A pulse on the specialty chemical sector

1 Introduction

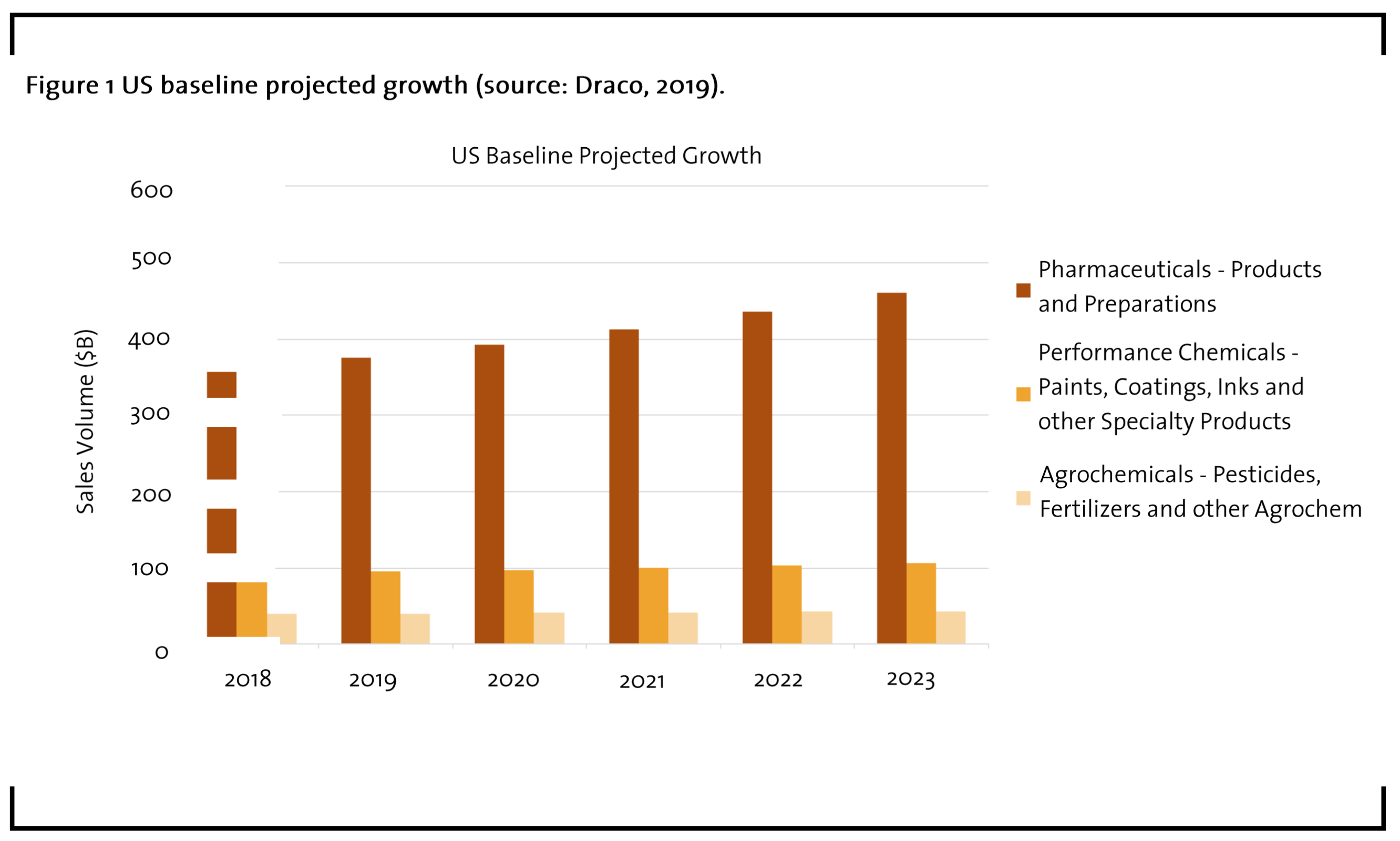

When examining the chemical industry, it is important to differentiate between commodity chemicals – which are often manufactured via large-scale, bulk volumes – and specialty and fine chemicals – manufactured for customized applications and characteristics at much smaller volumes. Specialty and fine chemical manufacturers supply into industries across pharmaceutical, performance and agrochemical sectors accounting for up to $357B in the United States compared to circa $800B associated with the chemical industry overall. As a corollary of being rooted in smaller volumes, the specialty chemical landscape is composed of contract and custom manufacturers which can be more agile due to their diverse range of capabilities and find themselves better poised to react to trade disruptions to the global supply chain. The most impactful challenges facing these industries in the coming years will be more rooted in industry socio- and technical trends – such as sustainability, cyber security and digitalization – than global megatrends rippling through commodity chemical markets.

