms, including complex generics based on drug delivery systems.

The R&D wing of Cipla is involved in the development of new drug formulations for existing and new active drug substances, novel drug delivery system (NDDS) and development of products related to the indigenous systems of medicines. The total R&D expenditure as a percentage of total turnover was around 5% during the financial year 2014. The R&D of the company focuses on various therapeutic segments like respiratory, anti-viral, gynaecology and urology. Zydus Cadila focused on finding innovative therapies for diseases affecting mankind through continuous R&D. The total R&D expenditure as a percentage of total turnover was around 11% during the financial year 2014. The major areas of R&D include new chemical entities (metabolic disorders, diabetes, obesity, dyslipidaemia, inflammation and pain, rheumatoid arthritis, bacterial infections, and cancer) research, formulation development, process research and novel drug delivery system.

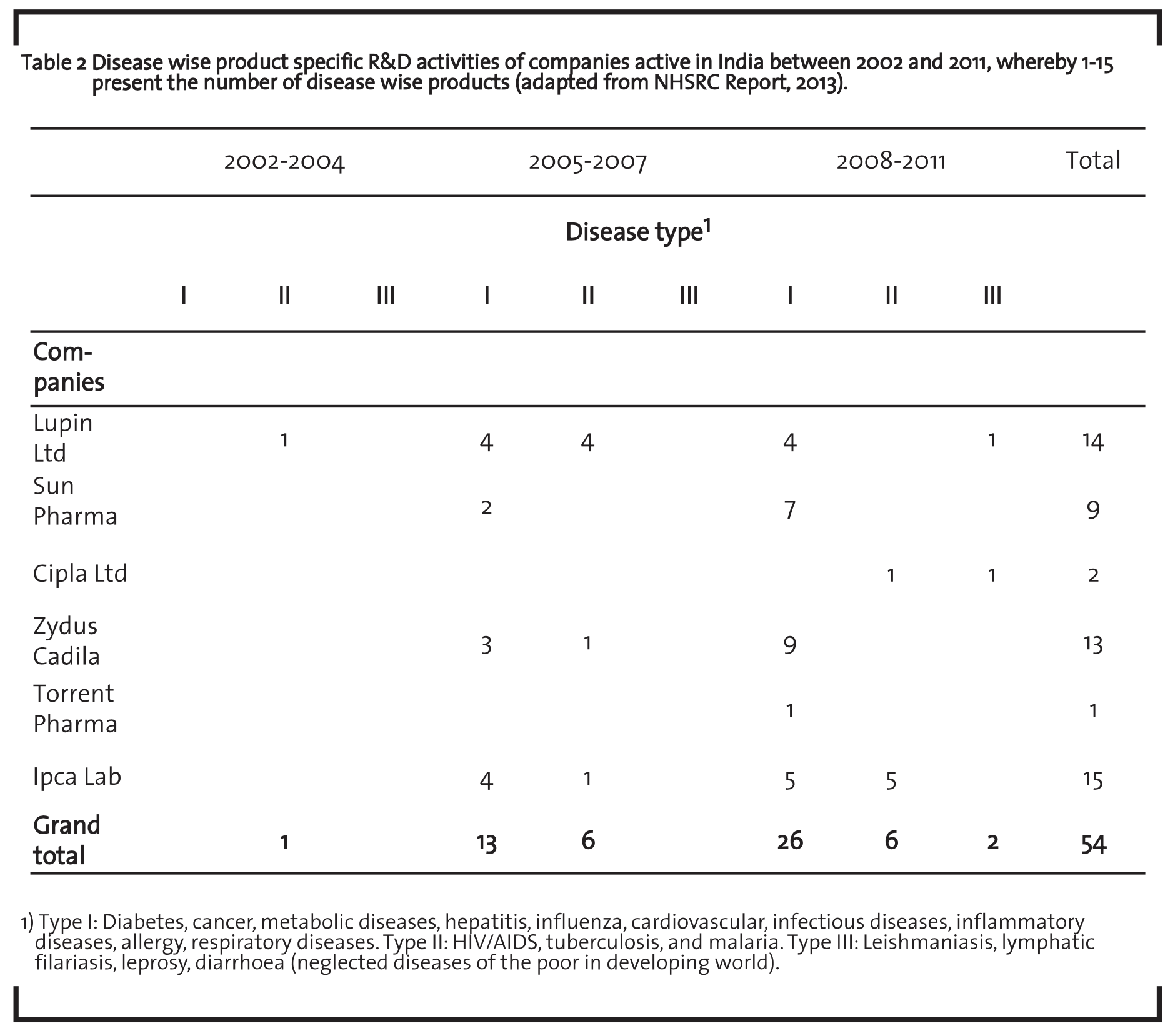

Torrent Pharma is currently working on several in-house new chemical entities R&D projects within the areas of diabetes and its related complications, metabolic, cardiovascular and respiratory disorders. The total R&D expenditure as a percentage of turnover was 4.26% during the financial year 2014. The company R&D expenses have increased by 10% to US$ 21.57 million as compared to US$ 19.54 million during the financial year 2013. Product development costs accounted for 71% and discovery research costs accounted for 29% in 2014 of the total R&D cost. The company has expert scientist teams who offer dedicated services in the areas of discovery research, generic drug development, new drug delivery systems and value added generics thereby transforming discoveries into the highest quality therapeutic products. Ipca is a therapy leader in India for anti-malarial and also leads in DMARDs (Disease Modifying Anti-Rheumatic Drugs) treatment for rheumatoid arthritis. The company carries out R&D in several areas including the development of newer dosage forms and new drug delivery systems, process improvements, technology absorption and optimization of basic drugs, process simplification, etc. The company had stepped up its R&D expenditure from US$ 15.69 million in the financial year 2013 to US$ 19.2 million in the year under report. The total R&D expenditure as a percentage of total turnover is 3.87% during the financial year 2014. Table 2 shows the disease wise product specific R&D activities of the selected pharmaceutical companies in India.

The table shows the categorization of diseases into type I, II, and III and product wise specific R&D activities of selected companies during 2002 to 2011. This indicates that Ipca Lab and Lupin Ltd are more active in type I and type II diseases. Sun Pharma and Zydus Cadila are more active in type I diseases. In case of Cipla and Torrent Pharma are less R&D activities compared to other companies.

