Optimization of economic conditions in the chemical, pharmaceutical and medical technology industry through a stringently interlocking procurement in the holistic business approach

Abstract

The paper discusses the findings of a survey which was conducted in 2012 by ConMoto Consulting Group among top managers in German speaking countries. The aim of the survey was to analyze the value orientation of companies from a variety of industrial sectors, i.e. to evaluate the companies’ procurement. This paper briefly presents the overall findings, but the main focus is on the results of the chemical, pharmaceutical and medical technology sector. Finally, the success factors which lead to value-oriented procurement are outlined.

1 Introduction

Nowadays, if a company wants to be successful within a market and keep up with the fierce competition, it needs to focus on success factors which lead to value-oriented procurement.

Value-oriented procurement makes a substantial contribution to lowering material/non-personal and process costs, reducing the amount of capital required, and minimizing procurement risks. It also facilitates progress and innovation. Therefore, procurement should have an absolute command of three key areas: “Strategy and Innovation”, “Networks, Cooperation and Integration”, and “Processes, Technology and Standards”.

Since procurement plays an important role in terms of increasing the value of a company, an early inclusion of procurement is substantial in the context of achieving success and not being left behind when compared to other companies. In spite of this, there is still a large number of companies which do not make full use of the success factor that is procurement, as well of its development potential.

This is also the case with companies in the chemical and pharmaceutical industry which have not fully exploited their potential in terms of achieving a higher procurement performance. In order to achieve that, they should focus on developing a procurement strategy and work on enhancing the sway factors which will be presented in the main section of the paper.

When exploring procurement strategies, certain facts should be kept in mind, i.e. that 90% of chemical production is based on carbon compounds, which are mainly obtained from petroleum derivatives, e.g. naphtha, ethylene, propylene, benzene, phenol. Important markets in the chemical industry are China and India, and these are largely responsible for the supply of the so important commodities (BIP “Best in Procurement”, 2011).

2 How value-oriented is your procurement? – 2012 survey of top managers

2.1 Survey – Participants and Industrial Structure

In 2012, ConMoto conducted a survey “How value-oriented is your procurement?” among 111 companies from German speaking countries (Germany, Austria and Switzerland) to evaluate their procurement. ConMoto Consulting Group has summarized the findings of the survey, possible future fields of action and the success factors which lead to value-oriented procurement in the form of a study whose content will be presented in this paper.

The survey covered eight industrial sectors: service providers, mechanical and plant engineering, metal and electrical industry, automotive, chemical, pharmaceutical and medical technology, building sector, energy and energy suppliers and other (this category includes companies from aviation, food and also consumer goods sectors as well as print products, yarn, furniture and packaging manufacturers). It comprised a sample of listed companies as well as small and medium-sized enterprises (SMEs).

Top managers from these 111 companies rated their procurement on the basis of eleven core statements and by applying a grading system from 1 (“very good”) to 6 (“unsatisfactory”). The first nine statements aimed at evaluating the sway factors that impact value-oriented procurement, and the core statements ten and eleven were used to provide a final evaluation in terms of how satisfied the companies are with the contribution procurement makes to their success, and to explore its development potential.

2.2 Core Sway Factors

The evaluation was based on the following nine core sway factors and their underlying core statements (ConMoto Group GmbH, 2012):

- Sway factor: Procurement Strategy

The core statement underlying this sway factor is: An up-to-date procurement strategy derived from your business strategy is in place. A development program has been defined for implementation and communicated to all parties involved in the process. - Sway factor: Organization and Procurement Process

The core statement underlying this sway factor is: The procurement process in your company is fast, flexible and efficient. Procurement is integrated across all stages of the process early on (cross-functional operation). - Sway factor: Employee Qualification

The core statement underlying this sway factor is: You are satisfied with the qualifications and the flexibility of your procurement staff. - Sway factor: Decision Efficiency

The core statement underlying this sway factor is: The decisions awarding contracts (prices, terms and conditions and content) to your suppliers are systematically reached and documented, with all internal partners involved in the process casting a vote. - Sway factor: Material Group Management and Cost Transparency

The core statement underlying this sway factor is: Your procurement department has bundled the goods and services to be procured in a systematic effective and cost-transparent manner. - Sway factor: Supplier Management

The core statement underlying this sway factor is: Your suppliers’ potential for innovation and adding value is known and transparent. There are constant efforts to tap this potential. - Sway factor: Risk Management

The core statement underlying this sway factor is: Your procurement department consistently takes steps to hedge against risks, e.g. arising from volatile procurement markets or

the threat of supplier insolvencies. - Sway factor: Intensifying Competition

The core statement underlying this sway factor is: Your company is familiar with and uses global supplier markets and specifically “develops” intense competition. - Sway factor: Performance Management

The core statement underlying this sway factor is: Procurement performance and/or the value contributed by procurement within your company are measured and reported to the company’s management.

In spite of the negative outcome within some sectors, the survey has shown that there is still substantial room for improvement, which would eventually enhance the company’s results and liquidity.

3 Results for the Chemical, Pharmaceutical, and Medical Technology Cluster

3.1 Grades awarded for the Core Sway Factors

This paper has, so far, addressed some general issues related to the study design, i.e. its participants and industrial structure, but will, in terms of the above listed nine sway factors, mainly focus on one particular industrial sector, i.e. chemical, pharmaceutical, and medical technology (ConMoto Group GmbH, 2012).

