Design thinking as driver for innovation in the chemical industry

In a time of increasing market pressure, managers value innovations as a precious currency. While shifting the focus away from incremental innovations at the level of molecules, companies in the chemical industry should consider a more systematic approach to the development of ideas during the innovation processes. However, solely aligning all research activities with the upcoming megatrends for the industry is not sufficient. This article empirically demonstrates the strategic relevance of Design Thinking as a method to not only overcome typical barriers in the innovation process but also to guide stakeholders through all iterative stages required for innovation.

1 Necessity of innovation for chemical companies

The chemical industry has undergone large scale change since the 1990s. Up until then, the focus of innovation lay on the discovery of new molecules, and certain major improvements such as heterogenic catalysis, new purification methods and new forms of spectroscopy which drove the development of the chemical industry.

Nowadays improving the efficiency of existing production processes has become the main priority and there have been no major breakthroughs in new products since the 1950s (Whitesides, 2015; Schröter, 2007). As Lehr and Auch have pointed out, these incremental efficiency improvements will result in increased earnings in the short-term, but may not be sufficient for sustainable success (Lehr and Auch, 2017). Hariolf Kottmann, CEO of Clariant, holds the opinion that “a company that seeks to be sustainably successful must […] change and develop permanently” (Kottmann, 2016), underlining the importance of innovation and transformation in the chemical industry.

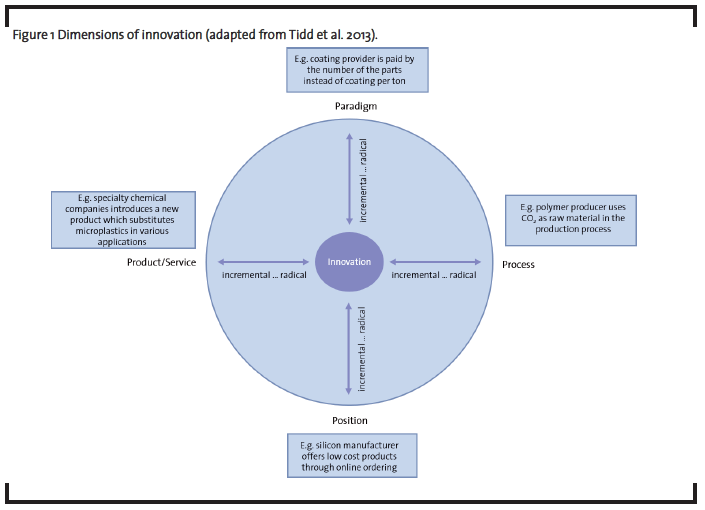

Taking the innovation management perspective into account, chemical companies have predominantly been good at incremental innovations in products and processes. However, innovations can be characterized in several ways. Besides thinking in the aforementioned categories, managers and decision-makers should also consider position and paradigm innovations as sources of competitive advantage. Figure 1 demonstrates the four categories of innovations, namely:

- Product innovation: changes in products/services that an organization offers

- Process innovation: changes to the ways in which products/services are created and delivered

- Position innovation: changes to the context in which the products/services are introduced

- Paradigm innovation: changes in the underlying mental models which frame what the organizations does

The other dimension depicted in Figure 1 indicates the degree of novelty for the respective categories, ranging from incremental (“do what we do but better”) to radical (“new to the world”). As the representation illustrates, there is no strict demarcation for either dimension. (Tidd and Bessant, 2013).

Another influencing factor is the increasing concentration of chemical production in Asia. While in 2005 the EU held the biggest world market share at 28.2%, this value almost halved by 2015, reaching 14.7%. In 2016 the EU occupied third place behind China (39.9%) and the NAFTA region (16.5%). Local industry struggles to participate in the overall growth of chemical sales. The €434 billion increase from 2014 to 2015 was mainly driven by China’s high growth levels, the rest of the world accounted for only 25%. And this trend is expected to continue as the Cefic predicts China’s market share will grow to 44% and the EU’s will drop further to 12% by 2030 (Cefic, 2016).

At the same time the chemical industry is experiencing a decline in sale prices, mainly caused by falling oil and naphtha prices (Bock, 2016). The expected continuation of rising energy and labor costs accounts for additional pressure on the profit situation (BAVC 2013/2014, BAVC 2016).

