How to secure sustainable competitiveness of Chemical Industry Parks: Global competitive challenges and a systematic, customer-centric response

Abstract

The central question of the following paper is how Chemical Industry Park operators could systematically integrate the external investors’ perspective into their decisions about the park’s future competitive positioning and continuous improvement of operational excellence. In today’s chemical industry landscape, Chemical Industry Parks and their operators face great challenges. On the one hand, they have to meet increased and more complex demands of globally-active chemical companies. On the other hand, ongoing globalization leads to an intensified competition amongst Chemical Industry Parks that try to be successful in attracting investors on an international level. The presented methodology and some insights from an international competitivenessstudy of leading Chemical Industry Parks shall serve as a guideline as to howoperators of Chemical Industry Parks could introduce customer centricity in their business model and how they could effectively compete on a global scale.

1 Introduction

Strategic positioning based on investors’ key investment criteria combined with operational excellence in site operations is decisive. Chemical park operators have to contribute added value to the competitiveness of the chemical companies at the chemical park and, at the same time, have to organize their site operations in a customer-oriented, flexible and cost effective manner, defining their core competencies while outsourcing non-core services to external companies. In order to understand and best meet the requirements of investors, site operators have to put themselves in the perspective of the investing chemical production company as the “customer”. This is valid for both the European Chemical Industry Parks with a high degree of integration and long production history as well as for the developing chemical production clusters in South-East-Asia, China and the Middle East that were designed on the drawing board following decade oriented master plans. Role models like Jurong Island in Singapore together with the Singapore Economic Development Board (EDB) have a very proactive chemical investor acquisition strategy. Before even speaking to potential investors, they have already done thorough business and technology analyses. From the beginning, they are able to discuss with the potential investor about best value chain fit and future requirements of infrastructure and service integration.

In general, the definition of ‘customer’ does not only include potential investors, but also already existing production companies on site. The terms chemical site operator and chemical park management are used analogous and describe the management unit of a Chemical Industry Park.

The following Site Benchmarking Framework focuses on different options to improve competitiveness and increase attractiveness of Chemical Industry Parks and related site services from an investor’s perspective. It shows how this could be achieved in as a systematic, ongoing and customer-centric approach.

The following key questions define the initial situation of the Chemical Industry Parks and their challenges:

- How can Chemical Industry Parks successfully position themselves in global competition for future investors?

- How can Chemical Industry Park operators systematically integrate the customer perspective into their strategic and operational decisions to increase the sites’ competitiveness?

- How could Chemical Industry Parks systematically identify, develop and promote their key competitive advantages compared to the global peer group?

- How could Chemical Industry Park operators define areas for improvement in the park’s strategy and operations with the highest leverage to increase the competitiveness and attractiveness?

- How could Chemical Industry Park operators continuously measure the investors’ confidence and satisfaction for an ongoing site development?

The following sections of the paper first describe the basic methodology and the approach that has been developed as a result of continuing business and technology consulting work in the chemical industry with special focus on Chemical Industry Parks. Secondly, the added value of the Site Benchmarking Framework as a management tool is defined by presenting different result formats of benchmarking exercises. Following this section, results from an international study of Chemical Industry Park’s competitiveness using the herein presented Site Benchmarking Framework are presented. Finally, an outlook and short summary of key aspects should initiate both continuous practical and theoretical discussions on the topic as to how to secure sustainable competitiveness of Chemical Industry Parks in the future.

2 Basic methodology and approach: Site Benchmarking Framework

The presented integrated approach is based on the principles of benchmarking as a management tool (Mertins and Kohl, 2009). The basic objective of systematically comparing one Chemical Industry Park with its peer group aims at identifying different options to improve competitiveness of individual Chemical Industry Parks.

Two central arguments have been followed by developing the framework:

- Chemical Industry Parks gain competitive advantages by continuously orienting themselves towards key investment criteria of global chemical producers.

- Chemical Industry Parks compete on an international level for potential investors and have to position themselves towards their global peers based on clearly defined site-successfactors derived from the key investment criteria

In the following, the elaboration on the Site Benchmarking Framework will concentrate on Chemical Industry Parks as benchmarking object. Basically, the used term Chemical Industry Park defines a settlement of several chemical production companies or production units, i.e. chemical plants within the so-called battery limits of a defined production area. Entrance to the park is constantly controlled and only possible through secured access gates. The single production units in a Chemical Industry Park tend to show a high degree of mass flow and infrastructure integration. In most case the central provision and management of infrastructure and services is done by a so-called site operator. Availability and efficiency of site services and infrastructure are decisive for the site’s attractiveness because Chemical Industry Park investors can focus on their core business and competences. Major objective of the production companies is to gain a competitive advantage from synergies and scale effects while sharing capital intensive site infrastructure and cost intensive site service provision.

In comparison, the term chemical site refers more to the single plant and the location of a specific production unit within a Chemical Industry Park or as a stand-alone production site. Chemical clusters, e.g. Antwerp Chemical Cluster, are a mixture of Chemical Industry Parks and single production sites of one major user company. Here, the whole area of the cluster has no security access gates or fenced battery limits as in the case of an access restricted park or single chemical production site with establish security controls. Furthermore, the degree of infrastructure and mass flow integration tends to be lower in the cluster format than in an established Chemical Industry Park (Bergmann, Bode, Festel and Hauthal, 2004).

2.1 Site-success-factors for Chemical Industry Parks

Based on defined site-success-factors for high site competitiveness and attractiveness, Chemical Industry Parks could be objectively evaluated from an investor’s or existing resident’s perspective. This has to be done in a standardized way, both to generate comparable data over the years and to be able to compare the own Chemical Industry Park with its global peers applying the same set of evaluation criteria and definitions. The site-success-factors and more than 80 underlying benchmarks are derived from companies’ investment decision processes for new production sites and represent the first part of the Site Benchmarking Framework. The following presented factors are the result of a survey done with a selection of chemical producers in Germany. The objective was to identify the most important factors in new investment and site decisions. Interview partners have been the companies’ investment project leaders, corporate development representatives, corporate finance representatives, plant managers and internal service providers.

