The Global Business of Chemistry: Prospects and Challenges

Abstract: The global business of chemistry has faced numerous challenges in recent years. This article addresses the near-term business environment in which the industry will operate as well as the implications for the global business of chemistry during 2006 and 2007.

Introduction

The business of chemistry is a $2.24 trillion enterprize, an enabling industry that is essential to our everyday lives, making possible many innovations and benefits for society. When the science of chemistry is applied, it helps make the lives of humankind world safer, healthier and more productive.

The industry faces considerable challenges (and opportunities) in the opening years of the 21st century. Included are rising energy prices, geo- political shocks, and globalization. The prime aim of this article is to present the short-term

outlook for the global business of chemistry as well as address some longer-term issues. It is oriented toward the decision-maker in business of chemistry or others interested in the interaction between changes in the global economy and industry dynamics.

The article is organized into three sections. A first section deals with the business environment for the global economy, with a particular focus on industrial activity, the prime end-use market for chemicals. The expected outlook is reviewed as are the potential risks. A second section deals with the the linkage between overall industrial activity and the business of chemistry and proceeds to the implications of rising industrial output for the global business of chemistry’s outlook during the next two years, with a discussion of national/regional differences as well as opportunities by segment. In a third section, the prospects for the global business of chemistry during the 2005-2015 time frame are addressed as is a discussion of the effects on demographic change on longer-term demand for chemicals. A final section deals with sources of the data and methodologies employed.

Business Environment

Led by continued strong performance in the United States and China, the global economy recorded robust, albeit slower, growth in the first half of 2005. After averaging 5.1% in 20041, world economic growth (on a purchasing power basis) as presented in Table 1 will moderate to 4.2% in 2005 and is expected to further moderate to 4.0% in 2006 and 2007. These growth rates are in line with the historic averages reflecting a robust, healthy economic environment. This optimistic view of global prospects assumes that no major economic or political shocks that would alter the course of growth will occur. There are, however, a number of possible risks to the world economy.

A significant escalation in oil prices would pose a threat to world growth. Although the global economy has become significantly less dependent on oil since the 1970s, higher oil and natural gas prices continue to act as a downside risk to economic growth and as an upside risk to inflation. Inflationary pressures have risen. If upward pressure on core inflation measures intensifies, this will result in higher interest rates, which in turn could eventually engender the next downturn.

Large imbalances remain in the world economy, particularly in relation to the record US current account deficit, which increasingly strains the global financial system. Consequently, another significant drop in the dollar against other major currencies is possible. Weakness in the dollar could pose a threat by undermining export-driven economic growth in Europe and Japan. Threats aside, prospects remain strong for world trade into 2007.

Another source of global risk arises from the unsure economic recovery in Western Europe. Although there have been some signs of improvement, the recoveries in France, Germany and Italy in particular are still fragile and largely externally driven, making them especially vulnerable to any set-backs in the global economy.

Global growth could also be derailed by fresh geopolitical shocks. Further terrorist attacks in the major Western economies could depress confidence. There is also a specific concern relating to a possible global pandemic if Asian ‘avian flu’ spreads more widely within the human population. The impact of such risks is impossible to quantify with any precision at this stage, but in a worst case scenario it could be devastating in both economic and human terms.

There are also some positive factors to bear in mind. First, despite headwinds from high energy costs, the US economy remains relatively strong, and the latest indicators are generally positive. The other major economic engine, China, still has significant upward momentum. In addition, there are signs that the continental economies of Western Europe and the Japanese economy are improving.

