The digitalization of marketing and sales in the chemical B2B sector

Abstract

Marketing and sales in the B2B chemical sector are slowly making their way into the digital era. Especially in Europe the development is inhibited, as long established firms set the tone by listening to their best customer only, relying on deeply embedded routines and processes, and fostering their fear of cannibalization. In this article, the author outlines the current structures of sales processes in the chemical industry and presents a promising perspective for its digitalization by pointing out the great potential of disruptive newcomers in the form of innovative startups free from constraints of high-ranking incumbents.

1 Introduction

The ongoing digitalization does not stop at the Business-to-Business (B2B) sector. The internet is a key facilitator for entering the global market, but it also entails several challenges. While new technologies make it much easier to reach more customers or partners from all around the globe, it becomes more challenging to build stable partnerships (Samiee, 2008). The abundance of information available on the internet, makes global customers often better informed and more attentive to cost efficient offers of new players on the global market. Thus, suppliers are put under increasing price pressure and customer service and global networks become increasingly relevant (Matthyssens et al., 2008).

This article sheds light on current issues the European B2B chemical sector is facing. Digitalization and globalization are influencing the industry and presenting it with the challenge of successfully mastering the step towards the digital era. The fields of research, production and processing have benefited from new, digital technologies from the beginning, while e-solutions for the sales sector seem to develop much slower (VCI and Deloitte, 2017). The aim of this article is to draw the attention of marketers, practitioners and managers of the chemical industry to the possibilities a holistic approach to B2B e-commerce offers for the chemical sector. It will begin with a description of the current situation of the B2B sales sector in the European chemical industry and inhibitors for incumbent firms to create disruptive innovations themselves. In chapter three, the article portrays the ongoing processes of digitalization, i.e. the development of e-commerce solutions for chemicals, claiming that the mere shift to digital sales solutions is just the first step to an efficient B2B sales concept. Afterwards, the disruptive potential of innovative startups and their impact on the industry will be outlined. As an example of a young spin-off on its way to innovate the chemical B2B sales sector, the author proceeds with a portrait of the German company chembid, which is the first firm to introduce an all-in-one platform solution for the global B2B market for chemicals and related services. The concept, functions and technologies of the platform in detail as well as the advantages of such holistic approach to B2B e-commerce for the chemical industry will be explained and an overview of the main benefits the ‘chembid concept’ offers for commercial sellers as well as buyers of chemicals is given. To conclude, we will summarize the key points of our argumentation for a holistic approach to B2B e-commerce in the chemical B2B sales sector. ́

