REACH implementation costs in the Belgian food industry: A semi-qualitative study

Abstract

In this paper we discuss how companies in the Belgian food industry are affected by the REACH legislation and whether their competitiveness is weakened as a result. The study has been carried out through an extensive literature study, an electronic survey, in-depth interviews, and a case-study. No indication is observed of REACH compliance significantly hampering the competitive position of Belgian food industry. The overall cost burden seems to be relatively low. In contrast with the chemical industry, large food companies bear the highest costs,whereas the financial impact on small and medium-sized food companies remains limited.

1 Introduction

REACH concerns European legislation dealing with the Registration, Evaluation and Authorization of CHemical substances in the European Union. The main goal of REACH is an improved protection of human and environmental health within the context of sustainable development and without compromising competitive strengths of businesses subject to the legislation. The underlying principle of REACH is that companies themselves should thoroughly assess the risks of chemical substances they use, process, or store (ECA, 2008).

The regulation applies to chemical substances produced within, imported into or placed on the European market,where they are further used or sold. These substances can be pure chemical substances as such, as well as chemical substances in mixtures, e.g. in paints or inks, as well as materials in articles such as packages. Chemicals excluded from the legislation include medicines, radioactive substances or cosmetics. Chemical substances directly used in food are excluded as well (Watson, 2008).

REACH discerns between companies’ roles as regards handling the chemicals: manufacturers, importers, and downstream users. According to the role a business takes on, different obligations originate.

Manufacturers and importers have to register their substances when the production or import of these substances surpass the threshold of one tonne annually. Registration is the most important obligation within REACH and might give rise to significant costs for businesses. The registration process includes companies gathering information required to bettermanage risks with regard to chemical substances and making this information available to the authorities and to other companies. Required information may differ depending on the concerning volume and hazardous properties of the substance. Registration dead-lines differ depending on the tonnage band of the substance and its hazardous properties. Since the number of existing substances is particularly high (some 30,000 chemicals are envisioned), the registration is divided in phases over a period of eleven years. As the tonnage or the risk of the substance is higher, the deadline for registration will be earlier. New substances will have to be registered immediately when brought onto the market. Besides registration, other important obligations include authorization, notification, classification, labeling, developing Safety Data Sheets, advanced communication, etc.

Downstream users are formulators of preparations, users of chemicals in industrial processes, professional users or producers of articles. They basically buy substances from EUbased suppliers. Such companies are not required to register the substances they use, since these substances have already been registered at a particular point upstream in the supply chain. Downstreamusers’ obligations include amongst others verification of the Chemical Safety Sheets, passing on information throughout the supply chain, authorization and putting in place appropriate risk control measures (ECA, 2008; Koch, 2006).

To summarize, the European REACH legislation brings about a number of obligations. In order to meet with these obligations, companies have to incur expenses. As an example, for gathering the required information demanded by REACH, companies may need to carry out laboratory tests for which the costs may be substantial. Meeting the obligations also requires a considerable amount of administration (and its accompanying costs).

Furthermore, not only the chemicals sector may experience a strong impact of REACH, other sectors that use chemical substances may be financially affected as well. These sectors are referred to as ‘downstream sectors’. The food industry is an example of such a sector. Examining the cost impact of REACH implementation on industrial companies active in the Belgian food industry is therefore highly relevant. This study thus investigates whether the competitiveness of the Belgian food companies will not be affected by this new European regulation.

2. Approach

To obtain an understanding of the contents of REACH and its implementation implications, an extensive literature study on REACH was carried out. Furthermore, the Belgian food industry was analyzed. In-depth interviews with managers from Belgian food companies and with a representative from the Federation of the Belgian Food Industry (FEVIA) were carried out and academic and professional literature was employed to acquire a general idea of the Belgian food industry. Subsequently, a literature study on costs following the implementation of REACH in the chemical industry was performed. The costs identified for the chemicals sector were then used to obtain an apprehension of those for the food sector. At present, no information is available on aggregated REACH-related costs directly from the Belgian food industry.

To empirically assess our literature-based findings and to obtain concrete figures from the Belgian food enterprises, an electronic survey was carried out and questionnaires were send to more than 700 companies active in the food sector. In this survey, amongst other questions, companies were asked whether they were knowledgeable of REACH and whether they could identify their role under REACH (i.e., manufacturer, importer or downstream user). If these companies had already incurred any expenses in consequence of REACH, they were asked to make an indication of the size of these costs.

