Chemistry 4.0 – Growth through innovation in a transforming world

Abstract

A new phase of development is beginning in the German chemical industry. With “Chemistry 4.0” begins the fourth stage of development in the industry’s 150-year history, which will be shaped by digitalization, the circular economy and sustainability in the coming decades. This is the conclusion of the study “Chemistry 4.0 – Growth through Innovation in a Changing World”, created by the German Chemical Industry Association (VCI) with the support of Deloitte.

1 A transforming world is challenging the chemical sector

The business situation of the German chemical industry is currently very good. Following a strong upswing in 2017, the perspectives remain favorable in 2018 and the sector is heading for new records. For the first time in its history, the German chemical industry could surpass the € 200 billion mark in revenues. To be prepared for the future, the companies invest in new capacities, research and development as well as in tertiary education of high-skilled employees. But looking for the decades to come, the industry is faced with elementary strategic and structural challenges:

On the one hand, demand for chemical products in Western Europe will grow only modestly in the decades ahead, moving the focus toward markets in Asia, South America, and, eventually, Africa. Since international and local competitors are expanding their production capacities there, and additional capacities in resource-rich regions are to be expected, the whole competitive environment in the chemical industry is about to face a transformation. In addition, manufacturers in developing and resource-rich countries are expanding their scope to include specialty chemicals – which until now had often been covered by German exports. These changes mean a further increase in competitive intensity for the chemical sector in Germany, both in its European home market and in the export markets: in Europe, import pressure on base chemicals and intermediate products from resource-rich regions will go up, while in export markets, competition with local providers and other importers will intensify.

On the other hand, a paradigm change in demand structures and public preferences has already been taking place for a while and is set to continue. The desire to use resources in an efficient and environmentally friendly way has noticeable effects on energy supply and consumption habits. The trend toward the Sharing Economy illustrates this transformation. By developing strategies to serve changing customer requirements, companies make an important contribution toward reaching UN sustainability goals. Circular economies will gain in importance, and digitalization will lead to extensive changes in all sectors. These two core topics are of central importance to the trends in the chemical sector up to 2030 and beyond.

Consequently, the environment of the chemical industry in Germany is not only changing more strongly than in earlier decades. In the future, there will also be disruptive changes for which the companies need to get ready. The digitalization of agriculture, personalized medicine or autonomous driving with electrical vehicles are prominent examples of changes with considerable impact on chemical business. In view of these major challenges, considerable efforts are required to continue the industry’s 150 years of success. It is obvious that process innovation and product innovation should in most cases be accompanied by new, service oriented business models in the future. Solutions for customers will increasingly be developed and marketed in cooperation with other companies, research institutes or start-ups.

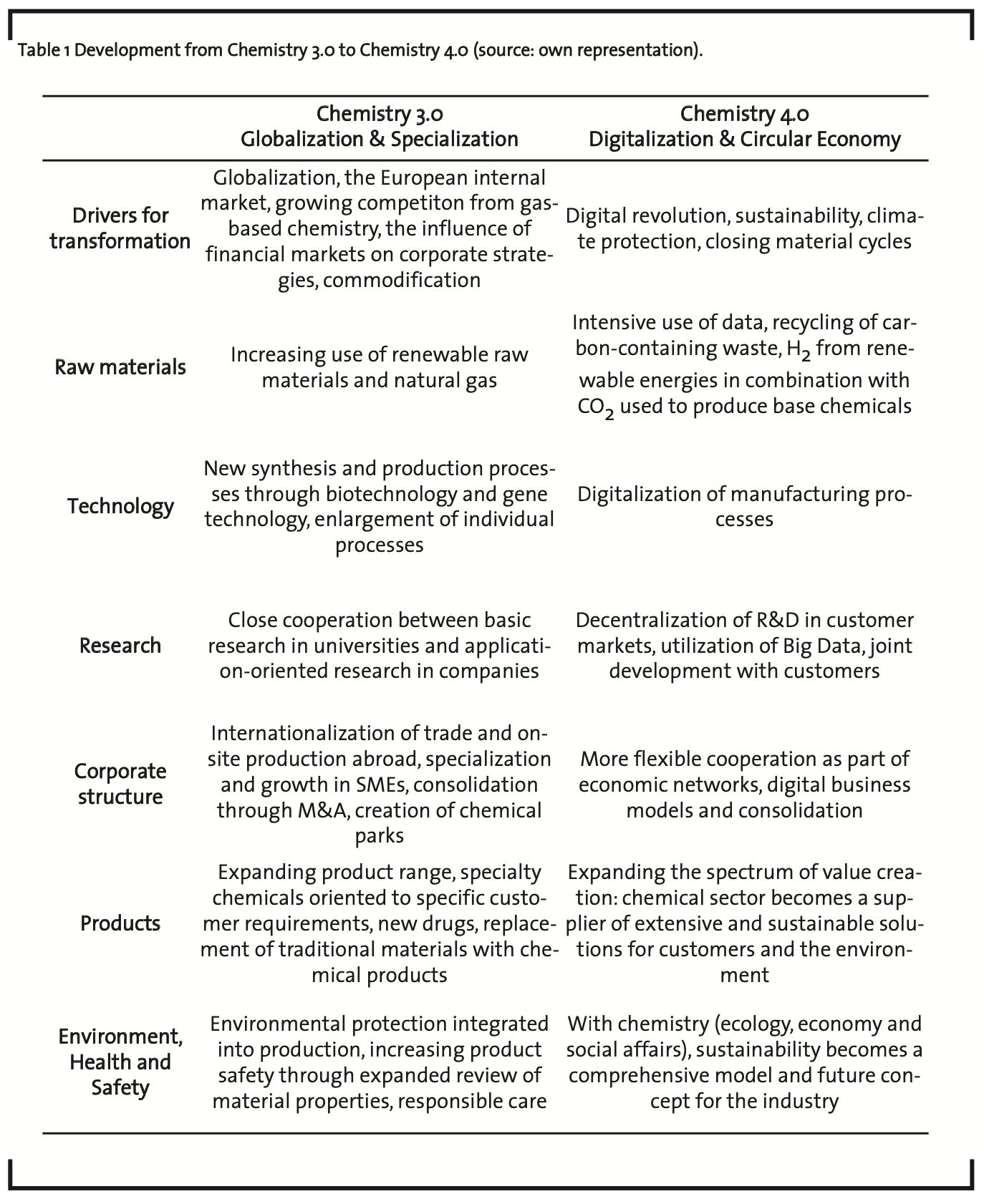

The VCI/Deloitte study shows that the chemical industry in Germany is in a transition to a new development phase. After industrialization and coal chemistry (Chemistry 1.0), the emergence of petrochemistry (Chemistry 2.0) and increasing globalization and specialization (Chemistry 3.0), the industry is entering the new phase of Chemistry 4.0 in which digitalization, sustainability and circular economy play key roles. These topics are not detached from each other: In particular, the interplay between digitalization and circular economy is growing in importance and contributes to achieving the UN sustainable development goals.