2 Marketing and sales in the European chemical industry

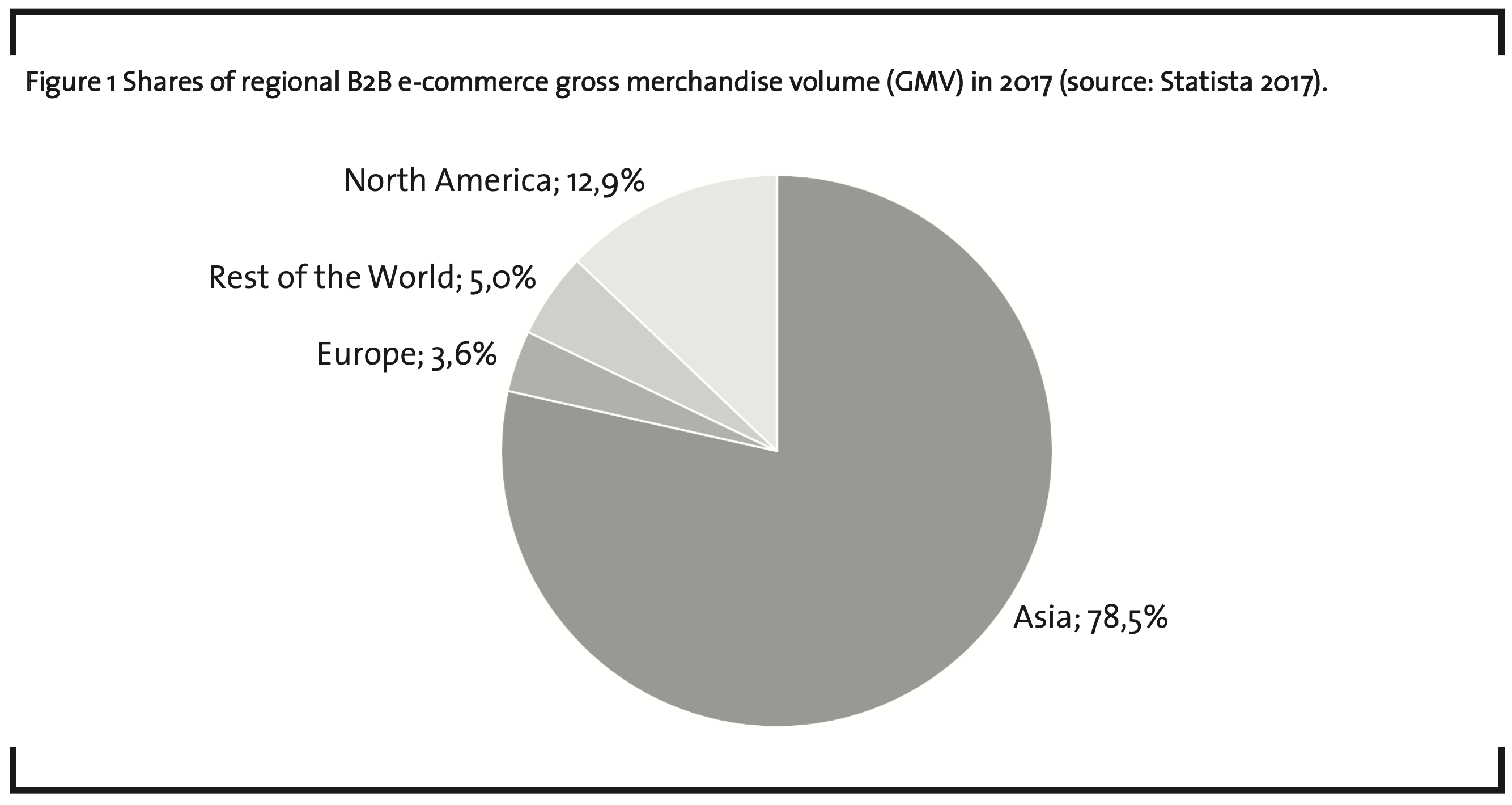

Considering the global revenues from e-commerce, i.e. the use of the internet to conduct business transactions (Terzi, 2011), the trend is obvious. Between 2013 and 2017 the sales volume was expected to increase steadily. Last year, it was predicted to reach an estimated generalized mean value of US$ 7.661 million. Especially the regional distribution of this number, displayed in figure 1, reveals a clear picture: 78.5 % are turned over in Asia, mainly China, and 12.9 % in North America, while Europe lags behind with only 3.6 % (Statista, 2017). With the EU being the second biggest market in the world according to its gross domestic product (GDP) (International Monetary Fund, 2018), it is quite surprising that the role Europe plays in B2B sales is almost neglectable. It seems like Europe is on the verge of missing the trend of the early 21st century, while e-commerce is changing the working processes of the digitalized sector in the rest of the world (Terzi, 2011).

Taking a specific look at the chemical industry this picture does not change much. Being part of the ‘old economy’, changes do happen slower than in other industries and focus on other areas, respectively. Although, the number of investments is increasing in general (CEFIC, 2017), the chemical industry in Europe seems to lag one step behind internationally when it comes to marketing and sales (VCI and Deloitte, 2017). The industry still relies on old principles, i.e. business is generally conducted on a person-to-person basis. Suppliers or customers are acquired through extensive searches, contacted via phone and asked for quotes. Often, several phone calls and meetings are necessary to finally come to an agreement. The other way around works similarly: suppliers send their sales personnel to potential buyers to promote their goods and offers. Despite this extensive and time-consuming effort for both sides, the numbers of quotes buyers end up with as well as the conclusions of contracts the sales persons achieve often remain rather limited.

Once a contract is closed, it often results in a long-lasting cooperation, as the finding process is so complex as well as time-consuming. One could argue that long-lasting partnerships ensure stable businesses and should thus be beneficial for both sides. And, indeed, for the decades when telephone and fax were the most efficient communication channels, this is true. In times of globalization and interconnectedness, however, the benefits of personally knowing your supplier or customer cannot outweigh the advantages of modern technologies. Compared to the manifold possibilities opened up by digital technologies, the traditional processes appear rather slow, expensive and inefficient – not to say outdated. Also, suppliers are often using the opacity of the market for their benefit. The sales person visiting potential customers makes individual offers for each one, considering the size of the company, the insights the customer has on the pricing of certain products and so forth. The results are extensive negotiations about the conditions and prices.