Therefore, European chemical companies need to find innovative business models to position themselves and their products on the market and find new ways to sustain competitive advantages. Otherwise, they will be easy prey for investors and takeovers, as Gapper recently argued in the Financial Times (Gapper, 2017).

2 Drivers for innovation

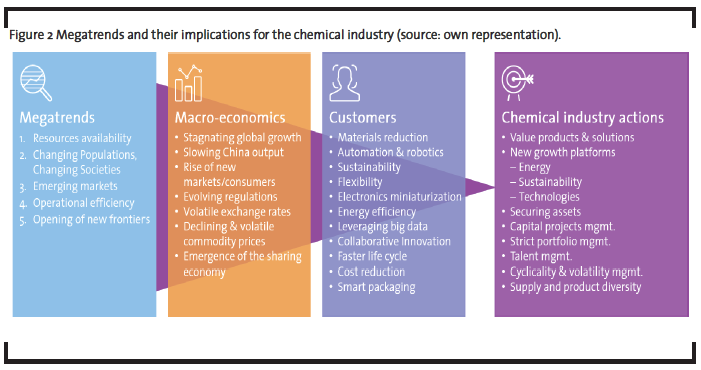

The best way to understand the changes in the chemical industry is to look at the underlying megatrends that form the framework for innovation activities. The Accenture Chemical Industry Vision 2016 identifies these megatrends as “Resource availability”, “Changing populations, changing societies”, “Emerging markets”, “Operational efficiency” and “Opening of new frontiers” (Accenture Chemical Industry Vision, 2016).

Resource availability describes the current situation that some resources are available in abundance while others are becoming – or predicted to become – scarce. The finite amount of fossil fuel left as feedstock is one example for how this trend affects the chemical industry directly. Water- and carbon emissions management, as well as renewable energy sources are further ones. The result of these trends will be the emergence of circular processes where product design enables feedstock generation from waste.

Changing populations, changing societies summarizes trends like the aging of the population in Europe, urbanization and the changed expectations of generations that grew up with technology, a rapidly evolving world and environmental responsibility. The effects are shorter production lifecycles and the necessity for companies to provide an unmistakable product experience.

The increasing demand for chemicals in emerging markets like China, India or Mexico is both opportunity and threat. The former entails chances to participate in growth, while the latter involves increased competition from new players emerging together with those markets.

The convergence of software, hardware and communication technologies leads to increased and improved automation (e.g. through robots and 3D printing) and thereby to a higher level of operational efficiency. A side effect is that labor as a factor of production will decrease in meaning.

The opening of new frontiers involves, on one hand, the exploration of previously inaccessible commodity sources, such as the seabed or deepearth mining. On the other hand, these techniques, together with the pushing of the boundaries in both private spaceflights and the aerospace industry, require new high performance materials and thus offer new opportunities for the chemical industry.

To remain relevant and competitive, the current and next generation of CEOs must manage these megatrends and drive innovation activities forward (Utikal and Leker, 2015). Key to such innovation is the digitalization of both the administrative and – more importantly – the production processes, Track & Trace, sensors, analytics and the internet of things (IoT) are just a few examples of the vast range of possible applications, with IoT being among the most important for it represents the connection between a digitally enabled enterprise and the physical world (Accenture Chemical Industry Vision, 2016).

The digitalization of production processes fosters greater efficiency and flexibility, as well as higher levels of automation; it also provides real-time insights into operations, leading to increased uptime and reliability of production plants. Another advantage is the data stock that can be used in practices like business analytics, predictive maintenance and demand sensing, which offer new opportunities to reduce the capital employed and improve capacity management. Additionally, the flexibility and automation advantages of digitalization make smaller production quantities cost effective, thereby facilitating new levels of product personalization.

The next step after the digitalization of processes is to create new business models making the most of the resulting possibilities. As Hariolf Kottmann, CEO of Clariant, said: “Digitalization will succeed in turning a customer’s requirements into entirely new business opportunities reaching far beyond the actual products” (Kottmann, 2016). One resulting opportunity for chemical companies is to move from being a simple supplier to being a service provider that guarantees a certain outcome instead of selling a one-off physical product. These outcome-based business models require the performance of the service provided to be measurable, which in most cases can be achieved by digitalizing the affected processes. Close collaboration between supplier and customer is also necessary. Such collaboration in combination with high levels of personalization leads to customer bonding through relatively high switching barriers and can be the first step to building intra-supply-chain partnerships. Rachael Bartels, Global Chemicals & Natural Resources Lead at Accenture, thinks that “companies will need ‘connected innovation’, which breaks down internal silos to include more areas of the organization, and also forms external links with alliance partners, universities, customers and customers’ customers”. This collaboration can offer new opportunities, including the possibility to innovate the traditional R&D process to become more open, agile and disruptive (Accenture Chemical Industry Vision, 2016).