This study analyzes in detail this dramatic change, with the following guiding questions:

- How can the chemical industry at the location Germany expand its value creation potentials domestically while at the same time improving its international competitive position?

- How can the industry comprehensively use digitalization, identify attractive digital business models early-on and thus open up new business potentials that go beyond the production of chemical products and materials?

- How can the industry contribute to closing material cycles, minimize resource consumption and, in this manner, equally achieve social, economic and ecological goals?

- Can we improve economic framework conditions, supporting the chemical industry to remain an innovation and growth driver of the German economy and essentially contributing to the prosperity of our country?

2 Methodology

The analysis was made in a multi-stage process involving experts from VCI member companies and VCI, Deloitte, associations of suppliers and customer industries, as well as from science and politics. The study consists of four sections:

2.1 Analysis of the business environment

Major trends were identified, based on a comprehensive, artificial intelligence-supported literature analysis by the Deloitte Center for the Long View. Relying on that, an expert workshop prioritized 30 trends for further analysis. These trends are likely to have a significant influence on the chemical and pharmaceutical industry in Germany to 2030.

That was followed by 5 expert workshops and around 40 expert interviews which analyzed the developments in energy and raw material markets, pharma and health markets, business-to-consumer and business-to-business activities of the chemical industry, and special characteristics of Germany as an investment location. Each of the 30 trends was analyzed in detail and evaluated concerning the impact on the chemical industry in Germany, and whether it constitutes a chance or a risk for the chemical industry in Germany in current framework conditions.

1) In the following summarized as chemical industry, comprising NACE segments 20/21.

2.2 Detailed analysis of chances and risks of digi- talization and circular economy

Building on the analysis of the broader environment, further detailed analysis considered the impacts and chances of digitalization and circular economy as key topics. For this purpose, two workshops each were held on digitalization and circular economy. The connection between digitalization and circular economy was addressed more profoundly, and potential roles of chemical companies in (digital) economic networks were considered.

2.3 Survey among medium-sized enterprises

The analyses were supplemented by a comprehensive survey among medium-sized chemical and pharma companies. The survey aimed at obtaining information on the preparation of companies for the digital and circular transformation, on corresponding challenges, and on expectations towards policymakers and associations. In total, 124 medium-sized enterprises from the chemical and pharma industry took part in the survey (response rate >15%).

2.4 Recommendations for action

Results of the study were summarized in a catalogue of recommendations, directed at policy-makers, industry associations and chemical companies.

3 Results

3.1 Incremental innovation and disruptive changes in chemical business

Within the study, 30 trends were identified that will be of special importance to the chemical and pharmaceutical industry1 in Germany to 2030. In the medium-term, many of the trends have considerable impacts on the companies of the chemical industry. In particular, it can be differentiated according to whether the trends in their impacts on the chemical industry need to be seen rather as incremental or disruptive.

Incremental changes are characterized by continuous innovation and improvement processes that largely take place inside existing product portfolios, process technologies and established business models. The structure of value chains remains largely unchanged. Such incremental, continuous innovation processes are part of the existing business and success models of the chemical industry in Germany. Also in the future, they will offer significant growth opportunities for chemical companies. The chemical industry in Germany is traditionally in a good position for coping with the challenges of incremental changes.

But intensifying competition in the national and international environment means an ever-faster erosion of prior competitive advantages. Also in the future, major efforts will need to be made in research and development. Here, the medium-sized chemical industry – as an innovative industry close to consumers – is an important driver. Especially this industry can and needs to deploy its strengths through cooperation across companies and sectors (see chapter “Recommendations for action to companies and their associations”).

Disruptive changes in the chemical industry’s environment profoundly influence product portfolios, value structures and new business models. This comprises both the chemical companies themselves and the entire structure of their customer and supplier relations. Frequently, disruptive changes are triggered by changing needs of society, regulatory changes or new technologies. On the one hand, this type of change brings changes for chemical and pharma companies in new fields of growth. On the other hand, it presents challenges for fundamentally adapting products, services and business models to the new framework conditions.

Disruptive changes come in two forms: disruptive product innovations and disruptive changes of business models.

- Disruptive product innovations describe technologies or products that are fundamentally different from existing ones. They offer great growth potential while competing with existing products. The above-described trends (e.g. in e-mobility and personalized medicine) can be subsumed here, as they can profoundly change the demand structures in the respective product segments. All the same, disruptive product innovations only have a limit- ed impact on the structure of value chains – to the extent that products can continue to be manufactured and marketed within existing structures.

- By contrast, disruptive changes of business models describe a new form of service rendering where several companies bundle various products and services and jointly offer them to customers. On the one hand, this gives the opportunity to chemistry to get closer to customers and to take over a larger share of value creation. On the other hand, there is the risk of the chemical industry being reduced purely to a supplier of materials and chemicals, while new market players establish themselves between the customers and chemical companies. Here, digital business platforms and value networks are gaining in importance, and the gathering, exchange and analysis of digital mass data are becoming ever more important. In this new environment, the above-described role as a chemical supplier – with a focus on a more efficient production of innovative chemicals – can pose a risk if other non-chemical competitors build market power and control value networks.