Every industry has its own characteristics and specific features, and so does the chemical, pharmaceutical, and medical technology sector. In this industry, the qualitative requirements are very high, and thus strong supplier relationships are essential. The partial geographical bond together with choosing the adequate improvement method also present challenges that need to be taken into account in order to increase and, to the greatest possible extent, optimize the results and findings from the chemical, pharmaceutical, and medical industry which have been listed in the study.

The industrial procurement of chemical and pharmaceutical products and materials is subject to very specific and extremely critical challenges. The crude oil price coupling is reflected in the very volatile markets. The result is that a hedge is hardly possible, let alone the possibility to calculate economically.

A geographical bond, depending on the location of recovery and production of materials or components, has partially a significant anti-competitive effect. The same effects come from situational and structural factors such as material losses and market adjustment. Long-term supply contracts, vertical integration (backward integration), and increasing the resource efficiency can help in this situation and ensure supply.

3.1.1 Procurement Strategy

Regarding the first sway factorProcurement Strategy, the chemical, pharmaceutical, and medical technology cluster lag far behind – with 18% of the decision-makers declaring that they have no procurement strategy and 27% rating their procurement strategy as patchy. The results are related to the failure to develop a general coordinated business strategy that is communicated within the company, and thus an adequately communicated procurement strategy. Not only do companies have to formulate a procurement strategy, but permanently check and adjust it to ensure continuity.

Companies have no, or not consistent, coordinated and within the company communicated business strategy. Even in large companies, particularly in holding structures, there is a partial lack of a standardized strategy development process that takes into account the individual identity and culture of each subsidiary, as well as the effects of bundling in the group. This makes it difficult for the embedded business units, such as procurement, to shape their business strategies and add value. Through targeted bundling, the market power of a company can be sustained and strengthened, and lead to significant savings effects and other positive effects (earlier supply, consistent quality, etc.).