The site-success-factors could be weighted according to the respective position of the investing company within the chemical value chain coming from petrochemicals, base chemicals towards polymers, specialty chemicals and down-stream areas of agrochemicals, pharmaceuticals and biotechnology.

Starting from a more general level, chemical park investors consider macroeconomic conditions, tax situation, financial investment incentives, regional laws and regulations in their investment and site decisions. They look at the geographical position of the site that best fits their individual business strategy. The perspectives of access to promising customer and cost-efficient sourcing markets are of highest relevance. The sourcing situation at the potential investment locations has not only a cost component. The availability of the required raw materials with the right specifications is decisive. Here, the already existing production network at the site could play an important role. Chemical companies could extensively benefit from production network effects with connected up- or downstream industries. Therefore, one major focus lies on the site’s value chain coverage and range of companies already present on site. Site attractiveness is further increased by individual Investor Relations management and efficient administrative permission processes that enable “Plug & Play” plant investments with established up-to-date infrastructure and service provision, i.e. competitive lead times between investment decision and production start.

Chemical Industry Park investors further evaluate site factor bundles according to their business model and its needs, e.g. available, highly-qualified local workforce as well as labor cost level, site infrastructure, R&D facilities and technology, logistical infrastructure and pipeline connectivity. Especially, the performance of site operators and availability of comprehensive site service portfolios are decisive for the site’s attractiveness as Chemical Industry Park investors can focus on their core business and outsource support processes. Existing shared on-site infrastructure generates cost-reducing synergies, enables economies of scale, increases flexibility, minimizes risks and optimizes business related investment activities (InfraServ Hoechst, 2009).

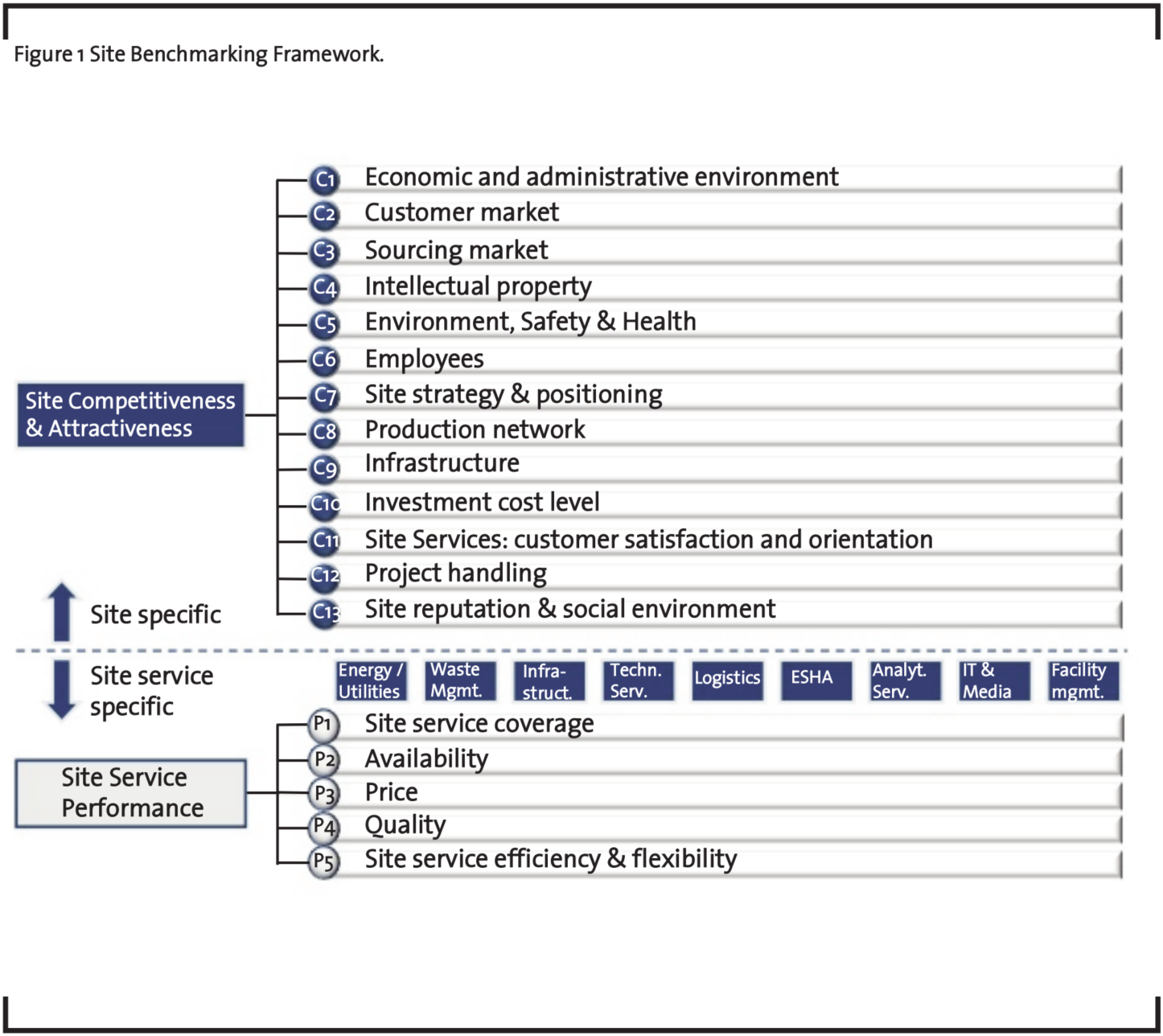

Following the investment rationale of chemical companies, these site-success-factors are the basis for the Site Benchmarking Framework. They are used to derive the required benchmarking criteria, both qualitative and quantitative in nature. The site-success-factors and benchmarking criteria could be arranged according to the following three clusters:

The first cluster deals with the “Geographic position” of the Chemical Industry Park, and covers, amongst others, the following qualitative and quantitative benchmarking criteria:

- Economic and administrative environment: Political stability, financial stability, BERI-Index, Legal Corruption Perception Index (CPI). Logistical Performance Index (LPI), approval procedures, taxes (corporate income tax, withholding tax, etc.), tax deduction possibilities, investment incentives, customs and tariffs, etc.

