Size does matter in chemical distribution

This article provides an overview on the current and likely future situation of chemical distribution in Europe. Chemical distribution markets in Europe are described and put into global perspective. Chemical distribution is compared to other distribution channels (direct sales, agents, traders, resellers) and reasons for the above average growth rates of chemical distribution are given. In addition, underlying root causes for the recent consolidation trends in chemical distribution are analyzed. As the article forecasts that size matters, further consolidation can be expected in this sector in the near future. Different characteristics and key success factors for distributing either standard molecules/bulk industrial chemicals or providing specialty solution chemicals are discussed. For the former local asset effectiveness is identified as a major consolidation driver, whereby for the latter three growth and profitability drivers are postulated.

1 European chemical distribution markets in global perspective

1.1 Introduction to chemical distribution

More than 85% of global chemicals are sold directly by the producers. Less than 15% are sold indirectly, either through agents, traders or chemical distributors.

Agents typically receive a pre-agreed commission from the producer and price the chemicals according to the producer´s instructions. Agents do not take title of the chemicals and they are very often small “one-man-bands”. Their success factor is the knowledge of a seller and potential buyer of certain chemicals and bringing them together.

Traders are typically active upstream in the value chain, trading commodity products in large “parcels”, which are often moved by vessel or barge. They take title and buy on own account or on behalf of a customer. Most frequently, traders buy “back-toback” and do not have any stock. Their knowledge of supply markets, their arbitrage, pricing and global logistics skills are the major differentiators. In the end, traders follow an “opportunistic” business model, in which the availability and price of chemicals determine, if they are successful or not.

Chemical distributors typically buy, store, sell and ship chemicals. They show activities further downstream, take title of the chemicals and offer a wide product mix, ranging from bulk commodity chemicals via plastic and rubber materials to packed specialty chemicals, which often require specific application know-how. They often bundle products in their warehouses and offer additional services over and beyond the logistical supply chain and commercial sales functions. Those services can range from mixing, blending, packaging, drumming, labeling via just-in-time delivery, financing, waste handling, regulatory, environmental, health, safety and laboratory services to recycling and consulting. Chemical distributors establish resale prices that ensure healthy, integrated margins. Sometimes, chemical distributors also act as traders or even as agents. For those parts of their business, only trader margins and commissions, but not revenues, have been considered in the following business and overall market numbers.

The following views and findings regarding the role, growth, most important actors and consolidation trends of chemical distribution in Europe result from consulting chemical distributors and their principals, interviews and discussions with many managers involved in the distribution of chemicals, and the participation in the European Association of Chemical Distributors (FECC) conferences.

1.2 Role and value proposition of chemical distributors in between principals and customers

When looking at the motivations in order to increase sales via chemical distribution, particularly in specialty solution chemicals, principals/producers, customers and chemical distributors themselves exhibit differences.

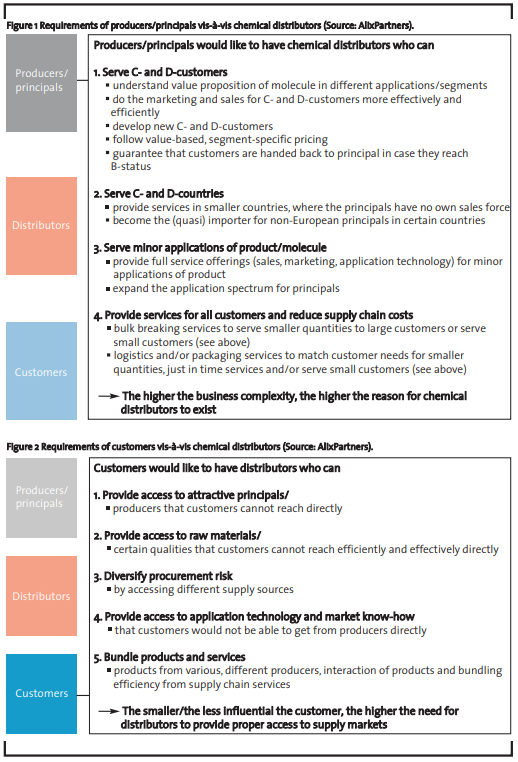

From a principal perspective (Figure 1), it is about serving C- and D-customers as well as -countries, applications and providing service to all customers at reduced supply chain and commercial costs.