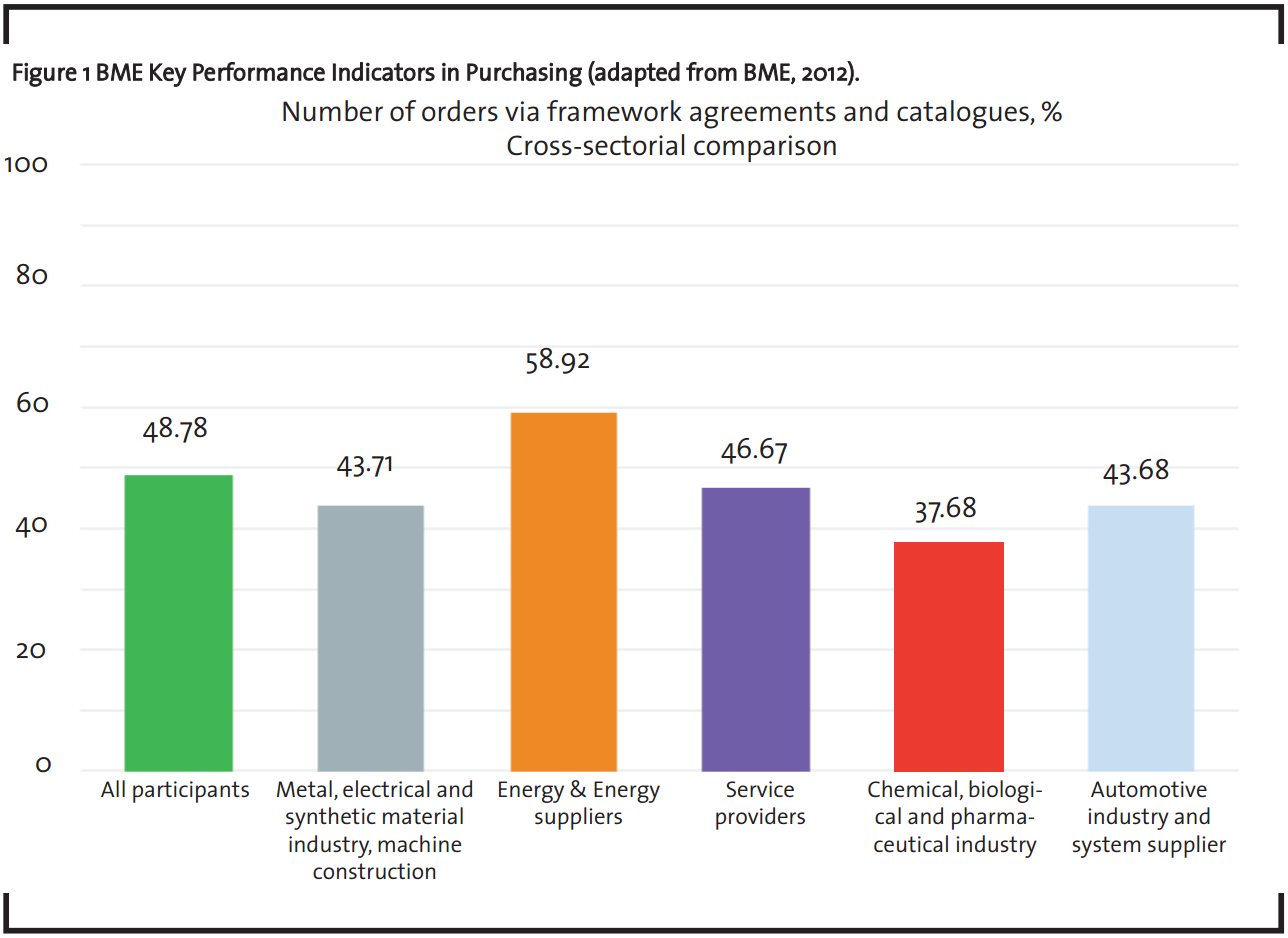

Without a general business strategy, there is no procurement strategy, and thus it is not possible to integrate effective procurement early. The majority of the following sway factors are directly related to the procurement strategy. A clear indication of this is, for example, the fact that in the chemical/pharmaceutical sector nearly 59% of the procurement volume is covered with long-term contracts. However, according to a BME study, the rate from framework agreements and catalogs is well below the industry average (37.6%) (BME, 2012).

3.1.2 Organization and Procurement Process

In terms of the second sway factor Organization and Procurement Process, i.e. swiftness, flexibility, and efficiency, the chemical, pharmaceutical, and medical technology cluster received a “satisfactory” rating (2.8). Of the decision-makers in this sector, 9% “strongly disagree” with the core statement that the procurement process is fast, flexible, and efficient, whereas 9% “entirely agree” with the statement. The ratings of the majority range from “somewhat disagree” to “almost entirely agree”.

The chemistry/pharmacy sector shows best practice in terms of the cost per order process. However, there is potential for improvement regarding the proportion of orders handled electronically, including statements (Procure-to-Pay). According to relevant studies (e.g. BME and University of Würzburg, 2013), the cost of the procurement process through e-procurement can be reduced by at least 30%. This is a potential that is not yet fully exploited in this industry.

The ratings in all surveyed industrial sectors show that procurement activities can be planned and managed more specifically, and such activities would eventually lead to a fast, flexible and efficient procurement process, but the organization of the procurement process should be adapted to suit the conditions of the company.

Although the early integration of procurement requires forward shifting and interlinking of procurement activities with the interface partners, the early exchange of information allows in return a more accurate planning and management of procurement activities. Particularly noteworthy is that the procurement market research and the actual procurement may run simultaneously with the planning activities, which can significantly speed up the procurement process. Through the “early procurement involvement” it is possible to identify, assess and manage risks and opportunities earlier. The best practice would be to establish a so-called “learning organization”, in which events are considered as a stimulus and used in development processes in order to adapt the knowledge and capacity to the new requirements. A predictive cross-functional cooperation between users and procurement becomes a guarantee for fast, flexible, and efficient procurement processes in the chemical industry. It is undisputed that there is no easy solution for this. Rather, the organizational design of the procurement should be adapted to the business realities and implemented with regard to a particular situation. A process orientation can be implemented only within flexible organizational structures, which are already present in the company.

3.1.3 Employee Qualification

With regard to the third sway factor Employee Qualification, the degree of procurement staff qualifications is seen as being predominantly or mostly satisfactory. Only 9% of the decision-makers in the chemical, pharmaceutical, and medical technology sector are “completely dissatisfied”, 46% are “somewhat/reasonably satisfied”, 36% “mostly/predominantly satisfied” and 9% “completely satisfied”.

Since value-oriented procurement has a substantial impact on a company’s success, qualified, motivated employees are needed. This can be achieved through the creation of extensive employee qualification schemes tailored to suit the company’s needs and through training courses for purchasers and groups of requisitioners.

According to a 2013 salary survey conducted by BME (BME and University of Würzburg, 2013), the chemical/pharmaceutical industry gives the highest annual salaries to procurement managers. However, this is not directly related to the qualifications of the procurement staff. The ratios of the BME study (BME, 2012) show that the costs of professional training in chemistry/pharmacy per employee are just above the industry average. If only 9% of decision-makers are “completely satisfied”, then there should be an increased investment in training to enhance the skills of procurement staff. Only highly qualified staff is cross-functionally accepted and early involved.

3.1.4 Decision Efficiency

The results for the sway factor Decision Efficiencyreveal that in the industry cluster for chemicals, pharmaceuticals, and medical technology, 18% of the respondents do not consider themselves at all capable of making their decisions “efficiently”, whereas 18% of them “entirely agree” with the statement that the decisions for awarding contracts to the suppliers are systematically reached and documented.

The overall results show that decisions are generally not sufficiently documented, and that companies should pay more attention to coordinating and introducing role assignments, ground rules, and reports.

Decision efficiency and transparency is increasingly important component of the role of procurement within cross-functional teams. When considering the ever-worsening compliance criteria, it is clearly understood that an order should be documented and countersigned to ensure a verifiable security. Best practice is an independent decision-making body that examines relevant decision documents and agrees upon the selection. The competition among providers can thus be optimally maintained.

3.1.5 Material Group Management and Cost Transparency

Furthermore, the respondents from the chemical, pharmaceutical, and medical technology sector give their Material Group Managementa midtable ranking (2.7). Only 9% “strongly disagree” with the core statement that their procurement department has bundled the goods and services to be procured in a systematic, effective and cost-transparent manner. The majority of the respondents, 46% “mostly/almost entirely agree” with the aforementioned statement. The overall results for this factor, unfortunately, show that, although companies have much knowledge of the goods and services to be procured, it is rarely documented systematically and transparently, and there is no progress in how it is structured further.

