The logistics profile of the German chemical industry

Abstract

The article aims at giving basic data and interpretations on the chemical logistics sector in Germany. The findings are based on a combination of primary research and secondary data in the field of logistics service providers, logistics agglomerations and logistics employment. Logistics service providers that are specialized in services for the chemical industry are identified. The special requirements for logistics handling goods for the chemical industry are derived and logistics clusters in the German chemical industry are presented. The development of logistics employment indicates that logistics activities in the chemical sector are frequently outsourced.

1 Introduction

Global players such as BASF, Henkel or Dow Chemical are competitors within the chemical industry which is an important business sector. Interconnections between the industry and other sectors such as the automotive manufacturing industry, the pharmaceutical or the consumer goods production industry underline this importance.

The chemical sector has a unique supply chain and demands a range of logistics services. Make or buy decisions regarding logistics projects are frequently required. As deciders and supply chain operators often need to plan under high uncertainty (Chae, 2009), basic data regarding the structure of the sector’s logistics set-up on particular geographical markets is essential in order to support decision- making processes.

Contemporary logistics research tends to be focused on particular topics and case studies focus on single companies or particular developments. Apart from that, the purpose of this essay is to deliver approaches and basic quantitative data on the chemical industry and its logistics environment over time. The research work presented in this article is based on evaluations and ongoing work of the Fraunhofer Center for applied research on Supply Chain Services (SCS) for the purpose of building knowledge, expertise and data on supply chain services. Basic studies of Fraunhofer are addressing logistics market sizes, market segments, logistic service providers (LSPs), logistics employment, logistics locations, trade interconnections and future trends. The basic motivation is to improve circumstances for complex decision situations that occur on a daily basis in globally interconnected firms, their supply chains and, following Cooper et al. (1997), supply networks. Referring to Cooper et al. (1997), a supply chain seldom looks like a pipeline, but more like a tree with its roots and branches, which need to be managed properly.

The structure of this article is as follows. Subsequent to the introduction, section 2 gives an overview of the chemical industry in Germany. Sections 3 to 5 provide insights in methods and results for three different dimensions of the chemical industry’s logistics: the chemical logistics market (section 3), the chemical logistics employment (section 4) and the chemical logistics sites in Germany (section 5). Each of these sections 3 to 5 presents methods as well as results. Section 6 shows trends that the chemical logistics industry is currently facing. Section 7 concludes with final remarks and suggests fields where research should help to gain transparency on industry-specific logistics.

2 The chemical industry in Germany

In 2013, the chemical and pharmaceutical industry reached total revenues of EUR 854 bn in Europe and held a share of more than 10% of the total European manufacturing industries’ turnover (Eurostat, 2015; own calculations). For Germany, the corresponding figures show revenues of about EUR 147 bn (Destatis, 2015; own calculations). About 17% of the European total revenues of this industry are concentrated in Germany and about 328,000 employees work in the sector (Destatis, 2015; own calculations).

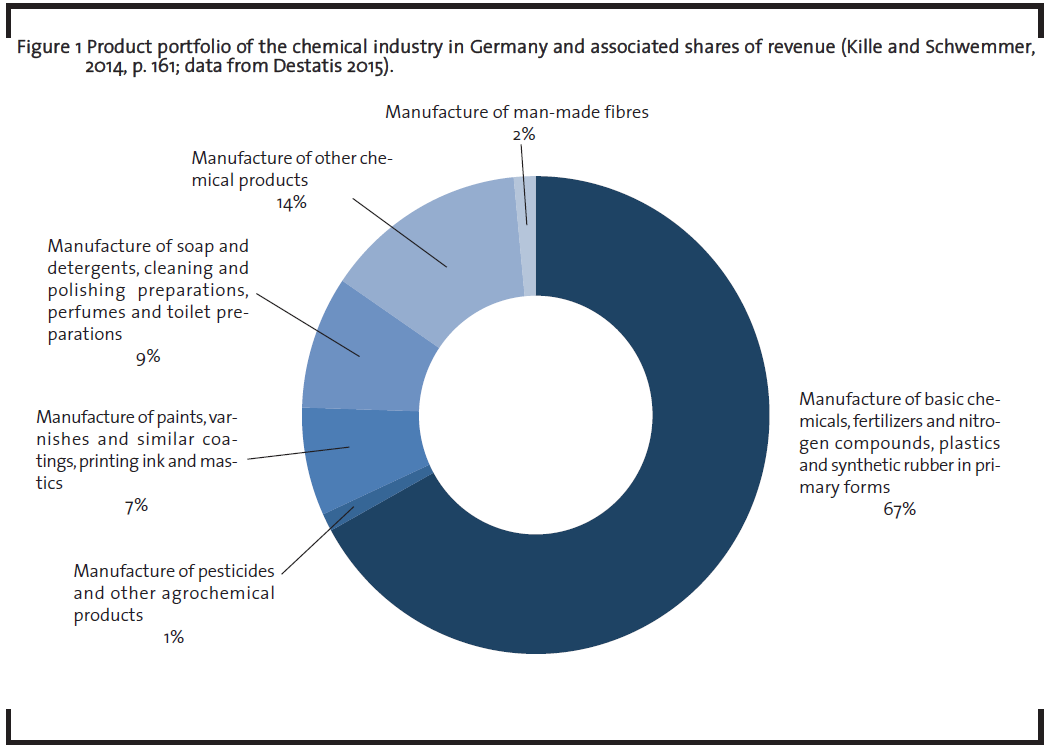

Figure 1 shows the products manufactured by the German chemical sector in the year 2013. About two thirds of the revenues are generated by manufacturing and selling basic chemicals. Soap and detergents (9%), coating and paints (7%) as well as chemical fibers (2%) and pesticides (1%) occupy further shares. A noticeable share of 14% of the manufactured products is clustered as other products in statistics, showing that the chemical industry holds a variety of products that cannot be clustered otherwise.