- Customer market: Regional gross domestic product, chemical market growth rates, market volumes and size, etc.

- Sourcing market: Raw materials availability, Raw materials cost level, Electrical energy cost level, Natural Gas cost level, etc.

- Intellectual Property: Legislation and execution, Intellectual Property (IP) protection, etc.

- Environment, Safety and Health: Environmental regulative conditions, Safety standards on site, ESH Management, etc.

- Employees: Availability of qualified personnel (operational personnel, supervisor, engineer), labor cost level, personnel turnover rate, labor laws, variety of unit operations, expertise on site/in region, labor productivity, etc.

- Site reputation and social environment: Reputation and acceptance of site within public, attractiveness for (international) employees, hardship index, etc.

The second cluster covers all aspects related to the “Production network” including the process of investment within the battery limits, amongst others the following qualitative and quantitative benchmarking criteria:

- Site strategy and positioning: Production network development, site services strategy, Investor Relations (IR) management, education and research facilities, existence of R&D facilities, investment volume for projects, PR/communication and lobbying, etc.

- Production network: Mass flow and infrastructure integration, value chain coverage, raw material availability through network options, pipeline network and connections, etc.

- Investment cost level: Materials cost level, engineering cost level, construction cost level, administrational cost level, permitting cost level, etc.

- Project handling: Project handling time, project handling cost, project management support of site operator, authority management of site operator, etc.

The third cluster “Infrastructure” looks at the installed infrastructure and site services provision on and next to the chemical sites, the following qualitative and quantitative benchmarking criteria:

- Infrastructure: Availability and condition of site infrastructure, “Plug & Play” readiness, access and support for special equipment, logistical infrastructure and connectivity, availability of vacant and developed site area, etc.

- Site services – Customer satisfaction and orientation: Customer orientation of service and product portfolio, site service quality, monopolistic vs. competing site services, site service coordination (key account management), qualification level of site operators’ employees, etc.

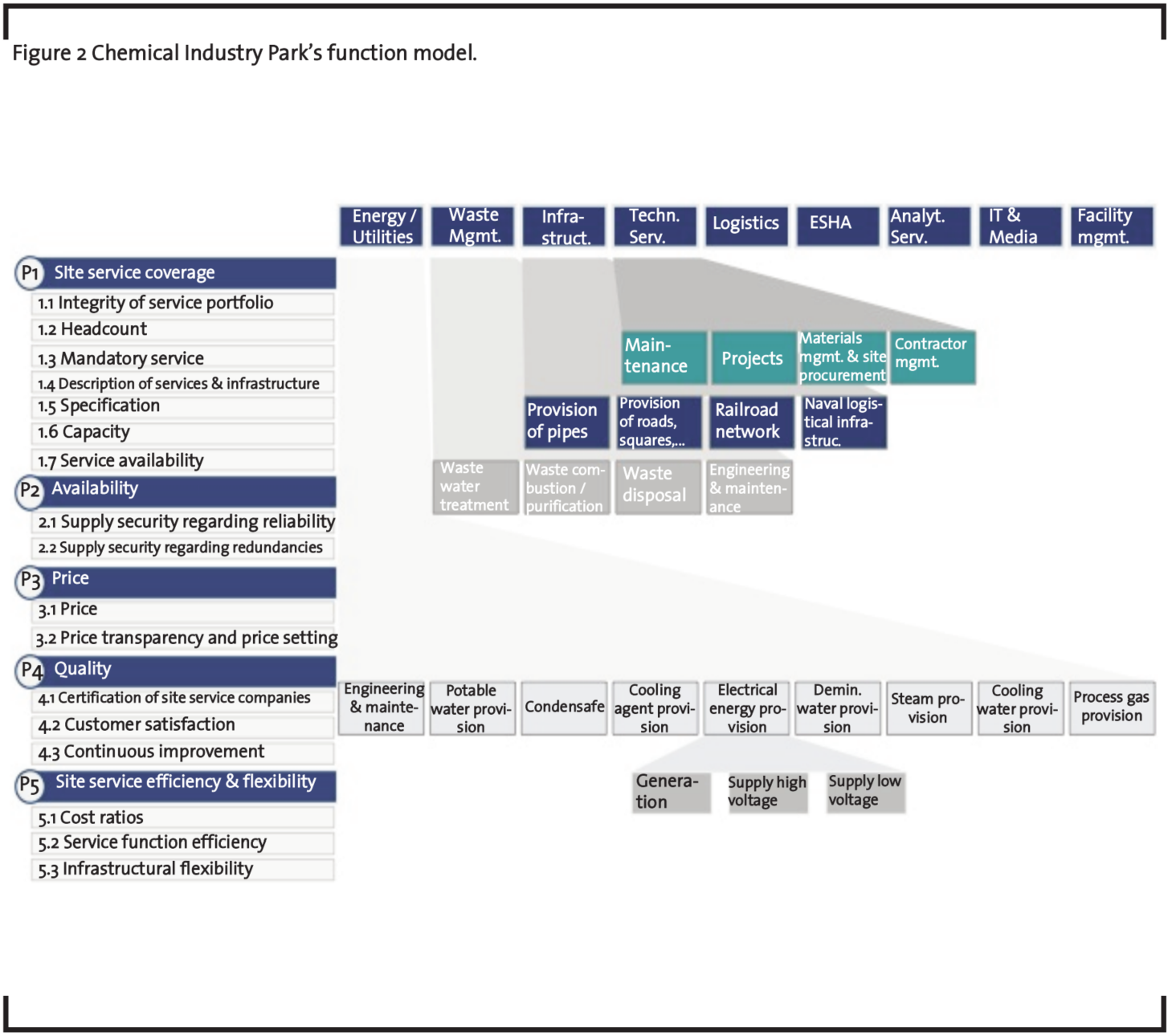

These in total thirteen site-success-factors refer to the first part of the Site Benchmarking Framework, the “Site’s Competitiveness & Attractiveness” (see figure 1). The second part of the Site Benchmarking Framework consists of an assessment of the Site Service Performance. The Site Service Performance evaluation is based on a holistic function model for Chemical Industry Parks. All required site services and energies by the producing chemical companies are evaluated and analyzed applying criteria such as site service coverage, availability, price and cost level, quality as well as site service efficiency and flexibility (see figure 2).