Technology and processes are not the only areas that require innovation. The workforce must be adapted to the changes as well. Digitalization requires skills in new fields like advanced analytics, artificial intelligence, machine learning, cyber security and robotics technology, as well as data engineering, computer science and data modelling. These can be provided by a new type of employee; the “data scientist” (Kersten et al., 2017). In general, workforces must become more flexible and build their own innovation ecosystems, including freelance engineers, researchers, students and strategic-partner employees. Especially when bearing in mind that a big wave of retirement is coming up, with loss of experience, knowledge and customer relations, companies would do well to practice employer branding to augment their attractiveness for new talents and be aware that they are in competition with companies from other areas of the digital economy (e.g. Google and Amazon) for these future employees.

3 Typical barriers in the traditional innovation process

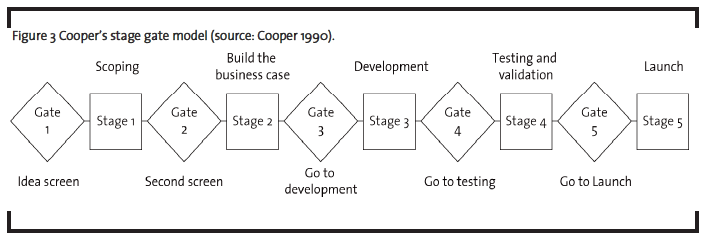

The stage gate model by Cooper will serve as an example to provide an overview of the traditional innovation process in the chemical industry. Here, the innovation process is divided into five stages: “Scoping”, “Build the business case”, “Development”, “Testing and validation” and “Launch”. After each stage, there is a so-called gate, representing the decision to continue or to stop the project (Cooper, 1986). Cooper found that many companies had deficient or nonexistent evaluation procedures for their projects. So, by implementing defined stage gates for “Go/Kill” decisions in the process, situations could be avoided whereby projects run like unstoppable “express trains” (Cooper, 1990). On the other hand, this formalized approach can lead to inflexible, lengthy and risk minimizing innovation processes.

In their development of new products companies often encounter barriers that hamper the processes. These barriers can be divided into two categories: Internal and external ones. For the chemical industry, the most influential of the external barriers is the increasing restrictiveness of regulations, especially since the introduction of the REACH in Europe in 2007. The costly and timely authorization processes for new products can act as a deterrent from developing new products and provide an additional risk factor on the way to the market. In Europe, as elsewhere, weak venture capital markets are responsible for further difficulties affecting companies that do not have the necessary capital for bigger innovation projects. This restricts them to smaller incremental innovations. Another factor is regulation and the public acceptance of new products. In a society that is increasingly concerned about safety, health and environmental responsibility, companies must develop sustainable products if they are to remain meaningful.

The internal barriers should not to be neglected either. There is, for example, the cannibalization effect, referring to a situation where a new product consumes the sales and demand of an existing or related product, potentially leading to a push back to support the existing business. This can be illustrated at the example of Kodak. Kodak once was the leader of its industry. Nowadays, Kodak serves as an example, where the management has failed to react adequately to external triggers (e.g. changing technology and customer expectations). Business schools study companies like Kodak and dissect their strategies to see why they were not successful to adjust in time. Analogous to Kodak, the chemical industry is now confronted with fundamental change. Another example is described by the filtering effect that the existing business model can have on the flow of information in R&D and innovation teams. Prahalad and Bettis (1995) call this effect the “dominant logic”, which results in situations where new opportunities not fitting the current business model are more likely to be dismissed or even not thought about in the first place (Chesbrough, 2010). While this can be solved quite easily by building innovation teams consisting of both long-term members of the company and new hires (Govindarajan and Trimble, 2010), another barrier cannot: The limited resources of the company – both of the human and the financial kind – have to be split between the ongoing business and the innovation projects. Accenture’s Chief Strategy Officer, Omar Abbosh, has just recently released a blog article on this topic (Abbosh, 2017).

