Innovation Strategies for the Australian Chemical Industry

Abstract: The Australian chemical industry is facing a testing period as it adjusts to the challenges of the new global era. This paper briefly traces the evolution of the industry through an extended period behind protective tariff barriers to the situation today, as it confronts the new competitive environment. While the industry is adjusting as new companies emerge and specialist export-oriented production increases, the cur- rent situation continues as “work in progress”. We argue that its future success will depend on its ability to innovate and to renew itself. We draw some generic lessons from a review of successful innovation in the Australian chemical industry and identify four key strategies for companies namely: (1) working within exist- ing global value chains, (2) engaging with other globally focused industries, (3) developing an integrated pack- aging concept for their products and services, and (4) leveraging the knowledge of others.

Introduction

The central role of the chemical industry in the economic and social fabric of most advanced economies has been demonstrated over the past 150 years. Over that time the industry has been continuously transformed by the introduction of product and process innovations largely driven by research and development conducted by corpora- tions, universities and national laboratories. The industry produces over 70,000 different chemical substances valued at over USD 1.5 trillion per an- num [1]. In more recent times the industry has faced some serious problems with the evolution of global markets, the growth in regulatory controls, the slowing down of innovation as exhibited in diminishing returns to R&D, and skills shortages [2].

Arora et al. have highlighted the role of science in the productivity and growth of the chemical in- dustry in Europe, the United States and Japan [3], the changes in the industry brought about by li- censing of patent protected technology [4], the changing division of labour and emerging markets for technology in the chemical industry [5]. Arora et al. described the massive restructuring that took place in the US chemical industry in the 1980’s (well in advance of Europe or Japan) and which contributed to improved results in many US chemical firms. In particular, these authors noted the division of “innovative” labour and the devel- opment of wide networks of collaboration preva- lent in the new and emerging areas of the chemical industry in contrast to the activities of the large- scale basic ‘commodities-type’ chemical industry. Both of these factors are important as the Austra- lian chemical industry makes readjustments to market deregulation. In addition to the work of Arora et al., other literature has also addressed the importance of large scale production [6], and the increasing rise of licensing activity [7]. Very re- cently, Swift [8] reviewed the near-term business environment in which the world industry will op- erate and the prospects and challenges to be faced in 2006 and 2007.

In addition, there have been a number of re- ports addressing some of the problems facing the industry at the level of national concern:

- In the European Union [9, 10] the frequency for innovative opportunities has been a major concern along with the issue of the number of newly banned chemicals. Harries-Rees [11] has suggested that there has been a shift towards short- and medium-term customer and market driven incremental changes in products and processes in the European industry, with higher risk longer-term activities have been handled in a variety of individualistic ways in different companies – motivated by “getting the balance right” between the short/medium- and long-term activities. In addition, interna- tional collaboration at the research level, and the movement of people and ideas within the industry, has occurred [11].

- In the USA two reviews [12, 13], and the es- tablishment of the industry-led Chemistry In- dustry Vision 2020 [14] with a strong emphasis on energy efficiency and protection of the en- vironment and more recently on environ- mental and health impacts of nano-materials [15].

- In the UK [16], Japan [17], and Denmark [18], where energy savings emerge as a princi- ple issue.

Whatever the commentary, the fact is that each company working in the chemical industry must chart its own innovation strategy in such a way that exploits its key strengths and the opportuni- ties that are available to it. This may take a variety of forms. Innovation may be technological – in the form of new products, or processes-or non- technological – e. g., in the form of new services or organisational arrangements as described by Tidd et al. [19]. Moreover, increasingly it is likely to involve others outside the company for ways to develop and exploit ideas, as Chesborough con- vincingly argues [20]. Nonetheless, the envelope of strategies that are available for countries will differ according to different national innovation systems, including consideration of the nations’ resource endowments, the company base and the links with international companies, and the particular regula- tory settings in which they function.

What is the Chemical Industry?

We follow a structure of the chemical industry as defined by the international Standard Industry Classification (SIC) codes, which are used for data collection on the industry. Although the code systems used from nation to nation are marginally different, in general, the chemical industry embraces the manufacture of basic chemicals (including chemicals derived from coal and/or oil), other chemical products (including medicinal and pharmaceutical products), rubber and plastic (or polymer) products. In most cases the industry includes all products derived from petroleum refining [21]. We have also included consideration of biotechnology since much of the activity in this area in Australia is directed towards R&D on pharmaceuticals.

Impact of Change on the Australian Chemical Industry

The Australian chemical industry has also faced testing times in confronting the challenges posed by globalisation and the changing patterns of production and trade. Even though the Australian industry is enmeshed with the global chemical industry, its companies face a different set of challenges and opportunities. In particular it needs to rethink its prospects, and the role of innovation. For many years the industry was protected from external competition by high tariff barriers and restrictions to trade. With the liberalisation of world markets and the substantial lowering of tariffs, the future success of the industry in Australia will depend on its capacity to change through innovation, to introduce competitive new and innovative products, processes and services, and meet the demands of both existing and new markets.

Although the Australian industry is not large on a world scale, it plays an important role in the na- tional economy and is integrated with the global industry through the presence of multinational companies and the trade in chemicals. The Australian industry is important in several niche areas, for example, explosives, pharmaceuticals and agricul- tural chemicals. It has also benefited from a strong publicly funded research system. At the same time the industry continues to undergo the pains of ad- justment as sectors hitherto protected by tariff barriers face new tough competition from overseas. The industry will need to continue to change in the years ahead.

To this end the Australian government in consultation with industry recently released two reports (Chemical and Plastics Action Agenda [22] and Pharmaceuticals Industry Action Agenda [23]. These reports set out industry goals and suggested actions in areas such as regulatory reform, invest- ment and reinvestment in growth, in an attempt to ensure that a highly skilled workforce is available [22]; that Australia is positioned as a global pharmaceuticals hub; that a globally competitive operating environment is created; and that the ability to commercialise research by investing in skills, and by fostering a positive culture, image and profile for growth is strengthened [23].