Dominating trading partners in im- and exports are the Netherlands, Belgium and France. Most of the neighboring European countries are customers of Germany’s chemical sector. The flows of goods predominantly consist of basic chemicals presenting 82% of imports and 77% of exports (Kille and Schwemmer, 2014).

3 The market for chemical logistics

3.1 Methodological remarks and data processing

For the basic analysis of an industrial sector and the market for logistics activities for and in this sector, we first partition the field of interest into smaller sections that can be measured by using different approaches. A market is a physical or virtual space that connects supply and demand for products or services. Such a market can be segmented into its basic parts that are the suppliers and demanders. As they do not do business for an altruistic reason, the items of interest why suppliers and demanders work together also need to be taken into account, i.e. the goods (compare Bofinger, 2011).

3.1.1 Statistical classifications as key to ascertain facts on industrial sectors

One of the most important approaches to assess industrial sectors from an economic perspective is to use established industrial classification systems (such as ISIC, NACE in Europe or WZ08 in Germany). These systems provide distinct codes that enable a targeted analysis of parts of an economy and enable combining data from different statistical sources on revenues, tonnages moved, employees, the value of traded goods, type and number of relevant goods etc. in a sector. Furthermore, through the combination of these items of data, ratios can be calculated and compared across different sectors. In addition, the development of those figures can be traced via time series analyses. When using data this way, a basic prerequisite is that the retrieved statistics are structured according to these industry classifications. If data is prepared by using different classification systems, extensive efforts are necessary to harmonize this data to enable a joint analysis.

The German statistical classification WZ 2008 was developed by the Federal Statistical Office of Germany (Statistisches Bundesamt, 2008) and is commonly used. It also forms the basis for the evaluations of this essay. As this classification is corresponding to NACE Rev. 2, comparative analyses with data available from Eurostat on different countries of Europe is possible.

3.1.2 Manufactured and traded goods characteristics

The basic requirements for logistics can be derived from the nature and type of the goods that are manufactured and traded within an industry. The WZ 2008 system differentiates 16 types of manufactured goods for the chemical manufacturing industry (wholesale and raw material mining are excluded) (Statistisches Bundesamt, 2008). This classification system defines which products are included and which are excluded for every type of goods. To align interpretations from statistical data, sighting and clustering the manufactured goods regarding their physical characteristics is useful. Some basic characteristics regarding the logistics needs of goods are fluidity, bulkiness, solidity, toxicity and fugacity, which decide about how goods are handled and transported, e.g. either as palletized or packed goods, or via tanker.

In general, the typical means of transport can be derived via literature research and can be adapted to individual cases. Special issues might require additional qualitative or quantitative primary research among practitioners from the respective industry.

3.1.3 Assessing the demand side in logistics markets

Demanders in industrial logistics markets are those that have goods in need for transportation services. The following approach is used in order to identify the most relevant demanders within a specific industry (as surveying practitioners often does not result in a comprehensive list).

In step 1, data is extracted from company databases. There are some of them available for the German market and even more for other countries. Usually, these databases allow an export of data according to the industrial classifications that are used by statistical offices. Combined with the information on the turnovers of these firms that are mostly available in database extracts, a draft version of an industrial sector’s top firm ranking may easily be achieved. However, pitfalls and shortcomings of such rankings often come to light. The most frequent reason for problematic results is that the assignment of firms to industry sector codes is not as distinct as desirable. In addition, the affiliation is sometimes inadequate as many firms are active in different fields through a diversified setup. Thus, one statistical code might not be sufficient to classify such firms. For example, this is the case for Siemens, a global player in machinery, electricity, plant construction and other sectors. Therefore, company databases also display one or more secondary classification codes as a method to resolve such shortcomings. Usually, a company description is also available to characterize companies. Nevertheless, these pieces of information are insufficient to obtain a valid list of top firms in an industry without considering further information.

To set up a ranking, additional research needs to be carried out that encompasses the screening of business profiles, business reports, magazines and similar sources. An exchange with experts is helpful if a list needs to be set up from scratch, i.e. if not a single source or company database can be drawn from to draft a ranking. A recent research project (Schwemmer et al., 2015) aimed at just this topic with providing a list of the most important competitors in the field of less-than-truckload transportation across Europe. As information on this particular topic is not surveyed by any source or database, a list of the most important companies had to be created out of nothing.

3.1.4 Assessing the supply side in logistics markets

As logistics markets and companies are not sufficiently dealt with in official statistics, there is an essential gap for valid assessments of the logistic service provider sector. In need for data on this underestimated business sector, Fraunhofer SCS began to gather data on LSPs in Europe. For more than 20 years now, data has been gathered in exchange with logistics firms. The process includes identifying, cataloging and characterizing respectively profiling logistics companies.

Similar to establishing a list of the biggest firms in an industrial sector, the work to establish a top ranking for the biggest LSPs in Germany is only possible to be achieved by elaborate research work. Primary research on this topic includes identifying logistics firms and evaluating their businesses by surveying those firms concerning their business size, business model and other relevant aspects (like e.g. number of employees, organizational structure and customer segment focus). While the customer segment focus of a LSP might be easy to assess by the modern means of communication (homepages, company reports, etc.), the real capability of an LSP in doing business in a particular industrial segment can hardly be attained. Thus, collecting primary data is the method of choice.

3.2 The case of the German chemical industry

For Germany, the cost volume of logistics activities in and for the chemical industry is estimated to be about EUR 14 bn in 2013 (Kille and Schwemmer, 2014). This includes logistics activities that are outsourced to LSPs and those rendered in-house by wholesale or industrial firms (not outsourced).

The most important countries for Germany with regard to trading chemical commodities are the Netherlands and Belgium. This is especially attributable to the port of Rotterdam being of significant importance for the European chemical industry.