4.3 Therapeutic areas of new drug R&D

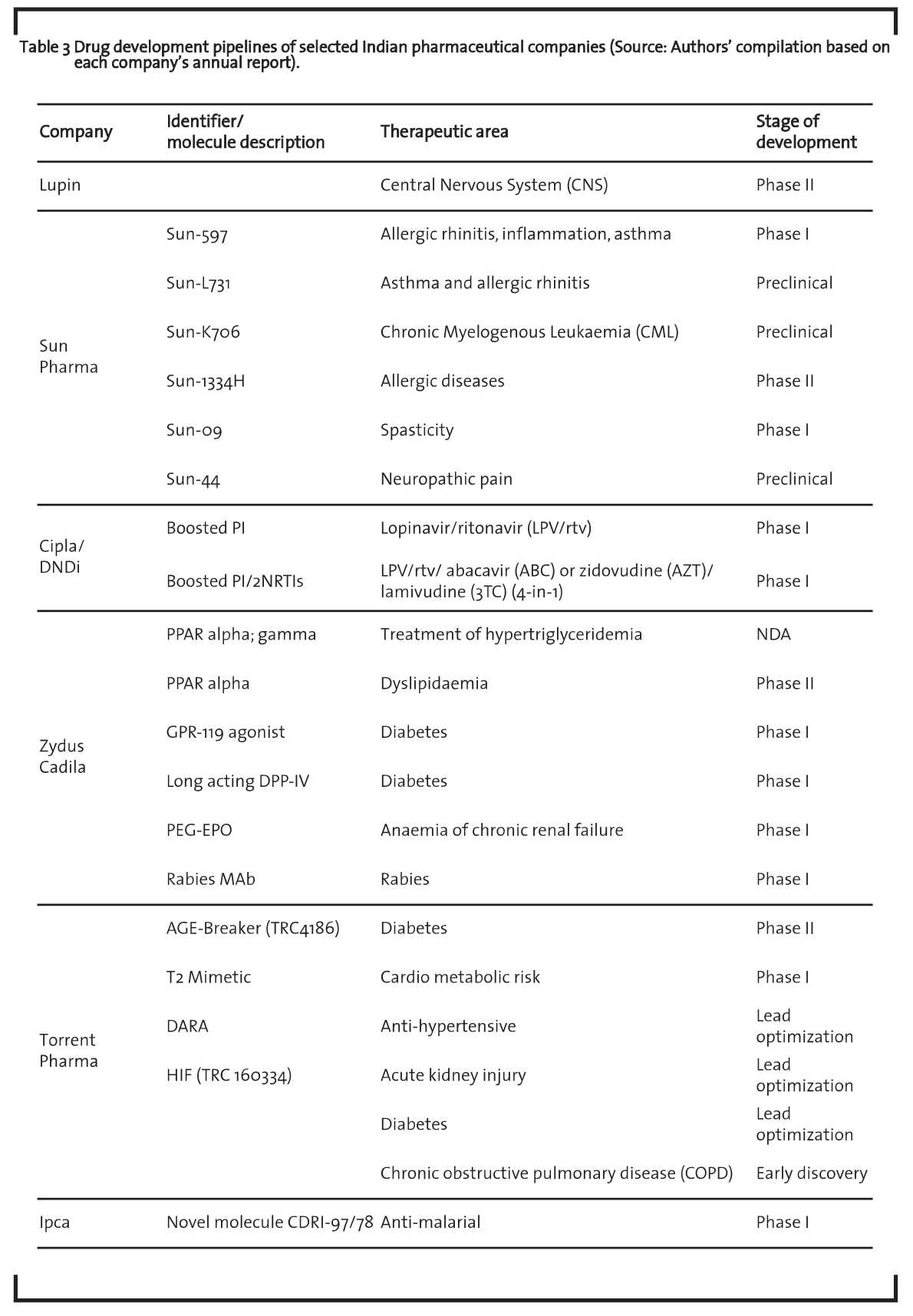

Research in the development of drugs has generally two major aspects: (i) discovery of a new drug molecule, and (ii) invention of new formulations of drugs with higher therapeutic index (Maitra, 2000). A drug discovery pipeline has various phases that can be grouped into four stages: discovery, pre-clinical, clinical trials and marketing (or post approval). It is an important indicator of the value and future prospects of a company. Usually, the more compounds in the pipeline and the more advanced stage these are in, the better. Table 3 includes a list of new molecules of selected leading pharmaceutical companies in the therapeutic segment in India which are at different stages of development.

The table shows that R&D efforts focus on chronic disease such as diabetes. Lupin’s Novel Drug Discovery and Development (NDDD) program focuses on the discovery, development and commercialization of new drugs that address disease areas with significant unmet medical needs. Currently, the program in the CNS area completed phase I studies in Europe and is being advanced to Phase II clinical trials in Europe. Cipla R&D is focused towards developing new products, improving existing products as well as drug delivery systems and expanding product applications. Cipla and the Drugs for Neglected Diseases initiative (DNDi) are developing a more acceptable granule formulation of 40/10 mg lopinavir/ritonavir as part of a first-line regimen for infants and young children.