The chemistry/pharmacy sector has still room for improvement in the perception of procurement responsibility, because the volume which is influenced by procurement is the industry average, while the rate from closed frame agreements is even significantly below the industry average (see figure1). Low rates from closed frame agreements point to weaknesses in the procurement processes or optimization of material group management. Frame agreements were made, but are not being used sufficiently by requisitioners or purchasers. Therefore, improvement and associated assistance is also needed in this area.

3.1.6 Supplier Management

Regarding the sway factor Supplier Management, the findings in all sectors show that only a small percentage of the surveyed companies (4%) made full use of the innovation potential and value-added reserves of their suppliers. In case of the chemical, pharmaceutical, and medical technology sector, 9% of the respondents entirely agreed with that, and half of the respondents thought there is still considerable potential for improvement in terms of how procurement can help make working with suppliers more successful.

However, the potential for enhancing efficiency and effectiveness in procurement has so far only been used by a few pioneers. Key issues, such as supplier management, are poorly implemented. Thus, it is important to work on developing efficient supplier management systems, and strengthen the relationship between the manufacturer and suppliers by assigning them the role of value-adding partners who will eventually contribute to quality work outcomes.

3.1.7 Risk Management

The companies in the chemical, pharmaceutical, and medical technology sectors gave their Risk Managementa satisfactory grade (2.6). 27% of all respondents do not believe that they are capable of taking “mostly” consistent measures to hedge against risks, whereas 18% “entirely agree” with the statement that the procurement department takes steps against risks. The overall results actually confirm that risks which companies encounter and have to deal with (risks associated with countries, branches, currencies, contracts and liabilities) are still frequently not taken into consideration in the procurement process, which eventually might lead to quality issues. Because of that, the procurement department needs to develop a strategy which would ensure consistent measures which would reduce or minimize risks. Particularly in relation to security of supply and maintenance of quality standards, a continuous monitoring of suppliers is important, as it is in respect of commodities e.g. from politically unstable regions where forecasting is difficult.

3.1.8 Intensifying Competition

The results for sway factor Intensifying Competitionreveal that respondents from all sectors gave themselves an average grade of 2.5 which is also the average grade awarded in the chemical, pharmaceutical and medical technology sector. Of decision-makers in that sector, 18% “entirely agree” that their company is familiar with the global market and the competitiveness within that market. 36% “mostly/almost entirely agree” with that, whereas 9% “strongly disagree”.

The overall results for this sway factor have confirmed that there is a substantial number of companies that still have no clear picture of their national and international procurement markets, which eventually means that some new procurement markets are not being used and that potential suppliers have not been identified. Hence, the focus should be on the use of global supplier markets and development of intense competition.

Due to a partial geographical bond, but also because of the highly specified control and aptitude tests in chemistry, an intensified competition is expensive, and is only feasible through early involvement of the quality, research and development department.