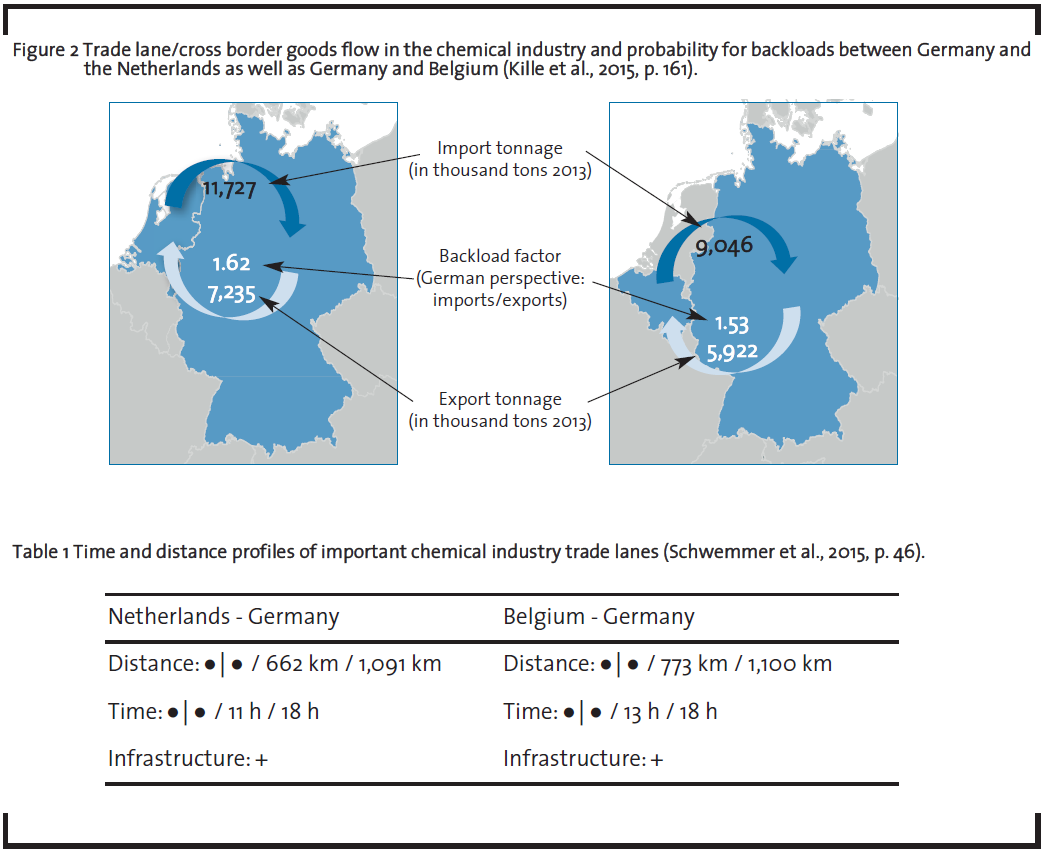

From a logistics perspective, the balance of trade flows is interesting to analyze as it can have effects on the kind of logistics services that are available and on price levels of logistics services regarding the trade lane. The decimal numbers within figure 2 represent directional backload factors. These are calculated as the imported measured against the exported tons. A backload factor of 1.0 represents equivalent goods flows in both directions (imports/exports=1). Backload factors that are below 1.0 (resp. above 1.0) show an unbalanced flow of goods with less (resp. more) tons flowing in than out. From a German point of view, the backload factors are 1.62 and 1.53, so that the incoming tonnage from the Netherlands and Belgium is about 50% higher than the amount delivered from Germany to those countries. The probability that backloads can be acquired for outgoing transports from Germany to the Netherlands (resp. Belgium) is high, and vice versa, the risk for an empty run backwards is low. The river Rhine between Rotterdam and Mannheim in Germany is the single most important trade lane for hinterland traffic from the port of Rotterdam.

Time and distance profiles for the mentioned trade lanes are displayed in table 1. As the countries are bordering each other, the minimum distance is set to 0 km by the used symbol (•|•). As shown by the second distance measure, the distance between the countries’ capital cities is 662 km resp. 773 km. The third distance measure denotes the furthest distance to connect the countries. Assuming an average speed of travel of 60 km per hour, the displayed time is necessary to travel the distance via road traffic. As the plus symbol indicates, the infrastructural conditions on these trade lanes are good, one can assume that the average speed of 60 km per hour can be reached within these countries.

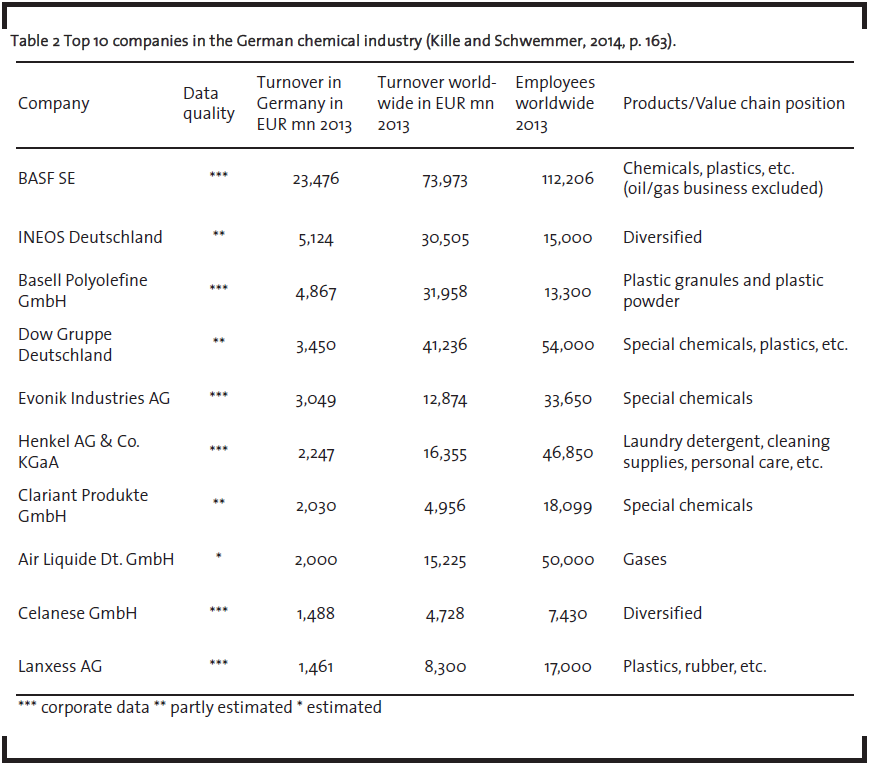

The demanders of logistics services in the chemical industry in Germany are displayed in Table 2. This top 10 list presents the demand side of the chemical logistics market for Germany as a result of a study conducted in 2014 with turnover information available for 2013.

