The smart-up ecosystem: Turning Open Innovation into smart business

Abstract

The Fourth Industrial Revolution is changing the world. IT-based technologies start to have an increasing impact on the chemical industry. Incumbents need to smart-up in order to stay competitive. Especially small and medium-sized enterprises (SMEs) are facing a tough challenge as they lack resources and expertise in implementing Industry 4.0. In this paper, the smart-up ecosystem is introduced: a conceptual model that offers SMEs guidance on how they can move, step by step, from an uninformed situation into smart business. Based on initial experiences using the model in practice, some critical points along this smartification journey are highlighted.

1 Introduction

Innovation has repeatedly been identified as a vital driver for the European chemical industry. Firms need to innovate in order to stay sustainably competitive. Universities are often seen as an important source of knowledge for (more) radical innovation. Over the last decades, however, scientific findings turned out to be too far from market application to be directly interesting for incumbents. This gap in the innovation process has been filled up by start-ups. These young, technology-based firms play an important role as (temporary) carrier of new, innovative developments (Clayton et al., 2018). Once a start-up grows and the technological risk decreases, it becomes an interesting collaboration partner or acquisition target for established firms. These incumbents can enrich their business portfolio this way, while minimizing the risk of failure that is normal in the innovation process. Nouryon, in this context, organizes an annual worldwide challenge for start-ups to uncover sustainable opportunities for the company (Imagine Chemistry). This new way of growing innovative ideas via start-ups and the resulting interaction with incumbents perfectly fits the current open innovation era (Chesbrough, 2003). As chemical firms are no longer able to cover the innovation process alone, they need to interact with external sources of knowledge and new paths to the market.

Innovation ecosystems play a vital role in enabling technology-based start-ups to be created and to get interaction with incumbents ongoing. Bearing Silicon Valley in mind, many European countries have started to build their own ecosystems (Rissola and Sörvik, 2018). In the Netherlands (ChemieLink), a fine-grained innovation ecosystem was built to boost chemical start-ups. The backbone of this network – called ChemieLink– are ten innovation labs (ilab) and seven centres for open innovation (coci). The ilabs are physical locations equipped to allow chemical start-ups to take their first business steps. These incubators were realized in the vicinity of universities in order to smoothen the step for entrepreneurial researchers to start their own business. Once the start-up grows, it can easily move to a so-called coci: a brown-field site equipped to accommodate chemical scale-ups. At these locations, the incumbent present (e.g. DSM, SABIC) agreed to act as custodian, helping the young firm to up-scale their business and access international markets. At this moment, approximately 300 young, innovative firms are located at the 17 ‘ChemieLink’-hotspots in the Netherlands. These locations together literally bridge the gap between scientific findings and market application. There is, however, no time to rest on laurels as a new, significant challenge is imminent.

2 The Rise of the smart chemical industry

Innovation ecosystems and their inhabitants around the world are currently facing the breakthrough of IT-based technologies, giving rise to the Fourth Industrial Revolution. The First Industrial Revolution – starting halfway the 18th century – introduced water and steam power to enable mechanization. It substituted agriculture for industry as the backbone of the economic structure. Nearly a century later, the Second Industrial Revolution used electric power to create mass production. The chemical industry, for example, began to grow and brought society new products like dyes and fertilizer on a large scale (Hoffman and Budde, 2006). Innovations like the transistor and microprocessor subsequently paved the way for the Third Industrial Revolution in the second half of the 20th century. Production was automated within factories by means of computers and telecommunications. Currently, the Fourth Industrial Revolution is building on the Third. According to Klaus Schwab (2017), the founder and CEO of the World Economic Forum, this new revolution is characterized by the rise of cyber-physical systems. Emerging technology fields such as robotics, industrial internet of things, unarmed aerial vehicles and machine learning will result in fusion of the biological, physical and digital world.

In short, the Fourth Industrial Revolution is said to force firms to become digitally connected: both within the factory as well to the outside world (e.g. along the value chain). A so-called smart factory is envisioned ‘a fully connected and flexible system – one that can use a constant stream of data from connected operations and production systems to learn and adapt to new demands’ (Burke et al., 2017). If firms fail to grasp the digital transformation, their business might become disrupted. Examples are already seen in the service (or tertiary economic) sector: retailers lost clients due to online stores, tourists prefer Airbnb to conventional hotels and regular taxi companies suffer from Uber. In order to try to overcome this situation in the manufacturing (or secondary economic) sector, countries started campaigns to prepare their established manufacturing firms. In Europe, Germany was one of the first movers and coined the digital transition ‘Industry 4.0’ (Kagermann et al., 2012). The Netherlands followed in 2014, included new manufacturing techniques like additive printing and robotics, and labelled it ‘Smart Industry’. Currently, more than half of the EU-countries are addressing the digital transformation in manufacturing industries at a national scale (European Commision).

This attention is justified: the impact of the Fourth Industrial Revolution on the chemical industry is expected to be enormous. The Digital Transformation Initiative (DTI) team by the World Economic Forum and Accenture (2017) estimated, based on the value-at-stake methodology, the cumulative economic value for the chemistry and advanced materials sector to range from about $310 billion to $550 billion over the period 2016-2025. Moreover, in terms of non-economic benefits, digitization has the potential to reduce CO2 emissions by 60-100 million tonnes. Regarding firm-level, the DTI- team identified three themes that are expected to have a great impact. First, the digitalization of the firm itself: the efficiency of core operat- ing functions like R&D and plant operations can be further increased using digital simulation technologies. Second, chemical firms will be able to improve their customer interaction (e.g. understanding customers’ needs by social media mining) and develop new digitally enabled offerings. A chemical company will, for example, no longer sell fertilizers, but guarantees its customers a certain yield; or years of preservation instead of paint (Yankovitz et al., 2016). The third theme that is expected to have a great impact at the firm-level is collaboration in innovation ecosystems.