At a second level of differentiation, a distinction is possible according to whether the above-described trends and the connected decisions largely follow economic or business management calculations or whether societal and political criteria have a dominant role for the further development. This categorization is difficult and also depends on the development of societal and political dialogues. However, a distinction according to these criteria indicates the breadh of the connected societal debate and points to the need to involve political and civil society stakeholders in the development.

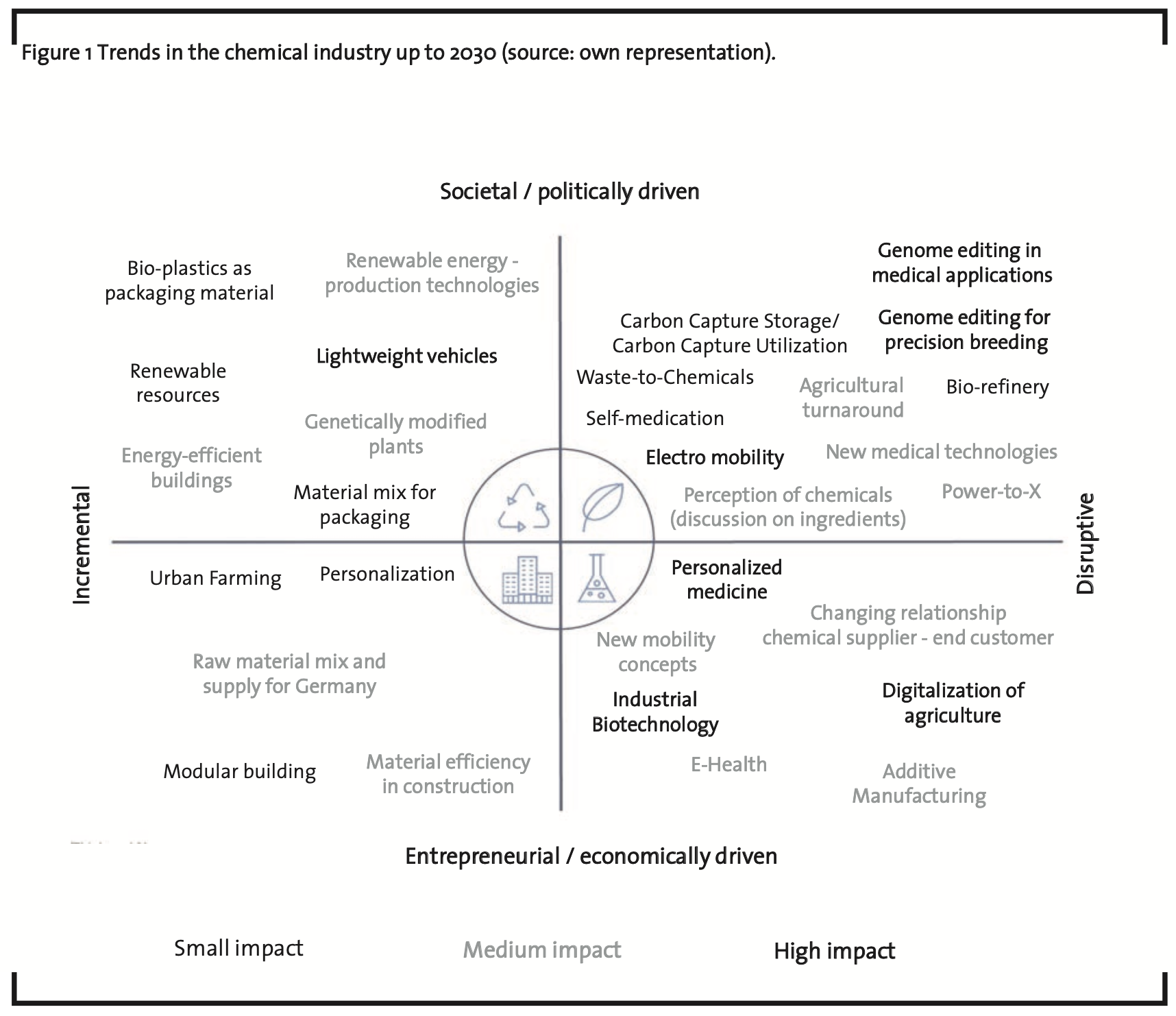

According to these distinction criteria, figure 1 categorizes the 30 trends examined within this study into four different groups. This is based on a joint assessment from the viewpoint of the participants in the expert workshops where the environment analysis was performed. The typeface of the trend names reflects the magnitude of the impacts on the chemical industry in Germany to 2030.

It emerges that many innovations in important business fields of the chemical industry like the automobile, construction and packaging industries but also in production processes like industrial biotechnology will rather come about stepwise. But in fact, an unusually large share of the changes for the chemical industry, which can already be predicted for the coming years due to product and technology innovations, have a disruptive character.

A number of these developments are closely connected with the advancing digitalization of business models, as is highlighted by the examples of additive manufacturing, digitalization of agriculture and e-health. Furthermore, many developments – especially in the upper half of the graph – have an obvious reference to sustainability topics and circular economy concepts (e.g. renewable resources, renewable energies, carbon capture storage, carbon capture utilization, bio-refineries, bio-plastics). Many of these trends also point to an increasing “biologization” of the chemical industry.

Thus, the analysis of developments in the chemical industry’s environment reveals two thematic focal points that can be subsumed under the headings “circular economy” and “digitalization”. Both topics will trigger transformation processes that will cover not only individual companies but the chemical industry and the economy as a whole. Business models and the distribution of roles in industrial networks will change considerably in the coming years.

At present, many industries are evaluating the potentials of digitalization. This tends to be linked with far-reaching changes in the structure of the industrial value chain. Therefore, digitalization is not only a trigger for fundamental change in the environment of the chemical industry. It also offers the opportunity to increase process efficiency and, above all, to open up perfectly new business and service sectors. Society and politicians demand the further development of circular economy concepts, in order to achieve sustainability goals. From the viewpoint of companies, this brings growth potentials – as products and services from chemistry can play an important role in closing the material cycles of the chemical industry’s customer industries. Furthermore, this tends to influence the perception of the chemical industry: Part of the general public still has an insufficient picture of the industry as a major innovation driver and problem solver for the main sustainability topics.