BASF is top of the list with a large turnover and is followed by INEOS’ German entity. Basell is ranked third. As Germany is a large economy, the top 10 chemical companies reach turn-over figures that are well above the mark of EUR 1 bn per year.

The products of the companies do not only differ in type but also regarding their requirements for distribution to customers. E.g. Henkel’s products are to be found at customers like supermarkets and drug stores, which are mostly located in inner cities, they are purchasable by end consumers. Most of the other manufacturers’ products are supplied to other industries in business-to-business relationships and are not specified according to end customers’ requirements. The top list mainly includes well-diversified players with a wide range of products involving different handling requirements and logistics services.

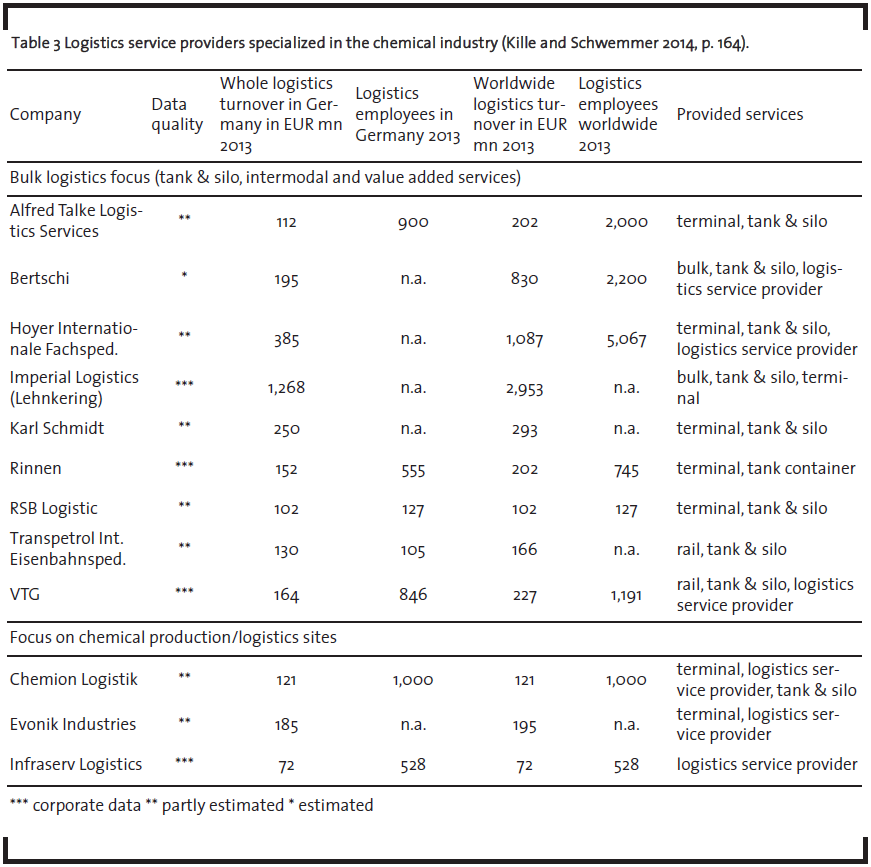

The LSPs that are specialized in the chemical industry are shown in Table 3. A complex range of produced goods requires a suitable logistics mix. The chemical industry is marked by fluid and bulky goods that are transported inbound to the manufacturers sites. Such sites may represent small and specialized as well as large and complex composite sites, so-called “Verbund sites” as coined by BASF. Such composite sites need own infrastructures that enable efficient internal transportation and value adding processes. In contrast to other industry sectors, a special kind of LSPs emerged from the chemical industry that carries out transports at the composite sites of the manufacturers as location-based service providers. As these are often spin-offs of the manufacturers at site, they mainly provide services for their parent company but might also provide services for third parties.

The included LSPs all hold specialized equipment and assets to provide their services and to handle hazardous goods. Therefore, barriers to entry into these LSP markets are high. Certificates that prove that LSPs are able to handle hazardous goods and fulfill quality standards are relevant to build trust to possible contractors.

Besides specialized load carriers, there are many generalized logistics services relevant for the chemical industry. The closer the end customer is, the more general is the logistics equipment. For example inbound transportation is often carried out with the use of pipelines, tankers or tanker trucks as bulk transports, the outbound transportation as well as distribution to original equipment manufacturers, wholesalers or retailers are more distinct and can be carried out by parcel or packaged goods carriers. No other industry holds a higher share of inland vessel transportation than the chemical industry with about 10% of the carried tonnages moved by barge. Transportation by train is also noticeably high at 14%, which even grew from 2011 to 2013 by about 1% (Kille and Schwemmer, 2014).

4 Chemical logistics employment

4.1 Methodological remarks

Logistics is often represented by an extra economic section within statistics (section H – Transporting and storage within NACE Rev. 2). This industry code does not obey the cross-sectional characteristic of logistics but encompasses the LSP market. Employees that perform logistics tasks at manufacturers and trade companies are not taken into account. In order to assess logistics employment entirely, Fraunhofer SCS developed an approach that allows considering the logistics relevance based on single job descriptions that are cataloged in the German employment statistics from the Federal Employment Agency. For each job that is classified in these statistics, an individual logistics share was derived (Kübler et al., 2015). Basis for this evaluation are special data sets on the German labor market published by the Federal Employment Agency (Bundesagentur für Arbeit, 2014).