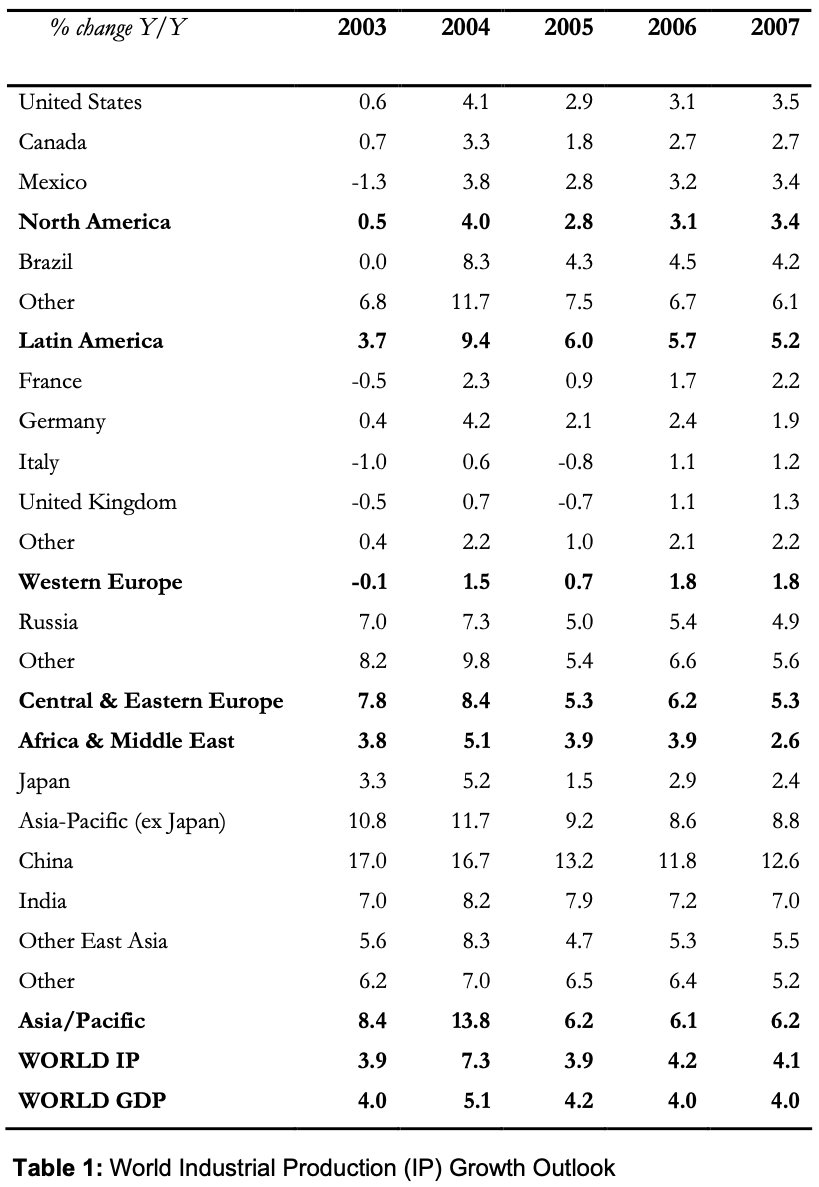

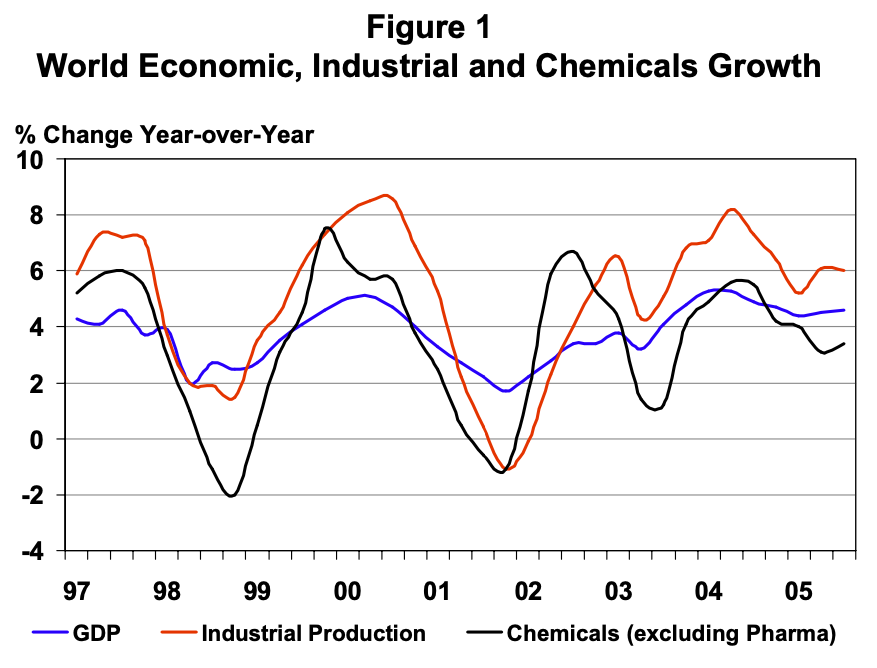

Industrial production is a more meaningful indicator than economic growth. On average, the industrial sectors purchase $43 worth of chemistry for every $1,000 worth of output (or revenues). In contrast, the services sectors purchase only $11 for every $1,000 worth of output. Moreover, the services sectors are more likely to purchase pharmaceuticals (for health care) and consumer products than basic and specialty chemicals, which are dominated by industrial uses. During 1st quarter 2005, year-over-year (Y/Y) growth in global industrial production slowed to 5.2%, down from a peak 8.2% Y/Y gain in 2nd quarter 2004. This reflected the soft patch in global manufacturing as high energy prices and a rush to trim inventories slowed manufacturing activity worldwide. The soft patch was rather short, with 2nd quarter Y/Y growth improving to 6.1%. The hurricanes during August and September, however, adversely affected US output, hampering 3rd quarter global activity. These patterns are illustrated in Figure 1.

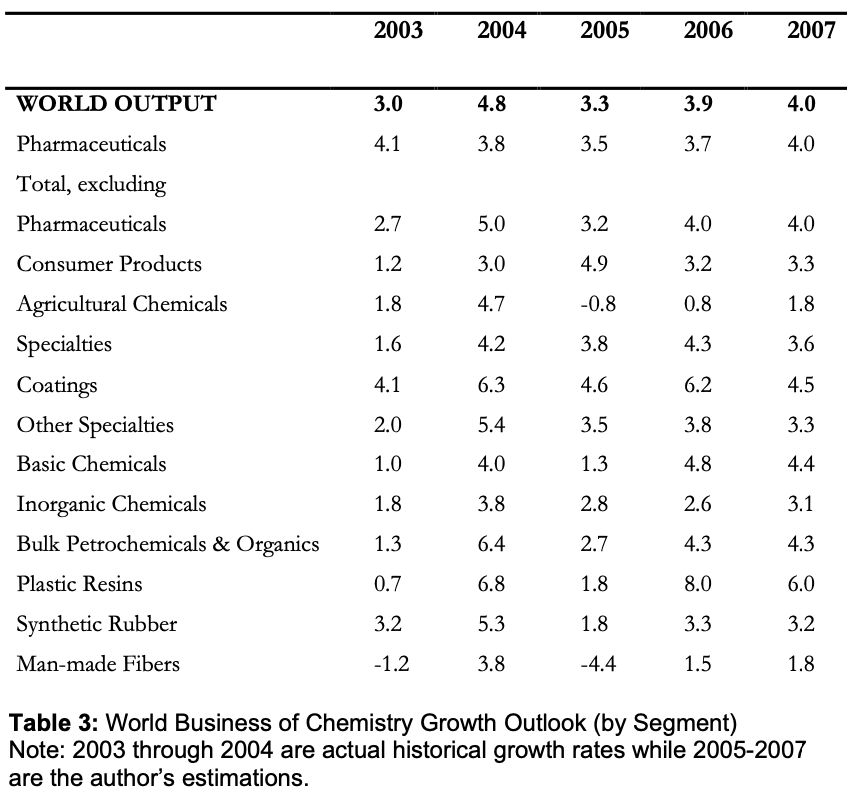

Note: 2003 through 2004 are actual historical growth rates while 2005-2007 are the author’s estimations.

Global industrial activity appears to be recovering, which will aid final demand, manufacturing, and ultimately demand for chemistry. As Table 1 indicates, expectations are for a 3.9% gain in global industrial production in 2005, accelerating to 4.2% in 2006. This will still trail the gain in 2004, which likely represented the peak in growth. As expected, the strongest growth is occurring in China and other East Asian economies.

Global Chemical Industry Outlook

As seen in Figure 1, the global business of chemistry clearly parallels trends in broader industry. During 2005, the pattern clearly reflects the global soft-patch in manufacturing and summer rebound from the inventory-led correction of the 1st half. The data for the summer months provide signs that this ended and that growth returned. The negative impact of Hurricane Katrina on US production weighed on chemical industry activity in North America and the world. Outside North America, improvement has generally been broad-based and is particularly strong in Africa & the Middle East and in the Asia-Pacific region.