So far, the interplay between circular economy concepts and digitalization has largely gone unnoticed. VCI and Deloitte’s analysis have shown that there are significant parallels in the structures of digital and circular business models which result in similar requirements in the companies. Moreover, digitalization can benefit the expansion of circular economy models. In the light of these interactions, it makes sense for the study to give emphasis on both focal points and to examine them together regarding their challenges and the ensuring recommendations for action.

The cumulative occurrence of many potentially disruptive developments, especially in the fields of digitalization and circular economy, is unusual, requiring high responsiveness and ability to innovate. Many of the developments discussed in the environment analysis – particularly the intensive use of data as production input – open-up further growth potentials if the companies use the connected chances. At the same time, there are huge risks of non-chemical competitors building mar- ket power and trying to take away value creation shares from the chemical industry.

3.2 Digital transformation of the chemical sector

Digitalization offers an opportunity for chemical companies to collect extensive data in their own businesses, then evaluate and utilize it to improve operational processes within the company. Due to new technologies and a systematic collection of large data volumes (digital bulk data, e.g., on customer behavior and preferences, utilization of products, environmental properties of products), digitalization opens new opportunities to make further improvements in the efficiency of processes and operating models, and to develop new business models. In future, data utilization will therefore become more and more important for value creation in the chemical sector. It can be split into three categories:

Transparency and digital processes as the first category, include the collection and initial utilization of comprehensive process data within the company. These lift efficiency potentials in the context of largely unchanged manufacturing and business models. Especially in its continuous and discontinuous production processes – but also in business processes – the chemical industry is comparatively advanced in this respect. Even in an industry that is already comparatively advanced in this respect, digitalization offers new technologies for progress, for example, by further automating manufacturing processes.

Data-based operating models intensively utilize operational big data, external data (e.g., about the behavior of markets, customers, and competitors), and advanced analytical methods for smarter decision making and higher efficiency. The industry is currently driving developments in areas like predictive maintenance, networked logistics, and the application of concepts from virtual reality and advanced simulation (‘in-silico’) for research.

Digital business models describe value creation structures that fundamentally alter existing processes, products, or business models. What differentiates them is that products and services are digitally augmented to increase customer utility. Often this is not created by an individual company, but within digital networks in which different providers join to generate solutions for their customers. Customers are often actively involved in this process, enabling them to specify their individual requirements. The combination of digital services with products from the chemical industry in the digitalization of agriculture, in additive manufacturing (3D printing), and in e-health concepts in the health sector are examples of current developments in this area.

The industry currently finds itself in a phase of change and development. Digital processes and data-based operating models are applied more frequently. Half of small and medium-sized chemical companies (SME) intend to invest extensively into the digitalization of their processes and business activities. Likewise, the importance of digital business models to the future viability of the German chemical industry has been recognized, and digital business models are undergoing dynamic expansion: 30% of chemical SMEs in Germany already achieve 5% of their revenue through digital business models, and a further 40% intend to introduce digital business models in future years. Over the next three to five years, chemical companies are planning to invest a total of more than a billion euros in digitalization projects and new digital business models to achieve this. Digitalization will therefore become an integral part of the business and success model of the chemical industry.