The interest in innovation ecosystems has increased in the last couple of years. Not only firms, but also governments and knowledge institutes are exploring the concept. However, while insights regarding the other themes (i.e. digitization of production and sales) emerge rapidly, the ecosystem concept remains rather vague. This ambiguity was recently addressed in a literature review (Suominen et al., 2018).

The researchers identified seven sub-clusters within ecosystem research; clusters such as knowledge ecosystems, the development of ecosystems and digital business ecosystems. The sub-clusters, however, overlapped when analyzing the most cited contributions. An indication, according to the scholars, that the research domain is still premature. The resultant lack of a practical ecosystem concept is a loss for chemical firms. It was hypothesized that those firms that are able to manage the complexity related to the ecosystem will strengthen their competitive advantage (Leker and Utikal, 2018). As complexity will only increase in the coming years due to digital technologies and the need for incumbents to interact with, for example, start-ups as source of innovative developments, a hands-on ecosystem model is highly desirable.

3 The smart-up ecosystem

In order to develop a concrete ecosystem model, one has to interweave the involvement of multiple stakeholders – both public and private – into the concept of open innovation. Only then all participants will experience enough recognition to join in and strive for collaboration in a symbiotic way. In this paragraph, such an ecosystem model – entitled the smart-up ecosystem – is introduced. This model was developed by adding insights from practice and theory to an existing ecosystem concept. However, before constructing the smart-up ecosystem, some methodological considerations and the existing concept (i.e. innovation ecosystem canvas) are briefly described.

3.1 Methodological considerations

In the last couple of years, the author of this manuscript was enrolled as senior project man- ager in multiple projects dealing with the analysis, development and management of ecosystems. The main inhabitants of these ecosystems were established firms from the manufacturing sector. Firms that were facing the digital revolution. In 2017, for example, the project management included the coordination of the national Smart Industry initiative in the eastern part of the Netherlands. In practice, a network of more than 25 organizations (industry associations, governmental organizations, knowledge institutes, etc.) was managed and developed.

The aim of this network – called BOOST (Smart Industry) – was to align, and where possible combine, the more than 500 support options of the network members for regionally-based SMEs (circa 4,500 firms in total). That way, the overview of options for SMEs would become clearer and stronger. As a project manager of this network, it was needed to act as a reflective practitioner (Schon, 1983): in order to get the stakeholders on the same page, it was required to go back and forth from practical discussions and experiences to theoretical conceptions. The smart-up ecosystem model that was developed in this period to align all support options was subsequently fine-tuned during a quick scan – on behalf of Holland Chemistry (Holland Chemistry) – on the smart chemical industry in 2018.

3.2 The innovation ecosystem canvas: From concept to product

The development of ChemieLink, the fine-grained innovation ecosystem to boost young, innovative firms in the Dutch chemical industry, is described in detail by van Gils and Rutjes (2017). They describe a five-year period in which a project team helped to realize an incubator (so-called ilab), tailored to the specific needs of chemical start-ups, in the vicinity of almost every Dutch university with a chemistry department. The rationale was that entrepreneurial chemistry students could hence start their firm almost as easily as, for example, a fellow student working on IT-innovation. Later on, the project team also assisted the creation of several brownfield locations for chemical scale-ups (so-called coci). That way, start-ups which out-grew the incubator would not lose too much time finding a suitable location to scale-up. The firm Flowid, for example, was born in the ilab of the Eindhoven University of Technology, but constructed a pilot plant at the coci ‘Brightlands Chemelot Campus’ in Sittard- Geleen (Flowid). At this moment, ChemieLink encompasses ten ilabs and seven coci-locations. To keep a high level of knowledge sharing between all locations, a network-coordinator was appointed and a steering committee installed. Together they draw up the annual plan, consisting of seminars on chemical and entrepreneurial topics, meetings of business angels and joint promotional activities.