2.3 Practical implementation of Site Benchmarking Framework

Besides secondary source research activities, structured on-site interviews with potential investors, the chemical park operator and owner, major chemical production companies and existing site service providers are particularly important for the gathering of all relevant site specific information. These interviews are mostly performed by an external service provider, but could be done as well inhouse. Standardized questionnaires are used that can be automatically evaluated by a specific software that has been developed for these kinds of site assessments. Handed over to the site operator, this software is a useful tool to perform regular site benchmarking of the own Chemical Industry Park and develop internal benchmarks over the course of time. Obviously, external benchmarks of global Chemical Industry Parks have to be inserted into the analysis to leverage the own benchmarking database. A kind of market intelligence function normally pursues these activities. External benchmarks can be either generated by own field research, by analyzing secondary data or by acquiring the data from specialized technological and management consulting companies. The software is easy to use and could be adapted to the site operators’ needs.

2.4 Site Benchmarking instruments and result formats

In particular for Chemical Industry Park operators, access to detailed up-to-date knowledge of the relevant site-success-factors and best practices is crucial for long-term success in the market. Not all site-success-factors and benchmarking criteria could be directly influenced by the site operator. Nevertheless, a sound information basis of these factors can be crucial in investor negotiations when production companies evaluate potential production locations on a global scale, i.e. in Europe, Middle East, USA South-East-Asia or China. The structured collection, objective evaluation and targeted provision of information per site-successfactor and site service in a comparison with selected benchmarks and best practices of international Chemical Industry Parks represents an integral part of a thorough competitive analysis.

The global peer group comparison enables to assess the considered park’s relative competitive position. The site benchmarking results helps site operators to make the most effective and efficient future investment decisions in order to further develop their competitive advantages and to close identified gaps. The benchmarking approach functions as facilitator to optimally apply instruments like best-in-class analysis per site-success-factor , strengths and weaknesses profiles, Site Service Performance evaluations, structured collection of investors’ feedback as in Investor Confidence Surveys or more quantified cost structure analyses related to Costs of Goods Sold (COGS) or industry cost curves for specific production set-ups. Eight different instruments and corresponding result formats are exemplarily described to show the diversity of potential usage options. Each provides a value added to a best possible set-up and development of the Chemical Industry Park:

2.4.1 Site Competitiveness & Attractiveness assessment

The Competitiveness & Attractiveness assessment uses spider diagrams to evaluate the predefined site-success-factors and more than 70 qualitative and quantitative benchmarking criteria in comparison to global peers. Site operators that systematically use the benchmarking approach within regular periods are able to develop internal benchmarks and analyze the Chemical Industry Park development in the course of time. The transparency of development potentials could be used to define specific measures to close gaps or to further leverage competitive advantages of the site. When comparing with other peers, know-how transfer and learnings effects could be generated.

2.4.2 Site Service Performance evaluation

The Site Service Performance evaluation of available infrastructure and site service portfolio gives a comprehensive overview on the offered electrical energy, utilities and site services regarding their availability, quality and price/cost levels as well as the quality of the infrastructural development of the Chemical Park.

2.4.3 “Best in Class”-Analysis

Comparison with the world’s leading Chemical Industry Parks shows the own competitive situation. An extensive site benchmarking database of world’s leading Chemical Industry Parks provides best practices, site benchmarks and role models, among others from analyzed chemical sites in Europe, USA, China and Southeast Asia. A strategic positioning towards competing Chemical Industry Parks worldwide, especially in growth regions, can and should be elaborated.

2.4.4 Cost Structure Analysis

Cost structure analyses for investments and operations of chemical production plants could be elaborated using the information of the Site Benchmarking Framework. Comparison of cost structures of the Chemical Industry Parks could include industry cost curves, Cost of Goods Sold (COGS) analyses for specified products, etc.

2.4.5 Site marketing and commercialization

Benchmarking results such as site assessments and site profiles can be perfectly used for future site marketing and commercialization activities to attract new investments, i.e. communication campaigns, “Best-in-Class comparison”, proactive communication and targeted approaching of potential investors. Clear understanding about own competitive advantages and strengths in relation to the peer group enables more effective discussions with potential investors. In addition, knowledge about continuously evolving requirements of chemical companies is essential to develop a customer-oriented service culture.

2.4.6 Investor Confidence Study

Analysis of investor needs and rate of satisfaction with investment and production conditions at the Chemical Industry Park enable more targeted site investment programs securing mid-to-longterm competitiveness. Furthermore, a communication channel for continuous information exchange between Chemical Industry Park management and investors will be established. Changing customer requirements will be identified more quickly and could be addressed in a more effective manner.

2.4.7 Site development concept and international cooperation

Continuous improvement of sites’ competitiveness and attractiveness enable Chemical Industry Parks to be best prepared for increased competition for potential investors. Targeted development of the Chemical Industry Park leads to a sustainable ensurance of site competitiveness beyond existing battery limits. Especially, the benefits from regional and international cooperations have to be taken into account to achieve further synergies and positive impulses for increased site attractiveness. Defined recommendations and measures as a result of the site benchmarking approach constitute the future action plan.

2.4.8 Site profiles

Site profiles for each Chemical Park provide all relevant data compiled in one information brochure. It could be used as a fact book for potential investors and contains all relevant data that that investors need to make a first judgment on the site’s compatibility with its requirements.

2.5 Selected real business applications of the methodology

2.5.1 Practice example: Investment planning support

The following example describes how the Site Benchmarking Framework offers a valuable instrument in the site selection process for chemical plant investments. In the reference project, the site benchmarking exercise was applied to support the site selection process at a chemical production company. Furthermore, the methodology was finally handed over to the responsible organizational unit to support investment project leaders in different stages of the site selection process providing continuously ready-to-use site information. It enables a proactive investment planning support through neutral, project-independent and standardized competitiveness evaluations, site service performance assessments and basic site profiles visualized in standardized and comparable result formats.