This paper compares projections from economic experts for the effect of trade of short-term factors and contextualizes projected megatrends and how the specialty chemical industry is best suited to weather them over the years. It furthermore discusses trends which may have a greater impact to business operations, such as a customer push for attention to sustainability, cyber security and digitalization.

2 Setting the stage in 2019 and beyond

The end of 2018 was characterized by a surge in purchasing for the specialty chemical industry, resulting from a stockpiling of inventory in preparation for tranches of tariffs in place for the US, Brexit, and offshore disruptions including environmental-based plant closures in China (Hirsh, 2019). The increase in inventory manifests itself with softer sales volumes, as manufacturers work through this material-on-hand. In spite of this phenomenon, capital investment in manufacturing facilities is expected to rise 2.2% over the next 12 months (Moutray, 2019), with 85% of those in the specialty and fine chemical sector planning some sort of capital expansion (SOCMA, 2019). While this may seem initially counter-intuitive, economic models project that the chemical industry will see growth in most all scenarios, albeit stinted from full potential.

The tendency of these key specialty chemical industry sectors to continue growth can be traced to chemistry’s role in day-to-day life of society, it’s relative independence from low-skill labor, and leadership in the realm of knowledge-intensive-value-add. Economic pressures may cause many companies to address long-term issues more expeditiously to take advantage of the potential for market share expansion. Just over four years out from the United Nations Sustainable Development Goals (SDGs), customer facing markets having become more sensitive to conveying their role in proactively advancing subsets of these goals. It is observable that these companies are working through areas for cutting their direct contributions to carbon emissions, climate action, life below the sea, etcetera. One can reasonably expect that they will next turn to their suppliers, and others upstream in the supply-chain, establishing a more holistic approach to tackling these goals. Some contract and custom manufacturers in the US have already noted requirements for sustainability appearing in their contracts. Global organizations, such as “Together for Sustainability” and “EcoVadis”, are beginning to arise to address standardizing approaches to measure and certify these criterion.