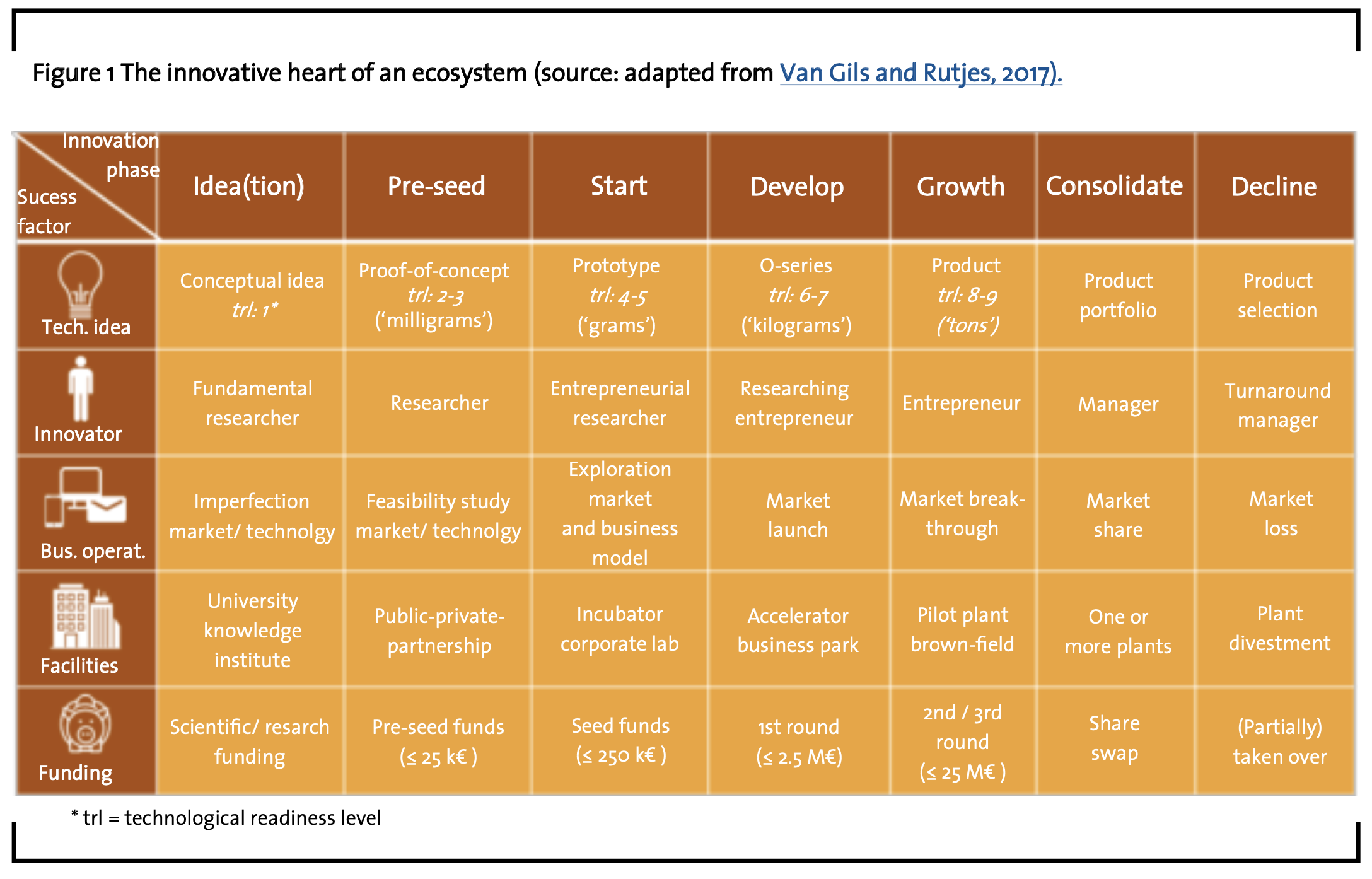

As a spin-off result of the work, the project team created the ‘innovation ecosystem canvas’ as a new method. The conceptual framework makes the changes explicit of four success factors for innovative activities alongside the technological development process. Based on the ideal type approach (Weber, 1947), the model shows for each technological development phase the best match for the innovator leading the team, business operations, facilities and funding (Figure 1). A researcher, for example, can best lead the team when working on a proof-of-concept, while an entrepreneur needs to be in charge once the 0-serie has to be introduced into the market.

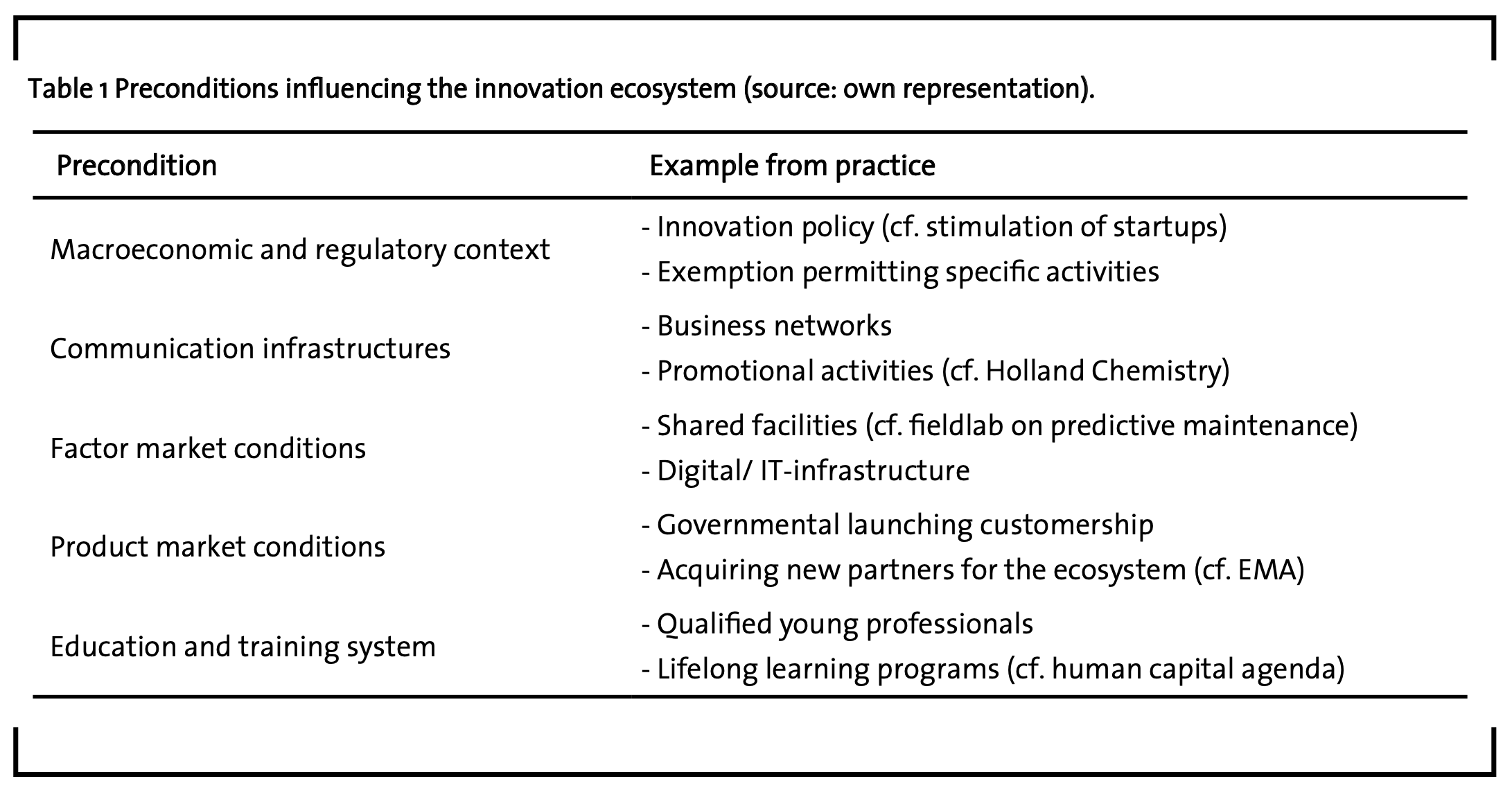

Next to outlining an appropriate configura- tion in each development phase, the model helps to depict the position of the stakeholders in the open innovation process. The innovative heart itself already involves two partners of the Triple Helix: firms and academia. Regarding the latter, the ‘heart’ mainly denotes its research and valorization task. The eldest task – education – of academia as well as the (tasks of the) third Triple Helix partner, governmental organizations, are found when considering the preconditions that ‘nourish’ the innovative heart (OECD, 1999). These five preconditions directly influence the ecosystem by means of examples as listed below (Table 1).