Companies are driven by their shareholders to maximize short-term earnings. This effect has increased since the 1990s and forces companies to focus on incremental rather than disruptive innovation, as has been stated by Christensen (Christensen, 2011). Where this is the case, company leadership has to be more courageous in order to prevail in a climate of mergers if they are to remain independent and develop their business. Normally, the new business model is far less profitable than the established one, so the reallocation of resources clearly contradicts the goal of making (short-term) profit (Chesbrough, 2010). This often leads to rivalry between the employees in R&D and operations and, when paired with an inadequate interdivision information flow, can even cause animosity (Govindarajan and Trimble, 2010).

Traditionally there is a “no failure culture” established in many firms with the effect that risky, disruptive innovations with the potential to achieve breakthrough are not pursued, and only incremental improvements are made. Kersten et al. (2017) propose a “fast failing culture” to overcome the barriers, meaning that innovation projects are allowed to fail at an early stage which may prevent them from being pushed to launch once it becomes clear that they won’t bring the expected outcome. This would enable the opportunity to learn from the failing projects and additionally foster the eagerness to experiment and take risks (Kersten et al., 2017). Additionally, companies will have to break down silos and build a more diverse workforce with respect to ethnicity, gender, age and profession. New ideas require open minds, freedom for cooperation and risk taking. Companies need scouts to observe, discover and understand new business model trends (Utikal and Woth, 2017).

Innovation takes place at the intersection of departments and is facilitated by an innovation eco-system. As Accenture’s CEO, Pierre Nanterme, said at the last Accenture SAP Leadership Council in June 2017, “The challenges businesses face today are so complex, no single company can navigate them without partners who share a common vision. The innovation ecosystem is a powerful part of the new reality we operate in […] and key to a successful ecosystem is collaboration between technology providers and business and, of course, clients. In other words, disruptors who are not afraid to disrupt each other to drive innovation and growth.”

Besides new products, business models can and should also be innovated in order to sustain customer centricity. As Gassmann postulated in 2013, “In future, competition will take place between business models, and not just between products and technologies” (Gassmann, 2013). Therefore, new methods to ideate products and solution design are necessary. One method that is more and more widely used in different industries is the approach of “Design Thinking”, which needs to be embedded in a broader structure.

4 Design Thinking as a method

Design Thinking is not a new approach per se, but put into context, it is a form of product design that has been established over many years. What is new is the specific field in which Design Thinking is applied, which goes beyond the application of product design. The roots for “Design Thinking” were established in the year 2005, with Hasso Plattner` s establishment of Design Thinking at SAP and his engagement for raising awareness about Design Thinking, for instance through founding the DSchool at Stanford and the Hasso-Plattner-Institut in Potsdam. Ever since, Design Thinking has been increasingly put into practice in the IT-service industry (e.g. Software, Hardware, IT-Consulting).

The Hasso-Plattner institute refers to Design Thinking as a systematic approach to complex problems from all aspects of life. In contrast to conventional approaches, starting with technical solvability, Design Thinking puts customers’ needs as well as user-centered inventions at the heart of the process. Furthermore, Design Thinking requires a steady back coupling between the innovator and the customer (see www.hpi.de).

At the same time, also since 2005, we are observing how traditional industry borders are unwinding: companies like Google, Amazon, Facebook and Apple have stepped into several “Markets” with their new products and services, and have proven extremely successful with their user-centric functions and user-friendly application design, taking away a considerable amount of market share from well established companies within traditional industry segments. These new products differ from existing ones in the market for the following reasons: they meet the needs of the individual, solve day to day challenges, make the life of the individual easier, and, because the individual`s needs are at the core of such products and services, they are, in a nutshell, truly customer-centric. The „Total Perceived Pain of Adoption” (TPPA) for those products is extremely small (see Pit Coburn, The Change Function: Why Some Technologies Take Off and Others Crash and Burn). Often, customers are willing to pay an additional amount for these kinds of products and services as they realize the value of their benefit.