From a customer perspective (Figure 2), having access to top principals through qualified chemical distributors, who can additionally complement the product, application and service portfolio is crucial.

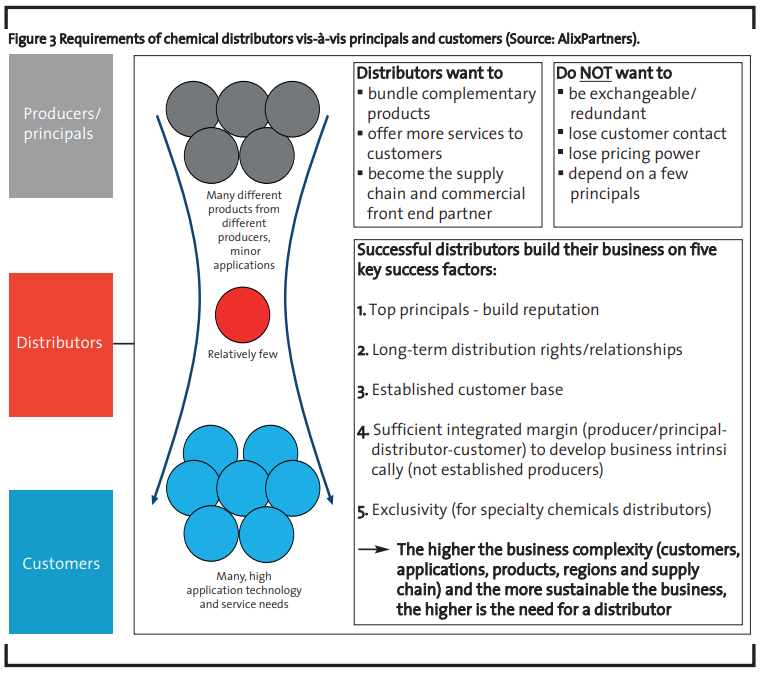

For the chemical distributors themselves (Figure 3), it is important to sustain their business and expand their value added between producers and customers. They aim to build long-term, exclusive relationships and distribution rights with top principals and build reputation by serving them well. They establish a customer base, which they actively care about. They aim to have an integrated margin that allows them to grow and develop the business intrinsically.

The attractiveness of the product-applicationregional segment might be different for a distributor than for a producer/principal. If there are only a few chemical distributors but many customers and different principals/producers in a given market segment, this would be a context that is more favorable for a chemical distributor. The more of these “hourglass”-like market characteristics, i.e. many different products from different producers, many minor applications, few chemical distributors and many fragmented customers with high technical solution and other service needs, exist, the more attractive the market segment appears to be for chemical distributors. In these kinds of market segments, distributors typically grow more than 5% per annum and generate more than 10% profitability (EBITDA/net revenues).

1.3 Size and structure of the European chemical distribution markets

It is difficult to define the size and structure of the European chemical distribution markets due to the fact that the borders between agents, traders and chemical distributors are not very well defined and due to the fact that many chemical distributors are small, family-owned, private companies which do not publish their performance and results. Therefore, only estimates are given in the following, based on experience gained in the sector.