The Action Agendas reflect current industry policy thinking in Australia, namely that govern- ment can contribute best by removing regulatory impediments, promoting the flow of information and skills, and ensuring that the public infrastruc- ture permits competitive companies to emerge. Since the early 1980s there has been a distinct shift in government, away from programs of selective support for industry, and little to no sympathy for “picking winners”.

While the Action Agendas have paid attention to the importance of international competitiveness in the industry they fall short in exploring in detail any of the strategies that may be available to the industry at large to innovate, and thus achieve a more competitive position. This paper addresses these issues in more detail, but first reviews the external and internal setting of the Australian chemicals industry and the factors that have shaped its development.

Methodology

We have adopted an inductive, comparative case study approach to theory development [24]. This permitted new factors to be examined as they emerged while also allowing patterns to be compared and contrasted across the cases. The case studies involved personal interviews by at least one of the researchers with senior personnel in each company, following a prescribed systematic format, which specifically addressed the circum- stances relating to the development and implementation of their innovation(s), but also permitted some flexibility in the discussions. In total we have conducted case studies on over 25 companies working in the chemicals sector. The choice of the case study approach was also motivated by our in- terest in developing a consistent framework to embrace the innovation activities of these compa- nies over time, and to monitor the achievements for a wide range of emerging Australian science and engineering based companies working in the chemical industry [25]. Several of the case studies have also formed the basis for a series of detailed industry profiles to inform specialists working in the chemical/biotechnology sector [26]. It is also important to note that many of the newer compa- nies reported in this paper may be characterised as having advanced technology products developed from the R&D base, and supported by strong in- tellectual property protection.

The historical setting for the Australian chemi- cal industry as a whole has been well documented by Kolm [27].

In addition to the case study approach we have analysed some of the dynamics of change within the industry sector by examining the National Ac- counts (the industry input-output statistics) avail- able for Australia and a number of other countries (the latter are not discussed) over the period of fif- teen years from 1983-84 to 1998-99 [28]. While the present analysis is preliminary, it serves to amplify the enormous changes that have occurred in the chemical industry sector, especially over the period involving the sector’s radical transformation through opening up the economy to international competition and globalisation.

Strategic Setting

Evolution of the Chemical Industry in Australia

The chemical industry in Australia has its ori- gins in the nineteenth century. Chemical manufac- turing was initially directed towards meeting the needs of new colonies, and to support its resource- based industries [27]. Fertilisers were needed for Australia’s nutrient-poor farmland, explosives for its mines, and processing chemicals to treat its mineral ores. The high cost of international freight meant that it was more economic to manufacture chemicals locally and a small but growing domestic manufacturing base emerged.

The focus on local markets continued well into the twentieth century, supported by the high tariff walls and licensing arrangements that applied to the manufacturing sector. This situation prevailed after the Second World War when government policies supported growing “infant industries”. From the 1950s a number of multinational com- panies entered Australia’s manufacturing sector, and expanded the ranks of the Australian chemical industry, which consisted of a large number of small and medium sized companies and just a few sizeable companies such as the diversified chemi- cal producer ICI Australia (now Orica), Faulding Pharmaceuticals, which is now part of the Mayne Group and Nicholas (Aspirin), which is now owned by Bayer.

While manufacturing tariff protection provided a cushion for the Australian chemical industry and secured local markets, it retarded innovation, ex- pansion and export seeking growth. There were also no government incentives for innovation- based exporting companies. A leading example is the integrated petrochemical complex established in Victoria in 1961 by a consortium of seven com- panies, Mobil, Exxon, Dow Chemicals, Union Carbide, BFGoodrich, BASF and Hoechst. It was built to process the oil findings from Bass Strait and produce synthetic resins and chemicals. While the plant operated efficiently in the tariff protected environment it remained small scale by world standards. The failure to expand the plant to world scale and compete internationally meant it became uneconomic when tariffs were eventually reduced.

In the 1980s the Australian government com- menced a series of reforms to deregulate the econ- omy and reduce tariffs. The 1986 recommenda- tions of the Industries Assistance Commission were adopted and tariff barriers for the chemical industry progressively decreased from levels as high as 45 % to between zero and 5 % by 1996. The tariff reductions were inevitably accompanied by increased imports. Further, the industry had to deal with the problem of aging assets and sub-scale plants and find ways to access international mar- kets. Today the industry continues to restructure to meet the demands of global competition.

Some companies continue to be in the throes of adjustment, while others have made the transition with some success. On the positive side, a number of new, “born-global” companies have been formed across parts of the industry [29].

The Australian Chemical Industry Today

The chemical industry accounts for about 12 % of total manufacturing in Australia, with a turnover of about AUD 28 billion (1999-2000) and employs over 91,000 people [23]. In 1999-2000, AUD 4.5 billion worth of chemical products were exported and AUD 15.1 billion of chemical prod- ucts imported – a net deficit of over AUD 10 billion. Australia accounts for only about 1 % of world chemical production and is clearly a significant net importer of chemicals. There are some 3,800 enterprises operating across the full spectrum of the chemical industry. More than 80 % of these are small and medium-sized busi- nesses, each employing less than 200 people. The Australian industry is also geographically dis- persed, with activity spread across the States of Victoria (38 %), New South Wales (34 %), Queen- sland (12 %), South Australia (7 %), Western Aus- tralia (7 %), and Tasmania (2 %).

The industry is extensively linked to the global chemical industry as well as most of the major ‘big pharma’ pharmaceutical houses., through interna- tional trade and the operations of several multina- tional companies such as DuPont, Dow Chemical, Huntsman, Pfizer, Exxon Chemicals, Merck, Pharmacia, Bristol Myers-Squibb, Eli Lilly, Wyeth, Schering Plough, Bayer, BASF, Sanofi-Aventis, Degussa, and Boehringer-Ingelheim. There are just a few large local companies such as CSL, Orica, Nufarm, and Incitec.