The final insight the ecosystem model can provide is a visual overview of all support initiatives aimed at innovative activities in a geographical and/or thematic delineated ecosystem. By using the model as a canvas and plotting an initiative at the point on the model it addresses an overview arises. Dragon’s Den, for example, is aimed at start-ups looking for funding, while an ilab covers the location need of start-ups. In other words: both initiatives are placed in the start-phase, however, Dragon’s Den is plotted on the success factor ‘funding’, the ilab on ‘facilities’. The resultant overview shows the options innovators have to get answers on specific challenges: you go to Dragon’s Den to get funded, not to ask them for help on your location; while you visit an incubator for the exact opposite. These well-defined cross-sections of an ecosystem (incubator, business angel network, etc.) were entitled ‘innovation biotopes’ (van Gils and Rutjes, 2017). The resulting overview of biotopes turned out to be helpful for governments and entrepreneurs. Policy-makers could start working on the improvement of the innovation ecosystem from a helicopter view. Entrepreneurs, on their turn, could find their way easier to support initiatives. An aspect that is particularly appealing to SMEs as it somewhat relieves the lack of organizational capacity and resources they face when engaging in open innovation (Brunswicker and Vanhaverbeke, 2014).

3.3 The challenge for SMEs: From uninformed to action

The ecosystem canvas turned out to be a powerful tool: several Dutch regions that focus on chemistry were mapped and discussions between stakeholders became – as they shared the same concept of an ecosystem – more to the point. In Southeast Drenthe, for example, the canvas helped to determine a blind spot in the support portfolio very accurately. Subsequent discussions with the regional triple helix led to an additional public investment in business development for chemical firms. This capacity was especially aimed at scale-up firms located at, or in the vicinity of, the coci in Emmen, being the physical hotspot of the regional chemistry cluster (Chemical Cluster Emmen). That way, the innovation ecosystem got a tar- geted boost. However, despite the added value in ecosystems covering predominantly young firms, the canvas it turned out to be less applicable in ecosystems consisting of mainly technology-based incumbents. Unlike digitally-born start-ups that almost automatically embrace new IT-technologies, incumbents still need to get fit first before they can adopt the digital revolution. Whereas corporates are able to fill out this need by installing a team overnight (e.g. Evonik established a digitalization subsidiary (Evonik)) or by cooperating with a start-up (e.g. Sabic cooperates with Ovinto to constantly track-and-trace its European fleet of 500 rail tank cars (EPCA)), established SMEs lack both resources and expertise in implementing Industry 4.0 (Schröder, 2016; Müller et al., 2018).

Established SMEs, while facing the digital revolution, are often ‘doing things like they have always done’. Whereas some of them are able to adopt new IT-technologies by means of learning-by-doing, other firms seem to be cramped. From their viewpoint, it seems almost impossible to make the right choice in the abundance of opportunities the revolution offers; let alone the implementation process (Smetsers, 2016). These firms clearly need some guidance through the transition process – going back from existing products to innovative concepts – even though it is impossible to show them the way individually. The main challenge: to get the firms out of their uninformed situation into an action modus. A process of learning that needs to be taken step-by-step in order not to lose them during the transition process. Despite the huge amount of recent literature on (organizational) learning processes, in daily practice the time-honored marketing funnel by Strong (1925) is still a suitable starting point. It discerns four phases someone needs to experience successively in order to go from getting acquainted with new possibilities to actually investing in them. The four phases of this journey are: creating awareness, generating interest, causing desire and, finally, taking action (the acronym is AIDA).