4.1.1 Extracting chemical logistics employment

An extraction of the chemical logistics employment from the statistical basis needs to take into account specific supply chain characteristics of the chemical industry: Handling and transportation of chemical goods and also related administrative tasks occur at chemical manufacturers, chemical trade companies (wholesale) and at LSPs. These LSPs carry out logistics activities that are outsourced by the shipping companies. While the amount of logistics personnel in the relevant manufacturing branches (e.g. “manufacture of coke and refined petroleum products” and “manufacture of basic pharmaceutical products and pharmaceuticals”) can be quoted directly from statistics drawn from the Federal Employment Agency, figures for wholesale and LSPs have to be estimated (Krupp et al., 2013).

4.1.2 Considering administrative and self-employed workers

The first steps of calculation include employees who obviously perform operational logistics activities. Analyses show that – regarding 100 logistics employees – there are 15 additional employees necessary for administrative and management processes in the background (e.g. billing and accounting processes, human resources or management) (Kübler et al., 2015). This results in a 15% increased figure for the absolute amount of chemical logistics employees.

As data from the Federal Employment Agency only considers employees who are subject to social insurance contributions, analyzing logistics employees encompasses some additional steps of analysis. An evaluation of micro-census data, a sample survey covering roughly 1% of the German population (Statistisches Bundesamt, 2014), has shown that the total logistics employment is about 15% higher (Kübler et al. 2015). To account for the high amount of self-employed truckers and parcel distributors in the German logistics market, these workers need to be added to obtain the total amount of employment within the chemical logistics sector.

4.2 The case of the German chemical industry

In 2014, the chemical logistics market in Germany employed about 64,000 workers subject to social insurance contributions; the total employment (including self-employed people) is at about 73,700.

4.2.1 Chemical logistics employees can be found in different economic sectors

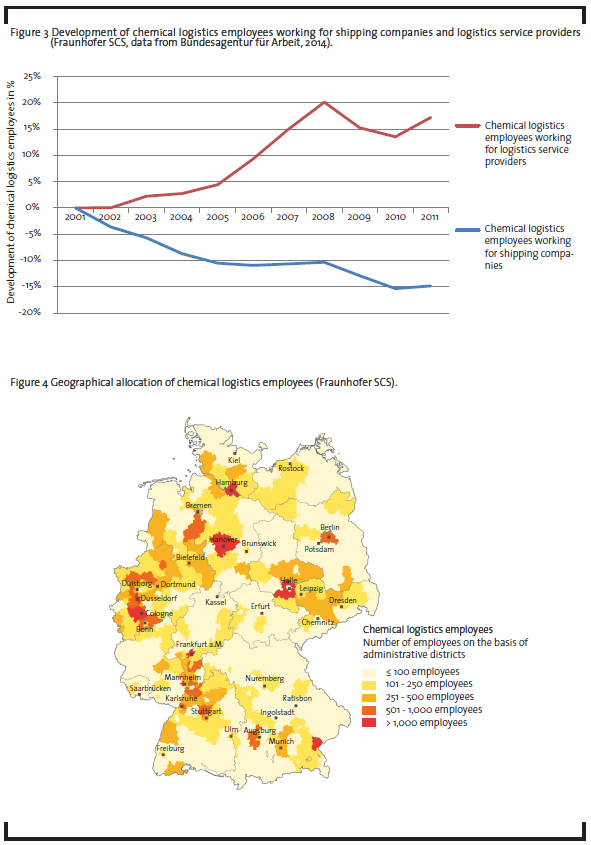

A share of 43% of the chemical logistics employees work for manufacturing companies such as BASF, INEOS or Henkel. Further 38% of the employment can be ascribed to LSPs specialized in chemical logistics. At least 19% of the total employees in the chemical logistics market work for wholesale companies, which deal with refinery and chemical products. Regarding the development of employees working at the LSPs, a constant increase can be observed while the number of employees working for shipping companies constantly decreases (figure 3).

These tendencies might be interpreted as a concentration of core competences in the manufacturing sector and a trend to further outsource logistics operations to LSPs. As data for other sectors look quite similar, these tendencies are not only specific for the chemical sector.