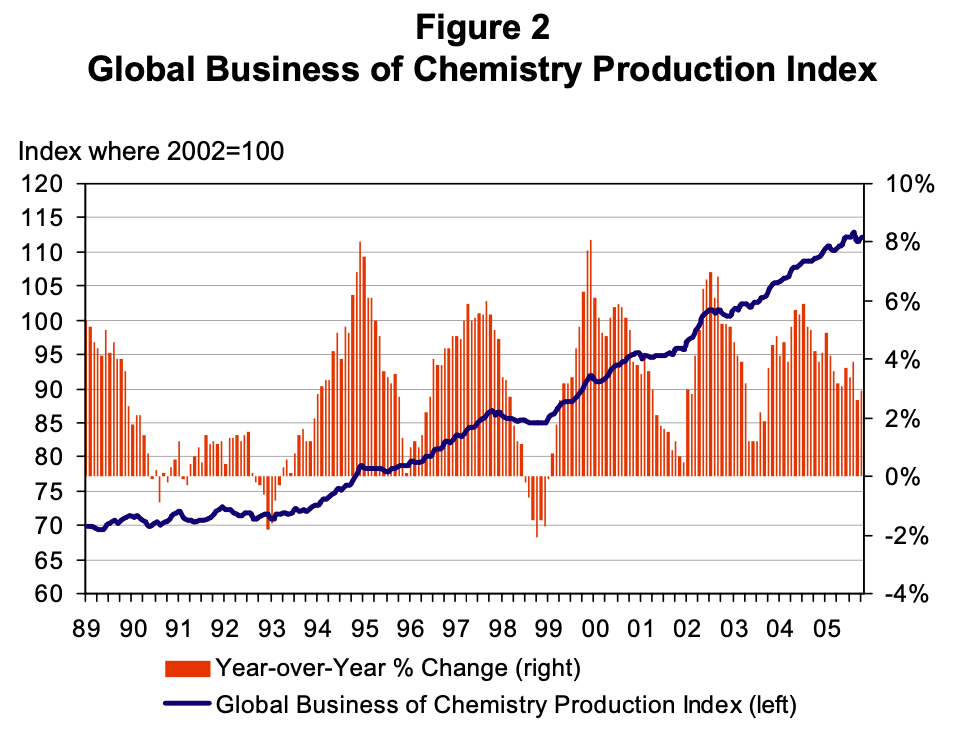

On a Y/Y basis, global chemical industry production was up 3.3% in the 3rd quarter, down from the peak Y/Y comparison of 5.9% last July. As Figure 2 illustrates, the past year was characterized by moderating Y/Y comparisons but also reflects the more mature phase of the cycle as well as the effects — a soft-patch — of high energy prices and the global inventory correction working their way through the global economy. Nonetheless, the global industry expects improved business conditions in 2006. Indeed, there have been a number of encouraging signals.

The industry still faces some economic headwinds. The hurricanes in the United States negatively affected output for some producers but may have presented opportunities for other producing nations. The major risk to the global economy and the business of chemistry at this point in the chemistry cycle is high oil prices, the result of sustained global demand as well as supply-driven gains recently in wake of Hurricane Katrina. In North America, this is further complicated by high and volatile natural gas prices where the effects of Katrina and Rita were equivalent to a classic supply shock.