The Sun Pharma strategy has been dominating the lifestyle disease segments. SUN-597 is a topical glucocorticoid being developed for allergic rhinitis, inflammation, asthma and other applications and completed its Phase I clinical trials in India. SUN-L731 is being developed as an oral LTD4 antagonist for treatment of Asthma & Allergic Rhinitis. SUN-K706 is a novel tyrosine kinase inhibitor (TKI), intended for the treatment of chronic myelogenous leukaemia (CML). Currently, available oral drugs like Imatinib (Gleevec®), Nilotinib (Tasigna®) and Dasatinib (Sprycel®) are quite effective chemotherapeutic agents CML. Sun 09 is a prodrug of Baclofen and is being developed as an efficient Baclofen. Baclofen is the standard drug of choice for the treatment of spasticity. Zydus Cadila currently conducts basic new drug discovery research in cardio-metabolic, inflammation, pain and oncology therapeutic areas. During the year 2014, the company launched Lipaglyn (Saroglitazar) in India, its first NCE for treating diabetic dyslipidaemia and hypertriglyceridemia. It is the first drug discovered and developed indigenously by an Indian pharmaceutical company.

Torrent Pharma R&D is engaged in the discovery of new chemical entities and the development of new processes and suitable formulations for known Active Pharmaceutical Ingredients (APIs). The most advanced discovery program of the Company is Advanced Glycation End-Products (AGE) Breaker, of which the Phase II clinical trials for the indication of diabetes associated heart failure in India and Europe is completed. Ipca is actively engaged in the segment of new Drug Discovery Development by collaborating with various research organizations and premier institutes in India and abroad. The company’s current pipeline includes pain management, anti-ulcer and anti-malarial and one of the novel molecules (CDRI- 97/78) has shown very promising anti-malarial activity and is currently in clinical Phase-I in India.