Afterward, a case study was carried out by means of an in-depth interview. A compliance manager from a major Belgian food company was interviewed to validate our empirical deductions and to comment on the research results.

3. Literature study

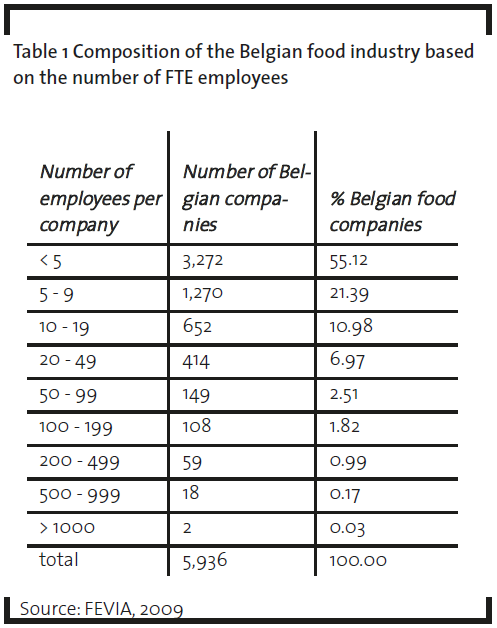

The Belgian food industry is referred to by its Federation as the “Small and Medium-sized Enterprises (SME) sector par excellence” (Bosch, 2009). A company is categorized as an SME when it employs at most 250 Full-Time Equivalent (FTE) employees and has a yearly turnover of maximum 50 million Euros. Table 1 illustrates the Belgian food industry’s composition based on the numbers of FTEs.More than 50% of the companies are so-called micro-companies that employ less than 5 employees. The number of large companies (>500 FTE) is very small. The Belgian food industry is therefore considered as an SME industry that is characterized by a very small amount of large companies (Bosch, 2009, De Schutter & Kielemoes, 2007).

In 2007 a total turnover of 36,931 million Euros was generated in the Belgian food sector (FEVIA, 2009). Approximately half of this turnover was generated on the Belgian market and the other half was generated by export. Approximately two third of the export is sent to France (21.7%), the Netherlands (19.3%), Germany (14.7%) and the United Kingdom(11.0%). A total of 85% of the export is intra EU while only 15% is destined for the rest of the world. The most important destinations outside Europe are Russia, the US and Japan. Given that REACH creates a disadvantage only for those companies that export to countries outside the EU, this disadvantage thus only applies to the 15% of the food companies exporting to non-EU countries (and consequently at first glance only these plants may suffer from a weakened competitiveness).

As already mentioned, chemical substances used in food are in general excluded from REACH. Companies that use these chemical substances for non-food purposes can however be subject to the legislation, for example when a certain production process creates a by-product of which the destination is a nonfood purpose or when one certain substance can simply be used for various purposes. Chemicals may for example be detergents for cleaning machines or lubricants for smearing machines. Packaging may also contain chemical substances.

It should be noted that until present a very limited amount of costs has already been made by food companies due to REACH. Actual costs will thus become ever more transparent during the next decade as the registration deadlines for the different categories (amounts of chemicals processed, used, imported, etc.) stipulated by REACH will fall successively. In order to estimate the extent of the costs resulting from REACH, a list of potential costs was made up (using the chemical industry as a guiding sector). Costs arise when manufacturers and importers meet their registration and other obligations. They can be divided in three categories: direct, indirect and hidden costs. Direct costs are a result of gathering required information, testing, administration or they result from rationalizing the product portfolio. The most important costs directly related to registration are laboratory test costs. In the case where not all required information is present, tests may have to be carried out to acquire all the necessary data. Costs for these tests may be considerable. For this reason, companies often form consortiums. This brings about a number of advantages, yet it is not obligatory. In such consortiums, companies may jointly perform certain tests and therefore split certain high costs among the various members. Furthermore, given that companies do various tests together, these tests have to be done only once and double testing is avoided since companies can share the obtained results. In case of testing on animals it is even compulsory by REACH to avoid double testing. The formation and management of these consortiums is an example of indirect costs that may arise. Other indirect costs include personnel training and increased communication with customers and suppliers (Heughebaert, 2008).