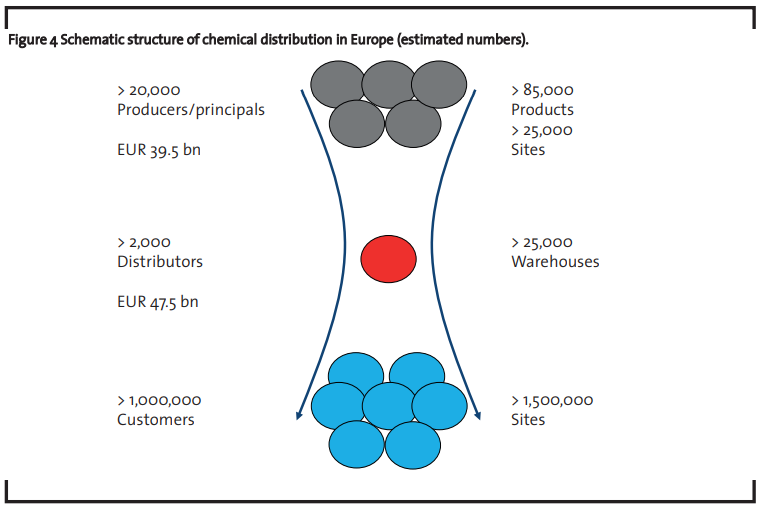

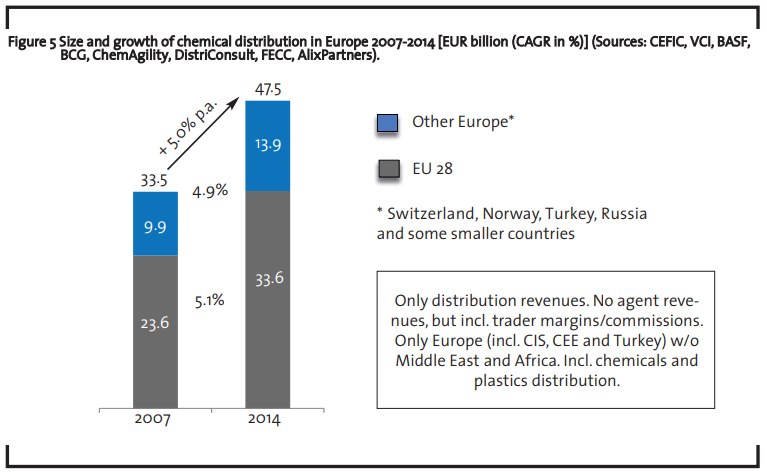

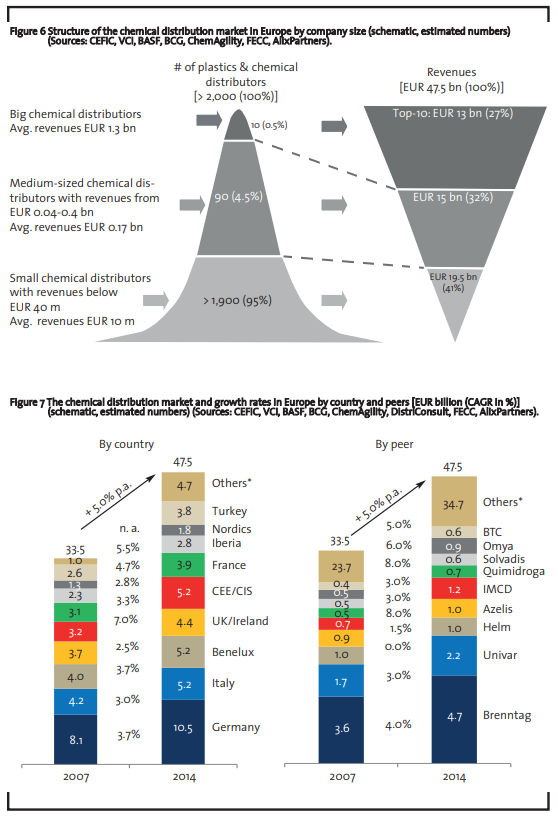

There are more than 2,000 chemical distributors active in Europe (incl. Eastern Europe, Russia and Turkey) that have generated revenues of approximately EUR 47.5 billion in 2014.

This is estimated to be more than 25% of the global chemical distribution market accounting for about EUR 185 billion. 20% of the global chemical distribution is located in China, followed by NAFTA (19%), Western Europe (18%), Latin America (10%) and Eastern Europe (7%). The European chemical distribution market of EUR 47.5 billion corresponds to 5-6% of the European consumption of chemicals and a chemical production value of approximately EUR 39.5 billion. The difference of EUR 8 billion results from the 17% margin the chemical distributors obtain. From those 17%, distributors have to cover transportation costs (3%), warehousing, refilling, bulk breaking and formulation costs (5%), SG&A (2%) and regulatory (REACH, HSE, Responsible Care, etc.) (1%) costs, resulting in 6% EBITDA profitability on average. Those numbers represent mean values. They differ significantly from commodity bulk to specialty packed chemicals and depend on the asset footprint, market-competitive position and entrepreneurial drive of the respective chemical distributor. All other things equal, profits tend to be higher in the North and West of Europe and lower in the South and East.