Starting with the investment decision, the site benchmarking tool and database provides top criteria of global chemical parks supporting the generation of a long-list of potentially interesting sites identifying deal breakers at the beginning of the whole process while identifying the best fit investment locations at the same time. Next, the shortlist of sites for further analysis could be derived by either using the existing database or pursuing new site benchmarking exercises that further complete the database. This includes the evaluation of the site’s competitiveness and attractiveness based on the qualitative and quantitative benchmarking criteria as well as the analysis of site service performance of all relevant site services at the selected Chemical Industry Park. Here, weighting factors for the different benchmarking criteria are used to account for the specifics of each plant investment project. Finally, the project specific site decision could be taken with a clear argumentation basis of why this site has been chosen. Furthermore, already detailed information about the target site could be used for both effective negotiations with the local Chemical Industry Park management and for the starting plant engineering activities.

The major advantages for the chemical production company of applying the Site Benchmarking Framework in a systematic manner have been the following. First, the whole site selection process has been significantly accelerated with instant information available. Second, the quality of the final decision and the whole selection process has been more resilient due to objective and detailed information about the leading global sites. Third, the selection process becomes more transparent and comprehensible to top management and site decisions could be more effectively challenged to identify the optimum for the company. Finally, it enables the company to effectively develop and steer its whole production network by establishing key strategic productions sites preventing a fragmented production set-up.

2.5.2 Practice example: Future Chemical Industry Park development

The following example describes the application of the Site Benchmarking Framework for a worldwide leading Chemical Industry Park. The objective was to elaborate strategic optimization levers with regard to site attractiveness and competitiveness in comparison to its global peers based on standardized performance indicators and existing benchmarks. The underlying rationale of the project was that continuous site development and objective assessments are necessary to get an upto-date competitive picture of the site and to identify areas for improvement. Using the Site Benchmarking Framework and the underlying benchmarking criteria, improvement hypotheses and recommendations have been defined on various dimensions, where gaps to leading international best practices or requirements from potential investors were not met.

The project started with an extensive interview series and data collection to gather the required information for benchmarking exercise. Interview partners have been the official authorities, the site operator itself, existing production companies, potential investors and the various site service providers within and outside the battery limits of the Chemical Industry Park, e.g. energy providers, logistics service providers, waste management service providers, technical service providers. Afterwards, interviews results were consolidated in the benchmarking database to identify the most promising improvement hypotheses. Furthermore, a detailed Strengths and Weaknesses profile of the respective park in comparison to other chemical parks have been compiled.

Finally, recommendations have been elaborated with detailed action plans, business cases and responsibilities to prepare the implementation of the whole recommendation catalogue handed over to the Chemical Industry Park operator.

Examples for improvement hypotheses and related recommendations could cover various dimensions, for example Chemical Industry Park strategy and commercialization as well as the site service concept. Here, exemplary recommendations ranged from a more proactive analysis of potential investors and their requirements as well as fit into existing and targeted value chain on site or the establishment of a central coordination function supporting authority management (key account management enabling “One-stop-shopping“). Regarding the site service concept, the introduction of market oriented pricing for provided site services in the chemical park due to in a global comparison partly higher service costs should have been addressed by breaking up the monopolistic supply situation for specific site services.

3 Insights from a Global Site Benchmarking study

3.1 Region-based assessment of international Chemical Industry Parks

The most important and still valid conclusion drawn from benchmarking the worlds’ leading chemical industry parks is that the “ideal chemical site for all kinds of investments with best-in-class chemical production conditions” does not exist. Instead, each site offers a portfolio of favorable and less favorable factors to be evaluated according to the projects’ specific requirements. The challenge for globally operating chemical companies is to find the best-fit investment location facing the heterogeneity of chemical production locations. At the same time it is an opportunity for Chemical Industry Parks and their operators to present themselves at their best. The global site benchmarking is key to both, identifying optimization levers for increased competitiveness for the own site and having a detailed and structured set of information regarding strengths and weaknesses of other worldwide leading Chemical Industry Parks.

As already stated, not all site relevant factors could be influenced by the chemical park management. Various factors are controlled by other institutions, e.g. the local government, or are pre-determined by geographic and natural conditions. Despite the partially limited or restricted influence on some factors like taxes, deep sea port access or customer market, chemical site operators are empowered in the negotiations with potential investors to best promote their site. Furthermore, they are enabled to better lead discussions with regional institutions to best develop not only the site within the battery limits, but to influence the general investment conditions in the region to their interest.