4.2.2 Geographical allocation of chemical logistics employees

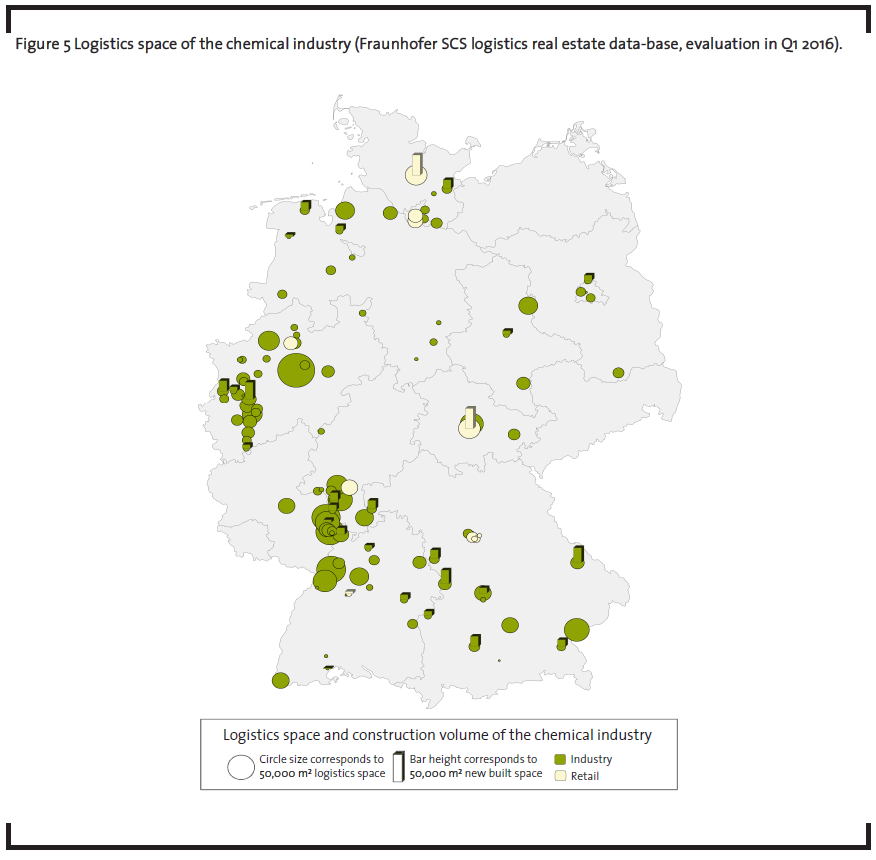

Regarding the geographical allocation of chemical logistics employees, a strong concentration on Western Germany – besides the area Leipzig-Halle and the south of Bavaria – is visible (figure 4). The highest numbers of employees can be detected close to the known chemical hotspots like the Rhineland and the metropolitan areas Rhine- Neckar and Rhine-Main. Almost 35% of all chemical logistics employees are working in those regions. While logistics employees (in general) are evenly distributed across Germany, chemical logistics employees are more concentrated. Nevertheless, there are many German administrative districts in rural areas that show a number of 100 employees or more besides the hotspots, e.g. at the border of Hesse and Thuringia in the center of Germany, in the west of Bavaria or in Mecklenburg-Western Pomerania in Northeastern Germany.

4.2.3 Requirements for chemical logistics workers

Chemical logistics offers a broad field of activity. A need for operational logistics activities exists when handling and storing highly diverse materials (chemicals, hazardous materials, liquids, etc.), in the procurement of materials for the manufacturing of chemical products and in the distribution of finished products towards wholesale and consumers. There is also a need for workers who have an administrative support function, like management activities or organizational tasks that are necessary to enable a smooth flow of logistics processes in the supply chain.

The challenges chemical logistics workers have to deal with are the heterogeneity of the handled products as well as the special instructions and safety requirements on hazardous materials. Chemical products show different aggregate states and a highly diverse value density; furthermore, they have to be monitored without a gap through the whole supply chain (Hardt et al., 2011). The high complexity concerning the handled products has led to the establishment of specialized LSPs. Another requirement those workers have to meet is the technical maintenance of plants as logistics employees might take part in manufacturing processes to some extent (Hardt et al., 2011). The deep integration of logistics in the manufacturing process is a reason why shipping companies operate logistics processes within their production plants by themselves. Until now, LSPs mostly take on distribution processes (Krupp et al., 2013).

5 Hotspots in chemical logistics

5.1 Methodological remarks

For the purpose of evaluating and identifying logistics hotspots on a scientific basis, Fraunhofer SCS developed an approach to evaluate logistics attractiveness on the basis of single administrative districts. About 20 different criteria concerning the logistics offer and demand of a district for logistics services form an evaluation index. The result is an index score for every German administrative district allowing conclusions regarding geographic logistics attractiveness (Veres-Homm et al., 2015).

5.1.1 Monitoring the German logistics real estate market

In order to match the “theoretical” attractiveness of geographic regions with real logistics settlements, nationwide data regarding newly built logistics properties in Germany has been collected by Fraunhofer SCS for about 10 years. Besides building knowledge on where logistics hotspots are located, the database was created in order to monitor and evaluate the development and structure of German logistics real estates. Prior to this kind of primary data gathering, information on logistics hotspots in Germany was only available from market reports of various real estate brokers. These reports mostly published data for the Big 5 sites in Germany (Berlin, Hamburg, Dusseldorf, Frankfurt and Munich), but did not cover the country as a whole.

The database includes about 8,500 data sets about properties which are explicitly used for logistics processes and cover a minimum warehouse space of about 2,500m2. Data sets are compiled via monitoring and evaluating press releases and internet-based tender platforms, market reports of business development agencies and real estate brokers. Further information sources are property offerings and exposés in internet platforms. This data collection method enables high transparency levels due to the availability of these resources to the public. So, newly built properties are captured almost completely, whereas data for real estate built before the year 2000 is not comprehensive.

5.1.2 Capturing different characteristics to run structural analyses

For each data set on logistics real estate, the following information is cataloged depending on its availability:

- Exact address to achieve a precise localization in a geo-information system

- Building size

- Land size

- Building year (date of the groundbreaking)

- Number of logistics employees at site

- Investment costs

- Economic sector of the user or in the case of LSPs, if known, the economic sector of the customer (shipping company)

- Further information regarding the building type, the distribution focus of the building or technical equipment (if available).

This database enables different analyses, e.g. of logistics settlements in specific geographical areas, the volume of new constructions of logistics real estate and thereby the dynamics of settlements. The database is also very suitable to evaluate logistics properties of an economic sector – to suggest its local hotspots and its site requirements. Furthermore, it offers the possibility to figure out if there are any specific characteristics, e.g. different sizes in relation to other economic sectors or specific technical features that investors have to consider when letting the warehouse to certain economic sectors.

5.2 The case of the German chemical industry

To visualize chemical logistics hotspots, the logistics properties, which are used by manufacturing or trading companies of the chemical industry or by LSPs operating logistics for the chemical sector, can be extracted from the database described in section 5.1.

5.2.1 Visualizing chemical logistics hotspots in Germany

Figure 5 depicts the logistics hubs of the chemical industry. Logistics properties which are solely used for the chemical industry are even more concentrated than the logistics employees (figure 4), who are often located in production plants or in case of wholesale in sales areas. Dominant logistics clusters exist in Western Germany with the Rhineland, the Ruhr area, the metropolitan areas Rhine-Neckar and Rhine-Main. Further settlement clusters represent Hamburg as central inbound site for containerized goods from overseas, Halle in the middle of Germany and Burghausen in the South of Bavaria. Besides these sites, some distribution centers operated by LSPs can be found.

Therefore, chemical logistics space can primarily be detected close to the historically settled production plants of the chemical industry along the Rhine, which is one of the most important inbound trade lanes for chemical raw materials (Kille and Schwemmer, 2015). The proximity to the shipping company turns out to be a priority for settlement decisions. BASF introduced the term “Verbund site” to express this closeness. According to BASF (2016), the site in Ludwigshafen located in the Rhine-Neckar area is the largest integrated chemical complex and biggest “Verbund site” within the BASF group.