4.4 R&D outcomes

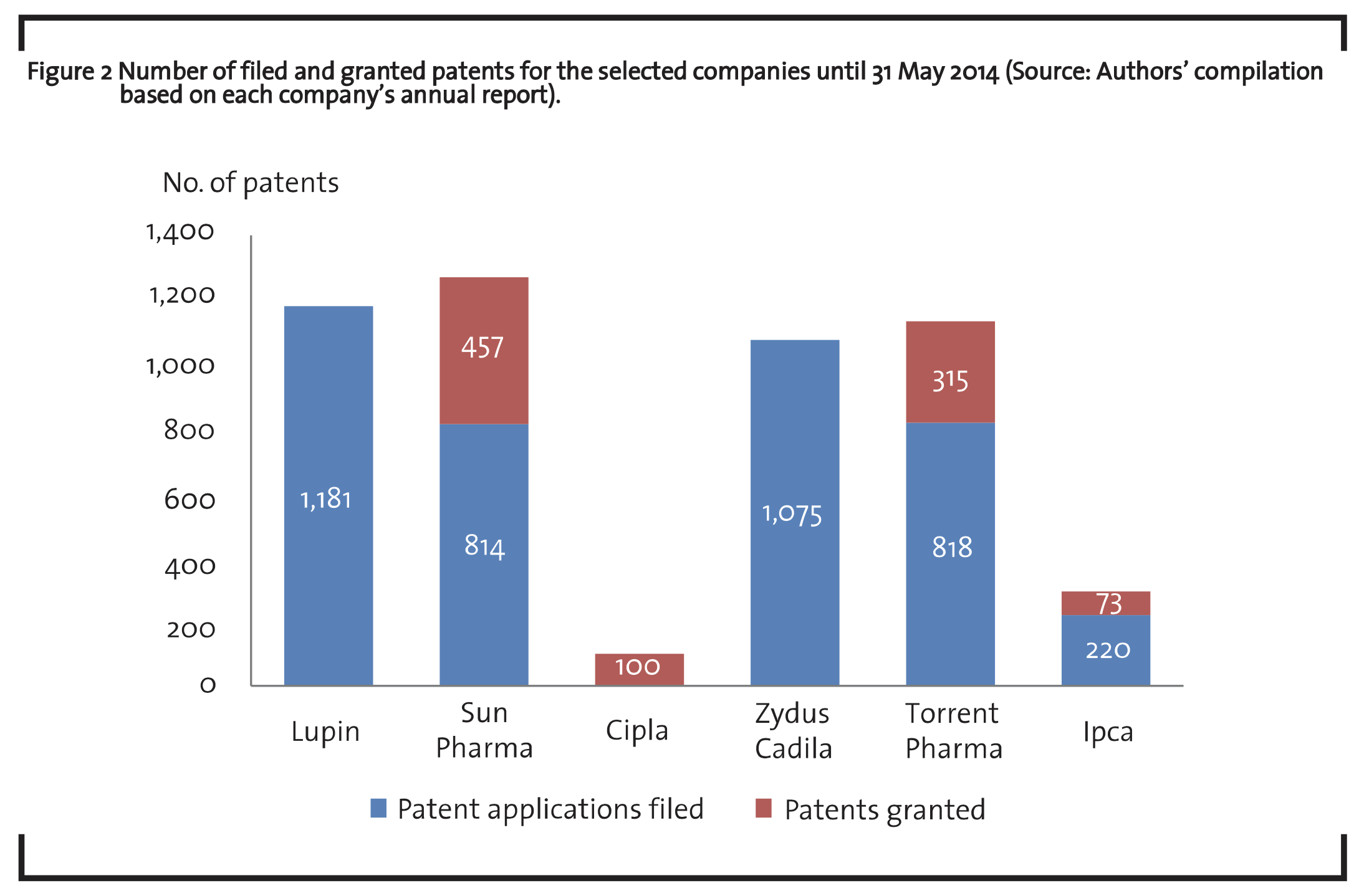

R&D investments are indicators for the main inputs into science based innovation. Publication and patent data provide complementary indicators for research and development activities, although capturing intermediate outputs (OECD, 2008). Patents are the most important way in which researchers can protect the ideas or technologies they have developed. It reflects the ability of transferring scientific results into technological applications. It is also essential for economic exploitation of research results and is thus central to any analysis which deals with economic potentials of technology and the identification of the most promising fields and actors in terms of persons, organizations or countries (Hullmann, 2006; Ali and Sinha, 2014). Figure 2 provides company wise patent applications filed and granted at different patent offices (Indian Patent Office (IPO), European (EPO) and United States Patent and Trade Office (USPTO)).

The figure shows that Sun pharma has the maximum number of patents granted. Lupin has comparably filed the highest number of patent applications in India and other countries. This included 108 formulation patents, 39 Active Pharmaceutical Ingredients (APIs) or process patents, 2 biotech and 232 new chemical entity (NCE) patents in India and other countries. Cipla has been granted about 100 patents. Patent filing includes drug substances, drug products, platform technologies, IP on polymorphs and crystallinity, and medical devices. Zydus Cadila has filed over 115 patents in the US, Europe and other countries, taking the cumulative number of filings to over 1,075. Torrent pharma has 818 patents filed for novel drug delivery