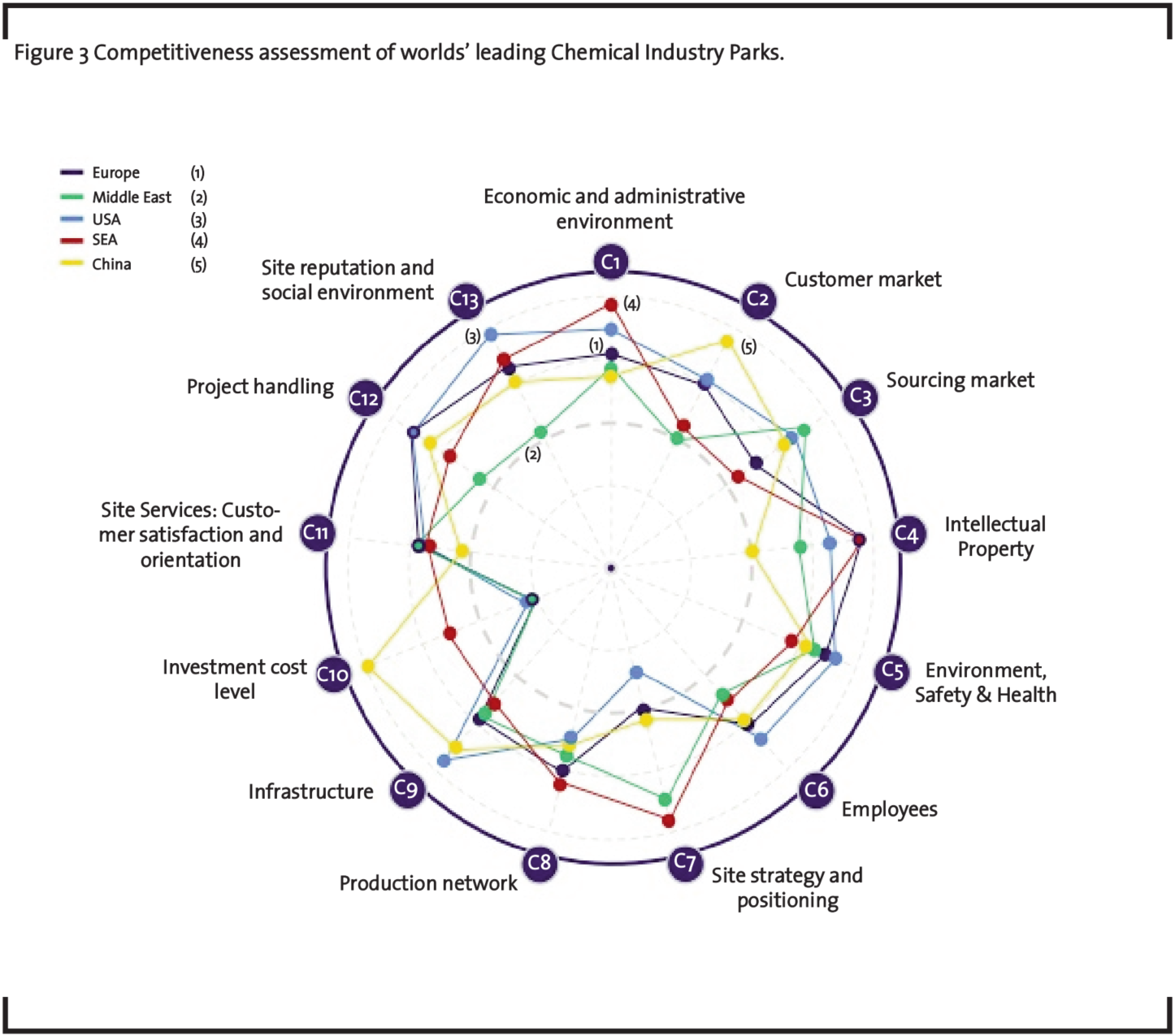

Figure 3 shows the results of a global competitiveness assessment of Chemical Industry Parks, summarized for the different regions Europe, Middle East, USA, South-East-Asia and China. The characteristics of the 13 analyzed site-success-factors are based on the 70 underlying qualitative and quantitative benchmarking criteria.

3.2 Competitivenessinsights per site-success-factor

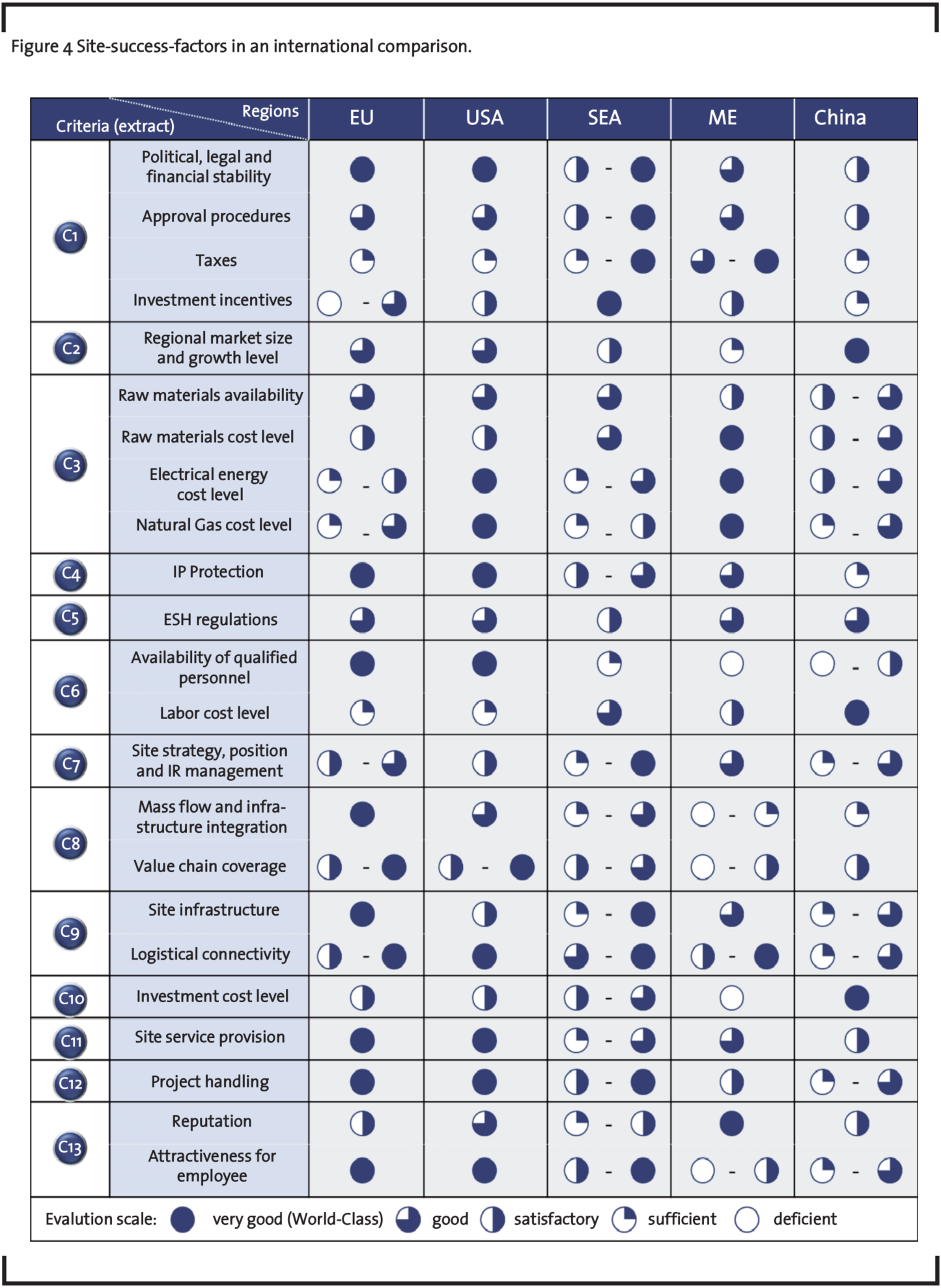

In the following, assessment results are described per site-success-factor with corresponding regional specifics and characteristics. The results are shown as an extract of the whole Site benchmarking Framework in figure 4.