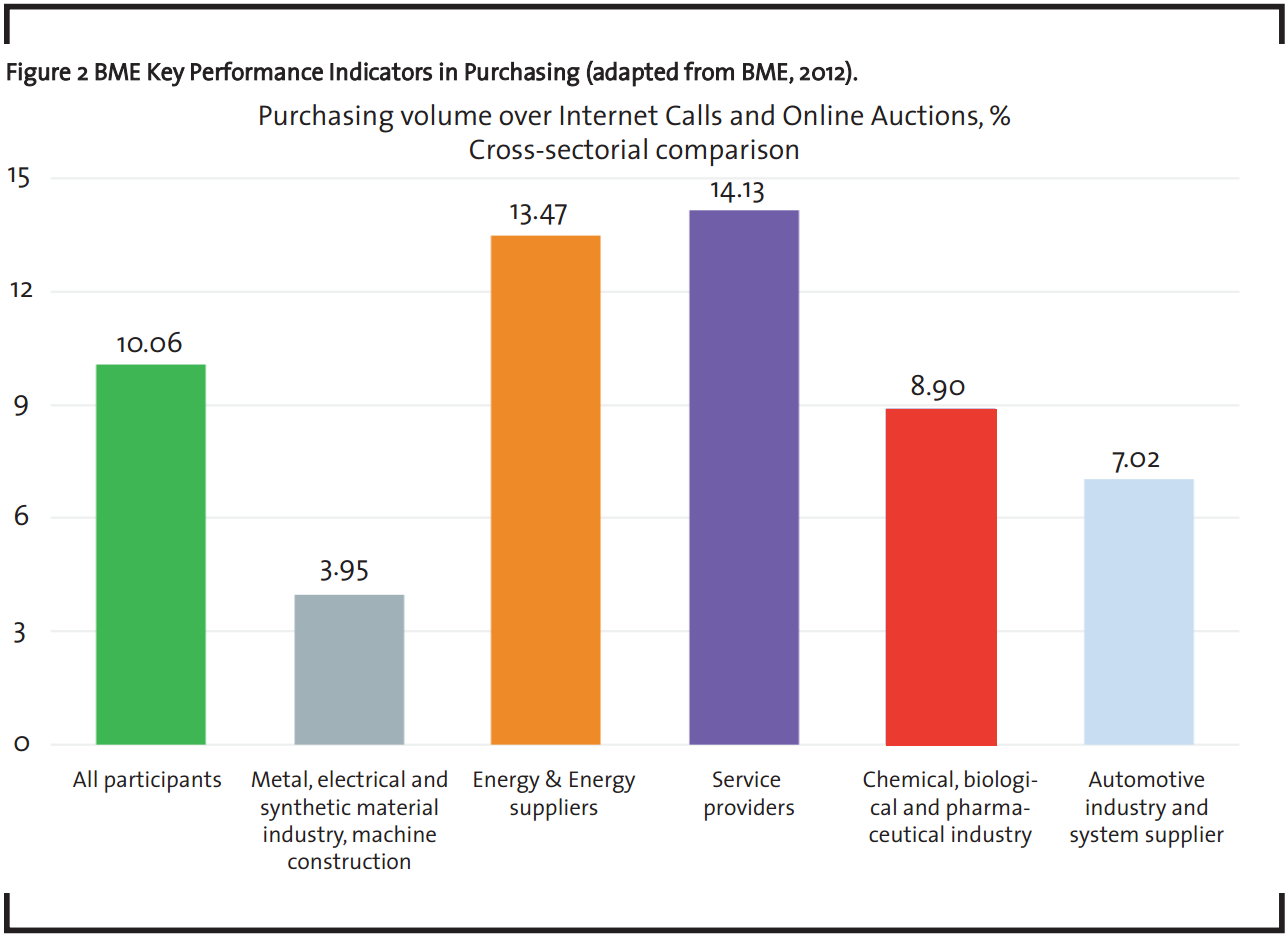

The low level of efficiency of online auctions and sourcing activities in chemistry/pharmacy, which is slightly above the average in the industry sectors, indicates that there is a significant untapped potential in relation to intensifying the competition. The intensifying competition also includes the use of e-sourcing and e-auction. The purchasing volume, which is handled via the aforementioned methods, can still be improved (see figure 2).

3.1.9 Performance Management

The sway factor Performance Management received the best average grade in the survey (2.3). It is interesting that 36% of the respondents in the chemical, pharmaceutical and medical technology sector measure and report on their procurement performance regularly every month. Only 9% never report on such performance. The overall results show that a mission for procurement is needed, and highlight the importance of measuring procurement performance systematically.

The procurement power, i.e. the value contribution of procurement is mostly properly assessed, measured and reported to the management by the procurement managers in the chemical industry. Adding value to the company’s profit is perceived very well in the chemical sector by other areas of the company, and also acknowledged, because a systematic and verifiable measurement of procurement power takes place as part of controlling involvement.

Reporting instruments and stringent tracking of measures along a hardness level system are widely known, but are rarely used in many industries. However, this is not the case within chemistry. In addition, there is often a lack of an (within the company) acknowledged “Savings Guideline” in which the starting points are defined for the purposes of properly calculating and measuring procurement performance. A particular challenge in the chemical/pharmaceutical industry is the clear distinction of the starting points due to the volatile markets. Windfall profits or the increase of commodity prices such as oil are to be reported or eliminated. Costs for risk hedging purposes could be considered. Essential for this is the previously established “Savings Guideline” and a careful selection of absolute and relative indicators to identify changes and trends, and take appropriate control measures within and outside the organization.