systems (NDDS) technology, drug discovery projects and innovative process of API and formulations for various geographies and 315 have been granted so far. Ipca has 220 patent applications filed till date in India, USA and other countries. These applications relate to novel and innovative manufacturing processes for the manufacture of APIs and pharmaceutical formulations.

5 Role of public sector units and research institutes

There are five central public sector companies established by the government of India, which are Indian Drugs and Pharmaceuticals Limited (IDPL), Hindustan Antibiotics Limited (HAL), Bengal Chemicals and Pharmaceuticals Limited (BCPL), Bengal Immunity Limited (BIL) and Smith Stanistreet Pharmaceuticals Limited (SSPL). HAL and IDPL play a very important role in the biomedical R&D in India. HAL is the first public sector company in drugs and pharmaceuticals and HAL was incorporated on 30th March, 1954 in Pune. It was established to produce antibiotic with the assistance of WHO and UNICEF. It is the first company in India to manufacture of antibiotic drugs like penicillin, ampicillin, gentamicin, streptomycin, sulphate, anhydrous from the basic stage (Mazumdar, 2013). IDPL was incorporated on 5th April, 1961 for achieving India’s march towards self-sufficiency and self-reliance in the field of drugs and pharmaceuticals, particularly with the primary objective of creating self-sufficiency in essential lifesaving drugs and medicines (DOP, 2012). Presently, under different classes of therapeutic medicines, around 87 generic or branded drugs covering tablets, capsules, injections, vitamins, oral rehydration solution (ORS) pouches etc. are being manufactured in various plants of IDPL (DOP, 2012).