The amount spent on research and develop- ment by the chemical industry in Australia is not large by international standards AUD 584 million in 2003-04 [30]. Of the top 50 R&D performing business spenders in 2002-03, 14 were in the chemicals sector. These companies spent over AUD 275 million on R&D in 2002-2003, with the biomedical/chemical company CSL Ltd being the leading performer spending more than AUD 90 million per annum [31]. In the related biotechnology sector the total R&D expenditure was AUD 378 million. Most of the multinational companies conduct R&D in Australia – indeed pharmaceutical multinationals rank in the top 50 business spenders on R&D, but the expenditures of the multinational companies are just a small fraction of their global budgets.

An offsetting factor is the expenditure on R&D by the public sector through universities, and re- search institutions such as CSIRO and State agen- cies. Australia has high public spending on R&D across all the manufacturing sectors. The strong research base is reflected in Australia’s position of 15th in an international ranking of chemical publi- cations with 15,682 papers published in the decade to August 2004 [32]. In addition, the medical and health related research provides a platform of sup- port for the local chemical industry. In 2002-2003 Australia public funded expenditure on the chemi- cal, biological and medical and health sciences was AUD 3.15 billion.

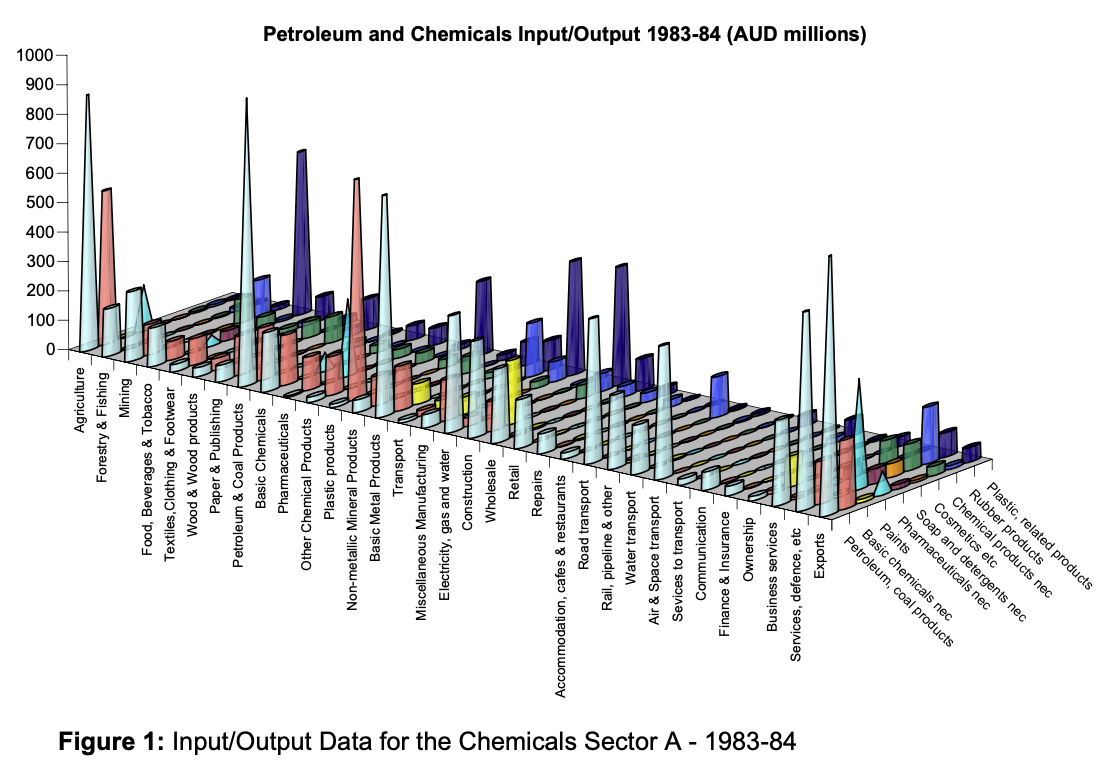

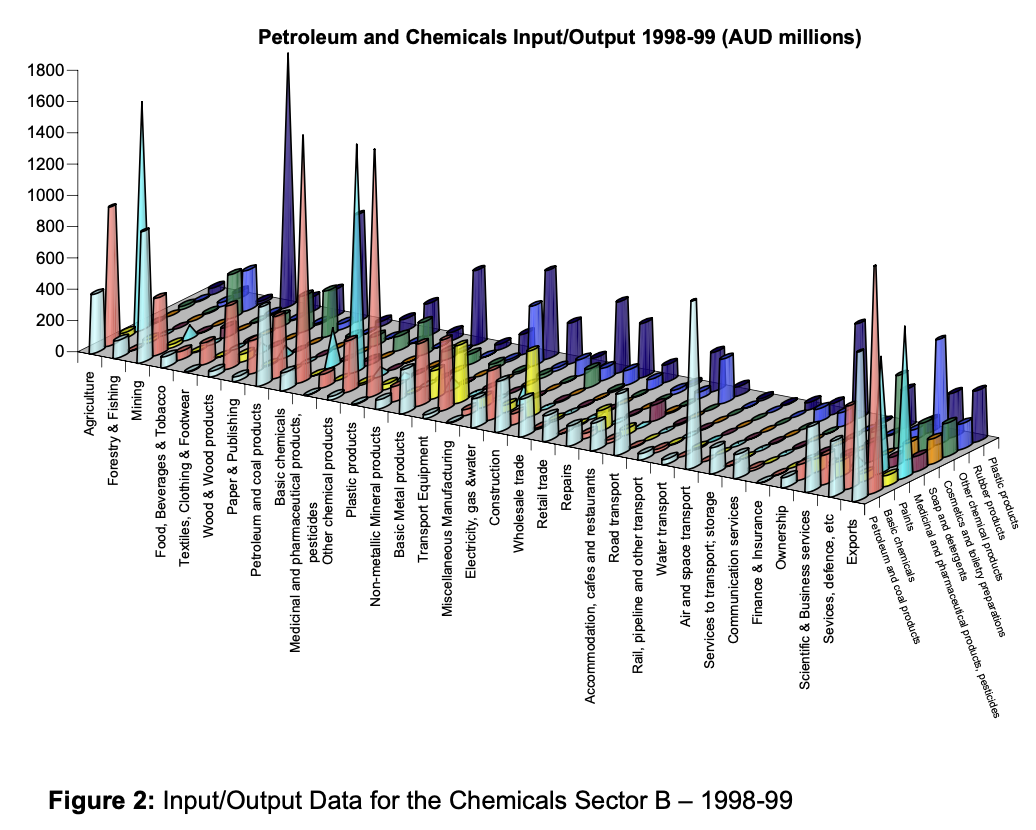

To illustrate how the chemical industry in Aus- tralia has evolved over the past two decades we compare data from the Australian National Ac- counts for 1983-84 with that of data for 1998-99, namely a gap of some 15 years, and one embracing the critical changes in micro-economic reforms. Australian National Accounts’, data at the 4-digit level provides detailed information on the inputs to a selected industry sector and traces these inputs to outputs across all sectors in the economy [28]. In order to provide a simplified illustration of the transformation of the chemical sector over the 15 year gap we have plotted the common inputs for each of the chosen years against the outputs across all important, but aggregated, sectors of the econ- omy, as shown in Figure 1 for 1983-84 and Figure 2 for 1998-99.

The stark changes in the contributions of the chemicals sector to other sectors of the Australian economy are shown by the changes in the magni- tude of the peaks in these plotted matrices. For example, by 1998-99 the medical and pharmaceuti- cals (human and animal) element of the sector exhibited a substantial increase for exports ~AUD 75 to ~ AUD 956 million and in uses in agriculture ~ AUD 152 to ~ AUD 1,447 million, and