3 Increasing number of marketplaces and web shops for chemicals

Looking at the number of marketplaces and web shops for chemicals on a global scale, there appears to be an abundance. So far, Europe only hosts a few promising but insignificant ones. Not all of the global marketplaces are specialized in chemicals only and they vary considerably in terms of their size, range and amount of offers. In order to get an overview of the various offers from different suppliers, commercial buyers of chemicals have to search, visit and compare multiple websites. Although, this process does save some time compared to the acquisition by phone, it is basically just a direct shift from the interaction on a person-to-person basis to a digital one. The information on products and offers is not spread personally but online, while buyers still have to search and organize it themselves. This might be somewhat more efficient, but it is still not close to what one would expect from digital services. The more marketplaces and web shops for laboratory and/or industrial supplies appear, the harder it gets to find the best offer. Hence, the development of the B2B e-commerce in the chemical sector is the direct transformation of the established principles and processes to digital platforms and communication channels. Compared to other sectors and even our private lives (e.g. travel websites, online shopping), it does not seem to be the optimal solution.

4 The European chemical industry is on the verge of being disrupted

While it was possible to rely on what worked for decades, the European chemical industry, which still is the third biggest in the world (CEFIC, 2017), now faces the risk of losing the lucrative sales side. What led those companies to be at the top once, ironically, is the very same thing enhancing the risk of being disrupted by newcomers now (Christensen, 1997). Over the past decades, many upcoming companies managed to outsmart incumbent players in other industries by making use of technological developments and/or radically rethinking business models (Markides, 2006; Yu and Hang, 2010). And first signs of a similar development for the chemical industry are already on the horizon when shift- ing the view to Asia or considering young and small players in Europe. Relative newcomers put forward innovation, introducing “a different set of features and performance attributes” (Govindarajan and Kopalle, 2006, p. 190). For the incumbent players those new features and attributes are hard to embrace for three main reasons:

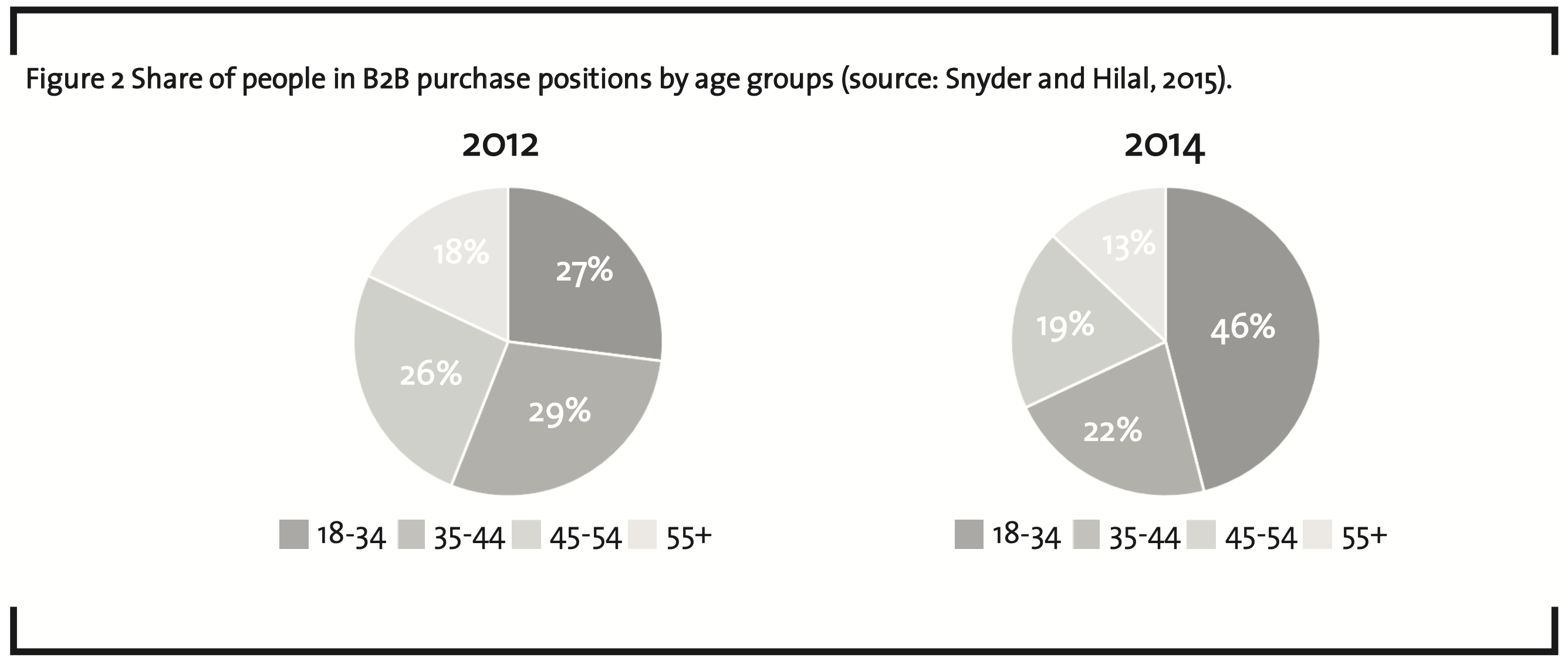

1) Listening to the best customers: Companies are led in order to pursue sustaining the current successful state instead of aiming for disruptive innovation (Daneels, 2004). In the past main customers of chemical companies did not request digital solutions on the marketing and sales side. Thus, the companies were caught by them and shifted their activities to the customers promising the highest profit (Slater and Mohr, 2006). However, the (still) best customers become older eventually, and a young and technology-affine generation is constantly growing into positions, where they have the responsibility and the power to decide what to buy from whom (Snyder and Hilal, 2015). This young generation has been using e-commerce platforms for years in their private life and has no reason to make an exception for their business life. This generation of so-called millennials (aged between 18 and 34) is constantly striving for modernization to improve their business’ efficiency, i.e. they want to achieve more in a shorter period of time compared to their predecessors. In business life, efficiency is considered the key for success and is rated higher than personal relationships with sub-contractors or suppliers. Young managers saw and experienced the rapid development of digital technologies during the past years and developed alongside it. More and more companies are embracing the possibilities the internet offers for their activities (Terzi, 2011). It has become normal to search for solutions to any problem online, as it is direct, fast and efficient. As shown in figure 2, the number of millennials in purchase positions has increased by 70 % from 2012 to 2014 (Snyder and Hilal, 2015) and there is no reason to assume that this trend has changed during the past years.

2) Deeply embedded routines and processes: Long-established principles are not suited for pursuing disruptive innovation and need to be adapted (Macher and Richman, 2004; Nelson and Winter, 1982). In this case, routines and processes, especially, refer to the ones applied for the evaluation of new initiatives (Assink, 2006). Disruptive projects often do not fulfill the company’s expectations in terms of market size or return and are much more uncertain at first. If disruptive projects are assessed by the same criteria on a routinized basis, they might get sorted out prematurely (Christensen, 1997, 2006). Routines are capable of securing efficiency in a stable environment but show weaknesses during times of change due to inflexibility (Nelson and Winter, 1982). Therefore, relevant routines and deeply embedded processes can become obstacles decreasing the manager’s ability in responding to disruptive innovations (Adner and Snow, 2010; Henderson, 2006). And if an initiative is not allocated with sufficient resources, it is prone to fail (Bergek et al., 2013). A study by KPMG (2016), conducted in Germany, reveals that in many companies, the staff is highly skeptical about new technologies. Afraid of investing in the wrong technologies or their employees not accepting the potential innovation, executives barely include budget for digital transformation of the company in their business plans. Without a budget, however, the number of qualified personnel able to evaluate the potential of new technologies and the benefits for the company remains low. Then again, the lack of adequately skilled employees to initiate and accelerate the digital progress of the company causes the skepticism about new technologies (KPMG, 2016).

3) Fear of cannibalization: This fear describes the effect of a firm’s product directly diminishing the returns of another firm’s product (Schilling, 2010). The willingness to execute projects possibly entail- ing this effect is described as the “extent to which a firm is prepared to reduce the actual or potential value of its investments” (Chandy and Tellis, 1998, p. 475). Accordingly, the introduction of new business models will be delayed, if company leaders are not prepared to reduce the value of their current business model and the fear of cannibalizing their own sales, assets or organizational routines prevails. Just like cost factors, this leads to a slow implementation of new business models. This was observed in the European chemical sector for a long time as the incumbent players rarely came up with own initiatives or undermined initiatives of other players successfully. By creating or supporting business models reducing the opacity of the market a beneficial aspect for the suppliers would falter. The organizational structures and the personnel are tuned to work in the old opaque model. Turning to a transparent model would render some investments obsolete by cannibalizing own sales.