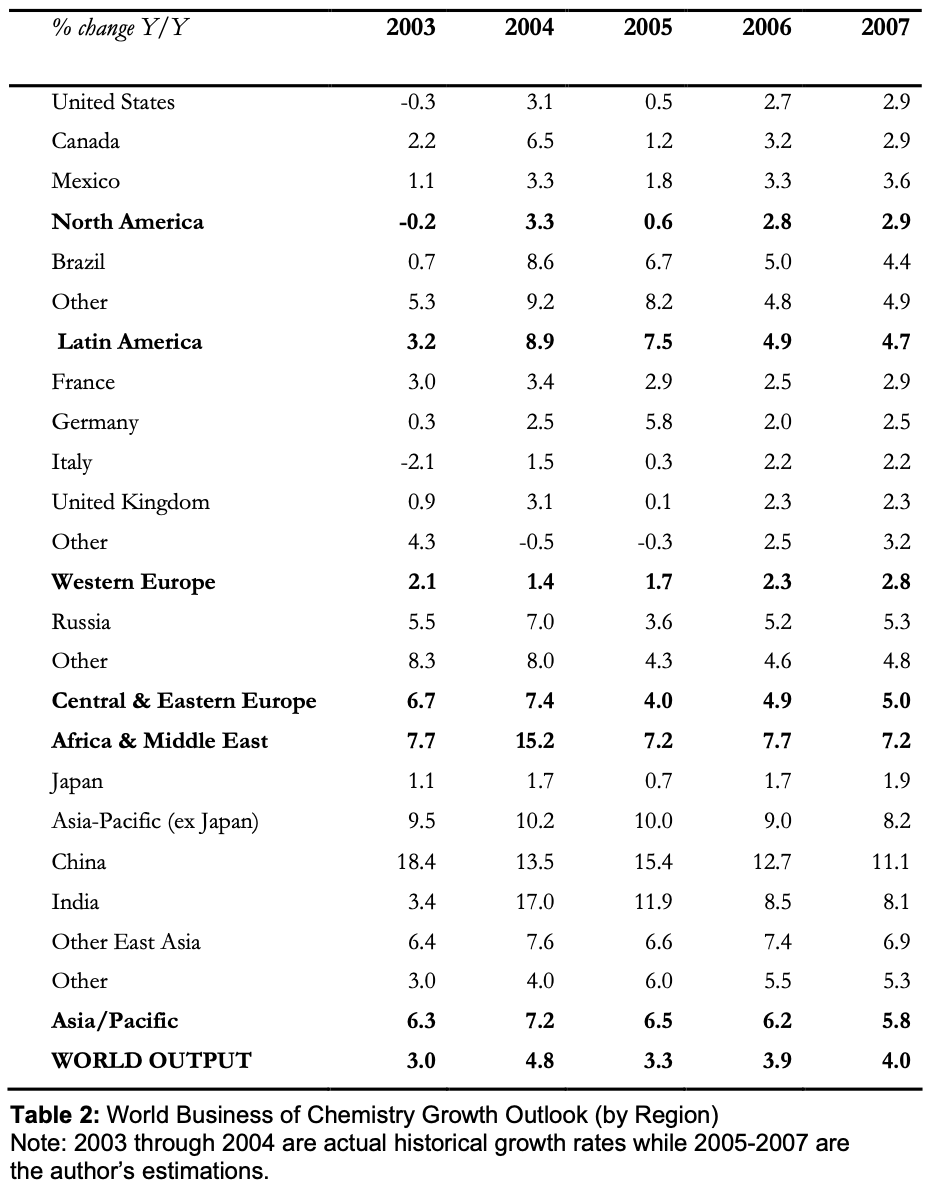

In parallel with renewed demand among industrial customers, the global chemical industry will continue to grow from its current base. As shown in Table 2, as global industrial production recovers it will pull worldwide chemical industry activity with it, with volumes improving from 3.3% in 2005 to 3.9% in 2006. During 2007, gains will improve slightly (to 4.0%) but will still be slower than the 2004 gain, which likely represents the growth peak. As would be expected, the largest gains are anticipated in China and elsewhere in the Asia-Pacific region (excluding Japan) as well as in Africa & the Middle East. Better prospects are expected in Western Europe during 2006 and activity is expected to improve in North America. Table 2 presents the global outlook for the business of chemistry on a regional basis, including several of the major economies.

The various segments of the chemical industry have been affected to different degrees by the global soft-patch in manufacturing as well as the slowing of the world economy. This year presented deterioration of petrochemical and downstream derivatives activity. Downstream customer and producer inventory de-stocking played a large role but the effects of the hurricanes on US activity has taken their toll on global output as well. Table 3 presents the global outlook for the business of chemistry on a segment basis. It appears that improving consumer and business confidence and sustained global economic growth along with rebounding global industrial output will aid most basic and specialty chemical segments. The recovery from the hurricanes will lift global

growth prospects for plasti resins and for bulk petrochemicals and organics. Improving light vehicle production and construction activity will aid the global coatings business.