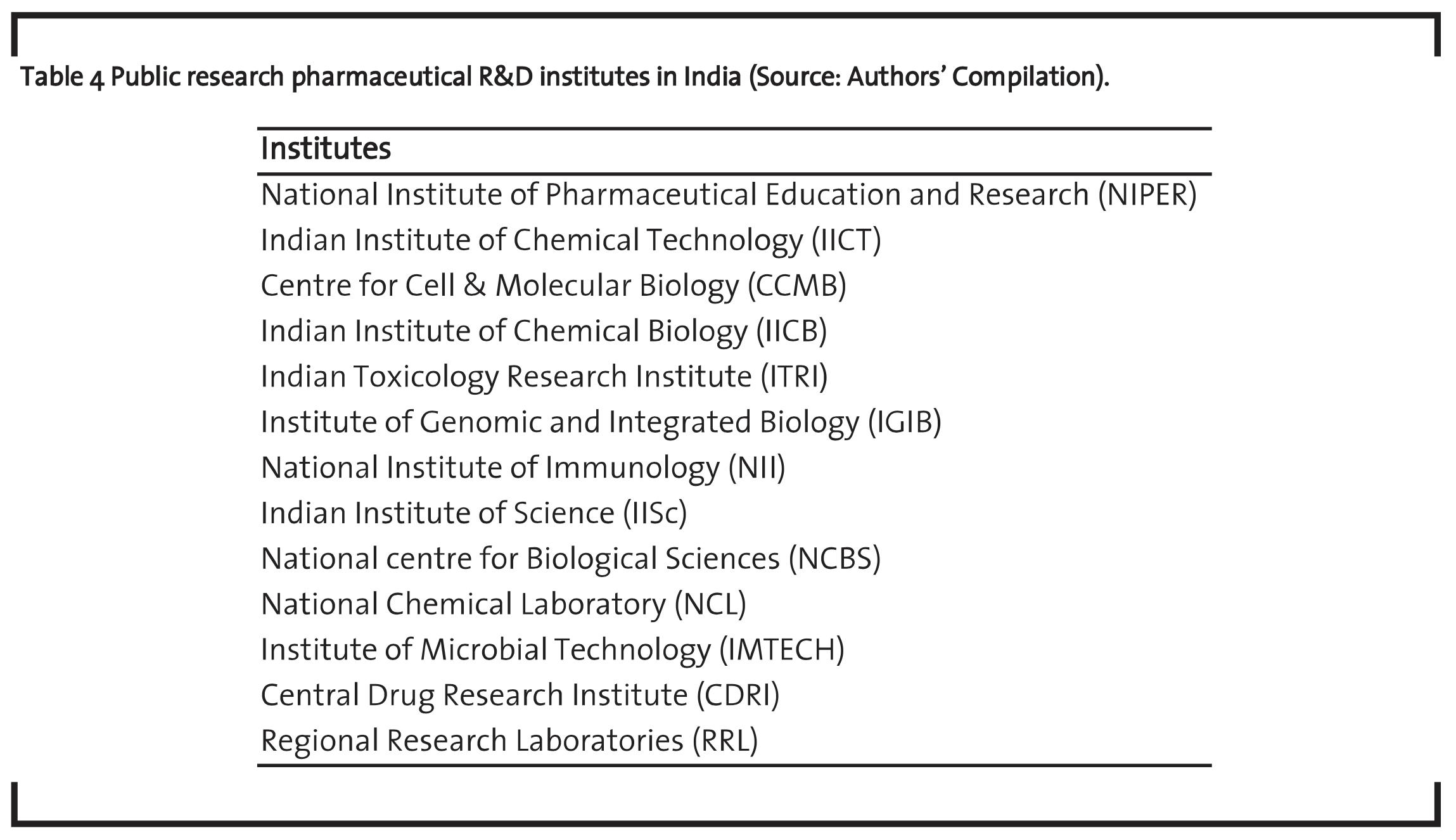

The publicly funded research institutes are also playing a key role in the growth of the biomedical sector in India. The government of India has created a number of research institutes under the guidance of the Indian Council of Medical Research (ICMR) and the Council of Scientific and Industrial Research (CSIR) to promote technological advancement of the country. The CSIR institutes are playing a significant role in boosting up the knowledge base in the biomedical R&D sector of India. The technologies developed by the public research institutes are also transferred effectively from laboratories to industries. The success of the CSIR laboratories in fostering the technological environment of the Indian pharmaceutical firms in the biomedical sector is also evident and shows that almost all the top pharmaceutical companies like Lupin, Ranbaxy, Cipla, Nicholas Primal, Wockhardt, Torrent Pharma, Sun Pharmaceutical, Orchid, and Aurobindo Pharma Ltd have benefited from the services of the research institutes in India in some or the other way. Table 4 shows some of the public research pharmaceutical R&D Institutes in India.

6 Conclusion

The Indian biomedical industry has been on a strong growth trajectory in the last decade. It has achieved several milestones and is well positioned to leverage emerging opportunities. The industry needs to tackle various issues related to its operations and regulations. The current Indian drug discovery pipeline offers attractive opportunities, as it illustrates that Indian pharma companies have proven their capability to build integrated drug discovery capabilities, and to drive molecules from the early discovery stage to development.

The analysis of R&D expenditures of pharmaceutical firms shows that there had been a growth in the R&D intensity. Presently, most of the company’s drug development pipeline is in the stages of lead identification, preclinical research and Phase I. In the R&D for new drugs, the analysis of the new drug pipelines of leading Indian pharma firms shows that the new patent regime has not been able to become the driving force. The R&D activities of Indian firms are increasingly getting concentrated on lifestyle diseases of global nature and they do not find any opportunity in local diseases such as tuberculosis and malaria except a single pharma company, i.e. Ipca laboratory. The patenting activity is focused on new processes, new dosage forms and drug delivery systems.