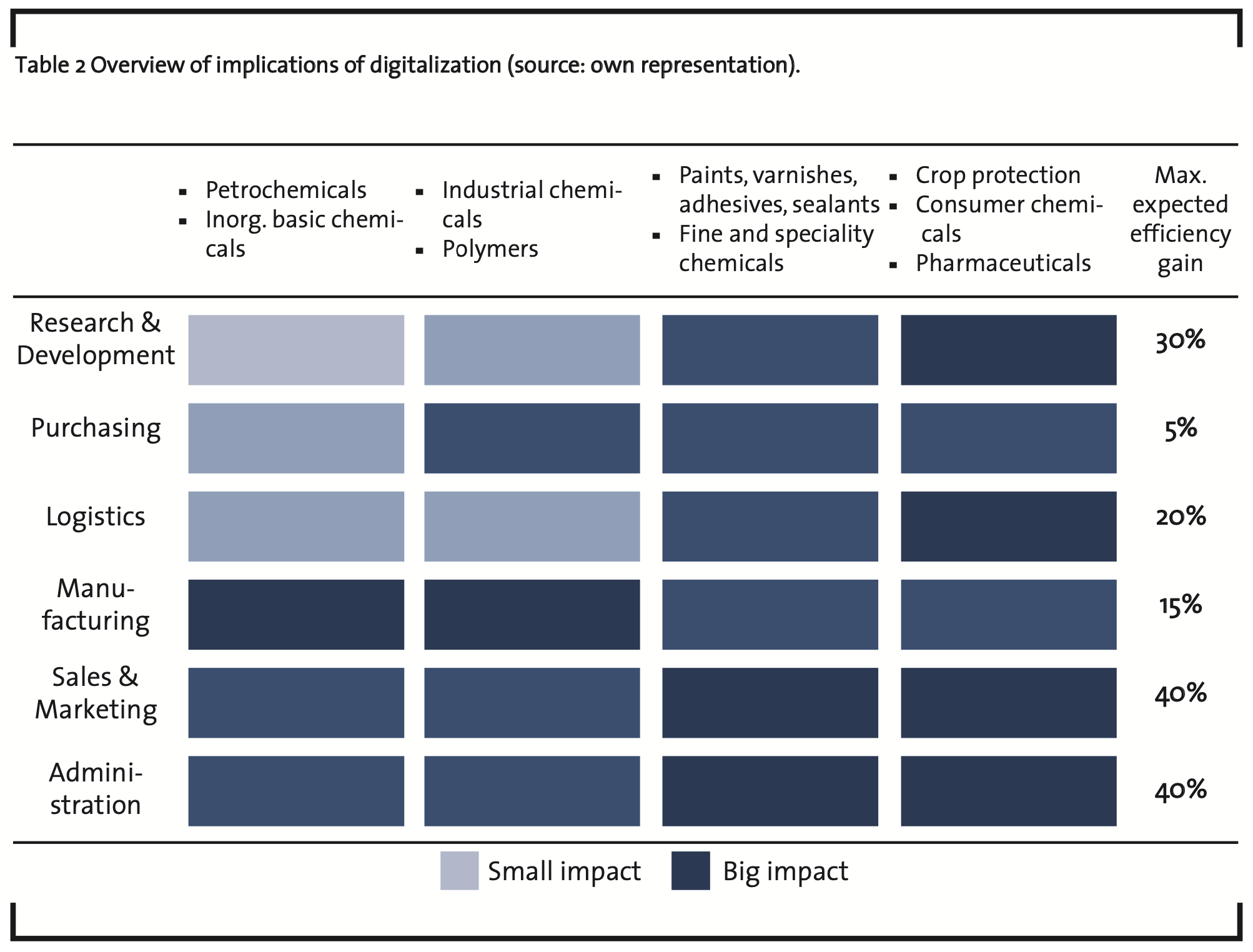

The potential for increasing efficiency through digital processes and data-based operating mod- els differs depending on the specific segment of chemical industry. Table 2 visualizes the expected efficiency gains on the value creation process. In upstream segments of the value chain, close to raw materials and energy, efficiency gains in manufacturing come into effect, for example through remote-controlled, preventative, and proactive maintenance and the corresponding operation of plants. In downstream segments, closer to the customer, efficiency gains lie more in the improvement of sales, marketing, and administration.

3.3 The chemical industry’s key role in the circu- lar economy

The change in public preferences toward sustainable production and consumption requires the development of new products and business models. In a circular economy, the chemical sector can utilize growth potentials: for example by supporting customers in reaching their sustainability targets or extending their core business with new circular business models, such as chemical leasing. Circular economy requires rethinking: the focus here is less on volume, and more on application utility and value-based pricing.

In this study, the circular economy concept encompasses all contributions toward protecting resources (such as raw material base and ecological systems) and includes the following measures:

- Increasing resource efficiency at all levels of the value chain (suppliers, chemical industry, customers).

- Extending the lifespan of products and components, as well as reducing resource consumption in the application phase.

- As far as possible, closing cycles by reusing, recycling, energetic utilization, and biological degradation, as well as maximally efficient utilization of residual materials.

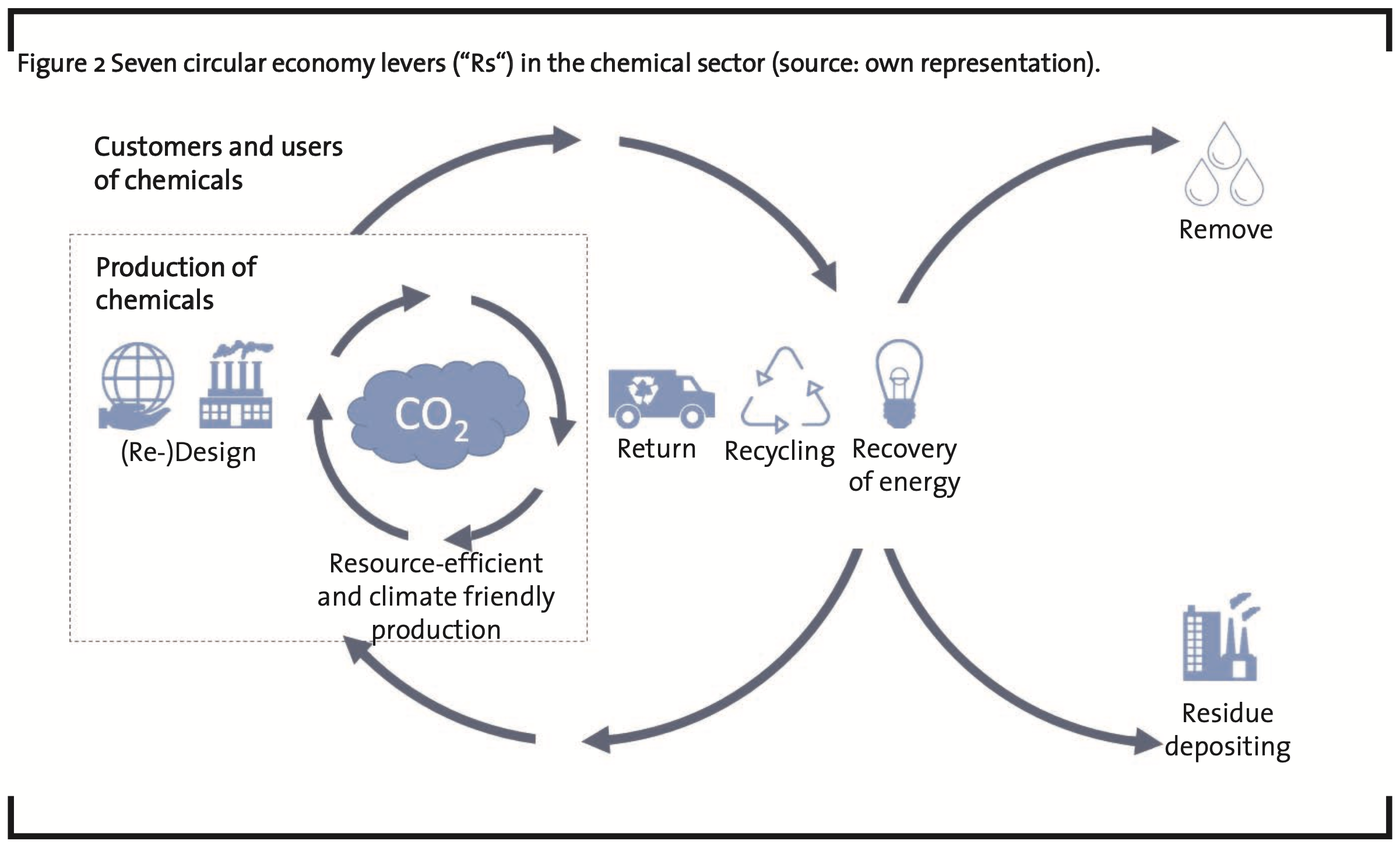

It is a task, a challenge, and an opportunity for chemical companies to take all aspects of the circular economy over the whole product life cycle into account. This begins with the production of base chemicals and extends over subsequent refining steps to the utilization phase of the (end) product. Options are avoiding waste by multiple usage, as well as higher efficiency through the utilization of byproducts, waste materials, and CO2 as raw materials (Waste-to-Chemicals and Carbon Capture Utilization). Additional possibilities are chemical recycling (also called feedstock recycling), biodegradability as CO2 cycle, and climate protection through “biologization of chemistry“ (use of industrial biotechnology, genome editing for precision breeding, biorefineries, and the utilization of renewables as raw materials). Following this broad definition of circular economy, the chemical sector delivers an increasing quantity of examples for circular applications.