3 Near-term horizon

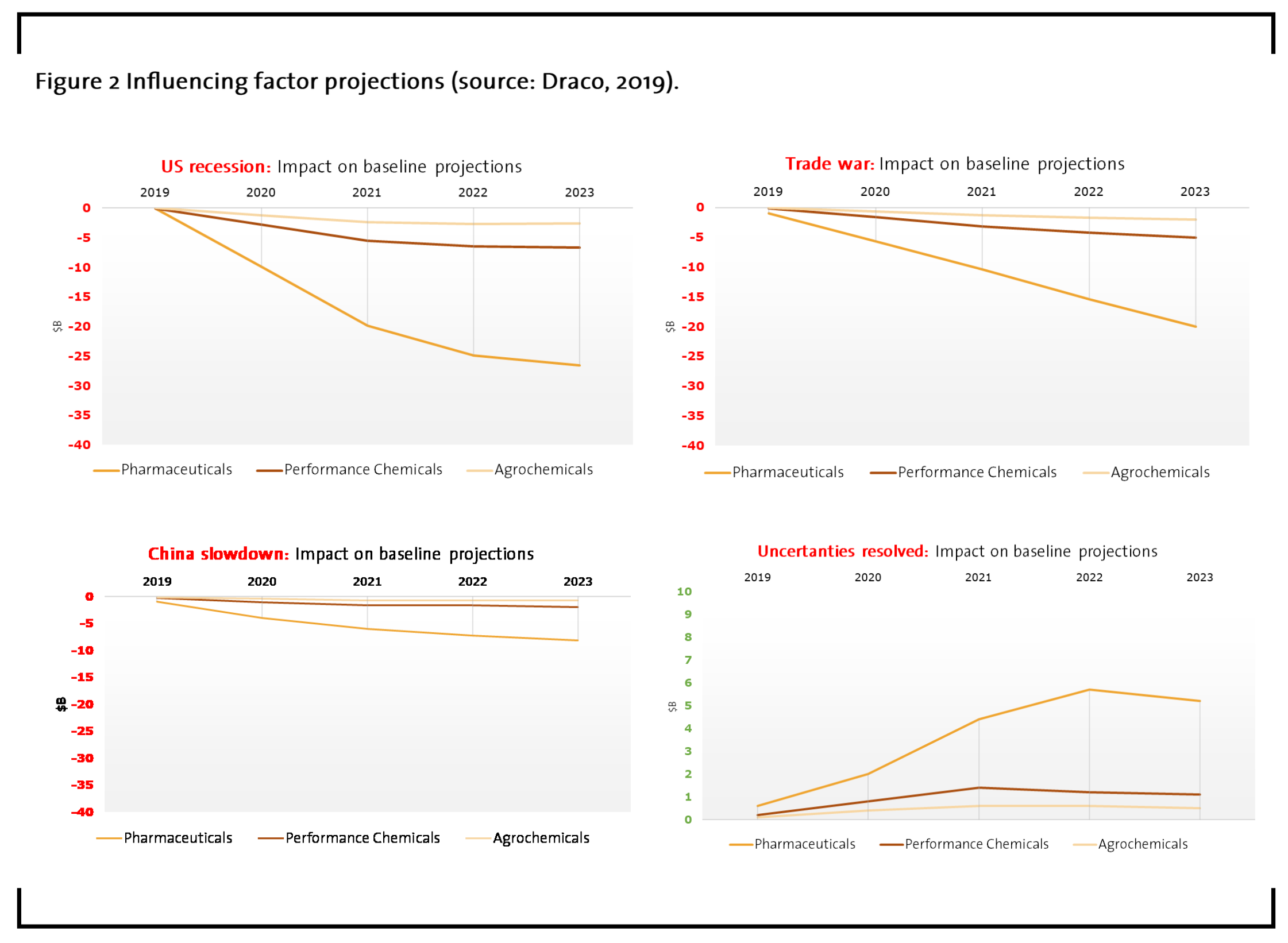

The most frequently predicted influencers for the US economy in 2019 have been around a domestic recession, an escalation of trade tensions, or a stalling of the Chinese economy and thus, their global buying power. While none of these would result in a contraction for the specialty and fine chemical market, they do correspond with up to $30B loss in unrealized year-over-year revenue per influencing event, as compared with the projected sales volumes reviewed in section 2 of this report.

Conversely, the quick mitigation of these factors would enable some sectors to grow by an additional $5B annually in addition to already projected expansions. In a recent survey of specialty chemical industry executives, over 40% affirmed they believe a US economic recession is imminent and will impact their business growth, while only about one in ten believe that trade war tensions will continue to escalate past their current state.

Given the breadth of contract and custom manufacturers in the specialty chemical industry and the demographics’ tendency toward batch processing, many facilities and companies stand able to take on repatriated volumes with little or no modifications to their systems. This agility mutes the impact of tariff/trade war induced revenue losses in comparison with an overall US economic recession, where capital investment would be tighter and could not accommodate any expansions or alterations made to facilities.

4 Long-term horizon

Looking forward for the specialty chemical industry, as in many sectors, artificial intelligence is identified as a major factor in altering the economics of manufacturing. Automated processes shift the levers of cost structure from wage-based to the cost of energy and quick and easy access to markets. When heavily implemented, artificial intelligence can be expected to encourage a sort of “regionalization” or “near-shoring”, compared with the globalization that has been observed in the last decade. A recent report by the McKinsey Global Institute commissioned by the World Bank Group notes that the overall pace of growth for global chemical supply chains has slowed to 5.5% between 2007 and 2018, down from 7.8% between 1995 and 2007 (Lund, et al, 2019).

Due to its cost-benefit advantage and the tendency of chemical industry leadership to utilize cost-cutting as the primary driver for profitability at a rate of 3:1 (Gotpagar, et al, 2018), one could expect artificial intelligence technology to move ahead as one of the more prevalent long-term issues taken-up and addressed. An often unanticipated factor for company valuations during mergers and acquisitions is a company’s consideration for sustainability. Anthesis Group, a global sustainability consultancy, notes that it is important to remember that “not every company can impact all 17 of the United Nations Sustainability Development Goals, but all businesses should identify which goals they do impact and how they have an opportunity to contribute to their achievement throughout the full value-chain of their business.” In the contract and custom manufacturing space, it’s becoming more and more common place to view this area of the supply-chain as something downstream companies face rather than part of a framework for performance and customer evaluation.