This is the crux of Design Thinking, from its underlying mindset and culture, to the design and selection of tools and exercises, all the way to the implementation of a project: the unconditional focus on the user group of these products or services, where the user’s needs are researched and understood from the very beginning in the best possible way. The idea-generation to follow is built upon the implicit needs of the future user. The technology to be applied for the solution is secondary, and so is the business model. Nevertheless, both aspects are of essential meaning and the innovation (per Schumpeter = invention plus market success) emerges as all three aspects overlap: focus on the end user & application of a suitable new technology & marketing of a functioning business model.

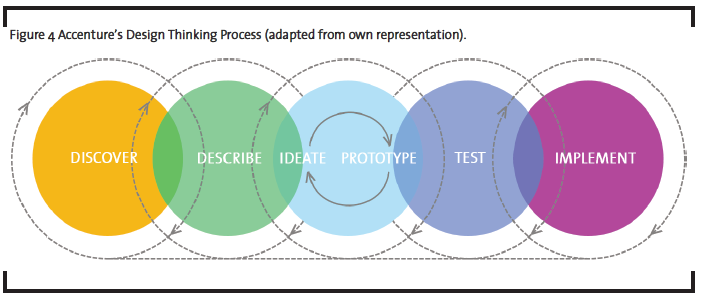

Accenture’s Design Thinking process follows different phases, from “Discover” through to “Implement”, while embedding feedback loops and early prototypes (see figure 4). The crucial aspect of difference compared to other processes (e.g. Stage-Gate) is the flexibility – and encouraged – procedure of going back and forth in the phases, depending on the feedback from prototypes and user testing.

All of this happens in a unique work culture, which is unfamiliar in Germany, as well as in many other countries. This culture is defined through:

- the combination of experts or expert knowledge from diverse areas –a vital basis for disruptive innovation, amongst other things – instead of the silo mentality familiar to all traditional industry segments;

- ”early” prototypes, built based on a minimal heuristic basis, with new products tested right away as well as improved iteratively – instead of a “waterfall approach”, where a product is created only at the end of a project and may not necessarily work as desired by the user, yet often needs to be implemented, as the project budget has often been used up;

- an iterative,agile and fully aware project management team, with the application of one of the established DT-Phase-Models – instead of a gradual “waterfall” based project management team;

- the “permission” to fail, often and early, or better yet: the opportunity for quick success, by working with an “early” prototype, which is purposely not perfect, but rather built to be continuously improved in an iterative process all the way to its market maturity, with all learning from early prototypes fed back into the process through closed feedback loops – instead of a mentality which is solely success-driven.

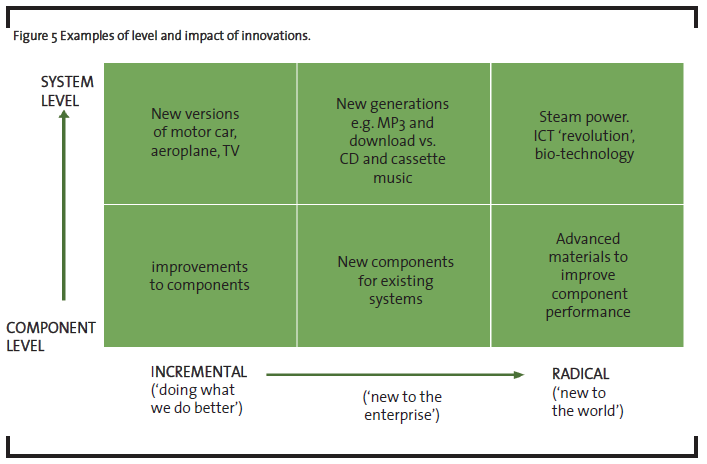

The success of this work culture, identifiable in several Apps, MP3-Players, etc. speaks for itself. Moreover, the DMI Design Value Index shows that companies that apply Design Thinking achieve “Outperformance”, as this approach facilitates out-of the box thinking and collaboration, thus easing the way towards more radical innovations (see figure 5), while a stage gate process usually enables a more incremental progress.

However, Design Thinking is “not only” about product -and service innovation. It is a matter of increasing the problem-solving competence for the user, or for the companies using it for all kinds of product and service innovation. Design Thinking is also increasingly used in revising internal company processes, especially in areas such as Finance & Accounting, Supply Chain, Personnel Administration, and Client Management, thereby complementing what traditional methods, such as Lean Six Sigma, have to offer.