doubled in magnitude in the provision of medical services (AUD 365 to AUD 734 million). In contrast, the use of chemical products in agriculture decreased substantially from AUD863million in 1983-84 to only AUD 376 million in 1998-99, as did the applica- tion of chemical products within the sector itself, from AUD 967 million to AUD 500 million. The applications of polymers (plastics) in the food, beverages and tobacco sector and of rubber in the mining sector rose from AUD 554 million to over AUD 1,610 million, and from AUD 124 million to AUD 255 million, respectively. Exports from Australia of petroleum and coal products rose for each element in the sector, but most particularly for pharmaceuticals, and for basic chemicals from AUD229million to AUD1,449million. In this paper our intent in using the national accounts data in this way is to stress that the chemicals sector has transformed to one much more strongly driven by meeting consumer and market demands over the 1980s to late 1990s.

Innovation and Industry Competitiveness

Innovation

There have been some notable successes over recent years and the Australian chemical industry appears to have lifted its innovation profile since deregulation (in this context success is defined by the commercial exploitation of ideas or continued operations with an increasing export profile). The Australian industry has long had a relatively strong record in support of domestic customers in the non-protected sectors of agriculture and minerals. In the case of minerals this extends to mining ex- plosives and corresponding services to the mining sector, advances in minerals exploration [33], flota- tion techniques in metal ore processing [27], and geochemical techniques in gold exploration [34].

In agriculture it includes plant and veterinary chemical developments [35]. And there is a longstanding tradition in scientific instrumentation, which stems from the invention of the atomic absorption spectrophotometer and other instruments which have now reached high export penetration levels [26]. The industry continues to have access to a broad ranging public sector research base in chemistry – in the Commonwealth Scientific and Industrial Research Organisation (CSIRO), Defence Science and Technology Organisation (DSTO), Australian Nuclear Science and Technol- ogy Organisation (ANSTO), the universities, and the Cooperative Research Centres (CRCs). Publicly funded biomedical public research institutions, the original home to nine to ten Nobel Prize winners, has provided the springboard for the development of the medical and health products industry (including pharmaceuticals). More recent examples of innovative outcomes in the Australian chemical industry are provided in more detail in Section 5.