Along the digital front, a cross-industry and cross-sector issue often considered more to do with risk mitigation is cyber security. The risk and exposure to chemical manufacturers spans from operational and process disablement to intellectual property and should be assessed for mitigation via technological barriers as well as insurance policies to protect against financial windfalls. During a forum for executives in the specialty chemical sector in Houston in May, Laura Burke, Vice President of McGriff, Seibels and Williams, cited examples from Ukrainian based bank networks being taken down in under 45 seconds, to a 2014 operational attack on a steel mill in Germany resulting in process failure and equipment damage (Gaines, 2019). Specialty chemical business plans must take these issues seriously in order to stay competitive in the long-term.

5 A paradigm shift in supplier audits

Not only are sustainability requirements and cyber security measures being included in company valuations for M&A, but also in pre-engagement audits for specialty chemical contract and custom manufacturers across the US. A recent trade association report notes a dramatic increase in time spent on customer audits and preparing facilities to meet designated requirements – in many cases, even before discussing and finalizing contractual engagement. (Hirsh, Sept 2019). The increased rigor of these audits can present a business opportunity if specialty chemical contract and custom manufacturers are proactive in subscribing to a standardized sustainable audit framework. Assessments and audits which are conducted to a pre-defined set of criteria and shared across industry, improves efficiency for all involved (Unger, 2019). Similar to vertical integration and streamlining within specialty chemical companies themselves for shared services, companies could realize time and operational savings by agreeing to a common framework. Such a concept could be further utilized by chemical distributors and application enhanced by setting up centers and structures to bundle critical expertise and compliance with environmental and sustainability factors; identifying and sharing best practices and eventually applying KPIs to ensure continuous accurate assessment (Jung, U. et al, 2019). Buy-in across the specialty chemical manufacturing landscape for common, transferable goals will assure it is aligned with its customer base and contribute to the general transformation of the industry to a more sustainable sector.

6 Summary

The nature of the specialty and fine chemical industry necessitates that it be agile and well diversified across a range of processes and specific chemistries. The traditional factors which delay the impact of overarching economic trends to the chemical industry give the sectors a chance to react and reposition themselves to weather disruption more smoothly than others for near-term events. By keeping a steady eye on key indicators, such as material sourcing issues, international trade tensions, and US-domestic recession signals, specialty and fine chemical manufacturers can strategically plan for their business operations.

Looking further to the future, cyber security topics to protect intellectual property, against ransomware and against general bad actors, must come into focus as a matter of good business practices. A changing consumer demographic must also be taken into account, with a heavier emphasis on sustainability, from energy consumption to product life-cycle. Current industry statistics show the majority of the specialty chemical industry is not well versed in this area, but this must change for future success.

Observed shifts with attention toward sustainability in public-facing-consumer markets can be expected to drift up the supply chain to specialty chemical manufacturers. Heeding these trends and subscribing to standardized frameworks for measuring and auditing these processes will lead to favorability in the marketplace and reduced operational costs, long term.

References

Draco, G. (2019): Country Economic Forecast United States, Oxford Economics Group, New York, NY.

Gaines, J. (2019): Is Your Company Prepared to Thwart a Cyber Attack?, SOCMA Specialty Insights, Arlington, VA

Gotpagar, J., et al (2018): Chemicals Trends 2018-19 – A tipping point of profitability, PwC, Houston, TX, available at https://cadencebank.com/fresh-insights/business/is-your-company-prepared-to-thwart-a-cyber-attack, accessed 8 October 2019.

Hendry, J. (2019): Implementing the Sustainability Development Goals in your business, Anthesis Group, Ottawa, Canada

Hirsh, P. (2019, June): ChemTrends: Business Planning for Uncertainty, Society of ChemicalManufacturers and Affiliates, Arlington, VA.

Hirsh, P. (2019, Sept): ChemTrends: Preparing for Customer Audits, Society of Chemical Manufacturers and Affiliates, Arlington, VA.

Jung, U., et al (2018): Why Specialty Chemical Distributors Need to Raise Their Game, Boston Consulting Group, Chicago, IL, available at https://www.bcg.com/publications/2018/why-specialty-chemical-distributors-need-to-raise-their-game.aspx, accessed 8 October 2019.

Lund, S. et al (2019): Globalization in Transition: The Future of Trade and Value Chains, McKinsey Global Institute, Washington, DC, available at https://www. mckinsey. com/featured-insights/innovationand-growth/globalization-in-transition-the-future-of-trade-and-value-chains, accessed 8 October 2019.

Moutray, C. (2019): 2019 2nd Quarter Manufacturers’ Outlook Survey, National Association of Manufacturers, Washington, DC.

Unger, G. (2019): The Chemical Initiative for Sustainable Supply Chains, Together for Sustainability, Auderghem, Belgium.