3.2.1 C.1 Economical and administrative environment

Basically, all regions show positive characteristics as far as criteria like political, legal and financial stability and management complexity of approval procedures are concerned. Legal prerequisites for equity participation schemes in joint venture structure with local partners in the Middle East and China could lead to deterring effects. In Qatar, foreign companies need a local sponsor to establish joint ventures that are characterized by a statutorily fixed share distribution among the partners.

In particular, taxation and investment incentives largely differ between the analyzed chemical sites in the different regions. Favorable conditions can be identified at Chemical Industry Parks in the Middle East and South-East-Asia. For example, investments in Jurong Island, Singapore, benefit from a world-class administrational environment that offers very favorable tax incentives and shows a very effective site commercialization. Tax holidays up to 12 years and a reduced corporate income tax of 17% could be highlighted. In comparison, investments at German sites have to show positive return with a nearly double as high tax burden and without further tax related investment incentives. In the USA, a rather high income tax up to 39.5%, due to high federal tax, has to be considered. The attractiveness of European and in particular German sites is very depending on the introduction of targeted investment incentives as the basis of a long-term oriented industrial politics.

3.2.2 C.2 Customer market

Without referring to the individual chemical product, high attractiveness for the accessibility of a large chemical market has been stated for the European, American and Chinese Chemical Industry Parks. In comparison, the expected growth potential of the markets has been evaluated differently. Here, the dynamic Chinese chemical market is expected to show high growth rates.

3.2.3 C.3 Sourcing market

Cheap feedstock access to the world’s largest crude oil and Natural Gas reserves, good raw materials’ availability and cost levels as well as veryfavorable electrical energy prices compared to all other global sites are key investment advantages for the Middle East region. At the Chemical Park Al Jubail, Saudi-Arabia, Natural Gas costs amount up to US$ 0.75 to US$ 1.00 per mmBtu. These conditions belong to the most competitive in the whole world. In comparison, European and South-East-Asian chemical sites face energy cost disadvantages because of price surcharges for electrical energy up to 150% to 400%. Missing concepts of secured energy availability and expected negative impacts of new federal legislations to support renewable energy sources put pressure on the local companies at the Chemical Industry Parks in Germany. Site-crossing energy concepts to increase the energy efficiency could be one solution to restore and maintain competitiveness of local production conditions.

Major disadvantages in Singapore are electrical energy prices that are as high as at several chemical sites in Europe, e.g. chemical cluster Antwerp, but double the price of other co-located South-East Asian chemical sites. At European sites, the longterm secured availability of cheap Natural Gas is a major concern, even though German sites are well connected to the far reaching West European pipeline network. The foundation of the „Allianz zur Rohstoffsicherung“ of the German industry is a first positive signal on a national level to address the concern of long-term, raw materials availability with dedicated raw material alliances between different companies depending on the same raw materials for their productions.

3.2.4 C.4 Intellectual Property

Intellectual Property (IP) protection remains an issue in China, although legislation has been adjusted to international standards in the meantime. Chinese approval procedures with substantial disclosure obligations for new plant constructions and import of technologies offer various risks for IP leakages and an uncontrollable outflow of confidential business and technological information.

In comparison, IP protection regulations and enforcement is seen to be very effective in the Middle East, Europe and USA. Most Arabic states are actively looking for foreign investment and technology partners following their economic development strategies, amongst others the settling of downstream chemistry. Therefore, all concerns of possible IP violations shall be avoided to attract international technology joint venture partners to the region by effective IP protection rules.

3.2.5 C.5 Environment, Safety & Health

Basically, Environment, Safety and Health (ESH) regulations at the examined Chemical Industry Parks follow international standards. In most cases, the global players among the chemical production companies have even installed stricter company internal ESH rules at their plants. In comparison to strongly integrated chemical sites in Europe, where the ESH management is strongly monitored and controlled by the chemical park operator, chemical production plants in South-East-Asia or China are somehow separated from the other plants in the chemical park. The production units have more of an “island” character with their own battery limits. Here, ESH management is much more driven by the chemical plant manager complementing the general ESH regulation of the whole local chemical cluster area.

3.2.6 C.6 Employees

Main advantage of European and American sites is the availability of well-qualified personnel on all levels, i.e. blue collar workers, supervisors and engineers. For plant investments and operations in regions such as South-East-Asia, Middle East and China, there is a strong need for internal company training on the job, because of the lack of an effective dual education system. The availability of skilled labor is partially very limited. The German education system still functions as a role model for several initiatives started in Asia and elsewhere. The network of universities, universities of applied sciences and research institutes combined with Germany’s system of on-the-job-training represent a key competitive advantage. Nevertheless, the demographic development and partial shortages for skilled labor put this favorable condition under pressure.

Low labor costs put Chinese Chemical Industry Parks in a favorable position when compared to other considered chemical sites. Labor cost levels amount to less than 10-20% compared to European sites. Comparing South-East Asian sites with European Sites, this labor cost advantage still amounts up to 50%, excluding sites like Jurong Island in Singapore from this consideration. Besides pure cost considerations, in the USA, labor productivity is very high in comparison with the rest of the world.

3.2.7 C.7 Positioning and strategy

Clearly defined Chemical Industry Park strategies and value chain positioning could be identified for “Greenfield”- designed chemical parks in South-East-Asia, China and in the Middle East. Here, the settlement of defined industries and companies is outlined in extensive master plans. These plans include the whole site development from the scratch. Value chains are partially planned on single product and technology level with ranked potential investors. In comparison, chemical sites with a long production history like in Germany proactively have started to address the challenges of increased globalization and structural change and position themselves with their inherent advantages towards global investors.