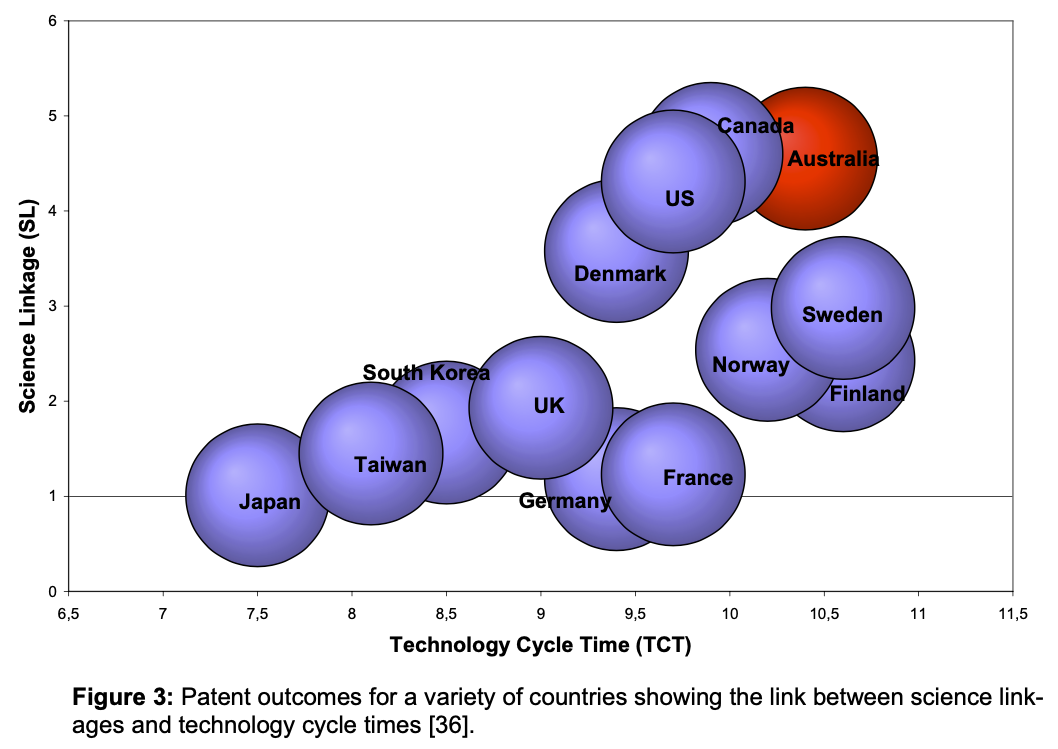

In addition, an analysis of patenting activity in the USA for a range of OECD countries, includ- ing Australia, independently demonstrates that over the period 1980 – 2001 Australia concentrated on slow changing technologies (having high technology cycle times, but with a strong focus on the scientific knowledge base, i.e., strong linkages between patents and scientific publications). This analysis is neatly summarised in Figure 3 [36]. Note that TCT was calculated on the basis of the average age of the patents cited, and SL on the number of scientific publications cited in the patent.

International Competitiveness

Let us consider the return on investment in in- novation across the chemical industry. Using R&D intensity (R&D expenditure/sales) as a proxy, Simpson et al. [37] have shown that the Australian chemical industry may be considered as sub- divided into three segments or “tiers”. Further, the growth prospects in each segment of the industry can also be deduced.

- Segment 1: The low R&D-intensity segment of the industry includes companies engaged in the production of high volume, low-value added products such as mineral-based inor- ganic chemicals, petrochemicals, and bulk polymers. This industry segment has diminished in importance in Australia as petrochemical and polymer production has moved towards a few world-scale production facilities – none of which are located in Australia, this in spite of the sustained process innovation that has occurred over the years in the design and application of catalysts to improve process efficiency, and to which Australian scientists have made significant contributions. More- over, this is a relatively mature segment of the industry.

- Segment 2: The moderate R&D-intensity segment of the industry comprises companies manufacturing special purpose chemicals, such as dyes, paints, food additives, photographic materials, with moderate innovation expenditures. Many of the products are mature and involve large scale, as opposed to batch production outputs. There continue to exist opportunities for smaller companies to grow as niche producers or suppliers to global production networks, despite the presence of large international firms in this segment.

- Segment 3: The high R&D-intensity seg- ment comprises companies that operate in high value added, low-volume chemicals. This includes pharmaceuticals and products from frontier areas of development like biotechnology and nanotechnology. In this segment growth is driven by excellence and understand- ing at the molecular level. New spin-off companies from research institutions and universities contribute to this segment.

First we observe that globalisation of the chemical industry and the “commoditisation” of many chemicals mean that price advantages lie with scale economies and large, low cost opera- tions. In the field of petrochemical processing the small scale and inefficient plants in Australia are increasingly unable to compete with large complexes established in the Asian region, in countries like Singapore, Korea and China. Moreover, there are few inducements for multinational companies to further develop competitive size plants in Australia following from the generally non- interventionist industry policy approach by Australian governments.

Second, the chemical sciences are no longer a strictly isolated discipline. Today it is necessary to address the pervasiveness of chemistry across a whole spectrum of activities. For example, the core technologies in fuel cells are electrochemistry and catalysis and such activities stand to revolutionise the transport industry, not the chemical sector. Companies in the industry have the opportunity to explore more ways to use their knowledge assets, e. g. in the way they deliver their product line, manage their intellectual property, or operate across a wider section of the industry value chain [38].

Third, the growing importance of partnerships and collaboration are evidenced by the surge in the growth of R&D and technology based alliances across the globe in recent years. This has become particularly significant over the past decade in the area of pharmaceuticals. It is generally acknowl- edged that Australia does not possess the resources necessary to take a new exploratory drug compound through the maze of phases and approvals necessary to bring such an advanced product to market. As a consequence, Australian businesses have been quick to realise the need to net- work and form alliances with the major pharmaceutical houses. Some successes have been achieved and there are many more in the pipeline where the alliance strategy must become second nature. In turn, such a strategy demands that the source of the idea (in Australia) must have strong intellectual property rights in order to gain the complete advantage from commercialisation. The growth in strategic alliance formation both within and external to Australia accelerated Australia to number one in the world in the number of alliances formed on a per capita basis [39].

Lessons from Experiences

In pursuing the case study approach we have examined in detail the innovation experiences of a range of successful companies and sought to de- termine their common behaviours in order to seek wider insights into current innovation processes within the Australian chemical industry. In addition we have drawn on the findings of the two Government Action Agenda Reports [22, 23], and on the experiences of other industry contacts. A number of important generalisations emerge from this collective information – notably the ingredents for the successful sustainability of Australian firms in the chemical industry.

The data reveal a considerable shift in the mindset within the Australian chemical industry, arising primarily from recognition of the need to focus on wider global markets. The successful companies demonstrated that their positioning in the international industry “system” was critical, and many made these moves to internationalise early in their development phase – the born-global companies [29]. Internationalisation not only un- derpins companies’ networking and relationship building, but also the way in which they develop their knowledge base and capabilities. Successful innovation is clearly associated with:

- working within the industry value chain,

- engaging in the global value chain of other industries.

A related but distinct theme is “leveraging knowledge from others”, especially in product development and in the process of marketing. This emerged from the case studies as an important phenomenon. It is consistent with the views of Chesborough on “open innovation” or drawing on external sources for ideas, e. g. from other companies through research or technology alliances or from public sector research institutions [20]. We consider that the formation of new companies from the public or private sector fall into these categories since “spin-offs” most frequently in- volve licensing the technology from a parent company or a research institution.