Rationalization of the product portfolio may occur for two reasons. First, it is possible that the authorities encounter certain substances as too risky or too dangerous for human and environmental health. Consequently, these substances may no longer be authorized, and as a result companies producing or importing these substances may no longer be permitted to do so. If this is the case for a company, rationalization of its product portfolio is obligatory. Second, it is possible that certain companies evaluate the registration costs as too high. These companies doubt the profitability of continuing to produce or to import these substances. In this case, the companies themselves choose to no longer produce or import the substance. Rationalization leads to high costs for the former importers or manufacturers because these have to cut parts of their portfolio or substitute these substances in their products for tolerated (authorized) alternatives which requires considerable time and money for research. (Van Gennip & Van Geel, 2004; Angerer et al., 2008; Danneels, 2009).

Hidden costs are for example increased costs for managing suppliers, replacement of critical substances or rationalization of the supplier base.

In the Belgian food industry, we are obviously mainly interested in downstream user costs. Although downstream users might not need to register any substances and therefore avoid the significant registration costs, due to REACH compliance, they may be confronted with increased costs due to the various obligations they do have to meet. Potential costs may arise due to administration, increased communication, and drawing Safety Data Sheets. Other important costs for downstream users may arise in case their suppliers rationalize their product portfolio. In case this rationalization is decided by the supplier himself and not imposed by the authorities, downstream users may have to find and negotiate with (new) suppliers still delivering the desired chemical substance(s). Converting to new suppliers often demands significant investigation and thus requires a considerable amount of resources. In case of rationalization is indeed enforced, downstream users will need to reconsider product designs that contain substances that are no longer authorized. They either need to substitute such unauthorized substances for other substances that are still permitted, or they have to completely eliminate them from the design. Redesigning products may require a considerable amount of research resources, being a time and money-consuming activity. Furthermore, such research implies a large part of the budget for R&D to be taken up for this purpose, and hence fewer resources are available for R&D, e.g. in function of innovation. The impact of REACH implementation on innovation is however not unambiguous, because it incites innovation as well by delivering an incentive for cost-reducing alternatives (Wolf & Delgado, 2003). Downstream users may furthermore be confronted with increased prices for chemicals if suppliers roll of a great share of their increased costs on their customers. They will be more willing to bear higher prices than to switch over to suppliers outside the EU who are not confronted with higher costs due to registration. If they would switch over, they would then no longer be downstream users but importers and would have to incur the high registration costs themselves (EC, 2002; Maeckelberghe, 2009).

Moreover, companies not complying with REACH obligations risk being heavily fined. In Belgium, fines may be monetary penalties amounting up to 4,000,000 Euros in case of a major offense and up to 1,200,000 Euros in case of a minor offense, or they may translate into custodial sanctions for company CEOs (Hamblok, 2009).

An obvious conclusion of our literature study is that REACH-induced costs may influence the competitiveness of Belgian food companies. Competitiveness is determined by whether the costs made by a company are competitive compared to its competitors as well as by its product portfolio (and thus indirectly by e.g. innovation). To study the impact of REACH on organizations’ competitiveness, a distinction needs to be made between large companies and SMEs and between whether the destination of the export is intra- or extra- EU.

REACH pressure on company competitiveness is not evenly distributed among the companies. Observing REACH implementation in the chemicals sector, small and medium-sized enterprises experience a far stronger pressure on their competitive positions compared to large companies: large chemical companies produce or import large quantities of substances and costs can be spread over much larger volumes. SMEs often produce or import a larger variety of chemical products in somewhat smaller quantities (although generally still surpassing the 1 tonne per year tier). Consequently, large companies are able to obtain much lower costs per tonne than SMEs.

Furthermore, a distinction must be made between intra-EU or extra-EU export. On the one hand, REACH discourages extra-EU export, since those companies selling their products on the global market will no longer be able to compete with non-EU companies on that market. Two arguments explain this observation: (i) importers or manufacturers within the EU facing test and registration costs may roll off their increased costs on their customers leaving these companies with a competitive disadvantage compared with non-EU competitors, and (ii) the manufacturers and importers themselves suffer lower profit margins compared with non-EU competitors. On the other hand, REACH favors intra-EU export, since European companies buying chemical substances or products containing chemicals will prefer to buy these products from suppliers within the EU this way avoiding registration costs. Hence, REACH can be considered as a technical trade barrier that enforces competitiveness amongst European companies selling products on the European market.

