Value Pricing in the Chemical Industry – Most Powerful Lever to Profitability

Abstract: The chemical industry in Europe is working hard on the improvement of their profitability base. But while innovation and complexity management are heavily discussed by the industry’s top managers, the most powerful lever to increase profitability is being ignored by many – value pricing. Arthur D. Little, jointly with Warwick Business School, conducted a pricing survey with the participation of managers from all chemical industry segments in which measures for profitability increases were investigated. Although a price increase of 1 % can lever the profit (EBIT) by 8 %, many companies focus on much weaker levers like reducing variable costs and sales volumes. In this article we look into the possible benefits of value pricing, the effective BASF approach and the problems posed by a customer management focussing on the perceived strategic importance of customers rather than their contribution margins.

Introduction

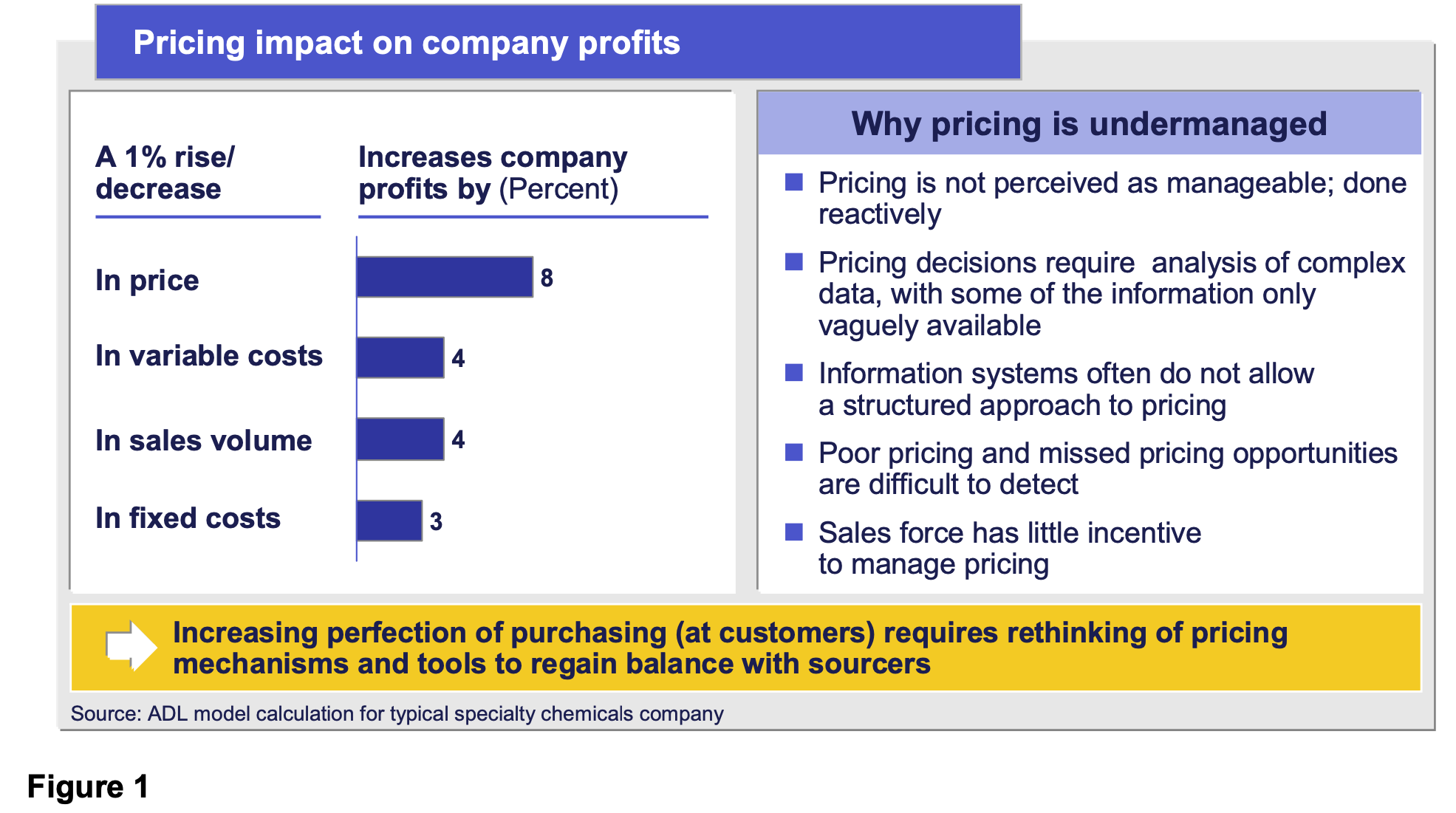

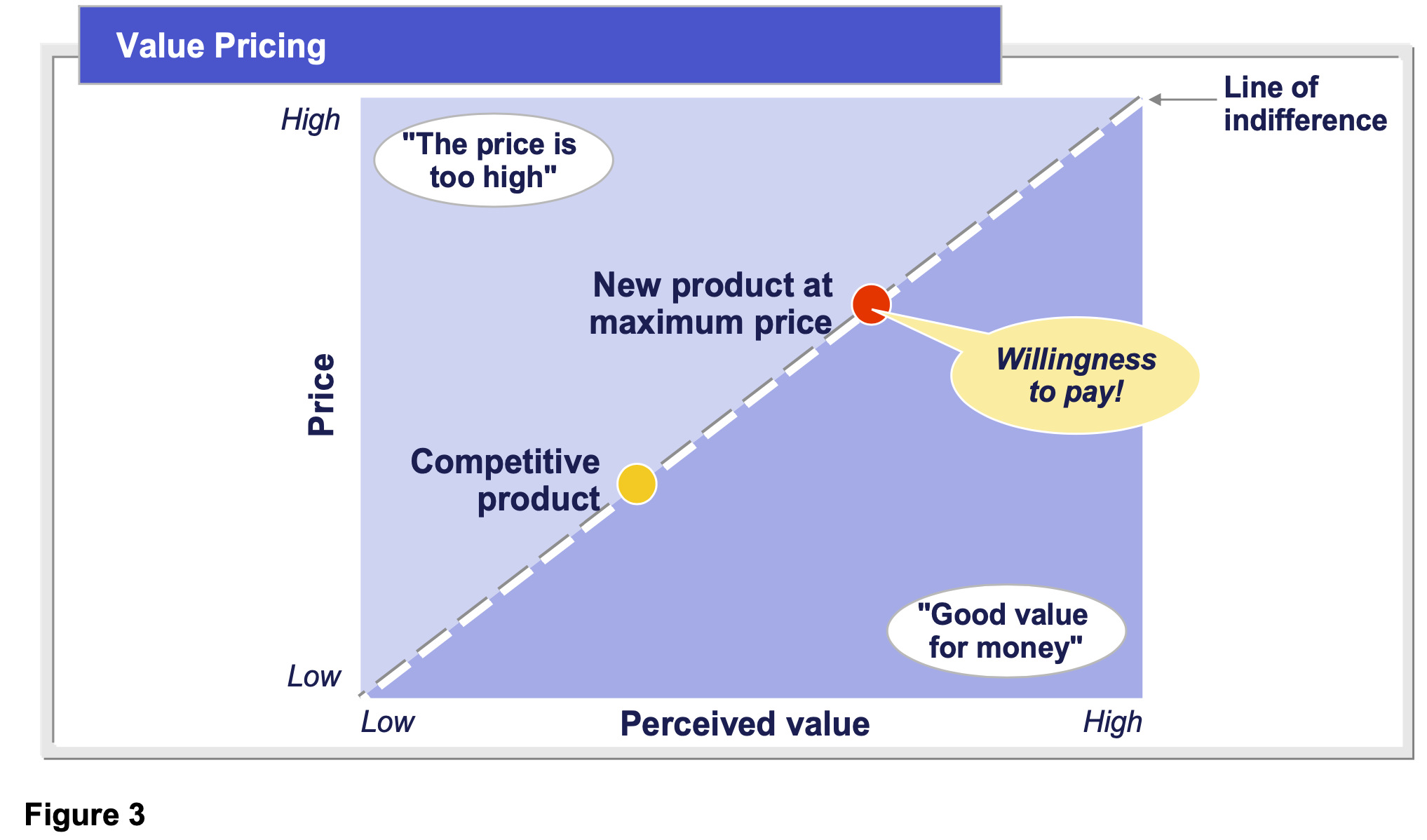

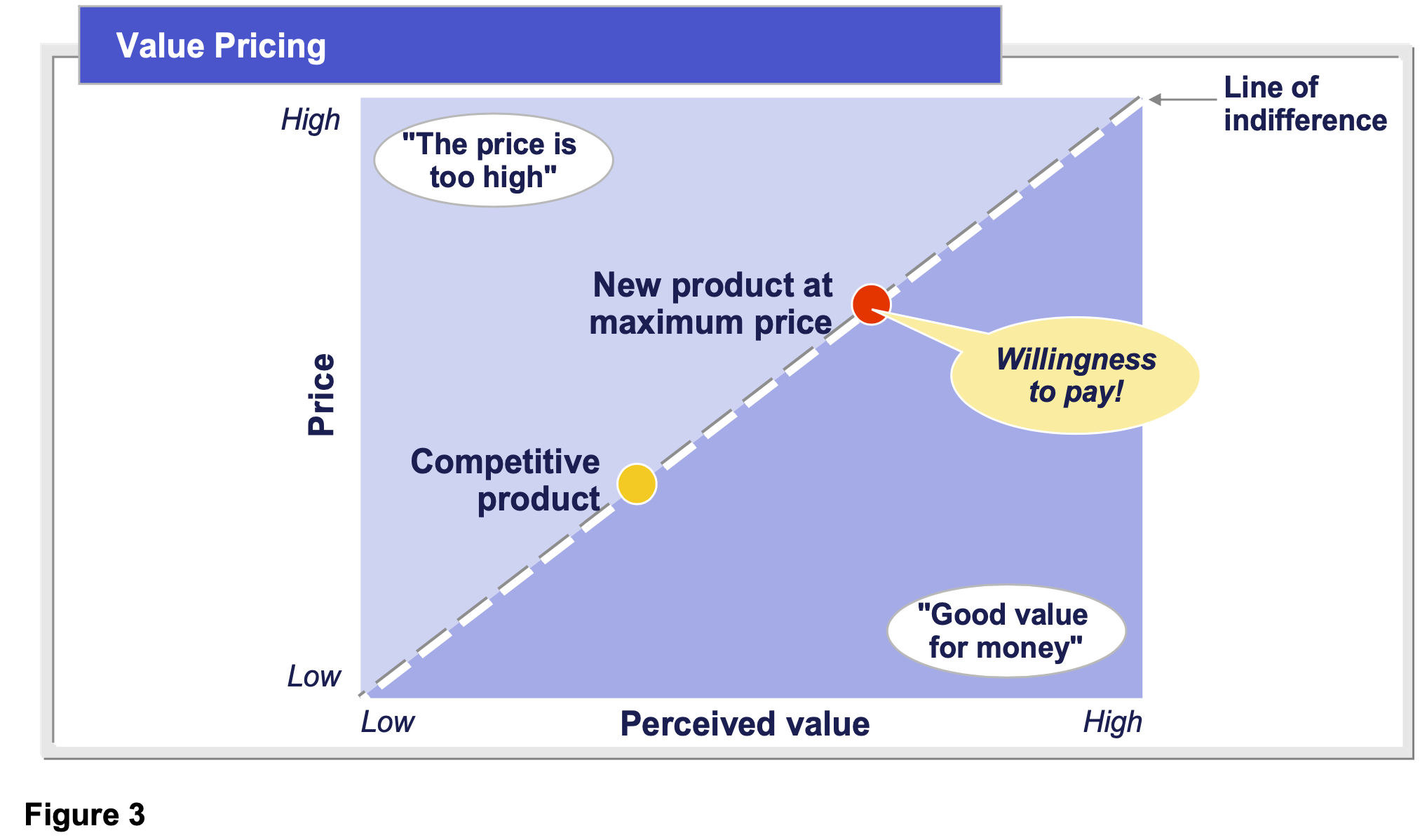

The chemical industry in Europe is facing various economic problems: long life-cycles result in margin decays, Asian competitors bring heavy price-pressure into the market and costs saving measures seem to be exhausted. However, various methods and possibilities still do exist