In summary, the two additional innovation strategies adopted by Australian chemical compa- nies to attain a world competitive position in the chemicals sector in the post-protectionist era have been:

3. developing an integrated packaging concept for their products and services, and

4. leveraging the knowledge of others.

Other authors [39, 40] have referred to “lever- aging the knowledge of others” in the broader sense as “systems integration” – combining the best from the world stable of innovative solutions, and creating from the combinations a unique and new product, system or service [29, 39].

Each of these mechanisms is illustrated in the next Section with reference to a cross section of case study examples.

Innovation Strategies

Working Within Existing Global Value Chains

The pharmaceuticals industry is a global value chain dominated by just a few large pharmaceutical houses. Each stage of the innovation process is a separate market within the overall pharmaceuticals market. At each stage value is added, innovation takes place, resources are used and people are em- ployed. One of the consequences of globalisation in this industry is that companies choose the location of their activities at each stage according to the perceived benefits. This creates opportunities for companies across the globe to contribute at various stages of the global chain activities.

The pharmaceuticals industry is the highest- growth and highest profitability segment of the chemical industry. It is an innovative knowledge- based segment with high R&D intensity, and a skilled workforce. While not large on an interna- tional scale, Australia makes significant investments in the development of a local pharmaceuticals industry – the human pharmaceutical industry is reported to have had a turnover of AUD 3.7 billion in 2001, a workforce of 8,400 people. Exports represented over AUD 1.4 billion [23].

The industry in Australia has also been sup- ported by a series of federal government programs in recent decades. These draw on the leverage available through the Pharmaceuticals Benefits scheme to provide offsets in pricing against com- mitments to research and development, manufacture and exports. Thus the first of these – the Factor f program was introduced in 1988, and modi- fied versions of this incentive have followed, including the PIIP program in 1999 and then the P3 program in 2004. Under the Factor f program there was a marked increase in R&D in Australia, and this led to a strong and growing position in discovery research. Australian capacity in clinical development grew under the influence of the later programs, but there has been limited net effect on investment in manufacture [23]. However, Australia has strengthened its position in recent years in the research-based identification and preparation of new chemical entities. The industry view is that this was directly influenced by government pro- grams, notably the former Factor f program. This provides an opportunity for Australian endeavour to contribute to the international industry and to secure a position in the global value chain. Australia’s capacity for conducting clinical trials also in- creased with the development of new facilities.

The well known drug development “funnel” for human pharmaceutical production emphasises that there may be many target/discovery drugs, but only a few make the grade through the process to market. Drug discovery has traditionally been focussed on large scale assaying of chemicals from natural sources, but increasingly this approach is being complemented by the design and molecular synthesis of drugs on a more targeted basis. In ad- dition, combinatorial chemical techniques have be- come common-place in academic research, but are not as yet frequently used in the pharmaceuticals industry. Australian software developments (chemometrics) provide a mechanism for the iden- tification of lead compounds from the complex mixtures involved (Scimetrics Ltd. and CSIRO) [41]. The interest of the ‘big pharma’ companies is in drawing on fresh streams of research, often stemming from the public sector research institu- tions as a source of new chemicals for testing. The manufacturing and marketing phase comprises four steps: the synthesis of the basic chemicals, the high value-adding step of manufacturing active in- gredients, formulation, and finally packaging and distribution.

The ‘big pharma’ operate across the full value chain, but there are also “safety gates” to international markets, including the US Food and Drug Administration (FDA). Successful drugs can achieve global markets of two or more USD billion dollars per year, but the path to success is narrow. The number of new chemical entities (these are the active ingredients which deliver the therapeutic benefit) finally cleared to enter the market is small, just 20 new chemical entities received FDA approval in 2004.

Australia has a few pharmaceutical manufactur- ing plants mainly involved in formulation and packaging, bolstered recently by GlaxoSmith- Kline’s decision to manufacture RelenzaTM in Aus- tralia. Basic chemical production is generally done in low cost countries like India and China; the active pharmaceutical ingredient (the main value adding step) is mostly done in countries that offer tax advantages like Ireland, Puerto Rico and Singapore. The subsequent steps of formulation and packaging are low value adding and can be done anywhere.

The big pharma companies generally choose to take most of their profit into the country in which they manufacture the active pharmaceutical ingredients. There has been a migration of production capacity to Singapore in recent years in response to tax incentives and subsidies. Over AUD 2.5 billion dollar has been spent on new plants by Merck, Sanofi-Aventis, GlaxoSmithKline, Wyeth and Pfizer, but until very recently there was no comparable investment in Australia for a decade. Austra- lia does have the capacity for small contract manufacturing at IDT, in radiopharmaceuticals at ANSTO, and in the extraction of alkaloids at a small number of research companies.

Specific Australian Developments in Pharmaceuticals

IDT: The Institute of Drug Technology Australia (IDT), based in Melbourne with an annual turnover of about AUD 21 million, has secured a successful niche in the high-value added stage of manufacturing active pharmaceutical ingredients. When IDT commenced operations in 1986 it provided analytical and other services to the pharmaceutical industry. IDT now manufactures active pharmaceutical ingredients for clients from many countries, and conducts the entire post- discovery pharmaceutical life cycle. That is, IDT can take a new chemical entity from the laboratory scale to full-scale production, including the con- duct phase I – IV clinical trials. There is a trend for pharmaceutical companies to outsource some or all of their research and development and clinical programs. IDT built a business around this grow- ing trend, and its success is based on the strategy of achieving and maintaining the highest levels of quality, the latter by meeting international Good Manufacturing Practice (GMP) standards. IDT’s quality systems were designed to exceed all inter- national regulatory requirements and passed scru- tiny from various regulatory bodies, including the US FDA.