In the chemicals sector, only 23% of chemicals sales are exported outside of the EU area (Cefic, 2009). The EU chemical industry comprises 29,000 enterprises, 96% of which have less than 250 employees and may be considered as SMEs. Only 4% of the EU enterprises employ more than 249 employees and generate 72% of total chemicals sales. Most of the chemical companies are thus SME downstream users.

In the chemical industry, REACH frustrates the competitive position of SMEs compared to the competitive position of large companies due to the costs per tonne. Although not as high volumes of chemical substances are produced or imported by chemical SMEs compared with large chemical enterprises, most of these companies produce or import a diversity of substances with relatively high amounts, and are therefore immediately subject to registration and REACH regulations for each of these substances. Thus, registration costs due to REACH implementation in the chemicals industrial sector are distributed over a large number of companies. The question arises whether the same conclusions can be drawn with respect to the Belgian food industry.

4. Empirical research

4.1. Survey

An e-survey was sent to 712 companies active in the Belgian food industry. Companies were asked to indicate their role with relation to REACH. In case a respondent indicated to be a downstream user, he was also asked identifying the company’s suppliers. Respondents were furthermore asked whether their companies complied with all REACH obligations at the moment of filling in the questionnaire, and, if not so, to indicate which obligations they did not comply with. Companies were asked for their REACH related costs, to give an indication of the nature of these expenses and to quantify them. The questionnaire was sent out in February 2009 and the deadline for filling in the e-survey was set on the end of April 2009. A response rate of approximately 4.5% was obtained. This is an acceptable rate given the fact that response rates for academic studies have been known to show a general decline in recent years (Griffis et al., 2003).

To limit the workload for the respondents (and also to increase the response rate of the survey), the selected companies were asked to identify a single informant. Checking his/her function within the company validated the competence of this informant. For more information and suggestions on selecting key informants, reference is given to Kumar et al. (Kumar et al., 1993). In our survey, respondents can be considered to be sufficiently knowledgeable such that the results are not tainted by informant bias: all respondents indicated to be either compliance managers or environmental managers.

A mix of large companies and small and medium-sized enterprises responded to the survey. As regards company activity types (i.e., breweries, bakeries, milk producing companies, candy producing plants, meat enterprises, chocolate companies, etc.), the participating plants also have a very diverse product portfolio. The representativeness of the sample can therefore be regarded as sound.

As regards the participating companies’ roles under REACH, 9.1% of the respondents were upstream users (manufacturer or importer), whereas 42.4% were downstream users. One third of the respondents (33.3%) either were not subject to REACH at all, or were unaware of these regulations. Apparently, 15.1% of the participating food companies explicitly mentioned to be ignorant as regards REACH. These figures are comparable with our observations in the chemical industry, where the largest group consists of downstream users as well (Danneels, 2009). It should however be noticed that within the food industry the amounts or the range of chemical products are usually rather limited (and generally lower than the 1 tonne per year tier, hence leading to non-exposure to REACH compliance).

Companies were further asked to give an indication of the costs they already made or they were expecting to make due to REACH implementation. Upstream user estimations range between 100,000 Euros and 300,000 Euros yearly.

Downstream users assessed their REACH implementation costs to amount to maximum 2,500 Euros yearly. As mentioned before, downstream users may however be confronted with significant costs in case their suppliers rationalize their product portfolio. From the survey it is obvious that food companies consider this possibility as very unlikely. The reason for this stems from the fact that chemical substances used in food and beverages are very unlikely to be considered as risky and therefore will (most likely) not be forbidden in the future. Hence, suppliers of downstream users will probably not be confronted with forced rationalization.