Due to those inhibitors only 30 % of the medium-sized companies in Germany have yet implemented digital business models, according to survey studies by VCI and Deloitte (2017). The remaining 70 % of the participants indicated that they only expect minor changes to their business models due to the ongoing digital transformation. Although, new distribution channels are often mentioned as important factors for improvement. In a recent study, Euroforum asked 50 experts from the chemical sector about the digital transformation of chemical companies. The survey revealed that most of the participants see the most important field for improvements by digitalization in the supply chain management not in new business models (Euroforum, 2017). Accordingly, digital distribution models are implemented hesitantly. In addition to the general skepticism, the additional expenses for the creation and maintenance of a web shop (which also requires an online marketing strategy to effectively increase the range of the company) are the main reasons for the hesitation. Many companies lack the personnel resources for such projects. However, in order to comply with the expectations of potential customers, online presence has already become much more than just an extra service. It is a necessity for professional businesses. They can answer customer inquiries in real-time, adapt new online offers, and analyze traffic and range. This way, businesses can make use of the digitalization to check their sales models, achieve predictable results, and generate long-lasting customer relationships, despite the growing number of competitors. Online marketplaces and web shops become increasingly relevant for many sectors (Euroforum, 2017).

5 An agile startup without the incumbent’s constraints presents an all-in-one-platform solution

For years, the chemical industry mainly consisted of established players, who, for a long time, cemented their position on the market and did not seem to leave room for smaller startups. With the upheaval into a new, digital era, this is due to change. An increasing number of startups strive to innovate the chemical sector and help leading it into the times of ‘marketing and sales 4.0’. This also applies for the first global metasearch engine for chemicals and related services. A startup company from northern Germany is the first to introduce such a concept to the sector.

The founders of chembid know the problems they want to tackle first-hand. Dealing with the opaque and complex market situation every day, the idea for a more efficient solution suited for the new digital era arose. In 2016 the company was officially founded. It took one and a half years to design and develop the metasearch engine and platform of the same name, which went online in October 2017. The idea and the aim is to collect, organize, and bundle commercial and technical information on chemicals from all over the world into one website, to make it easily accessible and guarantee simple and fast processing. In contrast to the incum- bents chembid is not limited by its past. Hence, the company is not constrained by static routines or a fear of cannibalization and the team can strive to develop a disruptive innovation for the future customers (Weiblen and Chesborough, 2015). Following this target would have been hard to accomplish staying along the beaten track.

5.1 The first metasearch engine for chemicals

The backbone of the platform is a metasearch engine. And although the technology itself is not new, it is new to the chemical industry and was adjusted to fit the demands of it. The platform can be found and visited like any other website on the internet. Traffic is generated from generalist online search engines, social media networks or other websites (e.g. via online marketing campaigns), etc. Being a highly specialized search engine itself, it can schematically be placed one level above the respective marketplaces for chemicals and the suppliers’ individual web shops, if available. The data is gathered in two distinct ways. On the one hand the relevant websites are searched for suitable offers by the intelligent search engine. So-called web crawlers are used to automatically search for product information from thousands of offers worldwide. On the other hand the platform uses application programming interfaces (API), which allow for the simple linking with other databases. Via those APIs, providers of marketplaces or web shops can easily, i.e. manually in a few steps or even automatically, transfer their offers onto the meta platform. The information is then made available in a single overview and can be narrowed down with chemical-specific filter functions.

On this meta-level of the search engine, the platform is not a direct competitor for online mar- ketplaces for chemicals, but simply bundles the information from various competitive marketplaces on one website. Partnerships with marketplaces and suppliers with their own web shops are even desired, as it ensures the accuracy of the information and offers. Being listed on the platform does not take away traffic, as all offers are linked to the original website, where purchases can be carried out as usual. However, the platform does offer its own marketplace for further opportunities as well. The search engine does not prioritize offers from the inbuilt marketplace, though, as this would disrupt its main purpose of creating more market transparency.

In addition to the product database a supplier database is included as well and can be browsed, too. The suppliers are linked to their respective chemicals and related services. This data is used to create a comprehensive worldwide data-base of supplier profiles and their products and online offers. Besides generating a value for itself as being the first index to link suppliers with their actual online offers, it is a highly important building block for the sourcing tool, which is another innovative feature of the platform.