CSL Limited [26] is another Australian company which operates across the full value chain, al- though this is mainly in the niche areas of plasma products and immunotherapy. CSL is the one company in Australia that is vertically integrated and active in all points of the value chain with a coherent R&D strategy in the area of immuno- therapy. CSL’s strategy has involved major acquisi- tions that have placed the company in a dominant position in blood collection and blood plasma processing in many international markets. The CSL group currently has an annual turnover of about AUD 2.8 billion, and has major facilities in Australia, Germany, Switzerland, the USA and Ja- pan, and a staff of 7,000 employees working in more than 25 countries.

Biota Holdings [26] is one of a very small group of companies worldwide that have brought bio- technology medicines from research to commer- cialisation. For other Australian companies the business opportunity in the discovery phase is the generation of new chemicals through research as candidates for further testing and evaluation by the ‘big pharmas’. The level of eventual success is low given the small number of chemicals that make it through the extended testing and approval proc- ess. The innovation strategy adopted by Biota in- volves the formation of strategic alliances on the back of a strong intellectual property portfolio of drug compounds. Biota is currently active in at least three additional alliances in Japan and the USA.

As a note of caution, of the success stories of bringing drugs from the discovery phase into in- ternational markets, only the Biota product RelenzaTM, and the colony stimulating factor (CSF) hormone cancer medical product based on re- search at the Walter and Eliza Hall Research Insti- tute have so far made the grade; and it is only the recent scare and resultant drug stockpiling that has led to the manufacture of RelenzaTM in Australia. However, in neither of the successful drug cases is a significant part of the value chain owned in Aus- tralia.

Thus, Australian companies also need to find a way of leveraging their discovery capability so that the nation owns a larger slice of the value chain. The challenge is to focus on those parts of value chain where the local industry can become among the best in the world and build mutually beneficial partnerships. Opportunities for greater efficiency lie in sharing resources, bringing companies of sub-critical size together, and mobilising the public R&D needed to capture more value in the global value chain.

Engage in the Global Value-Chain with Other Industries

As mentioned above, the chemical sciences are pervasive and contribute significantly to the growth of other international industries – e. g. minerals, agribusiness, health products, transport and printing. The minerals and agribusiness sec- tors are leading export sectors for Australia and leading edge users for new and improved tech- nologies. The leading sectors in manufacturing also offer opportunities for inputs from the chemical industry.

For example, polymers are integral to many products produced for export. There are opportunities for Australian companies to play a role as part of the supply chains for such industries. An example is the automotive industry which has high level requirements for a range of polymer components (which account for up to 8 % of car body weight) with each of the major car companies based in Australia having a select set of specialty suppliers. The situation is replicated with other ex- port industries producing products which involve polymer components – the opportunity exists for small and emerging companies to build specialist roles and supply high quality products to meet demanding specifications. Examples also arise in the medical and scientific equipment area – companies such as Resmed, Sola and Cochlear require and use polymeric components produced to the most exacting standards.

There may also be opportunities for customer driven processes involving the public sector re- search agencies.

Specific Australian Developments

Plastic bank note technology: now in use in Austra- lia and exported to many countries around the world was the outcome of a process initiated by the Reserve Bank and brought to fruition by re- searchers in the CSIRO Division of Chemicals and Polymers and Note Printing Australia. The work involved the development of a novel polymer sub- strate and the incorporation of a number of anti- counterfeiting devices.

Ciba Vision and Novartis: launched on world markets the day/night contact lens in 2001. This product emerged from a collaboration involving the University of New South Wales and the CSIRO (in the Vision CRC).

Moldflow Corporation: Although now headquartered in the USA, Moldflow was founded in 1978 in Melbourne, as a spin-off from the Royal Melbourne Institute of Technology and continues to have major development capability in Melbourne. Moldflow’s software solutions have brought promise of “better, faster, cheaper” plastic products to major companies in various industries around the world. Designs for molds and products ranging from toys to automotive and aerospace components to medical parts and many others were simulated and optimised prior to production, saving manufacturers hundreds of thousands of dollars every year. Such solutions enable customers to predict and solve injection molding manufacturing problems in the earliest stages of product development.

Australia maintains a valuable core capability in polymer research and this should provide a platform for moving to the next generation of polymer products. The shift in the polymer research thinking is toward tailoring the properties of the polymer to meet the specific needs of the product. This entails a shift from managing the bulk prop- erties of the polymer to managing molecular properties, and building science into the polymer. That is, chemically adapting properties to make the polymer useful for specific end uses. Some future typical examples might include a range of biocompatible polymers, polymers designed for controlled release of pharmaceuticals, and polymers for applications in human tissue engineering.

Developing an Integrated Packaging Con- cept for Goods and Services

It is not so long ago that chemical companies had no other thought than to make chemicals to sell to the next company in the value chain. This business model was built on the belief that the best assets (plants) would deliver the best value. How- ever today, chemical companies must rethink where and how they compete. We can see some of these changes in the way that the Australian com- pany Orica has integrated its explosives business into a suite of “mining services” and also in other chemical operations in Orica’s “water care busi- ness”. The need to think differently about the way products, and the knowledge associated with them, are sold in itself entails innovation [38].

This involves building on existing strengths and drawing on knowledge from other companies and from other fields and offering a new “package”; and subsequently delivering valuable new products and services. The value added here is in integration and product and service delivery, rather than the manufacture of individual components.

Specific Australian Developments

APS Plastics is a small Melbourne based na- tional-award winning firm which delivers high quality solutions through systems integration. The company provides polymer engineering and design services in the areas of plastics and polymers and has achieved success in areas as diverse as the coordination and delivery of plastic seats for the Lisbon football stadium for the 2004 European Cup and retractable plastic syringes. It brings together the engineering product development, the selection and design of the polymer, the robotics and assembly, equipment manufacture, and manufacture of the product, drawing in specialist contractors for specific projects. The company has demonstrated that it is able to compete internationally at the top of the market with a price advantage.