Long-Term Trends in Chemistry

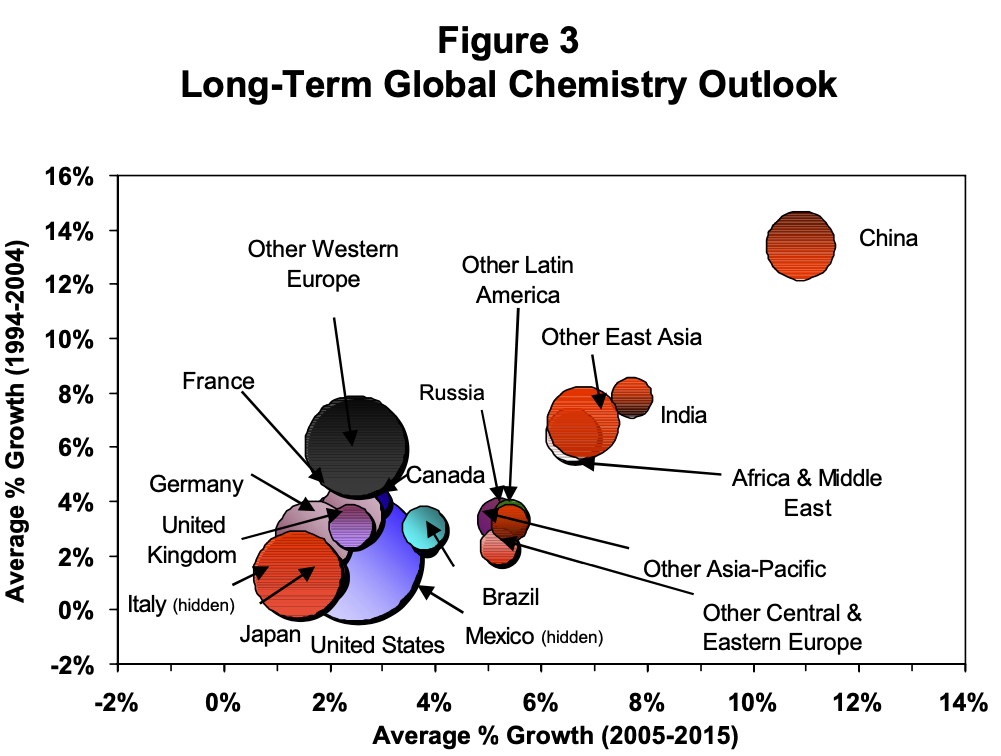

Looking to the long-term, global economic growth is expected to average 3.9% per year during the period between 2005 and 2015. Growth in global industrial output will average 4.6% per year, a pace 1.2 times that of global economic growth. As would be expected and as illustrated in Figure 3, growth prospects will be faster in China and the other East Asian nations. Indeed, China will account for about one-fifth of the incremental growth in industrial activity as the nation’s industrial prowess further progresses. India and several nations in Latin America and Central & Eastern Europe will also experience strong industrial growth while North America, Western Europe and Japan will lag.

During the period from 1994 through 2004, the global business of chemistry grew 3.7% per year, slightly lagging the 3.8% pace of average global economic growth. period included a still sluggish recovery from the early-1990s recession in Europe, the Asian crisis, and the most recession. During the next 10 years, the global business of chemistry is expected to continue lagging economic growth. It will lag global industrial output as well. Growth is expected to average 3.4% per year during the 2005-15 period. The best prospects will be found in Asia-Pacific (excluding Japan), where the business of chemistry’s growth will exceed (by 1.2 times) that of overall economic growth. Because of advantages in feedstocks, Africa and the Middle East will also experience strong growth. In other regions, growth will be closer to the pace of economic growth.