5.2.2 Establishing chemical parks operated by service providers

At the end of the 1990s, in the course of globalization, the German chemical industry had to restructure and reduce its process costs to face worldwide competition. This also led to the relocation of sites from foreign countries. In this context, various chemical parks have grown (Grap and Milnikel, 2011). These sites are operated by a service provider who additionally offers properties, infrastructure, maintenance, facility management and further site services. Examples are the industrial park Höchst operated by Infraserv or the chemical park Marl operated by Infracor, formerly Evonik Industries. These chemical parks allow shipping companies to concentrate on own core competencies and to use cost intensive infrastructure like pipelines or rail connection in association with other shipping companies. Furthermore, special conditions such as the storage and handling of hazardous goods and 24 hours operation time are fulfilled (Veres-Homm et al., 2015). Finally, those synergies led to an increase in efficiency and cost reduction (Grap and Milnikel, 2011).

5.2.3 The chemical logistics real estate market

The companies BASF, Dow, Akzo Nobel, L’Oréal, Procter & Gamble and Henkel are the largest commercial users of logistics space within the chemical sector in Germany. Regarding specialized LSPs, Alfred Talke, Alfons Greiwing or Infraserv have to be mentioned. Additionally, diversified LSPs play an important role, e.g. DHL, Loxxess, Dachser or Fiege operate a considerable amount of logistics space in Germany (also see section 3.2).

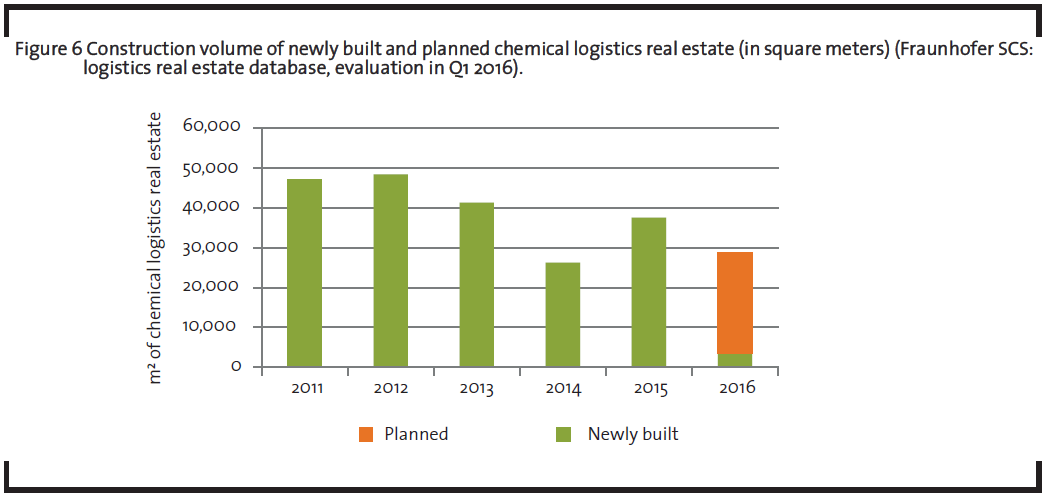

Regarding the construction volume of logistics properties in the last five years, the market for logistics properties in the chemical industry can be rated as small with a yearly volume of about 40,000m2 of new settlements (figure 6). Examples for new settlements in the recent past are Estée Lauder in Kerpen, Henkel in Dusseldorf or AlzChem in Trostberg. For the year 2016, further settlements are planned, e.g. Laverana in Barsinghausen.

The new properties are mainly located close to the described chemical industry clusters. Compared to locations outside of dedicated logistics parks, the construction of such settlements in dedicated logistics parks or commercial areas saves long and challenging approval processes to build up property that will be used for handling chemical goods. Besides that, synergies can be leveraged there more easily.

6 Trends in German chemical logistics

There are several developments that either affect the logistics sector or the chemical industry, or both.

Whereas the outsourcing degree of distribution processes within the chemical industry in Germany is already comparatively high, outsourcing in the field of highly complex and integrated logistics offers potential for future growth. Until today, shipping companies are very sensitive regarding the outsourcing of logistics tasks near to manufacturing processes like just-in-time delivery or in picking and packing. But as a higher usage of LSPs will lead to an increase in efficiency and accordingly to reduced costs in the course of a growing global world trade, it might also lead to an increase in competitiveness of the German chemical industry.

Due to restrictions for the settlement of new logistics properties and the given synergy effects, chemical parks will gain in importance in Germany. Potentials can also be found in the common use of IT and especially in a deeper IT-integration of LSPs and shipping companies.

As Germany and other European countries are challenged by the demographic change, the average logistics employee is getting older, and at the same time, less young people get trained. Especially in the field of transportation, the recruiting of truck drivers will become a difficult task. Already today, only 3% of the personnel which is used for transportation and delivery, is younger than 25 years (Bundesagentur für Arbeit, 2014).

Additive manufacturing is a technology on the rise. If this form of production and mass customization gains in importance, the chemical industry might provide raw materials to equip 3D printers. However, this scenario is dependent on the materials required for such digital direct manufacturing processes.

The chemical industry might face shifts in its supply chain and business models as distance trade (e-commerce) grows in importance in nearly every industry. Private customers currently represent a very small share of just above 4% as direct purchaser of outputs from the chemical industry. Therefore, the lever as origin of a paradigm shift is considerably small. As the trend to order via digital means of communication leads to smaller orders with increasing frequency over all industries in their business-to-business relationships, a shift towards a stronger end customer orientation within the chemical industry might occur in the near future.