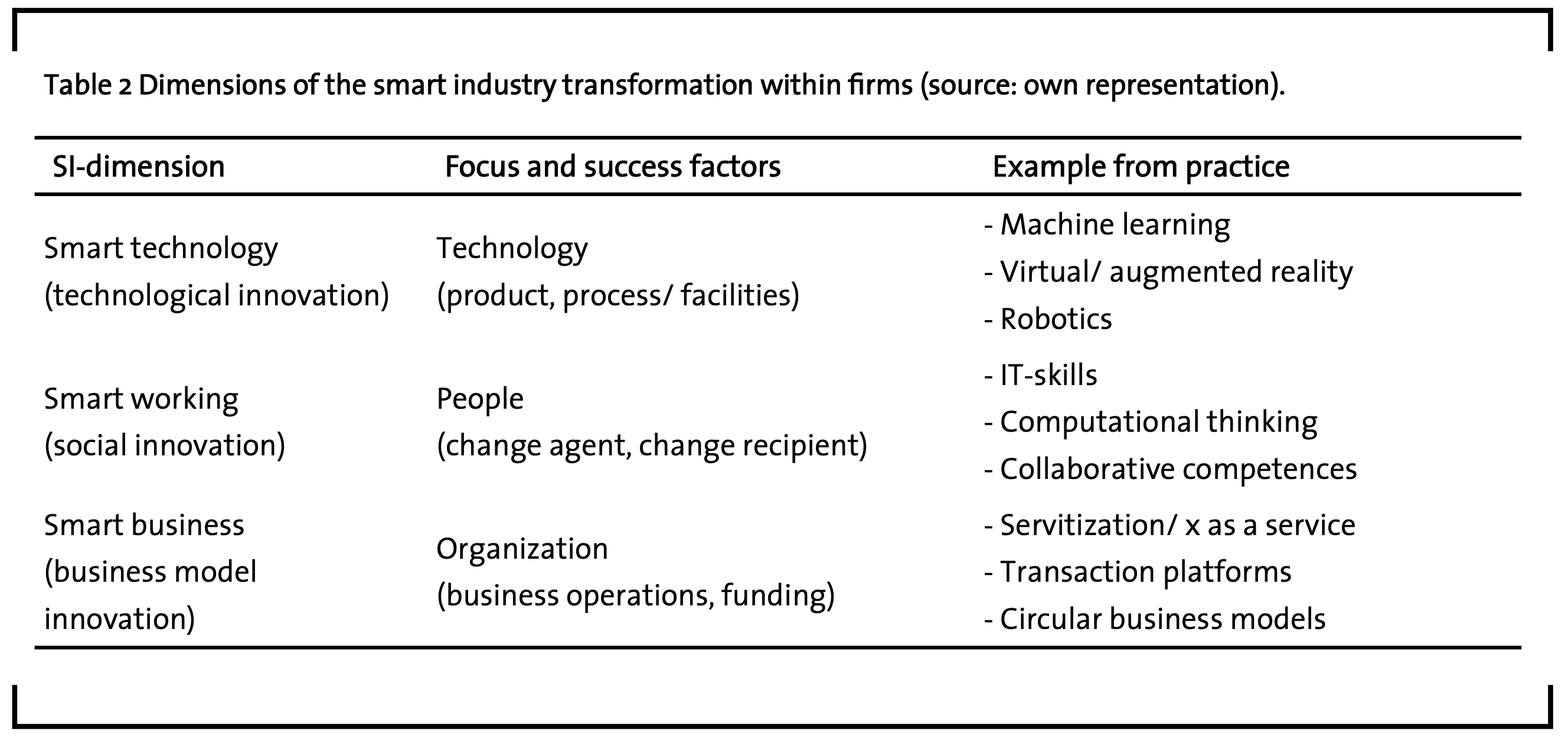

To make the AIDA-funnel applicable for the digital revolution, it is needed to interweave the smart industry dimensions into the transition process. In practice, three main dimensions are discerned: smart technology, smart working and smart business (Table 2). Firms need to act on all three in order to really smart-up. After all, buying a 3D-printer, but lacking the staff to operate it or a business model to turn its possibilities into revenue, will lead to failure. In other words: if one out of three is absent, successful implementation will be hard to achieve. Regarding the three dimensions, the same success factors as in the ecosystem canvas appeared relevant; however, the use of ‘change agent’ and ‘change recipient’ (Oreg et al., 2018) is more appropriate than ‘innovator and team’.

The combination of the AIDA-funnel and the three SI-dimensions leads to a basic model that shows the phases a firm has to undergo to ex-change their uninformed situation for action. In practice, initial awareness (first phase) about the digital revolution arises in a variety of ways: by talking to fellow entrepreneurs, reading the newspaper, listening to a customer, etc.. In other words, a spark – like in the model of Kline and Rosenberg (1986) – starts the firm’s smart-up process in most cases. Interest in a certain smart technology (big data, robotics, etc.) then normally evolves. The edited AIDA-funnel shows that one has to think, next to consulting knowledge sources on the technology, about how to involve the firm’s business and human part in this early ‘interest’ phase. For example by considering questions like: how will the firm profit from the investment in time? Does it merely offer possibilities for process optimization or also for product innovation? And which departments need to be involved? It is wise to already notify HR-officers and start a discussion about new skills? In reality, however, the next ‘desire’ phase is often entered after only completing the technological scan, increasing the risk of a failed implementation. In other words: a 3D-printer that gets dusted in a factory, an undesirable scenario thinking about the scarce resources SMEs have to smart-up (Schröder, 2016).