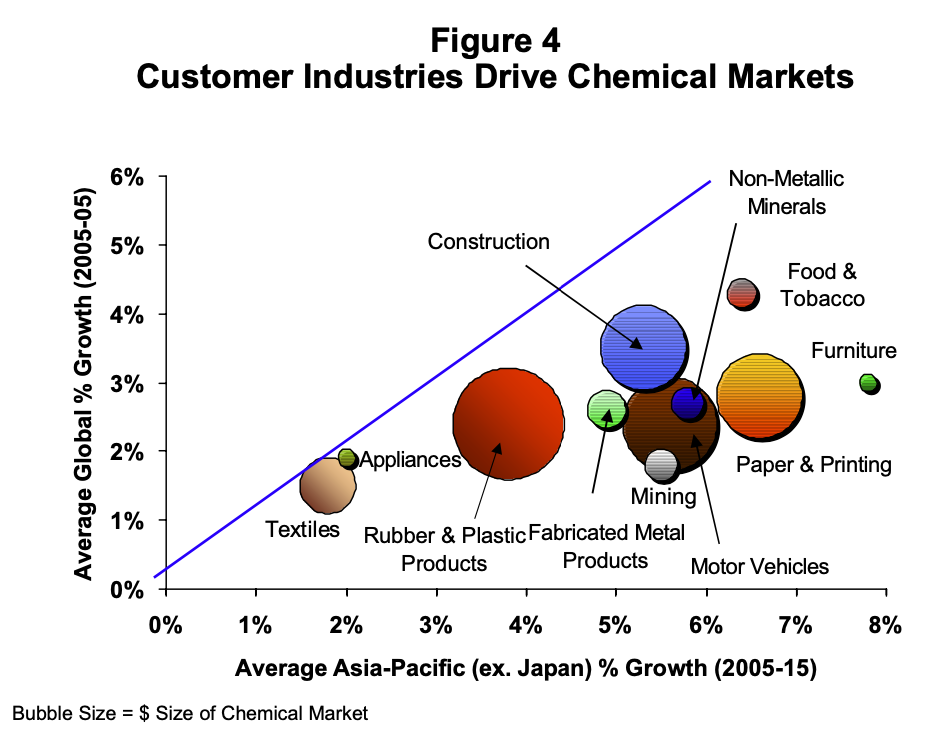

Two long-term trends are apparent. First, the movement of end-use customer industries to China and elsewhere in the Asia-Pacific region (excluding Japan) will continue as illustrated in Figure 4. This was led by textiles and has spread to light vehicles and now electronics. A shift in light vehicle assemblies from Western Europe to Central & Eastern Europe is also occurring as companies take advantage of lower-cost, skilled work forces in close proximity. One long-term structural issue is the move of pulp and paper production away from the northern hemisphere toward nations such as Brazil, China, and Indonesia where trees grow faster or costs are lower. A shift in the geographical focus of rubber and plastics processing is now occurring and the high levels of capital formation in China and elsewhere in the Asia-Pacific region is engendering much stronger construction activity and associated chemistry demand.

Second, there a number of nations with abundant hydrocarbon resources that represent advantaged feedstock locations. Most notable are Iran, Kuwait, Qatar, and Saudi Arabia. With strong low-cost advantages in petrochemical feedstocks, the Middle East is poised to obtain a larger share of global petrochemical capacity, the output of which will increasingly be exported to, Asia/Pacific, Western Europe, and possibly North America. Geo-political risks are high in this region but are balanced by significant feedstock advantages. With major investments underway, these nations have been adding significant capacity. Some delays in these projects could occur but rising demand from Asian markets will aid production gains.