in order to increase company’s profitability – the most important being value pricing (Figure 1). The central idea of value pricing is to measure the customers perceived value (i.e. “his willingness to pay up to X”) and to set the price accordingly. However investigation on this topic proofed that most companies in the chemical industry have no or limited professional pricing methods since pricing seems to be perceived as not manageable. This is an amazing finding, as value pricing is the most powerful lever for profitability increases.

Arthur D. Little, jointly with Warwick Business School, conducted a pricing survey with the participation of managers from all chemical industry segments in which measures for profitability increases were investigated.

The results show that managers believe innovation to be important for market success with the latest and promising trend being value based pricing. The majority of interviewees indicate that in the future customer specific contribution margins will play a more significant role. Among other interesting insights of the survey is the finding that it is not sufficient to introduce professional price finding methods in the company. The key success factor is the commitment and alignment of the top- management that will translate into sales force’s pricing rules. Overall intuitive negotiating should be avoided and a systematic and structured approach be introduced.

Innovation and pricing are the topics most discussed in the chemical industry today. Survey results give evidence for the positive sensitivity effect of professional pricing. Price increases of 1 % lever the profit (EBIT) by 8 %. Variable costs and sales volumes – being considered key performance indicators by top management – have a lesser effect: changes of 1 % lever profit (EBIT) by 4 % on average.

Bearing this in mind, it is particularly interesting that for roughly half of the interviewees pricing is not considered a top management issue, although optimised pricing could offer attractive opportunities.

On the other hand some top players have already reacted. The chemical company BASF has implemented value based pricing in the recent 2 years, now benefiting from these measures (see Appendix 2).

Charging for the Perceived Value

There is no clear picture for the pricing situation in the chemical industry: additional services such as consignment warehouses or 24- hour delivery service are often offered – but not charged. The survey confirmed that many companies have difficulties in quantifying the maximum value of a product perceived by their customers. On average, a price is determined by comparing to the relevant competitors’ prices as a reference. This can only work if the competitor accommodates professional pricing methods. Otherwise competition will suffer from orientation towards the supposed price leader. Furthermore this method distracts from an unbiased view at the strengths and advantages of the company’s own products – and this in turn means that pricing differentiators are not being charged for!

However, value based pricing should not be confused with just higher prices. It is important to understand that value based pricing charges proper prices – not just higher ones.

The Sales Force Needs a Different Incentive System

Most sales representatives in the chemical industry obtain salaries according to their sales numbers but mostly not to customer contribution margins. The survey shows that 75 % of the participating companies have an incentive system which measures sales force achievement according to their sales. Only 21 % consider the contribution margin of individual customers. This is a remarkable yet typical practice. Whereas high sales targets often justify and promote excessive price discounts, lower price limits beware (“walk-away- price”) from unprofitable decisions. But this assumes main focus at customer contribution margins. This result seems to be recognized by the participants of the survey: value pricing methods will be considered as most relevant in the sales and marketing segment (from 34 % today to 68 % in the future) followed by complexity management (from 23 % today to 55 % in the future) and price controlling (from 19% today to 54% in the future).