Using the survey results for manufacturers or importers and for downstream users, total cost impact for the Belgian food industry is estimated. To this end, manufacturing or importing companies’ estimated costs are aggregated and are added to the estimated aggregated costs for downstream users in the Belgian food industry. In this industry, 5,936 companies are active (FEVIA, 2009). Based on our empirical results, we estimate some 540 companies are upstream users and thus need to register. This is a conservative estimate, since a number of food companies are not yet aware of REACH and of their role in this new legislation. The total costs for this small upstream user group will then vary between 54 and 162 million Euros yearly. The survey results further indicate 42.4% of the food companies are downstream users. Total costs for downstream users can therefore conservatively be calculated to approximately 6.3 million Euros. Total cost impact of REACH implementation for the Belgian food industry can thus conservatively be estimated to vary between 60.3 and 168.3 million Euros yearly.

Furthermore, the Belgian food industry generates an annual average turnover of 36,931 million Euros. Hence, REACH implementation costs represent 0.1% to 0.5% of total turnover of the Belgian food sector. Angerer et al. (2008) indicate that in the chemicals industry, REACH costs amount to approximately 0.13% of total turnover.

In both the chemical industry and the food industry, costs thus remain rather limited compared with total turnover. However, there is a difference between both industrial sectors: unlike in the chemical industry, the spread of the costs in the foods sector is highly uneven. A large part of total costs is borne by a very small group of food companies requiring to register, whereas a very small part of total costs is carried by a large group of downstream users. Large food companies fall mostly into the category of manufacturer or importer, experiencing the strongest pressure. Food downstream users are mostly SMEs for which the impact remains limited. The latter observations are in contrast with the chemical industry, for which mostly the SMEs experience a large pressure on their competitive position and are sometimes no longer able to compete with the larger companies.

Furthermore, given that REACH favors intra- EU export and discourages extra-EU export and given that only 15% of Belgian export is extra-EU, the competitiveness impact of REACH on food companies remains limited in this regard as well. Once again, the large companies are globally active and export extra-EU, thus face possible negative impacts on their competitive position.

It follows thus from the empirical data that REACH affects the food industry in a fundamentally different way than it affects the chemical industry. To evaluate and to interprete these findings, a case-study in a major Belgian food enterprise was carried out.

4.2. Case-study

One of the respondents of the e-survey was the compliance manager of Citrique Belge, an upstream user company belonging to the Belgian food industry. He welcomed an in-depth interview in which costs and implications of REACH could be discussed. As an instructive document for the interview, a list of guiding questions was prepared in advance.

Citrique Belge is one of the worlds’ largest manufacturers of citric acid and produces approximately 100,000 tonnes of citric acid every year. Consequently, the company falls within REACH’s highest tonnage category and is subjected to registration requirements. In case of Citrique Belge, the registration deadline was November 30th, 2007.

REACH-related estimated costs for Citrique Belge are divided into direct, indirect and hidden costs. This company was formally part of a larger multinational company, Hoffman-La Roche, which executed toxicity studies and exposure safety studies. Meanwhile, the company has been taken over by DSM, a chemical multinational, which is now the parent company of Citrique Belge. Due to its past, the company did not have to incur expenses for testing. Compared with other food companies requiring to register, this may be considered as an exceptional situation in which Citrique Belge is able to avoid significant costs.

As indicated in section 3, companies take part in consortia in order to cut costs. For this reason, Citrique Belge founded a consortium for citric acid. The consortium consists of a limited number of manufacturers of citric acid. Citrique Belge does not have complete knowledge about REACH and has therefore hired consultants to lead the consortium. The costs to the company for further developing the consortium is estimated to amount to 25,000 Euros yearly.

Indirect costs made by Citrique Belge are for instance costs to inventorize all the substances followed by the identification of substances that need to be registered. These costs are borne by the parent company DSM. Citrique Belge did establish essential systems and procedures for REACH itself and gathered the data required for preregistration. This required a considerable amount of personnel costs (via personnel time). Other indirect costs follow from the required adaptation of Safety Data Sheets.

Citrique Belge assumes that all suppliers will register their products and that authorization for citric acid and its components is unnecessary. In this scenario none of the substances of Citrique Belge needs to be substituted. Hidden costs are thus estimated to remain zero.

Total costs are estimated by the company to range between 100,000 and 200,000 Euros yearly until the deadline expires on 30 November 2010. REACH related costs thus possibly amount to maximum 600,000 Euros in total for Citrique Belge.