Chemical companies are actively involved in sustainability and circular economy: all of the large companies analyzed in this study regard sustainability as an important aspect of their corporate strategy, and the concept of circular economy has entered corporate strategies through the levers mentioned above. Sustainability and circular economy are also very important to small and medium-sized enterprises. Over 20% of respondents are looking closely at the effects of a circular economy on their company. Just under 40% of the companies already have a sustainability strategy, and another 25% plan to introduce one in the coming years.

At a sector level, the chemical industry in Germany has already started a number of sustainability initiatives. Of particular importance in this context is the German chemical industry’s Chemie3 sustainability initiative.

3.4 Digitalization as enabler for circular business models

In all aspects of circular economy, the generation and analysis of digital mass data play an increasingly important role, as does exchanging data. Numerous technological options in the areas of connectivity, computing, and manufacturing technology affect the interface between digitalization and circular economy. Digitalization can thus enable the development of circular business models, accelerate them, and make them more efficient. The following approaches can serve as examples:

(Re)Design: Detailed, digitally collected and evaluated utilization patterns and specific data on environmental effects enable an improved, data-supported product design to enhance product performance and durability, and utility for the customer.

Resource-efficient production: Detailed and comprehensive insights into production processes as well as the analysis of process information and process simulation enable optimized processes and plant utilization with minimal application of resources. Advanced manufacturing technologies like modular production and robotics allow an increase in efficiency and in the degree of automation.

Return: The analysis of internal and external customer data (for example from social media via ‘Social Listening’) enables the identification of those cases in which a take-back business model holds advantages – for both customers and chemical companies. To do so, for example the consumption of chemicals over time is analyzed in comparison with other customers and set in relationship to other available information. By using customer data, e.g., through sensors in their manufacturing plants, chemical companies can draw conclusions about their products and recognize when they need to be replaced.

Recycling: Digital traceability and innovative processes, e.g. through modern sorting technologies, create transparency about material information. Recycling is made easier by efficient harmonization of waste capture and logistics, sorting and/or treatment, and subsequent utilization.

These examples reveal that there are significant parallels in the structures of future digital and circular business models. A significant commonality between circular and digital business models is that several companies deliver an extensive range of goods and services to their customers within network-structures. Companies that want to be successful therefore must combine technical and network competencies to develop innovative solu- tions and successfully establish these in complex and dynamic networks in the market.

In principle, chemical companies already have a high degree of network readiness and ability, because they have been operating in a complex environment from the start: they run complex manufacturing networks at integrated production sites or chemical parks, and deal with a large number of different suppliers and customers in a broad range of customer industries. However, the opportunities inherent in digital economic networks are not yet being fully exploited by the chemical industry. To better develop these opportunities, chemical companies not only need to recognize the development and dynamics of economic networks at an early stage, but also identify the role of their own company in these structures and organize themselves strategically. For many companies, these complex economic networks with new partners from other sectors are still unknown territory, characterized by uncertainties and risks.

3.5 The transition of SMEs

Although global companies dominate in public perception, the chemical industry in Germany is predominantly medium-sized. More than 90% of the chemical companies employ less than 500 employees. With an annual turnover of around EUR 55 billion, the “Mittelstand” accounts for almost 30% of the total turnover of the sector. Small and medium-sized enterprises are successful in their strategy of developing and occupying niches and are often world market leaders in their field.

The chemical and pharmaceutical SMEs in Germany are experiencing considerable adjustment pressure. The environmental trends examined in detail as part of this study as well as the digital revolution and the transformation into a circular economy will trigger change processes in the future. The majority of companies expect strong incremental changes. Around 30% of companies even expect significant, disruptive changes in the chemical and pharmaceutical business. This includes extensive adaptation of the product portfolio, the use of new process technologies as well as changes in the value chain and business models. Only 7% of companies do not expect change for their own company as a result of digitalization and the circular economy. In one thing, the surveyed companies agree: they see in the developments mainly opportunities for their company.

In order to strengthen the future viability of the 32% are planning to implement one. However, the goal is not yet reached: While one in four companies is already well prepared for the digital transformation, almost 30% of the companies recognize a need for action.

Overall, digitalization will leave its mark on the chemicals business. The majority of companies see the changes largely in the context of existing product portfolios, process technologies and established business models. However, almost every third company expects disruptive changes in their own companies as a result of the digitalization and networking of the economy. At the same time, digitalization has an overall positive impact. The opportunities outweigh the risks, especially for efficiency gains, but also for the development of new markets and the establishment of innovative business models.

Digital processes and digital operating models are already part of everyday life for many medium-sized chemical and pharmaceutical companies. Around 40% of companies claim to have digitalized production and business processes comprehensively, or to make extensive use of data to optimize their business operations. For the other companies (60%), however, digital processes and data-based operating models are only partially implemented. But that is about to change, with 50% of companies planning major investments in digitalizing their processes and business processes.

On the other hand, digital business models have so far had only a minor significance in the chemical and pharmaceutical SMEs. 70% of companies say they do not have digital business models. Nevertheless, the topic of “digital business models” is on the agenda of many SMEs. Around 40% plan to introduce digital business models in the coming company, the chemical industry invests almost 5% of its turnover in innovation. Traditionally, product and process innovations are very important. For 43% of companies, however, new business and ope- rating models are of high or very high importance, according to the member survey. Due to the high complexity of the changes in the environment of the chemical business, the innovative power of individual companies is often insufficient. The companies therefore rely on innovation cooperation. In their innovation projects, 75% of companies work years.