It should be emphasized, that the application of Design Thinking is a fundamental building block for Lean “User Experience” (UX): for some time now, many products have no longer been defined through their hardware and product composition, but rather through the integrated software, the User Interface (UI) and, moreover, the overall UX, which is developed for the user of a device or service. For more information on this topic, see Accenture’s Technology Vision 2017 (Accenture, 2017).

Overall, the “Chemical” industry is relatively steady and has not yet been challenged by disruptive innovators, unlike, for instance, the telecommunications and media industry, automotive industry, energy industry etc. Nevertheless, pressure on this industry is increasing. With regards to the different fields of innovation in the chemical industry, Design Thinking seems to be especially valuable if innovation is encouraged not only at the product-, but also at the system level. To create encompassing solutions for customers in the relevant arenas of the chemical industry such as farming, treatment of illnesses or mobility, the boundary spanning approach of Design Thinking seems especially valuable: experts from different departments and companies could work together using the Design Thinking method for creating valuable solutions for relevant customers.

The business divisions of many chemical companies demand support from their IT departments in the forward-looking modernization of their infrastructure and in the utilization of the new technologies which are needed to create innovation and to establish those innovations in the market. Digital technologies are heavily discussed amongst the chemical industry players, both for the support of business segments, as well as the modernization of the support of business processes like Finance, CRM, SCM and HR. Therefore, current technology trends and traditional competition, rather than “New Entrants”, are above all the driving forces that trigger the application of Design Thinking in the chemical industry.

5 Use Cases of Design Thinking in the Chemical Industry

Three current project examples may illustrate the application of Design Thinking in the chemical industry:

1) Design Thinking for Process Innovation – A leading, global vendor of specialty chemicals:

At their annual meeting in Germany, Accenture was asked to execute a creativity workshop about UX for the existing SAP architecture of a vendor of specialty chemicals.

In a series of workshops a team of Accenture consultants worked together with global IT experts from the client company. In different iterations, the As-Is-Situation was developed in interdisciplinary groups and a vision for the further development of the system was created.

Outcome: The client praised the collaborative approach and the professional performance. He concluded that highly innovative solutions had been created in an agile way. The collaboration with members from different departments prepared the way for a smooth implementation.

2) Design Thinking for Process Standardization – One of the TOP 10 chemical companies, which is, amongst others, a leader in the chemical agriculture sector (e.g. fertilizer, herbicides):

The global regulation of herbicides demands a gapless tracking of the distributed chemicals across all supply chain levels. This encompasses the delivery of the products to clients and the storage of the product at the client site as well. Even though the parent company provides a Supply Chain Track & Tracing System, the different basic components are not satisfactorily integrated for the end user in the production part of the process. Furthermore, the NatCos of the parent company partly developed non-standard solutions in a local language. As a result, a gapless tracking of the products was impossible. This situation was analyzed in a Design Thinking project. Various subject matter experts were brought together to analyze the status quo and to develop viable solutions. Design ideas for the UI were developed, that consisted of appropriate functionalities for the end user. The end users in different context situations were always integrated into the development of the solution.

Outcome: The Design Thinking approach led to impressive results. Soon after starting, the paper prototype was transformed into a wireframe/mockup and could be tested with the end user. A new basic architecture was developed as byproduct, which now is also being discussed within the company. The Design Thinking method came up with creative but pragmatic solutions.

3) Design Thinking for Business Model Innovation – A mid-sized provider of specialty chemicals:

The IT department of a mid-sized provider of specialty chemicals identified a profit and growth potential for their company due to the “Artificial Intelligence” trend. They wanted to explore and evaluate the opportunity and wanted to identify and implement some initial projects to test the assumptions. In collaboration with Accenture`s subject matter experts and the German Research Center for Artificial Intelligenc (German: Deutsches Forschungszentrum für Künstliche Intelligenz, DFKI), an ideation workshop with Design Thinking tools was conducted. The initial possible applications were identified and assessed from multiple perspectives. Based on the workshop result, a roadmap for future pilot projects was developed. These pilots can now be iterated quickly and learning can be integrated in the ongoing pilot design.

The overall feedback that was provided by these and other clients was that Design Thinking enabled the diverse teams from different parts of the respective organizations to quickly align and get into a productive working mode. This created a productive and collaborative environment and enabled impressive ideas and prototypes to come to life.