3.4 The smart-up ecosystem: Innovating and learning

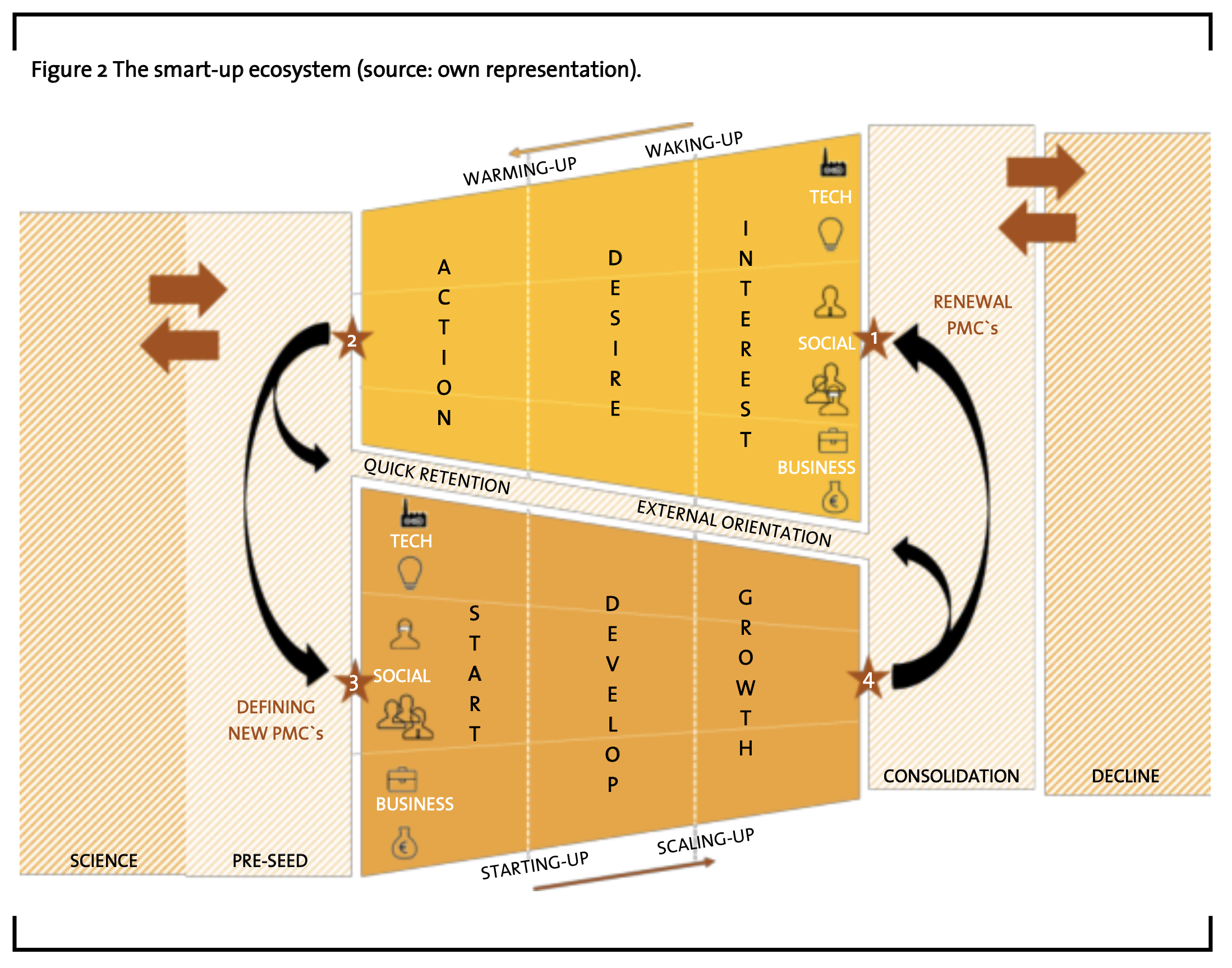

The innovation ecosystem model turned out to be a powerful tool, but its applicability in ecosystems consisting predominantly of technology-based incumbents was limited. It did not show how these firms, being innovators or laggards (Rogers, 1995), could renew themselves in the digital era. The innovation ecosystem model specified the process from concept to product, but not from existing product to new concept. In the previous paragraph, the way back was discussed. By enriching the AIDA-model with the three smart industry dimensions, a funnel originated that roughly outlines this route and helps to overcome opportunistic investments in smart technologies. When combining this ‘way-back’ funnel with the existing ecosystem canvas, the skeleton of the smart-up ecosystem arises (Figure 2). Central to the model are the innovating (ecosystem canvas; below) and learning (edited AIDA-funnel; above) pathways, which are connected by the pre-seed (left) and the consolidation phase (right). In both pathways, the corresponding phases as well as the SI-dimensions (i.e. people, technology and organization) are illustrated. On the two outsides are the phases that focus, on the one hand, on discovering new fundamental insights (idea phase) and, on the other, activities to avert the downfall of a firm (decline phase). 1

1 The preconditions as enlisted in Table1 also nourish the smart-up ecosystem, but are left away for clarity reasons.

In explaining the logic of the model, it is best to think about a firm that is in the consolidation phase. For example, a medium-sized firm that is producing a range of plastic products for a relatively steady group of clients. The firm possesses several injection moldings machines, has a clear focus on its running business and is acquainted with its competing colleagues. One day, at an international fair, the firm’s representatives are confronted with an new entrant: a start-up says to be able to print their less complex products for half the time and costs. Initially, the representatives laugh about it. However, a year later a regular client leaves the firm for the start-up. The entrant has found its way into the incumbent’s clientele. Starting from the less-profitable segment, the start-up aims to improve its performance and move upmarket. The incumbent is being disrupted (Christensen et al., 2015). Where earlier ‘awareness sparks’ – e.g. the fair, articles about 3D printing – stayed undetected, the loss of the client makes the CEO to start embracing the digital revolution (Figure 2: star #1). After an intensive process in which, among others, seminars are attended to grow the interest within the firm, workshops are followed by the management team to find out the most value added solution (desire phase) and skills are gained in a fieldlab (Smart Industry) by co-workers (action phase), the CEO decides to invest in 3D-printing (star #2). However, not to print clients’ products –like competitors do– but to produce plastic molds. Instead of buying a standard 3D-printer that can be used on occasional customer request by the trained co-workers (i.e. quick retention; intermediate path), the CEO decides to take it bigger and starts a full-blown innovation process (i.e. focus on the lower funnel). By producing plastic molds using 3D-printing, the firm will be able to better serve its customers: it can speed up the process from design to production, significantly lower the costs and offer small(er) series of plastics products as the high investments for regular molds are avoided. In order to realize the proof of concept – the level of technological development consistent with the pre-seed phase – the firm has to find co-development partners. On the one hand, to morph a commercially available 3D-printer to the specifications of the firm and, on the other, to develop a value proposition. The latter should include, according to the CEO, a digital assistant to increase the online connectivity with potential clients: a secure software platform that makes it possible for any customer to upload its 3D-file and receive a price indication directly. In other words: the chemical firm is looking to integrate several disciplines (e.g. IT, engineering, material science, business development), which are not all available in-house, to create a ‘Neue Kombination’ (Schumpeter, 1934). After joining network meetings to search for partners, discussing the best legal form for cooperation (project, start-up, etc.) and many other things, an internal project team – in close co-creation with external experts on IT and business development – is installed (star #3).

The route of starting-up and scaling-up begins. An innovation process, full of trial and error, follows in order to reach the desired technological product and sound value proposition. At the end of the growth phase, the project team presents the 3D-printer and shows how the digital assistant can help customers to order online the production of their plastic mold. This milestone marks a new point of strategic options for the chemical firm (star #4). On the one hand, the CEO could see it as the end point, adding the new proposition to the existing portfolio and trying to earn back the investments as soon as possible. On the other, he could also hold on to the innovative mood and stay externally oriented (i.e. taking the intermediate path). That way, the firm might bump into external partners like start-ups with new materials to print with or novel software solu- tions. According to Whitesides (2015), the latter option is the right way to go. He states (p. 3197) that ‘[the chemical] industry must either augment its commodity- and service-based model to re-engage with invention, or face the prospect of settling into a corner of an industrial society that is comfortable, but largely irrelevant to the flows of technology that change the world.’ In other words: being connected to early-stage developments at external partners is not only important for big corporates, but also for established SMEs if they are looking to continuously smarten-up their business in the digital era.