3.2.8 C.8 Production network

It is one of the major competitive advantages of European and especially German Chemical Industry Parks, the so-called „Verbundproduktion”, a high degree of chemical production integration. This high degree of mass flow and infrastructure integration with all resulting synergies and the high coverage of complete chemical value chains at one site still function as role models for the planning and set-up of new integrated Chemical Industry Parks in the world. At Chinese Chemical Industry Parks, the low degree of production integration at the considered sites is currently not really addressed by a proactive intercompany production network planning and site commercialization by the Chinese site operators. Production could be characterized rather as “island” solutions than an integrated chemical park concept.

3.2.9 C.9 Infrastructure

Existing infrastructure in Chemical Industry Parks is of major investors’ interest, amongst others availability of internal logistics, supply and disposal networks and communication infrastructure. Here again, German Chemical Industry Parks show favorable conditions because of the high degree of infrastructure integration, resulting in cost synergies and competitive advantages for local producers. Especially at some South-East-Asian and Chinese Chemical Industry Parks, security of supply and quality of provided infrastructure show substantial deficits. In the Middle East region as in the United Arab Emirates and Saudi-Arabia, the picture is different. Most Chemical Industry Parks in the Middle East region are centrally-managed and developed by governmental institutions or state companies that are specifically responsible for the construction and operation of basic infrastructure facilities (land provision). Large investment programs in world-class chemical site infrastructure, such as in Qatar, generate very favorable conditions for investments and operations.

The favorable logistical location in the Middle East between Europe and Asia and the availability of deepwater port access at major chemical sites are prerequisites to optimally serve the export-oriented chemical production at place, especially because of a very small local customer market. Similar, Jurong Island in Singapore or the chemical cluster in Antwerp, Belgium, offer favorable logistical connectivity with the access to a deep sea water port to serve the global market. Chemical production at European or American sites, in case they have a more regional customer market focus, benefits from an excellent logistical infrastructure of railroads, motorways and water channels for the whole region.

3.2.10 C.10 Investment cost level

In general, investment cost levels in Europe and the USA are higher than at the Asian sites because of higher material, engineering, construction and permission costs, but far lower than expected cost levels in the Middle East. Major challenges for investing companies in the Middle East are high investment cost induced by extreme climatic conditions. Special materials, technologies and maintenance services are required to achieve global utilization rates from the plants. Compared to the European sites, cost surcharges amount to a plus of 25-30% for plant investments. On the other side, production investment in China and some SouthEast-Asian sites can be calculated with investment cost levels that are as much as 25% lower than the European reference values.

3.2.11 C.11 Site services – Customer satisfaction and orientation

European chemical production sites provide very stable production conditions thanks to their long production history and highly professional site operators. Here, site service providers offer a very comprehensive site service portfolio and reliable infrastructure for chemical production companies according to the “Plug & Play” principle. This results in a high degree of customer satisfaction. Wide range of site services with high customer orientation, secured availability, quality and efficiency lead to a clear competitive advantage in the global comparison. In the USA, American Chemical Industry Parks also offer a very favorable environment for investments and operations of chemical plants. The cost situation regarding all major utilities such as electrical energy, steam and especially natural gas are at a world class level.

The provision of site services in China shows a more heterogeneous picture. In most cases, there are monopolistic structures of site services supply that could lead to substantial dependency on the often state-owned providers. However, in total they have no influence on currently very favorable production costs for electrical energy, waste water treatment or maintenance services.

3.2.12 C.12 Project handling

Reliable adherence to time schedule and investment budgets within the planning and execution of investment projects could be stated especially at European and American Chemical Industry Parks. Here, the support from official institutions and the chemical park management has been valued extremely effective and efficient. At Chinese chemical parks, investors face much more heterogeneous conditions. Especially, more rural Chemical Industry Parks in China show a high development backlog.

3.2.13 C.13 Reputation and social environment of the Chemical Park

Chemical parks in the USA and the Middle East benefit from a high reputation in the local population. A different picture exists when considering the attractiveness of some Chemical Industry Parks from a Western employee perspective. Life conditions in the Middle East and some South-East-Asian and Chinese sites could generate a severe problem for investing companies to convince required highly skilled employees to work there for several years, e.g. Al Jubail in Saudi-Arabia, Map Ta Phut in Thailand or Chongqing in China.

4 Summary

European Chemical Industry Parks claim their position in an increased international competition for investors. They enable chemical producers to benefit from largely integrated mass flows and infrastructure at the various sites. The success model “Chemical Industry Park” with its comprehensive provision of site services, energies and infrastructure for the production plants on site secures the competitiveness of whole chemical value chains. The targeted and sustainable development of Chemical Industry Parks in Europe represents the prerequisite for long-term economic success combined with social and environmental responsibility.

5 Outlook

In summary, a clear strategic positioning, a synergy-targeted infrastructure as well as a comprehensive and customer-oriented site services portfolio are basic requirements for future high competitiveness of existing Chemical Industry Parks. Site operators need to effectively integrate the customer perspective of potential and existing investors into their development efforts of the Chemical Industry Parks. Close alignment with continuously changing customer needs and full transparency of the parks’ individual strengths and weaknesses portfolio allow a target improvement of the sites’ competitiveness and service performance. The Site Benchmarking Framework and the diversity of result formats that can be generated by applying it should offer a systematic and coherent approach for targeted site development, communication and promotion.

Comparison of the world’s leading Chemical Industry Parks shows the own competitive situation. This approach however creates a value-add beyond grasping the gap to best-in-class peers. It guides to new ways of goal-oriented and sustainable site development, based on best-practices, role models, site benchmarks and other valuable inside views into the leading chemical sites in Europe, USA, China, South-East-Asia and the Middle East.

References

Bergmann, T., Bode, M., Festel, G. and Hauthal, H.G. (2004): Industrieparks – Herausforderungen und Trends in der Chemie- und Pharmaindustrie, Festel Capital, Hünenberg, Germany.

InfraServ Hoechst (2009): Standortfitness, CHEManager Special edition.

Mertins, K. and Kohl, H. (2009): Benchmarking – Leitfaden für den Vergleich mit den Besten, 2nd revised edition, Düsseldorf, Germany: Symposion Publishing GmbH.