5.2 Sourcing tool – reversing the market

The online sourcing tool for chemicals and related services can help both vendors and buyers to increase their efficiency. Buyers can place their demands, wait for the responses of suppliers and compare the quotes in a standardized overview to choose the best offer. Vendors on the other hand can save on sales force, who would usually contact every potential buyer. They can send quotes fitted to the buyer’s request. This is somewhat reversing the market situation, but it also helps create a more balanced distribution of power. So far, so old. The unique point is derived from the combination of the gathered supplier and product data and an algorithm finding suitable suppliers for the product in question. The algorithm will check for suppliers fulfilling the specific criteria of the request. For example, typical amounts of the suppliers are compared to the amount requested. Accomplishing a more and more accurate algorithm will be a big step towards connecting buyers with potentially interested sellers only fully automatically.

5.3 Market statistics – big data, small effort

Since the process of providing such services includes the collection of a vast amount of data, it is used to create useful market statistics as an extra service for the users. While it was a time-consuming process to get reliable price information due to the lack of market transparency in the past, the data gathered by the web crawlers allow for the reliable computation of past prices, average prices or future trends. Based on this data, the statistical tool offers the possibility to create clear tables and graphs according to the users’ desired criteria. This automatically delivers a representative result from a big pool of suppliers rather than from a few who need to be called manually. The possibility to handle big data for the chemical B2B sales sector is made easily accessible for the users.

5.4 Artificial intelligence – virtual agent

In order to guarantee the best search results possible, Artificial Intelligence (AI) plays a significant role in the form of machine learning algorithms monitoring the users’ search behavior and adapting the search results according to their needs and preferences. Due to the abundance of offers, this saves users additional time, as it helps to find products for certain cases. At first, this feature can help rudimentary, but over time, with more and more data gathered, the AI will be able to advise in more advanced cases and serve as a virtual agent. As one of the main goals of the platform is to increase efficiency, the usage of AI/machine learning is vital to accelerate the processes while still providing qualitative results.