The compliance manager of Citrique Belge further recognized our empirical findings on REACH implications in the Belgian food industry and fully agreed with them. Additionally, he emphasizes there is a lot of room for interpretation of REACH legislation and it appears that various parties are insufficiently informed. The company’s representative, therefore, recommends that REACH communication between all stakeholders (companies, authorities, etc.) is substantially improved.

5. Conclusions

REACH is often considered as novel European legislation only applying to the chemical industry. Although mainly the chemicals sector is indeed subject to it, REACH should also be followed up by other industries using chemical substances (mainly in downstream activities), e.g. the food industry. Downstream companies frequently wrongfully assume that they have no connection to REACH whatsoever, despite using e.g. products containing chemical substances, detergents, etc.

A survey in the Belgian food sector clearly confirms the need for further communication about the existence and the importance of REACH to downstream sectors.

The impact of REACH implementation on the Belgian food industry cannot be compared with its impact on the chemical industry. As opposed to the chemicals sector, in the food sector a very limited number of companies bears nearly all costs and an overwhelming majority of companies, the downstream users, bears little costs. A number of downstream users even indicates to make no expenses at all. This is however unlikely and possibly due to the fact that these companies are not sufficiently aware of their REACH obligations. An in-depth interview with the compliance manager of a major Belgian food company backs up our empirical conclusions and indicates an urgent need to enhance REACH awareness and knowledge amongst downstream user sectors.

Acknowledgements

The authors are grateful to all managers who were willing to collaborate with this action-oriented academic research. Their cooperation is very much appreciated and acknowledged.

References

Angerer, G, Nordbeck, R., and Sartorius, C. (2008): Impacts on industry of Europe’s emerging chemicals policy REACh, J. Environ. Manag., 86, p. 636–647.

Bosch, C (2008): REACH in the Belgian food industry, Interview with Secretary General FEVIA, 21/11/2008.

Danneels, D. (2009): Comparison cost models chemical sector and food industry, Interview with REACH Initiative Director Honeywell, 20/05/2009.

De Schutter, B. and Kielemoes, J. (2007): Integrale milieuanalyse Vlaamse voedingsnijverheid, available at: http://www.lne.be/doelgroepen/bedrijven/document en-en-fotos/IMA%20voeding%202007.pdf

ECA (European Chemicals Agency) (2008): available at http://echa.europa.eu/

EC, Final Report Prepared for European Commission Enterprise Directorate-General (2002): Assessment of the business impact of new regulations in the chemicals sector, available at: http://chemicalspolicy.org/downloads/RPAreport.pdf

FEVIA (Federation of the Belgian Food Industry) (2009), Facts and Figures, available at: http://www.fevia.be/ pages/default.asp

Griffis, S.E., Goldsby, T.J. and Cooper, M. (2003): Web-based and mail surveys: a comparison of response, data, and cost, J. Business Logist., 24(2), p. 237-258.

Hamblok, E. (2009): Costs and impact of REACH on industry, Interview with Environmental Consultant SGS Belgium NV, 13/02/2009.

Heughebaert, L. (2008) Costs due to REACH, Interview with VLARIP project leader Essencia, 5/12/2008.

Koch, L. and Ashford, N. (2006): Rethinking the role of information in chemicals policy: implications for TSCA and REACH, J. Cleaner Prod., 14, p. 31-46.

Kumar, N., Stern, L., and Anderson, J. (1993): Conducting interorganizational research using key informants, Academy of Management Journal, 36(6), p. 1633-1651.

Maeckelberghe, I. (2009): Impact REACH on downstream users, Interview with environment coordinator Baronie Chocolates Belgium NV., 14/01/2009.

Van Gennip, K. and Van Geel, P. (2004): EU2004REACH: Overview of 36 studies on the impact of the new EU chemicals policy (REACH) on society and business, den Haag, available at http://www.eu2004-reach.nl/

Watson, E. (2008): REACH chemicals Regulation catches ingredients suppliers on the hop, available at http://www.foodmanufacture.co.uk/news/fullstory.php/aid/6242/REACH_chemicals_Regulation_catches_ingredients_suppliers_on_the_hop.html

Wolf, O and Delgado, L. (2003): The impact of REACH on innovation in the chemical industry, available at http://www.eu2004-reach.nl/downloads/03-EC%20JRC%20and%20IPTS%20innovation_analysis_final.pdf