Digitalization in small and medium-sized enterprises is hampered by high demands on data protection, but also by fears of being unable to adequately protect one’s own data (data security). A shortage of IT specialists as well as a lack of IT skills among employees further inhibit the pace of digitalization. Likewise, the development is hampered by an insufficient technical infrastructure and lack of technical standards, especially at the interfaces for data exchange with partners. In contrast, rapid closely with suppliers, customers, universities or research institutes.

Digitalization has reached strategic importance in the chemical and pharmaceutical SMEs. More than half of the executives participating in the VCI membership survey claim to be intensively involved in digitalization related topics. 18% of companies already have a digitalization strategy and another digitalization, according to surveyed SME, would not fail due to lack of financial resources.

Sustainability and the “circular economy” are very important for the chemical and pharmaceutical industry in Germany. More than 20% of companies report that they are working hard to under- stand the impact of a circular economy on their business. 45% of the companies have a managerial or governance body responsible for managing sustainability. Nearly 40% of companies already have a sustainability strategy and another 20% are planning to introduce it in the coming years. One in five companies is well prepared for the changes in a circular economy, but nearly 30% see a need for action.

For medium-sized chemical and pharmaceutical companies, circular economy primarily means resource-efficient and climate-friendly production. But “recycling” and the “design of the products for saving resources over the entire life cycle” also play a major role in the company’s strategy. In contrast, the return and recycling of chemicals (chemical leasing) is not relevant for many companies because their products are not suitable for them. Many companies see potential to accelerate the expansion of circular economic models with the help of digitalization or to make them more efficient. The development is only at the beginning. Concrete projects are currently only available in about 8% of companies.

Almost all medium-sized companies are responding to increasing competitive pressure and to changing customer requirements with the tried-and-tested strategy mix: expanding innovation, promoting specialization and occupying niches, and seizing the opportunities of globalization.

Disruptive changes often require a readjustment of the corporate strategy and a review of existing business models. Only in this way can companies seize growth opportunities and remain successful in the long term. Many middle-sized companies have recognized this need for action and implemented a digitalization and sustainability strategy.

The economic policy framework conditions are rated mostly positively by the companies. However, the regulatory environment has recently deteriorated slightly. The problems with regulation are mainly in implementation and enforcement. 67% of companies rated the approval procedures as “slow and bureaucratic”. Concrete support can be provided by politics and public administration, reducing bureaucracy further, making laws more cost-efficient and speeding up approval procedures.

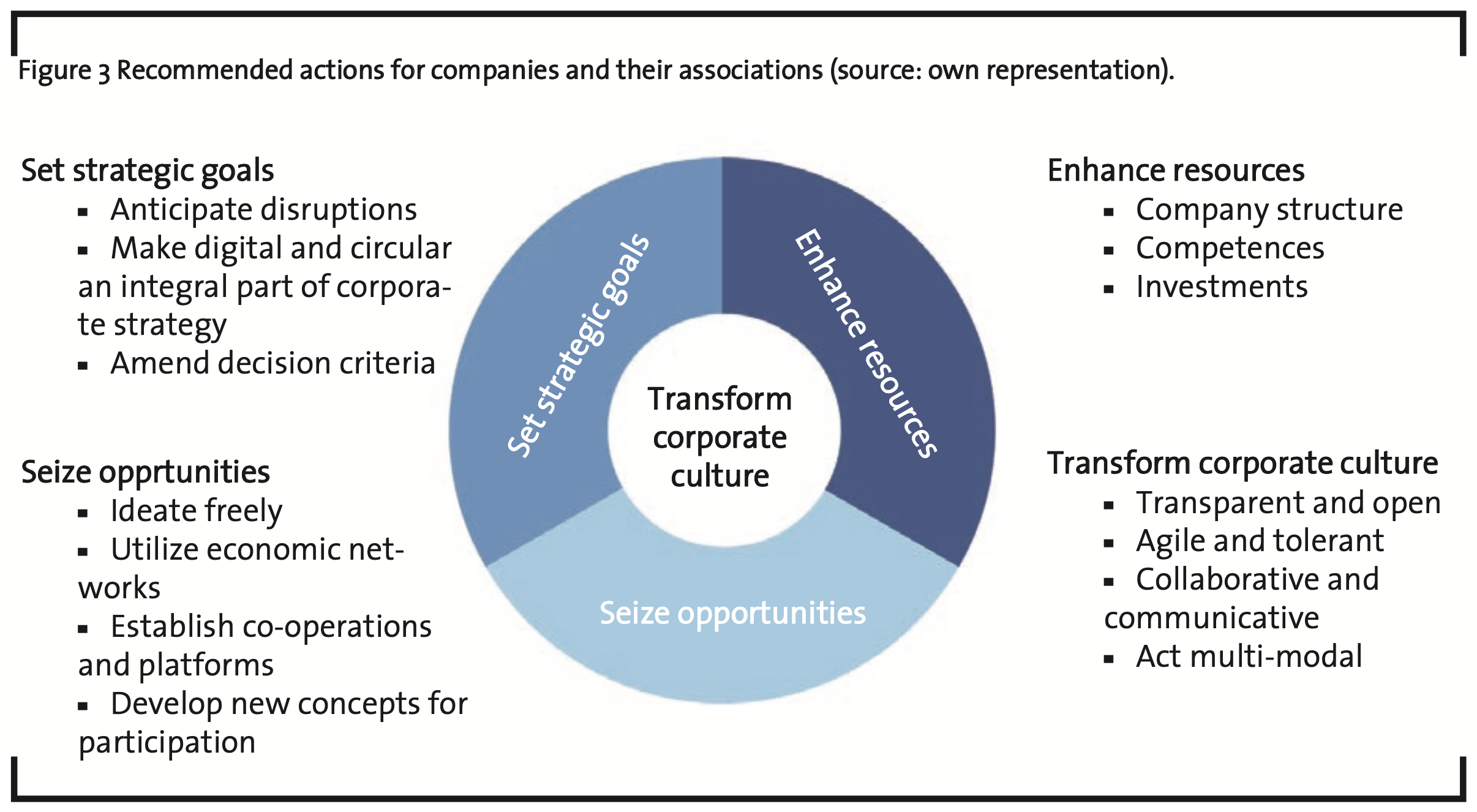

4 Recommendations to companies and their associations

Use the chances and set strategic goals: The future importance of digital business models makes it necessary for the chemical industry in Germany to look even more intensively into identifying, assessing and introducing such models. Business models developed by networks require a comprehensive analysis of incentive structures, value contributions and remuneration structures. Companies need to define digitalization, circular economy and innovation as elements of the corporate strategy. The interplay between digitalization and circular economy, too, needs to be seen for the business model. Furthermore, new assessment criteria have to be added to the classic performance parameters of business management. They should take into account the properties of new production and value creation structures (higher flexibility, smaller lot sizes/personalization, appraisal of existing and newly generated data).