Unlike in Asian and emerging markets, chemical distribution is well established in Europe. More than 85,000 chemical products, which are produced in more than 25,000 European and non-European sites, are delivered via chemical distributors through more than 25,000 warehouses to more than a million customers and more than 1.5 million customer sites (see Figure 4). Thus, chemical distribution is largely about handling the supply chain complexity between chemical producers and chemical users. The core role of the distributor in the value chain is to help making the supply chain between producers and customers more effective and efficient – “connecting chemistry“ as the clear market leader Brenntag defines it.

1.4 Role of chemical distribution vis-à-vis its suppliers and customers and its impact on consolidation trends

Will this role of chemical distributors change in the future? Will suppliers or customers consolidate and in turn drive consolidation of chemical distributors?

On the supply side, chemical producers and sites in Europe consolidate and at the same time, more and more non-European producers are offering their chemicals to the European market out of non- European assets. Fine and specialty chemicals are increasingly produced in China and bulk commodities and petrochemicals in the Middle East and United States, so that the fragmentation of the chemicals industry overall remains the same and does not increase. This is very different from automotive, airlines, food, packaging, steel and many other sectors. The global market share of BASF, Dow, Sabic, Sinopec, etc. remains constant. BASF is still capturing less than 4% global market share. For every consolidation move in Europe or North America, new players are popping up in other regions of the world.

However, there is an increasing consolidation trend on a product segment level. The top 5 suppliers in selected segments control more than 75% of the global markets. This is true for many product groups, ranging from industrial gases over amines, polyolefins, adhesives to textile and leather chemicals. Formerly integrated national champions are changing to become global segment leaders. For chemical distributors that might short-term and individually be a disadvantage as they may lose distribution rights. From a long-term perspective and in structural terms, it is a benefit as the role of a chemical distributor to complement products from different segments into application increases. As mentioned above, suppliers are more spread around the globe and for consolidating suppliers in Europe, the US or Japan, there are new suppliers emerging in China and other countries. All of this makes the procurement and supply chain function of chemical distributors more important.

On the customer side, there are typically large lead customers, who consolidate and take more market shares. In segments such as “coatings”, for instance, PPG and Akzo become global players and in “food”, Kraft and Nestlé are pursuing global leadership positions, taking market shares through acquisitions. In spite of this consolidation at the top of the customer segments, the overall fragmentation in the coatings and food industry remains the same. There are still more than 3,500 coatings and 275,000 food companies in Europe, which need to be served with coatings and food ingredients. This can not only be observed in coatings and food, but also in adhesives, plastics, rubbers as well as in construction, fine and care chemicals and many other relevant application areas. So in spite of the consolidation of customers at the top, small and medium-sized customers do sustain and in many areas, new, small customers appear.

So both – from a supplier and customer perspective – there is no clear reason, why chemical distribution should or needs to further consolidate. Principal and customer trends are thus not a driver of further consolidation in chemicals distribution. Still, there is potentially a threat for medium-sized chemical distributors with revenues ranging from EUR 40 to 400 million per annum. They are the target companies for large distributors who continue to further consolidate. Smaller distributors are probably safer, if they have a specific competence in a country/region and/or a niche application. Additionally, new formats emerge such as new, local unconventional resellers who buy standard chemicals and formulate locally to fulfill customer needs better and quicker; or carve outs, whereby chemical distributors either support or are confronted with individuals taking over the supplier and customer relationship to start their own, small distribution business. In spite of the already high fragmentation of the chemical distribution industry, there are new entrepreneurs starting new chemical distribution businesses in Europe, especially in specialty chemicals distribution, where the entry barriers (capital expenditures) are lower than in bulk commodity distribution. Therefore, the disappearance of mid-sized chemical distributors, which are on the “hunting list” of large companies, is probably offset by the emergence of new start-up businesses.