3.2 Position in the ConMoto Maturity Model for Value-oriented Procurement

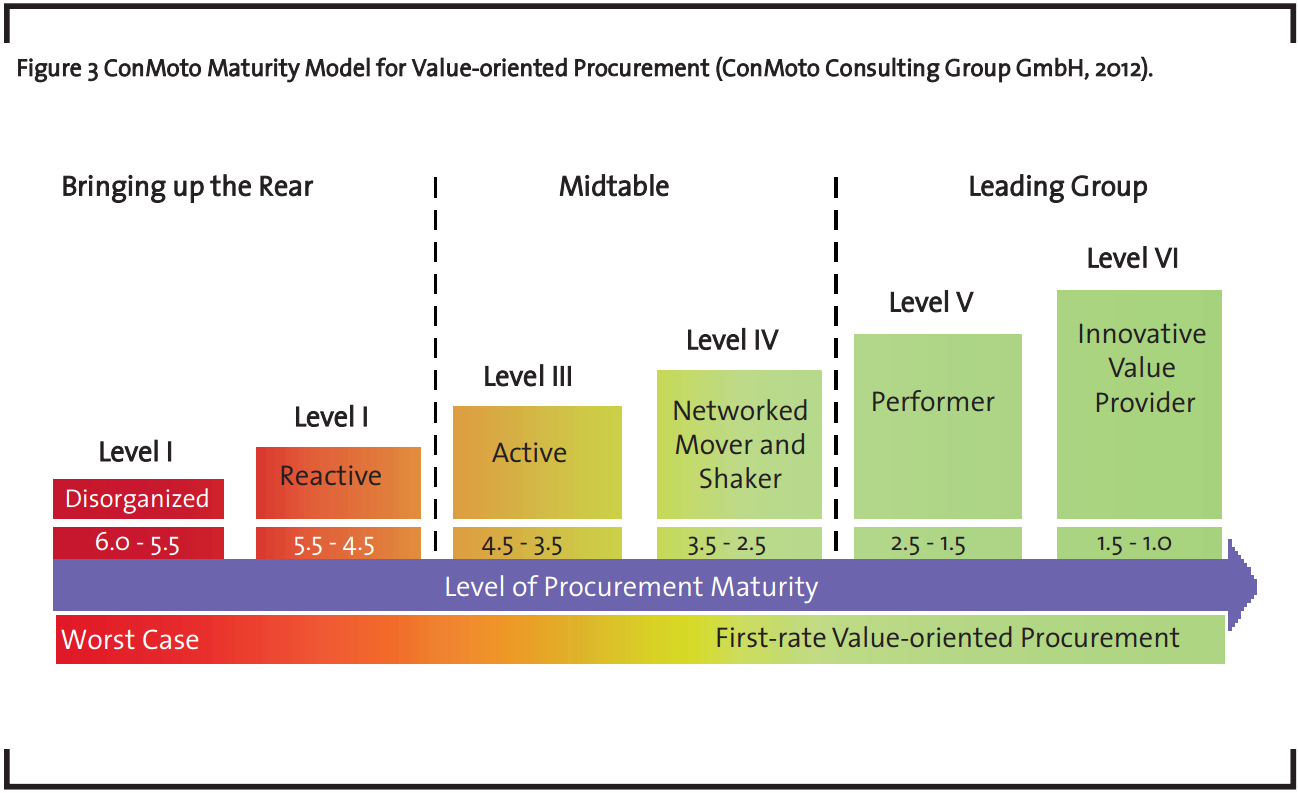

Based on the findings of their survey, ConMoto has developed a maturity model for value-oriented procurement, in which they have classified companies into different levels (ConMoto Consulting Group GmbH, 2012):

Level I “Disorganized”: Procurement processes are disorganized and not clearly defined. The procurement process is often initiated by the requisitioner, i.e., it is decentralized (= Maverick Buying).

Level II “Reactive”: Procurement is reactive and there is not sufficient market research. Here, procurement functions as a clerk’s office and has no influence on the procurement decision, which was already pre-empted by the requisitioner. There is no active control system through procurement.

Level III “Active”: Procurement structures are defined. The procurement has still no large control function. Bundling through projects and throughout the sectors does not occur. However, there are some proactive bids for required scope.

Level IV “Networked Mover and Shaker”: Procurement plays an important role within the company, and is aware of the company’s contacts to suppliers. Procurement is included early in the requisition processes and may help create and control. Requirements can thus be bundled through projects and throughout the sectors. Procurement is an accepted partner both internally and in communication with the suppliers.

Level V “Performer”: A sourcing committee has been established, and the decisions are reached collectively. Procurement department is a process driver. The procurement strategy is in line with the corporate strategy and the processes are efficient, coordinated, and lived throughout.

Level VI “Innovative Value Provider”: Decision efficiency is at the highest possible level. Procurement department shapes processes and is not only an innovator, but a value driver as well. Suppliers are also part of the innovation process. The procurement strategy is optimized continuously. Procurement is a learning organization.

In short, it can be stated that Level I-III can contribute only limitedly with their hard-earned savings. A long-term increase in value does not start until Level IV, in fact it is supported by the use of all procurement leverages:

- Increase in operating income by reductions in the cost of capital

- Targeted reductions in the cost of materials and manufacturing

- Streamlining of business processes

- Contribution to sustainable profitable revenue growth by utilizing the innovation power of suppliers and thus ensuring competitiveness

- Reduced time-to-market and reaction time.

As it can be seen in figure 3, the levels are further grouped into three categories: “Bringing up the Rear” (Level I and Level II), Midtable (Level II and Level IV) and Leading Group (Level V and Level VI). Regarding the chemical, pharmaceutical and medical technology sector, the respondents rated their procurement as “satisfactory”, and therefore this sector falls into the Level IV category of “Network Mover and Shaker” in the maturity model, which means that it has an upper mid-range ranking. It also implies that there is still work to do before it can reach the best level, i.e. “Innovative Values Provider”. Another interesting fact in terms of the grades awarded for the core sway factors is that the spread of the grades for best (1.1) and worst (4.9) rated companies is most prominent in this sector.

The ConMoto Maturity Model shows the general state of the chemical industry in the overall economy among the companies surveyed. The survey of top management participants in the industry sector “chemistry” shows that there is still a lot to improve, and enormous potential could be generated through the procurement and its setting and value in the company. The conducted study has confirmed the practical knowledge gained through numerous projects in chemistry, and has given further insights in the approach and potential for improvement.

4 The Succes Factors

4.1 Twelve success factors

Based on their experience and engagement in projects, ConMoto’s procurement experts have highlighted the success formula for procurement, i.e. the twelve core components which lead to first-rate value-oriented procurement. These twelve factors should be regarded in individual contexts and should be adapted to the company’s specific situation (ConMoto Consulting Group GmbH, 2012).