There is a need for real prioritization of R&D and innovation activities by the government. The public sector companies and public sector laboratories have played a major role in augmenting the science and technology skills of the private sector industry. The discovery and development of new drugs are the result of a close collaboration between university and industry researchers. In this process, the public and private sectors pursue distinct but complementary objectives. Whereas the role of the public sector is centred on deepening our basic understanding of disease, that of the private sector is more focused on applied research aimed at converting this knowledge into effective treatments. Public research institutions play an important role in the system’s positive evolution but they are dependent on the government policy and budget. The benefits that flow from public subsidies to university research can be reaped only once effective treatments have been developed – only the pharmaceutical industry is in the position to play this role.

References

Ali, A., Sinha, K. (2014): Emerging scenario of nanobiotechnology development in India, European Academic Research, 2 (2), pp. 1707-1727.

Bhadoria, V., Bhajanka, A., Chakraborty, K., Mitra, P. (2012): India pharma 2020: Propelling access and acceptance, realizing true potential, McKinsey & Company.

Business Standard (2014): Success strategies for Indian pharma industry in an uncertain world, available at http://www.business-standard.com/content/b2b-chemicals/success-strategies-forindian-pharma-industry-in-an-uncertain-world-114021701557_1.html, accessed 5 July, 2014.

Chakma, J., Gordon, H., Sun, M. D., Steinberg, J. D., Stephen, M. S., Jagsi, R. (2014): Asia’s ascent: Global trends in biomedical R&D expenditures, The New England Journal of Medicine, 370 (1), pp. 3- 6.

DOP (2012): Annual Report 2011-2012, Department of Pharmaceuticals, Government of India, Ministry of Chemicals & Fertilizers, New Delhi.

DOP (2013): Annual report 2012-2013, Department of Pharmaceuticals, Government of India, Ministry of Chemicals & Fertilizers, New Delhi.

Gupta, I., Guin, P. (2010): Communicable diseases in the South-East Asia Region of the World Health Organization: Towards a more effective response, Bulletin of the World Health Organization, 88, pp. 199-205.