1.5 Growth rates of European chemical distribution

Over the past seven years, chemical distribution in Europe has grown about 5% per annum, in spite of the economic downturn in 2009 (see Figure 5). This growth of European chemical distribution is 1.5%- points higher than the underlying consumption of chemicals in Europe. Thus, there must be additional reasons next to the structural developments at the supplier and customer markets driving growth over and above the average growth rates of chemical consumption.

1.6 Players and consolidation trends in European chemical distribution

The top 10 chemical distributors cover approximately EUR 13 billion (27%) of the European market (Figure 6). Brenntag is by far the market leader and more than double the size of the second largest actor Univar (Figure 7), at least in Europe. IMCD and Omya with their stronger specialty and solution provider portfolio have been outgrowing the market over the past years.

There are approximately 90 mid-sized chemical distributors with revenues of EUR 40-400 million (on average EUR 170 million), which account for about one third of European chemical distribution sales followed by a very large number (more than 1,900) of small and very small distributors.

As the growth rates of agents and traders have been more in line with the growth rates of chemical consumption in Europe, this means, that an increasing share of chemicals is marketed no longer directly, but indirectly via distributors.

This is less the case when referring to bulk commodity chemicals, but very strongly in specialty chemicals solutions. Especially European countries with a low and/or declining chemicals production (e.g. Greece, UK, CEE/ CIS) offer best intrinsic growth opportunities for chemical distributors. This effect is particularly strong in challenged markets and applications (e.g. leather, textile, paper, rubber chemicals), i.e. markets, where the production base in Europe is increasingly uncompetitive, where commoditization is stronger than innovation and traditional players in those markets lose market shares against backward integrated and/or emerging market competitors. Within those regions and applications, chemical distributors are able to capture over-proportionately market shares against traditional principals.

For the principals, it becomes less and less attractive to maintain a full presence with own warehouses, commercial and technical sales force, formulation and other services. Unlike their principals, chemical distributors can complement and leverage their offerings and can thus offer more cost competitive commercial and supply chain services. This is a major reason, why on average chemical distributors are able to increase their European business more than the underlying principals/producers and the overall growth of chemical consumption.

2 Fundamental differences in distributing standard molecules and providing solutions

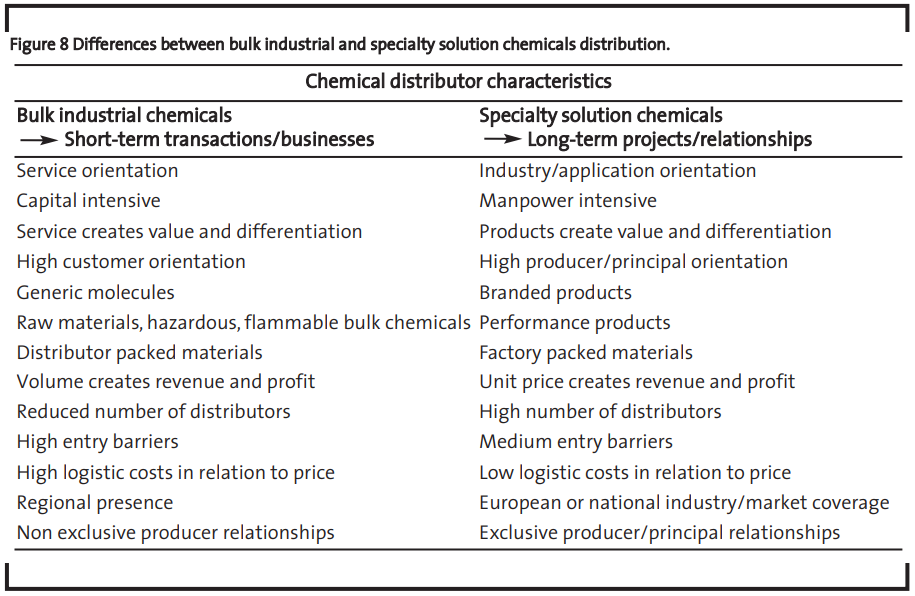

The distribution of standard molecules or bulk industrial chemicals has very different characteristics and key success factors compared to providing specialty chemical solutions (see Figure 8).