6 Outlook

As a leading industry consultant, Accenture is often approached by chemical companies who want to re-evaluate their business models, product portfolio or go-to-market strategy. These chemical companies consider new approaches to customers, business models, innovation, operations and the workforce. They will need to take advantage of evolving new methods, like Design Thinking, to achieve and sustain high levels of business performance. Two current trends may be used to illustrate the benefits of Design Thinking:

The area of Circular Economy holds a lot of potential, e.g. with renewable sourced materials, a mass balance approach or the growing trend of “Eco Design”, meaning product design in a way that already considers easy and complete recycling processes at the end of the product lifecycle. Accenture has recently published an extensive study on the topic of Circular Economy with the CEFIC (CEFIC 2017). Design Thinking approaches may help to bring the different players in the value chain together in order to analyze the business potential of the “circular economy approach”. By working together in diverse teams with a very strong customer focus and in an iterative manner, viable business models may be identified that will succeed in the market. The boundary-spanning and focused approach of Design Thinking will help to bring the “grand ideas” down to “viable profits”.

The area of Outcome-based product design means that a product is not sold based on volume any more – as has been the predominant mode of transaction until now – but based on measurable performance. This can for example entail, that a coating is not paid by the ton but by the number of readily coated parts. This means a paradigm shift in the suppliers’ logic from the goal to sell as much coating as possible towards a most effective use of chemicals to achieve the best results and a predefined quality level with as little use of chemicals as possible (CheManager 2017b).

In order to capitalize on the current trends, Accenture considers technology as a key enabler. The targeted application of digitalization capabilities is seen as a necessary condition to reap the benefits thereof. This is in accordance with the evolving customer needs. As Accenture has learned from Andreas Zöller, Strategic Marketing and Business Development Leader EMEA at DuPont, the next level of innovation in plastic products might be the creation of smart products with service innovation bundled to the polymer. Here, untapped potential could be leveraged to reduce costs, increase revenue as well as to minimize risk of new product introduction while decreasing the development time.

For this approach, raw material suppliers need to collect real-world data about the behavior of the product in end-user applications, complement those with existing data models raw material supplier typical generate and introduction of the entire dataset into the model that is being used in product design. Machine learning could enrich existing data models with the new incoming performance data and related met data from the use application. With the application of Big Data Analytics, designers and raw material suppliers will be able to create new and improved designs and getting new insights of the raw material in end-use application which would lead into modification of the polymer DNA to enable optimal product properties combined with perfect part design. The goal in this endeavor would ultimately be to create smart materials that could be steered to adapt to a changing environment. So, predictive engineering for instance of polymers, that harden under impact, but just in the regions where it is necessary, would lead to new step change in materials science, design thinking due to functional integration and enable major development breakthrough and reduced development time for part producer. (Dupont, 2016)

This could ultimately lead to a new business model and market buster for raw material suppliers to offer their polymers bundled with different levels of insight into product specifications. The customer can then choose whether to acquire basic product knowledge together with the polymer or license different levels of sophistication of data models through the applied software vendors to pay exactly for the level of data – in terms of quantity and quality – that he needs. (For this, also see “Marketbusters” by Rita McGrath and Ian MacMillan.)

In summary, Design Thinking might help to identify the customer needs and to indicate – in close collaboration with the customer – how a valuable solution may look like. The close collaboration with the customer, the frequent testing of assumptions and the strong collaboration of experts from different company divisions may open up the chemical company’s view on how they might deliver the best value – to their industrial clients, but as well to the end consumer and society as a whole.

References

BAVC (2013/2014): Erhöhter Kostendruck in der Chemie, available at https://www.bavc.de/bavc/mediendb.nsf/gfx/47BCAFEF4F59AC63C1257C37004D90BF/$file/ib_12_13_BAVC-Konjunkturumfrage.pdf,accessed 31. May 2017.

BAVC (2016): Kein Anlass für Optimismus, available at https://www.bavc.de/bavc/mediendb.nsf/gfx/D9E7F0E59274F76BC1257FA7003ADA6D/$file/Impuls_05_ 2016_BAVC-Konjunkturumfrage.pdf, accessed 29. May 2017.