Hullmann, A. (2006): The economic development of nanotechnology: An indicator based analysis, European Commission Report, available at ftp://ftp.cordis.europa.eu/pub/nanotechnology/docs/nanoarticle_hullmann_nov2006.pdf, accessed 2 July 2014.

IBEF (2014a): Healthcare industry in India, India Brand Equity Foundation, available at http://www.ibef.org/industry/healthcareindia. aspx, accessed 13 July 2014.

IBEF (2014b): Pharmaceuticals, Indian Brand Equity Foundation, available at www.ibef.org, accessed 11 July 2014.

Kumar, B. R., Satish, S. M. (2007): Growth Strategies of Indian Pharma Companies, The Icfai University Press, Hyderabad.

Maitra, A. (2000): Drug delivery: Today’s scenario and opportunities for Indian pharmaceutical industry, Current Science, 79 (10).

Mazumdar, M. (2013): Performance of Pharmaceutical Companies in India: A Critical Analysis of industrial Structure, Firm Specific Resources, and Emerging Strategies, Springer, Heidelberg.

New Jersey Association for Biomedical Research (2014): What is biomedical research?, available at http://biology.unm.edu/MARC/what-is-biomedical-research.html, accessed 11 July 2014.

NHSRC Report (2013): Opportunities, ecosystem requirements and road-map to innovations in the health sector, Draft Report of the Sector Innovation Council for Health, National Health System Resource Centre, Ministry of Health and Family Welfare, Government of India. New Delhi.

OECD (2008): Nanotechnology innovation: An overview, Working party on Nanotechnology, Organization for Economic Cooperation and Development, available at http://www.oecd.org/science/sci-tech/oecdworkingpartyonnanotechnology.htm, accessed 2 July 2014.

Pappachan, M. J. (2011): Increasing prevalence of lifestyle diseases: High time for action, Indian Journal of Medical Research, 134, pp. 143-145.

PWC (2010): Capitalizing on India’s Growth Potential, Price Waterhouse Coopers Private Limited, available at https://www.pwc.in/assets/pdfs/pharma/PwC-CII-pharma-Summit-Report-22Nov.pdf, accessed 23 May 2015.

PWC (2013): Changing landscape of the Indian pharma industry, Price Water Cooper India pharma Inc., available at http://www.pwc.in/assets/pdfs/publications/2013/changing-landscape-of-theindian-pharma-industry.pdf, accessed 5 July 2014.

Rakel, R. E. (2014): Therapeutics medicine, available at http://www.britannica.com/EBchecked/topic/591185/therapeutics, accessed 5 June 2014.

Rao, D. Y. (2014): R&D in pharmaceuticals sector, Paper presented at the national conference on pharmaceutical policies in India: Balancing industrial and public health interests, March 7, 2014 at ISID Auditorium ISID Complex, New Delhi.

Shah, B. N., Nayak, B. S., Jain, V. C., Shah, D. P. (2010): Textbook of Pharmaceutical Industrial Management, Reed Elsevier India Private Limited.

UN News (2013): World population projected to reach 9.6 billion by 2050, available at http://www.un.org/apps/news/story.asp?NewsID=45165#.U7jb3_QW3CI, accessed 06 July 2014.

WHO (2004): Global burden of disease 2004 update: Selected figures and tables, available at http://www.who.int/healthinfo/global_burden_disease/GBD2004ReportFigures.ppt#2, accessed 13 July 2014.

WHO (2010): Global status report on non-communicable diseases, available at http://whqlibdoc.who.int/publications/2011/9789240686458_eng.pdf?ua=1, accessed 13 July 2014.

WHO (2014a): Ageing and life course, available at http://www.who.int/ageing/en, accessed 12 July 2014.

WHO (2014b): WHO maps non-communicable disease trends in all countries, available at http://www.who.int/mediacentre/news/releases/2011/NCDs_profiles_20110914/en, accessed 13 July 2014.

Yin, R. K. (2003): Case study research: Design and methods, Sage Publications, USA.