7 Concluding remarks

According to Baghalian et al. (2013), supply chain planning is changing and firms need to rethink their role as part of supply chains and not as single enterprises any more. Consequently, supply chains instead of companies compete with each other as mentioned by different research work (see e.g. Cabral et al., 2012 and Christopher, 2000). Thus, supply chain planners need to take into account what the market and customers need (Fisher, 1997) and not only what the products and goods handled might need. Therefore, different concepts like “agility”, “flexibility”, “sustainability”, “resilience”, “robustness” and “leanness“ (of supply chains) have emerged in supply chain management research. To be able to manage those different strategic directions comprehensively, data and evaluations from different perspectives become indispensable.

This article’s purpose was to provide insights on how practical research work can help to make supply chains transparent from a national economics’ point of view. The combination of secondary data and primary research handled with specific designed databases and methods enables the compilation of a multi-layered picture. Especially, surveys among experts and practitioners are essential for knowledge building.

The methods applied in the article fit the German market best due to the expertise of the authors and the available statistics. As supply chains and logistics are multi-national, an international perspective should be taken into account in further research. Furthermore, from a researcher’s point of view, the comparability of different industrial sectors should become possible to elaborate crosssectional best practices.

As the world is developing towards service economies, a service perspective might gain in importance in supply chains that handle goods, just like the chemical industry. There might be a need to align logistics systems, supply chains and networks according to this service economy development in the near future. Researchers as well as practitioners should consider this when planning future supply networks.

References

Baghalian, A., Rezapour, S. and Farahani, R.Z. (2013): Robust supply chain network design with service level against disruptions and demand uncertainties: A real-life case, European Journal of Operational Research, 227 (1), pp. 199-215.

BASF (2016): Verbundstandorte weltweit, available at https://www.basf.com/de/company/aboutus/ strategy-and-organization/verbund/verbundsites. html, accessed 31 March 2016.

Bofinger, P. (2011): Grundzüge der Volkswirtschaftslehre – Einführung in die Wissenschaft von Märkten, Pearson Education, Munich.

Bundesagentur für Arbeit (2014): Jährliche Sonderauswertung sozialversicherungspflichtig Beschäftigter im Alter von 15 bis 64 Jahre nach ausgeübten Tätigkeiten der Logistik. Deutschland, Kreise und kreisfreie Städte (regionale Abgrenzung nach dem Arbeitsort), Bundesagentur für Arbeit, Nürnberg.

Cabral, I., Grilo, A. and Cruz-Machado, V. (2012): A decision-making model for Lean, Agile, Resilient and Green supply chain management, International Journal of Production Research, 50 (17), pp. 4830- 4845.

Chae, Bongsug (2009): Developing key performance indicators for supply chain: An industry perspective, Supply Chain Management: An International Journal, 14 (6), pp. 422-428.

Christopher, M. (2000): The Agile Supply Chain. Competing in Volatile Markets, Industrial Marketing Management, 29 (1), pp. 37-44.

Cooper, M.C., Lambert, D.M. and Pagh, J.D. (1997): Supply Chain Management: More Than a New Name for Logistics, The International Journal of Logistics Management, 8 (1), pp. 1-14.

Destatis (2015): Data available at https://www.destatis.de/, Statistisches Bundesamt, Wiesbaden.

Distel, S. (2005): Vermessung der Logistik in Deutschland. Eine quantitative Analyse der wirtschaftsweiten Logistikleistungen auf Basis der volkswirtschaftlichen Input-Output-Darstellung und der Beschäftigtenstatistik, Deutscher Verkehrs- Verlag, Hamburg.

Eurostat (2015): Data available at http://ec.europa.eu/eurostat/data/database, European Commission, Luxembourg.

Fisher, M. (1997): What Is the Right Supply Chain for Your Product?, Harvard Business Review, (March- April), pp. 105-116.

Grap, R. and Milnikel, B. (2011): Chemielogistik im Kontext allgemeiner logistischer Anforderungen, in: Suntrop, C. (ed.), Chemielogistik: Markt, Geschäftsmodelle, Prozesse, Wiley-VCH, Weinheim, pp. 12-13.

Hardt, A., Clemens, G. and Hinterlang, L. (2011): Standortlogistik für die chemische Industrie, in: Suntrop, C. (ed.), Chemielogistik: Markt, Geschäftsmodelle, Prozesse, Wiley-VCH, Weinheim, pp. 227-230.

Kille, C., Schwemmer, M. and Reichenauer, C. (2015): TOP 100 in European Transport and Logistics Services, DVV Media Group, Hamburg.

Kille, C. and Schwemmer, M. (2015): TOP 100 der Logistik – Marktgrößen, Marktsegmente und Marktführer, DVV Media Group, Hamburg.

Krupp, T., Suntrop, C., Kille, C., Veres-Homm, U. and Heeg, L. (2013): Chemielogistik. Bedeutung, Strukturen, Dynamik, DVV Media Group, Hamburg, pp. 10-11.

Kübler, A., Distel, S. and Veres-Homm, U. (2015): Logistikbeschäftigung in Deutschland – Vermessung, Bedeutung und Struktur, Fraunhofer Verlag, Stuttgart, pp. 26-37.

Schwemmer, M., Kille, C. and Reichenauer, C. (2015): “Less-than truckload” networks – The European Market for network based cross border goods flows, Fraunhofer Verlag, Stuttgart.

Statistisches Bundesamt (2008): Klassifikation der Wirtschaftszweige, Statistisches Bundesamt, Wiesbaden.

Statistisches Bundesamt (2013): Jahresstatistik im Handel: Unternehmen, Beschäftigte, Umsatz und weitere betriebs- und volkswirtschaftliche Kennzahlen im Handel: Deutschland, Jahre, Wirtschaftszweige, Statistisches Bundesamt, Wiesbaden.

Statistisches Bundesamt (2014): Mikrozensus – Bevölkerung und Erwerbstätigkeit, Stand und Entwicklung der Erwerbstätigkeit in Deutschland 2013. Fachserie 1 Reihe 4.1.1, Statistisches Bundesamt, Wiesbaden.

Veres-Homm, U., Kübler, A., Weber, N. and Caesar, E. (2015): Logistikimmobilien – Markt und Standorte 2015, Fraunhofer Verlag, Stuttgart, pp. 46-54.