2.1 Standard molecules or bulk industrial chemicals

Bulk industrial chemicals are often standardized chemical grades, which are sourced non-exclusively by the chemical distributor. Sourcing and selling are mostly separated. Thereby, customer relationships are more important than supplier relationship. Bulk chemicals are unpacked or distributor packed and are often hazardous and liquid, requiring capital-intensive investments into tank farms and fleets. Supply chain costs are high in relation to product price and regional presence is a must. Regional/local competition is about unit price, volume, scale and minimizing handling costs. A differentiator is often a high responsiveness to deliver the right product in full on time. Business is thus more transactional and short-term oriented. As the bulk industrial chemicals distribution business shows growth below average and as maintenance as well as the need to offer an effective supply chain increase, a local/regional consolidation in the markets towards the more efficient bulk supply chain peers can be recognized.

2.2 Packed, tailor-made specialty solution chemicals

Packed, tailor made specialty solution chemicals are products that are branded by the principal and typically sourced exclusively by the chemical distributor. Exclusivity applies to both sides: The principal may not sell his products in the applications and countries agreed upon to another chemical distributor and the distributor may not source this product type from any other source. Specialty solution chemicals are mostly factory-packed performance products requiring a good understanding of the value-in-use for the respective applications.

Thus, the supplier relationships appear to be more important than the relationship to customers. Unlike with bulk chemicals, sourcing and selling are often performed by the same product manager. Warehousing and logistics are often not a key success factor of the chemical distributor and therefore outsourced to third party logistics providers. Good relationships or projects with principals as well as the product portfolio, application services and market coverage are often competitive differentiators.

Due to the tendency of principals to outsource the commercial and supply chain functions in many specialty applications to partners, the packed specialty chemicals segment grows above average. With relatively low capital entry barriers, there is a lot of competition and more and more chemical distributors try to participate in these growing markets.

The allocation of chemicals either in the group of bulk industrial or specialty solution chemicals is not always obvious. For instance, standard polymers and rubbers rather follow bulk industrial chemicals, while high performance elastomers rather exhibit specialty chemicals characteristics. Within those general product groups, there are often more specific subgroups which might belong to one or the other category. This is more than a theoretical exercise to segment chemical distribution markets.

There are about a dozen of local bulk industrial chemical distributors in the major countries or regions controlling the market, such as ECEM, Helm, Julius Hoesch, Quimasso, Solvadis, and Tillmann. There are even less plastics and rubber distributors like Albis, Lautrup, Nexeo Solutions, Resinex, and A.Schulmann.

Due to low entry barriers, there are hundreds of specialty solution chemical distributors who increasingly focus on various application areas and multiple regions and countries. Typical examples are: Azelis, Barentz, BTC (BASF), DKSH, Eigenmann & Veronelli, Grolman, HSH group, IMCD, Krahn, Lanxess Distribution, Nordmann Rassmann, Omya, Pluschem EEIG, A.E.Tiefenbacher and Unipex.

Furthermore, the different characteristics of bulk industrial and packed specialty chemicals have also led larger chemical distributors which offer both services to organizationally separate those activities, in spite of some cross-selling opportunities.

Consequently, one should think about the European chemical distribution market as (combining) three markets: 1. Bulk industrial chemicals, 2. specialty solution chemicals and 3. plastics and rubbers.