Enhance resources: Digital and circular business models call for technical and network competencies. The chemical industry has a good starting position, as its core business is characterized by complex value creation and highly integrated (Verbund) structures and by cooperation between large businesses and medium-sized specialists. But these competencies and structures of chemistry need to be expanded and adapted, in order to overcome the remaining barriers and to fully use the chances for growth. Such change involves many risks and requires high investments in education, equipment and software.

Transform corporate culture: The successful development and scaling of new business models for digitalization and circular economy – especially at the interface between both fields – call for corporate cultures of start-up character. Innovation cycles are becoming shorter, and new products and business models need to be implemented in an agile and timely way. Important elements of the prerequisite corporate culture are transparency and openness, agility and failure tolerance as well as a culture of cooperation and communication, also across companies. In their operative activities, the companies have to cope with the potential field of tension between traditional business and new business models. Furthermore, they need to create structures that also allow them to operate in parallel within different models. This includes enabling and permitting the scaling of new business models that can be directed against the core business (“managed cannibalization”). Moreover, large parts of the chemical industry’s business model are based on protecting intellectual property: This is another potential obstacle to a fast cultural change towards openness and cooperation across companies and needs to be discussed in a frank manner. The associations should actively support the change in the industry’s culture.

Build up cooperations and platforms: Digital and circular business models require far-reaching cooperations, both within the chemical industry and across industries. Through its associations, the chemical industry can promote the development of platforms for knowledge exchange and initiating partnerships inside the industry, position itself as an open and attractive partner for start-ups and technology companies, and expand research collaborations. Chemical industry associations can actively support this by developing catalogues of criteria (best practice analyses, toolboxes, guidelines) for adequately assessing digital and circular business models and implementing them in the companies.

Develop new participation concepts: The speed and complexity of change can provoke rejections of these innovations. Beyond stronger communication, the associations and companies should open up their innovation development for a stronger participation of politicians and other interested groups in society. Thinking and acting in networks is necessary for the success of digitalization; this should also include the cooperation with societal stakeholders. For this purpose, companies and associations can jointly develop new participation concepts.

5 Conclusion

Chemical and pharmaceutical companies in Germany have shown many times that they are able to successfully master the tectonic shifts in their competitive environment; examples in the 150 year old history of industrial chemistry are changes in raw materials, relocation of growth centers to emerging economies, and the call to make business more sustainable, which has been receiving broad public support recently.

The key to the sector ́s competitiveness is the innovative power held in chemical and pharmaceutical companies: new and improved molecules, production and business processes. In Europe, the sector has been characterized by globalization, specialization, and focusing on the core business since the 1980s. The industry has now reached the next level: The era Chemistry 4.0. Digitalization and circular economy are key characteristics, and these two elements will fundamentally alter the way we work, as well as support sustainable management. Digitalisation the chemical industry offers new opportunities as well as risks. Research and development, manufacturing, and business models will be transformed. It is not easy to separate myths from real risks and opportunities, take appropriate measures, and gain a competitive advantage. This transformation offers great opportunities for the highly developed chemical industry in Germany in terms of enhancing its global competitiveness.

The chemical and pharmaceutical industry’s innovative processes, products, and services make a significant contribution to sustainable development of our society. The sector will continue to be a traditional supplier of materials, while the role as a service provider will grow in importance at the same time.

References

Bitkom (2016): In 10 Schritten digital – Ein Praxisleitfaden für den Mittelständler, available at https://www.bitkom.org/noindex/Publikationen /2017/Leitfaden/In-10-Schritten-digital-Markus-Humpert/170601-n-10-Schritten-digital- Praxisleitfaden.pdf, accessed 24 June 2017.

Commerzbank (2016): Fachkräftemangel und fehlende Qualifikation bremsen digitale Transformation, available at https://www.commerzbank.de/de/hauptnavigation/presse/pressemitteilungen/archiv1/2016/quartal_16_02/presse_archiv_detail_16_02_58570.html, accessed 01 June 2017.

Deloitte (2016): Deloitte EMEA 360° Boardroom Survey, available at https://www2.deloitte. com/ro/en/pages/about-deloitte/articles/ Deloitte-EMEA-360-Boardroom-Survey-Agenda-priorities- across-the-region.html, accessed 15 October 2016.

Deloitte (2016): Global Digital Chemistry Survey, available at https://www2.deloitte.com/de/de/pages/consumer-industrial-products/articles/globaldigital-chemistry-study2016.html, accessed 13 February 2017.

Deloitte and Wehberg (2016): Tripple-Longtail-Strategie, available at https://www2.deloitte.com/de/de/pages/consumer-industrialproducts/articles/triple-long-tail-strategie.html, accessed 13 May 2017.

Siems, D. (2017): Der schleichende Abstieg des Standorts Deutschland, available at http://www.xing-news.com/reader/news/ articles/757019?link_position=digest& newsletter_ id=22870&toolbar=true&xng_share_origin=email, accessed 02 June 2017.

VCI and Deloitte (2017): Chemie 4.0 Wachstum durch Innovation in einer Welt im Umbruch, available at http://www.xing-news.com/reader/news/articles/757019?link_position=digest& newsletter_id=22870&toolbar=true&xng_share_origin=email, accessed 02 June 2017.

VCI and Prognos (2017): Die deutsche chemische Industrie 2030, available at https://www.vci.de/services/publikationen/broschuerenfaltblaetter/vci-deloitte-stuide-chemie-4-punkt-0-langfassung.jsp, accessed 30 January 2018.