5.5 Advantages for buyers and suppliers

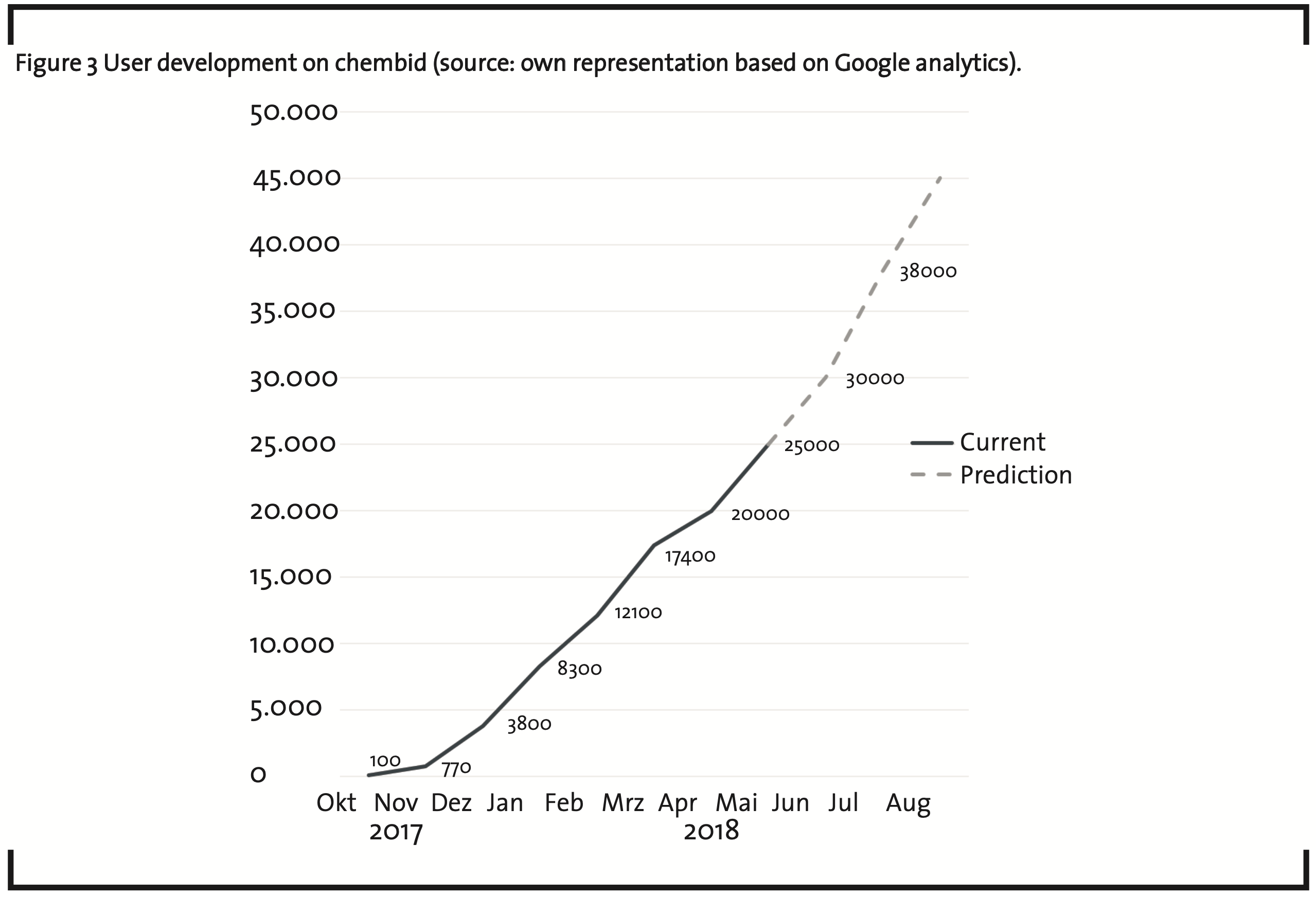

As a result of the ongoing digitalization and globalization in all sectors, vendors are put under increasing pressure (Matthyssens et al., 2008). They need to cope with a growing number of competitors from all around the globe as well as the high expectations of their customers. To stay competitive, they need to strive for more coordination and collaboration among supply chain partners to increase efficiencies in supply chain management (Terzi, 2011). An online platform solution, offering new distribution channels for sellers, can help firms to easily expand their range without requiring additional resources for e-commerce and online marketing (provided they chose a widely renowned marketplace). The unique all-in-one solution from Germany, for instance, had approx. 25,000 unique visitors in May 2018, while the projected number of users for August 2018 is estimated to be 45,000. Due to the usage of cloud computing the model is easily scalable and there is no hard limit to those numbers. The platform can thus be a useful addition to existing marketing and sales solutions. New leads are automatically acquired, so that marketing resources and sales force can be reduced. Additionally, the marketplace can serve as an alternative to an individual web shop or as an addition to it.

After creating a user account and being verified by the provider, product or service offers can either manually or automatically be uploaded onto the inbuilt marketplace. Big amounts of data, e.g. a supplier’s whole range of products, can be uploaded in bulks. All offers can be found on the metasearch engine. Offers from the inbuilt marketplace are highlighted, for better find ability of verified vendors. The number of current available offers, i.e. 1.8 million, and the 60,000 represented suppliers from more than 160 different countries, prove the platform’s potential.

The advantages of a global metasearch engine for commercial buyers of chemicals are quite straightforward as well: Buyers are usually the ones actively seeking for information and the best offer. Upon entering the name or CAS number of a product into the search bar, they will receive a comprehensive list of suitable offers from online marketplaces and websites worldwide. Various filtering options, e.g. place, price, quality and measurement unit, allow for further specification of the search request. Results can be sorted by price or relevance. Clicking on the search result will directly lead to the supplier’s website or the marketplace the offer can be found on.

6 Summary and conclusion

- Digitalization reaches out to the B2B marketing and sales sector and makes no exception for the chemical industry. European chemical companies, though, do not pursue sufficient digital initiatives. By going on conducting business in the old ways and without preparing for what is to come, other players – especially from Asia – might pace them out.

- Asian companies already developed an abundance of marketplaces and offer chemical products online. The growing number of those marketplaces leads to a mere transformation of the old, time-consuming and inefficient processes to digital channels.

- Three main factors are limiting incumbent European players in starting their own initiatives seriously: Listening to the best customers, deeply embedded routines and processes and fear of cannibalization. Hence, only 30% have implemented digital business models so far.

- As a young startup, chembid is not limited by the incumbent’s constraints and is, thus, a good example for a potentially disrupting innovation for the B2B sales sector of the chemical industry. The company developed the first metasearch engine for chemicals and related services. Its main purpose is to create full market transparency by organizing and making accessible chemical offers from the web.

- Besides other advantages this approach serves suppliers with an increased range and buyers with more and better market information.

- Among other features the holistic ‘chembid concept’ also includes market statistics based on big data techniques and a sourcing tool run by AI. By combining modern technologies, it is aimed to co-create the future of chemical businesses regarding marketing and sales.

References

Adner, R., Snow, D. (2010): Bold Retreat, Harvard Business Review, 88 (3), pp. 76–81.