Bettis, R. A., Prahalad, C. K. (1995): The Dominant Logic: Retrospective and Extension, in Strategic Management Journal, 16 (1), pp. 5-14.

Bock, K. (08.12.2016): Speech on the yearly press conference of the VCI, available at https://www.vci.de/vci/downloads-vci/media-weitere-downloads/2016-12-08-rede-vci-praesidentkurt-bock-vci-jahrespressekonferenz.pdf, accessed 31. May 2017.

Cefic (2016): European Chemical Industry Facts and Figures Report 2016, available at http://fr.zonesecure.net/13451/186036/#page=1, accessed 30. May 2017.

Cefic (2017): Taking the European Chemical Industry into the Circular Economy, www.cefic.org/newsroom/top-story/Circular-economy-New-Accenturestudy-shows-opportunities-for-EU-chemicals/, accessed 20. J 2017.

Chesbrough, H. (2010): Business Model Innovation: Opportunities and Barriers, in Long Range Planning, 43, pp. 354-363.

Christensen, C. (2011): Interview at the Gartner Symposium ITExpo 2011, http://gartner.mediasite.com/mediasite/play/9cfe6bba5c7941e09bee95eb63f769421d?t=1320659595.

CheManager (18.01.2017): Interview with Dr. Alfred Stern on the future of plastics, http://www.chemanager-online.com/themen/management/die-zukunft-von-kunststoffen-neu-gestalten, accessed 30. May 2017.

CheManager (09.02.2017): Der Kundennutzen zählt, Outcome-based Economy – mit Business Analytics zu neuen Geschäftsmodellen in der Chemieindustrie, http://www.chemanager-online.com/themen/strategie/der-kundennutzen-zaehlt, accessed 30. May 2017.

Cooper, R. G. (1986): Winning at new Products, Addison-Wesley, Boston.

Cooper, R. G. (1990): Stage-Gate Systems: A New Tool for Managing New Products, in Business Horizons May-June, pp. 44-54.

Dupont, Elliot, C. (2016): D3O Agrees Strategic Partnership with Dupont, available at https://www.d3o.com/d3o-agrees-strategic-partnership-with-dupont/, accessed 30. May 2017.

Gapper, J. (2017): „The chemicals industry has lost its future”, www.ft.com, accessed 31. May 2017.

Gassmann, O., Frankenberger, K., Csik, M. (2013): Geschäftsmodelle entwickeln, Carl Hanser Verlag München.

Govindarajan, V., Trimble, C. (2010): Stop the Innovation Wars, in Harvard Business Review, 88 (7-8), pp. 76-83.

Kersten, W., Seiter, M., von See, B., Hackius, N., Maurer, T. (2017): Trends und Strategien in Logistik und Supply Chain Management – Chancen der digitalen Transformation.

Kottmann, H. (2016): Interview on “Managing growth and profitability in the chemical industry”, in Journal of Business Chemistry, 13 (3), pp. 99-101.

Lehr, D., Auch, C. (2017): Novel approaches in professional education to foster innovation in the chemical industry, in Journal of Business Chemistry, 14 (1), pp. 2-10.

Mc Grath, R. G., Macmillan, I.C. (2005): Marketbusters: 40 Strategic Moves That Drive Exceptional Business Growth, Harvard Business Review Press.

Pit Coburn, The Change Function: Why some Technologies Take Off and Others Crash and Burn.

Schröter, H. (2007): Competitive Strategies of the World’s Largest Chemical Companies, 1970-2000, in: Galambos, L., Hiniko, T., and Zambagni, V., (eds.), The Global Chemical Industry in the Age of the Petrochemical Revolution, Cambridge University Press, Cambridge, pp. 53-80.

Utikal, H., Woth, J. (2015): From megatrends to business excellence: Managing change in the German chemical and pharmaceutical industry, in Journal of Business Chemistry, 12 (2), pp. 41-47.

Whitesides, G. M. (2015): Reinventing Chemistry, Angewandte Chemie International Edition, 54, pp. 3196-3209.

Yankowitz, D., Kreutzer, B., Bjacek, P. (2016):Accenture Chemical Industry Vision 2016, available at https://www.accenture.com/t20160609T025416__w__/us-en/_acnmedia/PDF-22/Accenture-Chemical-Vision-2016.pdf, accessed 29. May 2017.