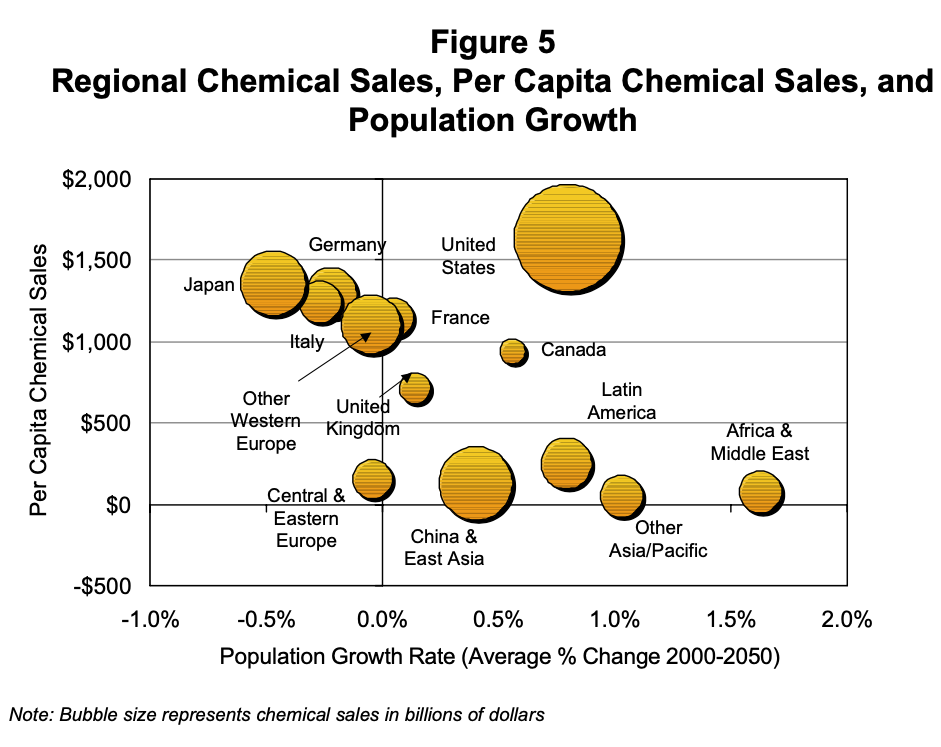

Looking even longer-term, demographic issues will play a dominate role. Declining working age populations in Europe, Japan, and eventually even in China raise questions about economic growth potential. At the same time, aging populations will strain government programs. Through the year 2050, overall population levels will decline in most of Europe and in Japan, while slowing elsewhere. Assuming long-term chemistry demand is correlated with population (and incomes, technology, etc.) this has negative implications for market developments in these nations. Stronger population growth in Africa and the Middle East imply the emergence of this region as a growth leader. Continued strong economic growth will aid prospects in Asia-Pacific (excluding Japan) and in Latin America. As highly developed markets, the United States and Canada cannot be ignored as they will present opportunities as population continues to grow. Figure 5 illustrates the relationship between population growth, current development of the chemical markets in these regions (as measured by per capita chemistry sales), and the size of the business of chemistry in each major nation or region.

Summary

In summary, in the main short-term scenario there will be some moderation of global growth in 2006 in response to higher energy prices, higher US interest rates, and a gradual adjustment of global imbalances. The business environment for the global business of chemistry is favorable and improving. Reflecting a recovery in overall industrial production, the output for the business of chemistry will improve during 2006 and 2007. Growth prospects will be faster in China and the East Asian nations than in Western Europe or North America. From a segment viewpoint, strong growth is expected in plastic resins, petrochemicals, and coatings. There are, however, still considerable uncertainties that need to be taken into account including energy prices, exchange rates and possible geopolitical shocks. During the next 10 years, the business of chemistry will mature, with growth prospects centered in China and other East Asian nations as well as in Africa & the Middle East. Looking even longer-term, demographic change will adversely affect demand potential in Europe and Japan.

Appendix: Sources and Methodology

The source of data on chemical industry growth presented in the tables and cited in the text by is the ACC Global Index of Business of Chemistry Activity. The ACC Global Index measures business of chemistry activity for 23 key nations, sub-regions, and regions, all aggregated to the world total. The index is comparable to government production indices and features a base year where 2002=100. This index is developed from government industrial production indices for chemicals from over 55 nations accounting for over 96% of the total global business of chemistry. Some segment data is provided at the regional level.

Historical economic growth is from the International Monetary Fund but the estimations or forecasts for 2005-2007 were made by the author. Data on industrial production are from the various national statistical agencies and are aggregated by the author based on relative weight of the national economy. The assessment is based on economic data and publicly available information through early-November.

In looking ahead, a proprietary model of global output for the business of chemistry is employed. The author also takes into account the forecasts made by economists at the various national chemical associations, the expertise of whom he gratefully acknowledges. Also gratefully acknowledged is the macroeconomic and chemical industry expertise of Oxford Economic Forecasting Ltd. (OEF), one of the world’s leading providers of independent economic advice and consultancy services. The long-term projections reflect on-going scenario development and modelling work by the author as part of an assessment of long-term demographic change and its effects on economic growth and the prospects for the business of chemistry.