3 Drivers for size and consolidation

3.1 In specialty solution chemicals

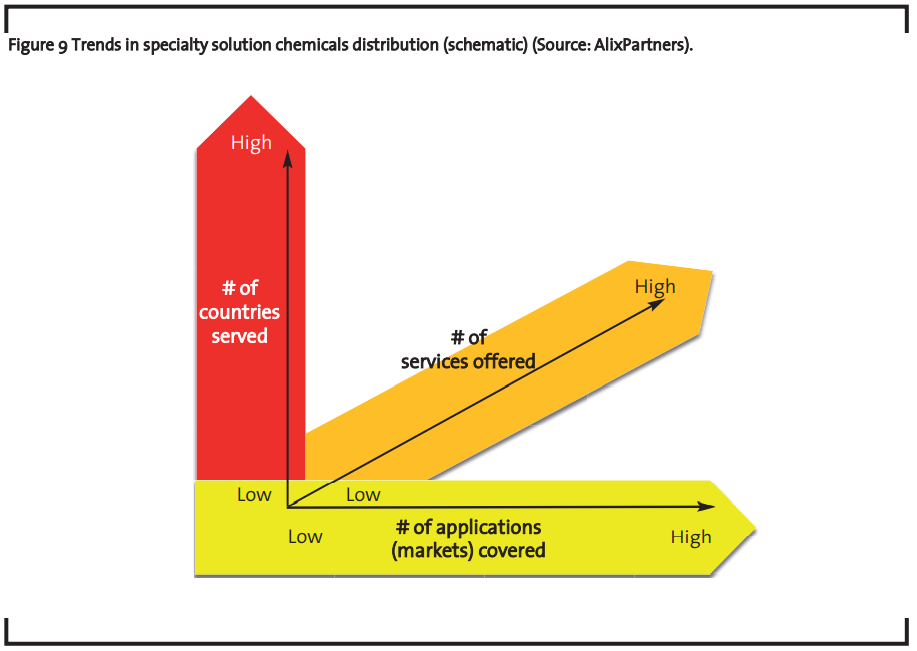

Keeping the general trends for solution providers in chemical distribution in mind, there are three drivers that ask for more size and consolidation (Figure 9). Those drivers are primarily influenced by producers/principals and chemical distributors. In the case of driver C, the demand for value adding services, customers play a role as well. The three drivers that ask for more critical mass and scale are:

- A. Serving more applications/market segment

- B. Serving more countries/regions

- C. Offering more value adding services.

A. Serving more applications/market segment

Principals increasingly want their preferred chemical distributors to understand the different application (market) needs of their differentiated (branded, formulated, or otherwise specified) chemicals and to serve those application segments (markets) differently to meet their specific needs.

Chemical distributors increasingly see the opportunity to service application (market) segments with similar service needs more effectively and efficiently than many principals by bundling complementary product groups and offering sampling, development, application and formulation services locally. This works specifically well in areas where unconventional resellers or other non-traditional market players try to capture market shares from principals/producers who can neither compete regarding cost nor regarding service any more.

From the perspective of a principal, but even more from the one of a chemical distributor, there is an increasing trend to be present in multiple applications (markets) to bundle competencies/skills and capture market synergies.

B. Serving more countries/regions

Principals are frequently asking for fewer distributors covering multiple countries in order to streamline and professionalize their distributor portfolio. Thus, principals are increasingly removing their commercial presence from C- and D-countries, asking chemical distributors to become their supply chain and commercial front end in those countries, so that they are increasingly capturing cross-border supply chain and commercial synergies. The LEL-network is an attempt of several midsized chemical distributors to act cross-border without changing the independent company status of members, similar to Star Alliance for airlines.

Both from a principal as well as chemical distributor perspective, there is a growing trend to be present in multiple countries – ideally all over Europe, but only in specialty chemicals and specialty plastics and rubber distribution.

C. Offering more value adding services

Principals increasingly view chemical distributors not as “indirect customers”, but as valuable “supply chain and commercial partners”. They want their distributors to become their partner in supply chain and warehousing excellence, including solicit-order-to-cash processes (e.g. in South-Eastern Europe), local formulation, application technology and technical service as well as new product introducer, product development and application partner.

Customers are asking for financing, vendor managed inventory, packaging handling/recycling and regulatory services. Chemical distributors increasingly see the opportunity to capture more value added services and thus secure their position in the relevant markets as well as in the value chain in order to be less easily substituted and more profitable.

From a principal but even more so from a chemical distributor perspective, there is an increasing tendency to offer more services in order to capture market opportunities, mitigate risks, differentiate and grow against peers and become more sustainable and profitable.