4 Learnings from the use of the model in practice

The smart-up ecosystem combines the pathways of innovating and learning. It provides incumbents guidance on how they can move, step by step, from an uninformed situation into a mode of realizing smart business. Based on initial experiences using the model in practice, some critical points along this smartification journey are highlighted. On the one hand, some extra considerations regarding the route mapped for firms are made. What are, for example, important challenges firms may encounter during the smartification journey? On the other hand, the model as canvas tool for (semi)public organizations is explained. How can it be used to upgrade an innovation ecosystem to a smart-up ecosystem?

4.1 The private perspective

The process of adopting smart technology and using it to increase the competitiveness is challenging for an established SME. However, being confronted with digitally-born competitors, while facing the end of the lifecycle, makes smartification a journey one has to undertake. Four critical points along that journey – like the strategic choice to stay externally oriented – were already highlighted in the previous paragraph. Two additional aspects, as they were witnessed in practice, need to be addressed:

- The need to focus on the business dimension to realize a smooth shift to the desire phase;

- The formation of a ‘coalition of the making’ to enter the start-phase.

Regarding the first aspect, it is important to concentrate on the type of activities that are in general available for incumbents walking along the learning path. Once convinced about the need to embrace the digital revolution, chemical firms bump into countless opportunities to build up their interest. They can visit multiple fairs and conferences each day. At those – often rather large scale – gatherings, firms are informed about the state-of-the-art on a particular topic. However, the employee himself has to translate the information received into possibilities for his firm. A difficult task, which becomes even harder when the employee returns to the firm and is confronted with all kind of urgent request by colleagues and clients. In many cases, the inspiration gained during a conference slowly fades away. A linkage to smoothen the shift to the next phase is to get a clear sense of the business potential in the interest phase. Success stories from other firms, for example, stressing that element turned out to help convincing management to continue to the desire phase. A phase in which the anonymity of a large-scale conference is absent as workshops, master classes and scans are usually the type of activities found in practice. Small teams of employees start working on the case of their own firm. The future business model, for which circularity could be a stimulating angle of approach, offers a good frame of reference when exploring the technology and human dimension.

With skills and expertise gained in the action phase, the chemical firm enters the preseed phase. To realize the proof-of-concept of the envisioned innovation, the firm has to find partners. After all, the innovation combines at least two disciplines (i.e. chemistry and IT), but probably even more. The technological development in this phase can often, particularly when a research institute is involved, be financed using public research funds. As a result, the formation of a coalition is feasible in most cases: firms are willing to join in as the financial risk is relatively low. A critical point is reached once the proof-of-concept is ready. The pre-competitive part is finished and public organizations have to give up their active role as a more commercial phase starts. The existing ‘coalition of the willing’ needs to be converted into a ‘coalition of the making’: a group of mainly private partners that needs to agree on a greater financial contribution (and risk) to develop the product. In practice, this implies that firms have to choose: either they join in or they are out. A difficult choice to make as not all aspects of the business case might be clear. Who should take the lead? What are the future prospects? Are all skills on board? What collaborative arrangement fits best? Questions that have to be answered; preferably not too late to prevent a break-up anyway. However, a manual is lacking.

4.2 The public perspective

The smart-up ecosystem model turned out to be helpful from a (semi)public perspective as well. The design and development of innova- tion ecosystems is often in hand of a regional and/or sectoral triple helix. Governments facilitate, in close collaboration with firms, industry associations and knowledge institutes, programs aimed at stimulating entrepreneurship and business growth. The innovation ecosystem canvas already proved to be a powerful tool in this situation: it enabled visualization of ecosystems, especially those created for start-ups and scale-ups, by plotting each initiative on the topic it addresses. The resulting overview improved discussions between stakeholders and helped to make better choices regarding new programs. Furthermore, the alignment between existing programs like accelerators, incubators and bootcamps was boosted and, accordingly, the bigger picture became easier to explain to entrepreneurs looking for support. The smart-up model offers similar possibilities. To be more precise, it helps a regional and/or sectoral triple helix to develop programs and instruments that established SMEs can use during their smartification journey. Or, in terms of a higher aggregation level: the model can help a triple helix to upgrade an innovation ecosystem –aimed at creating start-ups and growing scale-ups– to a smart-up ecosystem that boosts all types of firms.

Holland Chemistry, the triple helix for the Dutch chemical industry, is working on this upgrade. The quality of the current innovation ecosystem is already of a high level. It covers, for example, ten ilabs, seven coci-locations, grants for start-ups and challenges like ‘Image Chemistry’. With regard to the upgrade to a smart-up ecosystem, already quite a few initia- tives are in place. The portfolio includes, for example, a knowledge sharing platform ‘Molecules Meets Digits’, a fieldlab on condition-based maintenance and an action agenda on digital skills. The recent quickscan was a next step in the process that should lead to the smart chemical industry. The goal was to explore where the ecosystem could be further strengthened. By mapping developments and identifying low-hanging fruit – for example, use of VR for safety training – as well as long-term, highly promising opportunities (e.g. digital twinning), new insights were gained. The upgrade process now continues with the design of the optimal situation, bearing in mind these insights and the smartification journey SMEs face. The main challenge will be to find the right balance between (fundamental) research, needed to get accurate understandings, and innovative development and co-creation that is required to keep pace with the outside world.