Three Steps on the Way: Strategic Pricing, Operational Pricing and Implementation

The question remains how companies of the chemical industry should set up pricing initiatives to achieve pricing excellence. For a successful roll- out top managers must be aligned on strategic and value pricing initiatives as well as committed to their implementation. First of all the difference between the strategic and operational project phases must be drawn. Whereas during the strategic phase it is important to ensure the buy-in of top-management and to define roles and responsibilities, the operational phase is more about implementing and imposing initiative measures in the market and in the enterprise.

The key question is which tools the sales department needs to implement and hold the newly calculated prices in the market. In any case at the initiative’s end simple and binding guidelines need to be set up for the sales force. Going operational can only work if the sales force team knows the rules and support it. Arthur D. Little developed an easy-to-use electronic tool (dashboard) that helps sales forces identify and put a price on customer value. Before programming the dashboard, a so called “price positioning statement” has to be developed. Necessary for the statement is to find out what customers want and what the maximum price for which service will be. This is similar to provoking the additional services the customer is willing to pay for. From our experience one can say that many enterprises offer services which cannot be charged. These should be eliminated from the portfolio.

Behind this complex model is a simple approach: loyal customers should be rewarded for their buying behaviour and be kept. In some cases companies should refrain from keeping unprofitable customers.

A Sensible Task – Key success factors

A price increase of 1 % not only leads to a profit increase (EBIT) by 8 % – but unfortunately this works vice versa, too. It proofed to be extremely important for a pricing excellence project to provide the right tools to the sales forces. These tools calculate the price level at which a product can be offered – below this level selling is unprofitable and should not be done. Successful pricing methods work with many dimensions: exact knowledge of customers, systematic pricing methods, binding and easy rules for the sales forces and sophisticated incentive systems.

Further Marketing and Sales Methods

So far so good – but pricing is only a module of a whole toolbox to increase profitability with respect to sales and marketing methods. Within this framework there should be other strategic methods mentioned such as value proposition, value pricing and target grouping whereas operative methods are complexity management, key account management, sales force effectiveness and transactional pricing.

Appendix 1

The pricing survey

Arthur D. Little and the Warwick Business School conducted a pricing survey with the participation of 75 Business Unit Managers, Sales and Marketing Managers of European chemical companies. The survey addressed topics such as the relevance of pricing, value pricing and transactional pricing. From the consolidation of data two main problem areas were identified being topical to the chemical industry: innovation and customer value management. While innovation serves in most cases as the answer how to maintain the current market position, customer value management is considered as a method to structure the company’s customer portfolio according to profitable and less profitable customers. Furthermore it turned out that pricing is not the most relevant agenda point of top- management, obtaining relevance only if business success remains far behind expectations.

It seems curious: 59% of the survey participants the sales departments have binding rules and guidelines for determination of prices. On the other hand 53 % of the managers feel that they are lacking customer-relevant information for their willingness-to-pay for. Even less informed are the interviewees concerning the profitability of their customers: 39% do not know sales contribution of their customers. However, the chemical industry is about to change its mind: although up to now 73 % categorize customers with respect to strategic importance and only 28 % with respect to contribution margins, the survey found that in the future 48 % of the participants will take contribution margins into stronger consideration.

Most companies offer chemical products as well as services: 82 % of the participants have additional services such as warehousing or 24- hour-delievery service in their portfolio. Critical to this picture is the finding that the willingness to pay for these services is very limited: 21 % are not willing to pay and 57 % only partly.

The conclusion from these results is that price calculation is a rather unsystematic process in many companies. As many as 59% of the respondents calculate “as the competition”, only 22 % “value oriented” and 19 % on a “cost-plus” basis. This is a remarkable finding keeping in mind that the most respondents are very conscious about the key differentiators of their own products – obviously not successfully translating them into money.