From the minimum size to the level of offering services, there is a threshold, especially in specialty and solution chemicals distribution of approximately EUR 80-100 million in revenues, to fulfill all of the criteria mentioned above. Many players are beyond this minimum. It is thus likely that in parallel to the (former) basis of the large top 10 chemical distributors, there will be a similar trend in the “second league” of specialty distributors. This additional class of chemical distributors is necessary and will be sustainable. The few large players cannot cover the needs of multiple exclusive suppliers and are often already too big to serve very small customers or capture the needs of niche markets.

3.2 In bulk industrial chemicals, plastics and rubbers

In bulk and commodity chemicals, there will be further consolidation as well, but for different reasons. Standardized chemicals from multiple suppliers have an increasing price transparency. Even smaller customers are able to check prices online in real time. Thus, the availability of bulk chemicals, plastics and rubbers, lead times and supply chain/transportation costs are becoming more important decision-making criteria.

In consequence, the chemical distributor who has the most effective and efficient tank farm or warehouse with an efficient 24-7-transportation service will gradually outperform its local and regional peers. As bulk handling is capital-intense, financially stronger peers and those who have re-invested regularly into the integrity of their assets will most probably emerge as front runners to become the local champions in their respective markets. Often, weaker distributors start using the more efficient asset structure of the leader as well, but ultimately they hand over the business and customers to the more effective and efficient competitor.

There are tendencies of local champions to form alliances (e.g. Penta) in order to overcome scale disadvantages, especially in purchasing and cross-border marketing and sales. This can help to reduce the performance gap between smaller and larger chemical distributors, but it is probably only the second best solution as the general reasons to invest into scale, in order to cover fixed costs for REACH/ regulatory/ safety/ sustainability, invest into new services, and to attract and retain talent, are company- specific and difficult to share with competitors. Those company-specific reasons for growing in size are the same in bulk chemicals as well as in specialty chemicals and increasingly require a minimum size even for local champions or niche players.

4 Summary: Size does matter in chemical distribution – for different reasons in specialties and commodities

In summary, there is a strong logic in chemical distribution why size matters and this will ultimately lead to further consolidation, creating a group of second tier chemical distributors, which have a minimum size and are:

- customer-oriented, local bulk chemical distributors and

- supplier-oriented, pan-European specialty solution chemicals distributors.

The large players are increasingly hindered to grow further due to supplier conflicts in specialty solution chemicals. Supplier conflicts arise when a chemical distributor wants to acquire a competitor although this competitor has exclusive distribution rights for a product group and territory which the acquiring distributor has with another principal. In bulk industrial commodity chemicals, acquisitions are sometimes prevented by cartel authorities in order to avoid high local market shares of one chemical distributor.

Thus, a group of sustainable mid-sized players who either focus on certain regions or adjacent applications/markets will become stronger and form a second tier in chemical distribution markets. They will probably be slightly less profitable than the top 10 players, but their performance and attitude (nimble, flexible, fast) towards suppliers and customers will be well in line with expectations to make them stand out and prosper sustainably.

References

Baker, J. (2015): Seeking a wider Footprint, Presentation at the 51st FECC Annual Congress, Athens, Greece, 6-8 May, 2015.

BCG (2014): Specialty Chemical distribution – Market Update.

BCG (2013): The Growing Opportunity for Chemical distribution.

Eberhard, G. (2015): M&A in Chemical distribution, ICIS Chemical Business, March 2015.

Eberhard, G. (2015): Will the future bring growth and sustainability?, Distribution & Logistics, 3, May 2015.

FECC Supplement (2014): M&A will the pace continue?, ICIS Chemical Business, May 2014.

ICIS Chemical Business (2014): ICIS Top 100 Chemical Distributors.

Jensen-Korte, U. (2015): Towards a sustainable future, Distribution & Logistics, 3, May 2015.

Prior, N. (2015): Caught in the middle, Distribution & Logistics, 3, May 2015.

Note: The market model is based on discussions with owners of ChemAgility and DistriConsult, regular attendance of FECC, VCI and CEFIC events and interviews with many managers of chemical distributors over the past years.