5 Conclusion

The Fourth Industrial Revolution is changing the world. After disrupting the service sector (e.g. retail, hotel and taxi business), IT-based technologies like robotics and artificial intelligence are starting to have more and more impact on the manufacturing sector. Chemical incumbents need to smart-up in order to survive: digitally-born startups are on their way to disrupt existing markets. Where corporates appear to able to fill out their smartification journey by installing capable teams overnight or by collaborating with these startups, established SMEs in the chemical industry face a serious challenge. These firms lack both resources and expertise in implementing Industry 4.0. From their viewpoint, it seems almost impossible to make the right choices in the abundance of opportunities the digital revolution offers. In this paper, the smart-up ecosystem was presented for support. The conceptual model offers incumbents guidance on how they can move, step by step, from an uninformed situation into a mode of innovating. It shows how three important smart industry dimensions (technology, people and organization) are to be addressed throughout the transition process. The first experiences in practice showed that the model is useful for discussions with chemical SMEs: it helps them to better oversee the transition process which prevents them from dropping out early. Moreover, the model helped a triple helix alliance like Holland Chemistry in defining how they can upgrade their current innovation ecosystems – aimed at creating startups and growing scale-ups – to a smart-up ecosystem that boosts all types of firms. A key challenge was signaled in the pre-seed phase where ‘coalitions of the willing’ that are created around a certain idea need to be converted into ‘coalitions of the making’. Future research will address this point in order to resolve this disturbance in the process of turning open innovation into smart business.

References

Brunswicker, S., Vanhaverbeke, W. (2015): Open innovation in small and mediumsized enterprises (SMEs): External knowledge sourcing strategies and internal organizational facilitators, Journal of Small Business Management, 53 (4), pp. 1241-1263.

Burke, R., Mussomeli, A., Laaper, S., Hartigan, M., Sniderman, B. (2017): The smart factory: Responsive, adaptive, connected manufacturing, Deloitte University Press, New York.

Chemical Cluster Emmen, available at www.chemicalclusteremmen.eu, accessed 31 January 2019.

ChemieLink, available at www.chemielink.nl, accessed 31 January 2019.

Chesbrough, H. (2003): Open Innovation: the new imperative for creating and profiting from technology, Harvard Business School Press, Boston Christensen, C., Raynor, M., McDonald, R. (2015): Disruption, Harvard Business Review, 93 (12), pp. 44-53.

Clayton, P., Feldman, M., Lowe, N. (2018): Behind the scenes: Intermediary organizations that facilitate science commercialization through entrepreneurship, Academy of Management Perspectives, 32 (1), pp. 104-124.

Digital Transformation Initiative (2017): Chemistry and Advanced Materials Industry, White Paper, World Economic Forum and Accenture, Cologny/Geneva.

European Commission, available at ec.europa.eu/digital-single-market/en/coordination-european-national-regional-initiatives, accessed 31 January 2019.

European Petrochemical Association, https://newsroom.epca.eu/report-digitisation- in-the-petrochemical-supply-chain/, accessed 31 January 2019.

Evonik, available at https:// corporate.evonik.com/en/pages/article.aspx? articleId=322, accessed 31 January 2019.

Flowid, www.flowid.nl, accessed 31 January 2019.

Hofmann, K., Budde, F. (2006): Today’s Chemical Industry: Which Way Is Up?, Wiley- VCH, Weinheim.

Holland Chemistry, www.hollandchemi stry.nl, accessed 31 January 2019.

Imagine Chemistry, www.imaginechemistry .com, accessed 31 January 2019.

Kagermann, H., Wahlster, W., Helbig, J., Hellinger, A., Karger, R. (2012): Im Fokus: das Zukunftsprojekt Industrie 4.0: Handlungsempfehlungen zur Umsetzung, Bericht der Promotorengruppe Kommunikation, Forschungsunion, Berlin.

Kline, J. K., Rosenberg, N. (1986): An Over- view of Innovation, in: Landau, R., Rosenberg, N., (ed.), The Positive Sum Strategy: Harnessing Technology for Economic Growth, Academy of Engineering Press, Washington DC, pp. 275–305.

Leker, J., Utikal, H. (2018): Re-inventing chemistry – an industry in transition, Journal of Business Chemistry.

Müller, J., Buliga, O., Voigt, K. (2018): Fortune favors the prepared: How SMEs approach business model innovations in Industry 4.0, Technological Forecasting and Social Change, 132, pp. 2-17.

Oreg, S., Bartunek, J., Lee, G., Do, B. (2018): An affect-based model of recipients’ responses to organizational change events, Academy of Management Review, 43 (1), pp. 65-86.

Organisation for Economic Co-operation and Development (1999): Managing national innovation systems, OECD Publishing, Paris.

Rissola, G., Sörvik, J. (2018): Digital Innova- tion Hubs in Smart Specialisation Strategies, Publications Office of the European Union, Luxembourg.

Rogers E.M. (1995): Diffusion of innovations, The Free Press, New York.

Schon, D. (1983): The reflective practitioner, Basic Books, New York.

Schröder, C. (2016): The Challenges of Industry 4.0 for Small and Medium-sized Enterprises, Friedrich Ebert Stiftung, Bonn.

Schumpeter, J. (1911): The Theory of Economic Development, Harvard University Press Cambridge.

Schwab, K. (2017): The fourth industrial revolution, Crown Business, New York.

Smart Industry, available at www.smartindustry.nl/fieldlabs, accessed 31 January 2019.

Smart Industry, available at www.smartindustryoost.nl, accessed 31 January 2019.

Smetsers, D. (2016): Smart Industry Onderzoek 2016, Report, Kamer van Koophandel, Utrecht.

Strong, E.K. (1925): Theories of selling, Jour- nal of Applied Psychology, 9, pp. 75-86.

Suominen, A., Seppänen, M. and Dedehayir, O. (2018): A bibliometric review on innovation systems and ecosystems: a research agenda, European Journal of Innovation Management (early cite).

Yankovitz, D., Kreutzer, B. and Bjacek, P. (2016): Chemical Industry Vision 2016, Report, Accenture Chemicals, New York.

Van Gils, M.J.G.M., Rutjes, F.P.J.T. (2017): Accelerating chemical start-ups in ecosystems: The need for biotopes, European Journal of Innovation Management, 20 (1), pp. 135-152.

Weber, M. (1947): The Theory of Social and Economic Organization, Oxford University Press, New York.

Whitesides, G. (2015): Reinventing chemistry, Angewandte Chemie International Edition, 54 (11), pp. 3196-3209.