Assink, M. (2006): Inhibitors of disruptive innovation capability: A conceptual model, European Journal of Innovation Management, 9 (2), pp. 215–233.

Bergek, A., Berggren, C., Magnusson, T., Hobday, M. (2013): Technological dis-continuities and the challenge for incumbent firms: Destruction, disruption or creative accumulation?, Research Policy, 42 (6-7), pp. 1210–1224.

CEFIC (2017): Cefic – Facts and Figures 2017, available at http://fr.zone-secure.net/13451/451623/ #page=1, accessed 24 May 2018.

Chandy, R. K., Tellis, G. J. (1998): Organizing for Radical Product Innovation: The Overlooked Role of Willingness to Cannibalize, Journal of Marketing Research, 35 (4), pp. 474.

Christensen, C. M. (1997): The innovator’s dilemma: When new technologies cause great firms to fail. The management of innovation and change series, 2nd ed., Harvard Business School Press, Boston, Mass.

Christensen, C. M. (2006): The Ongoing Process of Building a Theory of Disruption, Journal of Product Innovation Management, 23 (1), pp. 39–55.

Danneels, E. (2004): Disruptive Technology Reconsidered: A Critique and Research Agenda, Journal of Product Innovation Management, 21 (4), pp. 246–258.

Euroforum, (2017): Industrie 4.0, Index 2018 – Der Wegweiser in die digitale Zukunft, available at: http://www.euroforum.ch/strategietagung/download-digitales-magazin-industrie-4-0-index-2018-der-wegweiser-in-die-digitale-zukunft-pc/accessed 20 May 2018.

Govindarajan, V., Kopalle, P. K. (2006): Disruptiveness of innovations: Measurement and an assessment of reliability and validity, Strategic Management Journal, 27 (2), pp. 189–199.

Henderson, R. (2006): The Innovator’s Dilemma asaProblemofOrganizationalCompetence,Journal of Product Innovation Management, 23 (1), pp. 5–11.

International Monetary Fund (2018): World Economic Outlook Database, available at http://www.imf.org/external/pubs/ft/weo/2018/01/weodata/weorept.aspx, accessed 24 May 2018.

KPMG (2016): Zeit zum Aufblühen – Digitalen Transformation der chemischen Industrie, available at: https://home.kpmg.com/de/de/home/the-men/2016/11/digitale-transformation-der-chemischen-industrie.html accessed 24 May 2018.

Macher, J. T., Richman, B. D. (2004): Organisational responses to Discontinuous Innovation: A Case Study Approach, International Journal of Innovation Management, 8 (1), pp. 87–114.

Matthyssens, P., Kirca, A., & Pace, S. (2008): Business‐to‐business marketing and globalization: two of a kind, International Marketing Review, 25(5), pp. 481-486.

Markides, C. (2006): Disruptive Innovation: In Need of Better Theory, Journal of Product Innovation Management, 23 (1), p. 19–25.

Nelson, R. R., Winter, S. G. (1982): An evolutionary theory of economic change. Cambridge, Mass.: Belknap Press of Harvard University Press.

Samiee, S. (2008): “Global marketing effectiveness via alliances and electronic commerce in business-to-business markets”, Industrial Marketing Management, 37 (1), pp. 3-8.

Slater, S. F., Mohr, J. J. (2006): Successful Development and Commercialization of Technological Innovation: Insights Based on Strategy Type, Journal of Product Innovation Management, 23 (1), pp. 26–33.

Snyder and Hilal (2015): The Changing Face of B2B Marketing, available at https://www.thinkwith-google.com/consumer-insights/the-changing-face-b2b-marketing/, accessed 24 May 2018.

Statista (2017): B2B e-Commerce 2017, available athttps://www.statista.com/study/44442/statista-report-b2b-e-commerce/, accessed 24 May 2018.

Terzi, N. (2011): The impact of e-commerce on international trade and employment, Procedia – Social and Behavioral Sciences, 24 , pp. 745-753.

VCI and Deloitte (2017): Chemie 4.0 – Wachstum durch Innovation in einer Welt im Umbruch, available at https://www.vci.de/vci/downloads- vci/publikation/vci-deloitte-studie-chemie-4-punkt-0-langfassung.pdf, accessed 24 May 2018.

Weiblen,T.,andChesbrough,H.W.(2015):Engaging with startups to enhance corporate innovation, California Management Review, 57 (2), pp. 66-90.

Yu, D., Hang, C. C. (2010): A Reflective Review of Disruptive Innovation Theory, International Journal of Management Reviews, 12 (4), pp. 435–452.