- Strategy and Implementation Expertise

It is essential to develop a corporate strategy that will then impact the procurement strategy. Without the procurement strategy, there are no common goals and thus no targeted control of the employees. The strategy elements and fields of action which need to be taken into consideration, include customer requirements, vision, mission, basic conditions, goals, responsibilities and deadlines, budget, and target agreements. In order to successfully pursue these elements, it is important to report any deviations as soon as they occur. The strategy must be coordinated efficiently and be in line with the management. Adjustments and optimization must occur in the context of a learning organization. - Decision Efficiency

The procurement department plays an important role in the process of make-or-buy decisions, innovation, product emergence, and the general procurement process. It is involved in improving decision efficiency by establishing a sourcing committee. This body needs to reach important decisions in terms of assigning tasks and awarding contracts. It is important that the committee is composed of members of departments involved in the process, and that all members are equal, so that the decisions and the impact of decisions are equally shared. However, procurement has to play the leading role in this committee in terms of processing all decision documents. - Financial Management

Savings guidelines are being introduced in order to measure procurement success transparently. These guidelines enable the calculation of financial procurement performance one year in advance. However, it is necessary to coordinate this calculation, which means that more departments, i.e. controlling, finance, and procurement departments, need to cooperate in preparing and performing the calculation.

A commonly agreed savings guideline prevents differences in the measurement and representation of procurement services. This increases the acceptance and appreciation of procurement within a company. A savings guideline is an absolute requirement for performance measurement in relation to the objectives set in the strategy. - Change Management

Due to market changes, the management process also undergoes changes. This calls for the procurement department to adapt to such new requirements by changing basic conditions, processes, and goals. This assumes taking internal customer requirements into consideration. New approaches should be developed and agreed upon together with the internal customer, so that these approaches are then actually adapted and lived. If solutions were imposed, the internal customer would feel “hindered”, and assume a defensive approach. Early integration and communication are here the alpha and omega, and thus essential for success. - Organizational Quality

The procurement department is a learning organization, which means that it adapts its organization to its internal customers. This upto-date approach leads to improvements regarding work instructions and organizational guidelines.

Here, procurement should be considered as the “driver seat” and again contribute to suggestions, as well as support suppliers to enhance innovation management. Suppliers can be disseminators of innovative ideas and solutions. - Human Resource Management

The procurement staff is an important force within the company, and therefore needs to be provided with comprehensive and specific training which will develop their qualifications. Such training will enhance the performance-oriented component, efficacy, and efficiency of the staff. In order to develop the most appropriate training and continue to play the role of active “Movers and Shakers”, the procurement staff is regularly monitored and evaluated.

ConMoto has developed one such specific training program, i.e. “QAMPUS”, which includes “Basic”, “Professional” and “Excellence” modules. These modules help employees meet their challenges and needs. Valuable theoretical approaches are underpinned here, with many practical examples and application exercises, and upon request developed in cross-functional teams and deepened together. This fosters cross-departmental communication and understanding of the respective roles within the company. - Quality Performance

The procurement department monitors the quality performance through a quality assurance system, and implements the received data into its sourcing decisions. If any problems with suppliers occur, the procurement department will assist staff in quality assurance. Quality performance is also an important part of supplier management and can, in the worst case, generate very high unwanted costs (delays, complaints, product recalls, loss of reputation, etc.). - Supplier Management

The procurement department possesses relevant data regarding the suppliers which they receive through researching the market, i.e. the global procurement market, and reviewing competitiveness of its suppliers. The competitive environment of suppliers is used by procurement to attain competitive advantage. But also shortening the delivery time, process improvements, quality improvements can be worked out together with the suppliers and lead to ensuring competitiveness. The development of new suppliers is part of the supplier management and is essential for a long-term cooperation. - Innovative Capacity

Product innovation and progress is also pursued by the procurement department. It conducts research in order to follow the developments on the supplier market. Such developments are then integrated into the company’s own production development process. - GRC Management (Corporate Governance, Risk Management, Compliance)

The procurement department is also part of the risk management system which tries to prevent any delivery failure. The staff aims at applying regulations which will prevent potential conflicts and risks. If a deviation occurs, it is recorded and corrected. GRC plays a major role with respect to the image both internally and externally, which again is important for the area of public relations. - Contract Management

Regarding contractual negotiations with suppliers, the procurement department plays the central role. The contracts are stored and processed electronically, and their content is reviewed in order to check whether they are in agreement with the rules. Compliance and transparency are here the top criteria, which can only be achieved through centralized contract management. An alert function supports early renewal, extension or early termination of contracts. Duplicates and incorrect versions of contracts are prevented. - IT / Data Management

An IT strategy plan also enhances the procurement processes, and thus procurement staff is trained to use the latest communication systems. All data structures are up-to-date and in accordance with industrial standards. IT requirements and standards are to be agreed upon and set by an expert panel, so that they can be bundled through frame agreements and negotiated centrally. Another field can be more optimized through e-procurement, e-sourcing, and e-auctions. Standardized procurement processes can be depicted through portal or cloud solutions, and safely and efficiently handled. Integrated electronic procurement systems also support the supplier management (training, evaluation, development), catalog management for C items (i.e. marginally important items for an organization in terms of their value and contribution to making profit), the spend management and contract management. E-sourcing simplifies the procurement market research, and all RFX processes1 and e-auctions increase

competition.

4.2 Success factors in chemical, pharmaceutical and medical industry

Success factors, for which the chemical/pharmaceutical industry received the lowest grades, offer conversely the largest potential for improvement:

According to the findings of the study, companies in the chemical, pharmaceutical, and medical industry were ranked 8 of 8 in terms of Procurement Strategy, and thus placed at the bottom. Many small and midsize companies do not have or have no consistently coordinated business strategy from which, by taking into account the situation on the procurement market, the procurement strategy would be derived. The respective strategy components are to be developed together with all responsible persons in order to provide a systematic and standardized methodology and definition of success factors which the companies often lack.