Appendix 2

Ten golden rules – from a successful pricing initiative with the BASF AG:

The BASF AG was one of the first enterprises in the chemical industry that conducted a pricing initiative very successfully. From this initiative ten golden rules were extracted:

- Visibility and engagement of top- management

- Simple and easy guidelines and principles

- Provide easy-to-use electronic tools that help the sales force identify and put a price on customer value

- Interdisciplinary project organization (sales/ marketing/ SCM/ IT)

- Exact definitions of rules and responsibilities

- Create value creation communication plan by top management

- Strengthen sales force’s role as a partner of the customer

- Align incentives for marketing and sales with pricing objectives

- Train/coach sales force in guidelines, tools and negotiation skills

Sustainably establishing value principle by organization development

Appendix 3

In the pricing diagnostic we assess areas of improvement potential along the following dimensions: pricing objectives (profit, market share etc.), current pricing practices (cost-plus etc.), value based pricing, inferring customer valuations and price sensitivities, tools used for evidence based pricing, competitive analysis and market management, incentives, knowledge management, monitoring and control systems, negotiation techniques.

Key questions to diagnose the pricing and negotiation “as is” situation are included on the next pages.

A Pricing diagnostic

- What are the company’s goals in certain segments (e.g. regain share, long term profitability, obtaining critical mass to fill capacity) and how does pricing contribute to achieving these goals?

- Is the goal realistic in view of competitive reactions? This is particularly important in low growth market segments where differentiation opportunities are relatively limited, especially given the considerable excess capacity (over 30 %).

- How to set correct pricing objectives to achieve this goal? There are typically very few companies that manage to gain market share through pricing alone. The ones that appear to be able to do so (e.g. Dell Computers) tend to have some underlying low-cost value chain that cannot be imitated by competitors.

- Analysis of current pricing practices (cost- plus, formula, list price, competitor driven, customer driven)

- Describe the typical price setting process, who is involved, what analyses are performed and which steps are sequentially taken?

- How is the effectiveness of current pricing measured?

- What is the frequency of price changes and frequency hereof?

- Value-based pricing (differentiated pricing) and inferring customer valuations

- In what way are prices differentiated over segments/ individual customers

- What does the price/ customer plot look like (and the customer profit margin/customer sales volume plot)?

- How does the company understand customers’ valuations (willingness-to-pay) and how does the company identify how these valuations differ across segments?

How does the company know how to influence/ raise that willingness to pay a price that reflects the product’s true value?

- Which lessons are learned so far from differentiated pricing?

- Do competitors differentiate their pricing towards their customers, if so how?

Evidence-based decision making

Does the company maximally extract the information from the data to estimate price elasticities (and hence optimal prices) and to extract higher prices from certain individual customers?

- What tools are used in the pricing process?

- Which data is collected to facilitate the pricing process?

- Competitive analysis and managing competition/ market management

- How does the company deal with entry threats? With price cuts by competitors?

- Which tools of analysis does the company systematically use to understand competitors’ intentions (and, as a result, e.g. avoid price instabilities) and predict competitor behavior?

- What type of competitor information does the company systematically collect to do so?

- Which tools of analysis does the company systematically use to manage competition (and to influence competitor behaviour in the company‘s favour)?

- How does Company signal its intentions to the market place?

Negotiation diagnostic

1. Alignment of company goals and incentives for sales people

- What are the incentives for sales people (what is their bonus or sales credit based upon (volume of contracts, total sales, profit margin per customer, total profit contribution, knowledge sharing on competitors/ customers/ key accounts)?

- How is sales monitored and controlled?

- Are walk away values put in place and what is the authorization procedure?

- Are these systems and procedures in line with the company’s pricing objectives?

2. Negotiation techniques

- What are some of the common pitfalls in negotiation strategy that sales people are trained to avoid?

- Conversely, do sales people get strict negotiation guidelines? If so what are some of these guidelines (to do’s)?

- Which tools do sales people use to perform an in-depth analysis of difficult sales situations (game theory, role plays, etc.) and to come up with a negotiation strategy?

- Does the preparation for a negotiation include questions like: how to set the initial offer, how to respond to an initial offer of the buyer, how to frame the negotiation in terms of the benefit of the solution one wants to sell, how to identify and how to make trade-offs?