Regarding the factorDecision Efficiencycompanies in the chemical, pharmaceutical and medical industry have still many optimizations potential to generate, because after the analysis of the

study in this area they were positioned at the bottom (ranked 8 of 8).

The most important point along the procurement process is the decision on awarding contracts to suppliers which would consider prices, conditions, and a defined scope. Frequently, contract award decisions are not directly made by the procurement department, but the specialist areas make sure that specific suppliers’ products and services will meet their requirements. There also might be some dependency on patents, subscription rights or tools owned by suppliers. Thus, not the best decision for the company is made, but individual interests of a department are considered. Contract award decisions are often not transparent and not sufficiently documented.

According to the study, the results for the factor Performance Managementare much better in the chemical, pharmaceutical, and medical industry. In this occasionally essential area, there is much room for improvement (rank 6 out of 8) to strengthen coordinated Performance Management. The mission and the function of procurement is often not clearly defined and coordinated. A „Mission Statement“ exists only rarely.

Procurement performance, i.e., the value-added procurement, is correctly assessed by responsible persons in procurement, but is rarely measured and reported to the company’s management. In this way, this added value is not perceived by other business areas, nor will it be acknowledged, unless there is a systematic and verifiable measurement of procurement performance.

5 Conclusion

In the ConMoto Study, companies that operate in the chemical, pharmaceutical, and medical industry show their weak points in different areas of procurement, but in turn have potential for the following areas, which will especially be reflected in the results of the company:

From the findings of the study and through an adapted methodology in the chemical, pharmaceutical, and medical technology sector, the foundation of a professional procurement is integrated, within the company coordinated and communicated procurement strategy, which takes into account the individual identity and culture of each subsidiary, as well as effects of bundling in the group. Accordingly, a systematic methodology is to be applied, and success factors should be defined.

In order to define the delegation of decisionmaking, an awarding body, i.e. a sourcing committee, in which all partners involved in the process would participate and have full voting rights, should be established. A distinction between, on one hand, the operational procurement and negotiation activities, and on the other hand, the actual contract award decision would be perfect. Introducing role assignments, ground rules, and reports are not to be underestimated.

In order to produce regular reports on procurement performance for the management of the company, reporting tools and a stringent pursuit of measures should be enhanced. However, there is also a need for a “Savings Guideline” acknowledged within the company, in which the starting points for an unambiguous calculation and evaluation of procurement performance would be defined. The status of procurement within the company is also increased through regular communication of procurement performance and the contribution to the company’s profit.

Due to the interdependence of corporate strategies and procurement strategies, it is necessary to coordinate the persons involved in the procurement process, and to avoid any information asymmetries within the company. Consequently, they will develop a high sense of responsibility. It is also beneficial and has a positive impact on the process itself when authorized persons are involved from the beginning of the process.

To achieve procurement potential through the conscious development of an elaborated supplier management, is one of the key points of a procurement potential analysis. For a comprehensive optimization, together with other areas in the company, (cross-functional) integrated approaches to optimize the collaboration within the company are to be developed. Only through a long-term orientation of processes and structures towards the principles of the company and a trustful cooperation with synchronous use of the competitive situation, the full savings potential can be achieved. For this purpose, the procurement potential analysis serves the objective to observe and, for different product groups, implement the most efficient material group strategy with different levels of cooperation intensities by the staff. Prerequisites for achieving these objectives are the intensive use of the supplier’s know-how and the creation of problem-solving capacity in procurement and its integration into the overall corporate image.

Likewise, the training, assessment, and development of suppliers pose a far underrated contribution to generating potentials. These three levels provide the basis for quality assurance, price negotiations, and deriving the consequences from the assessment. The vertical range of manufacture in companies is steadily being reduced, which leads to the fact that the procurement volume is between 40-70% of the turnover, and that reflects the increasing importance of the procurement department and supply chain management (BIP “Best in Procurement”, 2011).

In spite of its significance in terms of contributing to the company’s value, many companies have still not fully realized the value-added potential of procurement and, unfortunately, have not implemented a first-rate value-added procurement management system. The sooner they identify its significance, the earlier it can contribute to their own success. In order to pursue that goal, companies should focus on the success factors which will help them work towards value-oriented procurement as well as define future tasks and fields of action using the best in the industry as their benchmark. Not only cost reductions, but also quality improvements, product modifications, reduction of production, throughput, and delivery time can be initiated by procurement and performed collectively in cross-functional teams (BIP “Best in Procurement”, 2011).

References

BIP “Best in Procurement” – Das Fachmagazin für Manager in Einkauf und Logistik, Ausgabe 6 (November/Dezember 2011): Interview mit Karsten Malsch, Head of Strategic Commodities, BayerMaterial Science AG, Leverkusen.

BME (2013): Gehaltsstudie 2013, Frankfurt.

BME (2012): TOP-Kennzahlen im Einkauf 2012, Frankfurt.

BME and University of Würzburg (2013): Stimmungsbarometer Elektronische Beschaffung (über Stand der Nutzung und Trends), Würzburg.

ConMoto Consulting Group GmbH (2012): ConMoto Study “How value-oriented is your procurement?”, Findings of the 2012 survey of top managers, Munich, pp. 4-24.