Opportunities exist in Australia for companies such as APS Plastics to capture markets by draw- ing on the assorted skills and expertise available in the industry. John Petschel, CEO of APS talks of “the need to be global and brutal through estab- lishing agility and performance using excellent people, effective project management, and in competitive tendering” [25].

Orica is a publicly owned Australian company with about 9,000 employees in 36 countries and an annual turnover of about AUD 4 billion. Formerly ICI Australia, the company grew in the 1950s and 60s under high tariff protection. In the 1990s it was reconstituted as an Australian company and a number of its operations were sold off as part of a streamlining process. The businesses divested in- cluded several polymers and related chemicals (PVC, ethylene, polyurethanes), technical paints, and crop protection chemicals. Orica now specialises in four areas – mining services (explosives), consumer products (paints and horticultural prod- ucts), agriculture (mainly fertilisers), and industrial chemicals.

Explosives provide a good example of rethinking the business and leveraging knowledge. Orica has a long tradition in the relatively mature field of explosives, and a close association with the mining industry. Explosives were selected by Orica’s first CEO as a target for growth as an international industry. Several international explosives business interests were acquired and the “package” of goods and services offered by Orica expanded. The ex- plosives themselves are the core of the integrated blasting service, which also includes initiating systems, detonators, mobile manufacturing units, and GPS-based site management. Since 1997, Orica has become the world’s leading supplier of com- mercial explosives and fully integrated blasting services to the mining, quarrying and construction industries. It has manufacturing operations in 28 countries including China, India, Indonesia, Malaysia, Myanmar, Philippines, Papua New Guinea, Singapore and Thailand.

Leveraging the Knowledge of Others

There is a plethora of Australian public sector research institutions which are involved in research in the chemical and biotechnological sciences, all relevant to present and future industrial development. The list is far too large to be considered in the present paper. Some outcomes can include the commercialisation of the research by an existing company, or licensing the technology to provide a revenue stream in the form of Royalty payments, or alternatively to generate new spin-off compa- nies. Some examples follow:

Specific Australian Developments

Boron Molecular is a new, small company with a narrow product line. It was established in 2000 as a spin-off company from CSIRO, based on novel organoboron technology developed in the 1990s by Dr. Seb Marcuccio. It is now wholly owned by Xceed Biotechnology Ltd. Organoboron compounds are employed by a wide variety of large companies in their drug discovery programs. There was also a market for the new range of organoboron chemicals in the biotechnology industry and for direct sale to fine chemicals companies. The company underwent the “test by fire” of many new companies – with problems in establishing laboratory facilities, cost overruns and over- optimistic financial projections, but it has already established a business equating to several million dollars a year in selling its product on international markets. The establishment of a US office eased some, more perceived than real, difficulties of dealing with a supplier at an extended distance.

GBC Scientific [26]: Research at the CSIRO Division of Applied Physics provided GBC with the opportunity to further develop for the market an instrument now known as the MFC 2100 Micro Fourier Rheometer, which can perform analyses on volumes of less than 100 μL on samples like paints, adhesives, or on human tears. GBC manufactures and exports a broad range of scientific instruments, including atomic absorption spectrophotometers.

Starpharma Pty Ltd. [26] was established in 1996 to commercialise dendrimer technology discovered at the former Biomolecular Research Institute (BRI) Ltd. in Melbourne involving the synthesis of several biologically active dendrimers as protein mimics for pharmaceutical applications, in particular, for treating a broad range of viral and other human diseases, notably those that are sexually transmitted. Specifically, Starpharma developed the first dendrimerbased vaginal microbicide VivaGelTM, which offers early hope that nanoscale dendrimers could be developed as new drug delivery platforms.

This drug is aimed at preventing transmission of a broad spectrum of sexually transmitted dis- eases (STDs) including HIV, herpes, chlamydia and human papilloma virus. In the USA alone, STDs including genital herpes affect more than 70 million people annually. It was estimated in 1999 that the annual cost of all STDs was more than USD 10 billion a year.

All of the above examples are of born-global companies, since they all entered the international arena almost at the point of their conception [29].

There are also opportunities for companies to work collaboratively with public research organisations on projects with agreed shared objectives and to draw on these sources of expertise. Collaboration with industry partners has been a growing feature of research conducted by CSIRO and other public research institutions including universities. It is also a core feature of the seventy or so Coop- erative Research Centres which operate across the research spectrum. The value of this approach is exhibited in the success of Hawker de Havilland (HdH), a long standing core industry participant in the CRC for Advanced Composite Structures. Research conducted by the CRC and transferred to HdH was essential to the company’s recent success in winning the contract to construct all the wing trailing edge devices, including flaps, spoilers and ailerons on the new Boeing 787 [42].

Outlook

We have drawn some general lessons by reviewing the common elements in successful innovation case studies of more than 25 companies operating in the Australian chemical industry, following the deregulation and globalisation phenomena that have characterised the industry over the past one to two decades.

First, it is evident from the information on R&D intensity that the prospect for Australia to develop a position as a major player in Segment 1 of the industry – the area of production of bulk chemicals is negligible in the event that the major players do not invest in the near-term in large-scale processing plants in Australia.

Second, Segment 2 products are generally built around speciality chemicals, which do not necessarily demand high research intensity and the opportunities for Australia to make a significant mark on the world scene appears low and possibly reducing. Most of the products in Segments 1 and 2 of the industry are mature and for cost efficiencies to be gained these demand large scale processing. Where Australian companies may succeed in Seg- ment 2 may involve yet to be identified opportunities in novel customer-driven batch production.

Third, future success in the Australian chemical industry clearly depends on Australia’s capacity to change through innovation, either by drawing on its own high quality research base, or alternatively integrating capabilities from other sources. This approach is justified by the outcomes of the case studies.

We conclude that the lessons to be learned from the case studies for future opportunities in the chemicals sector must rest on at least the pur- suit of four simple mechanisms of innovation drawn from the case studies. These “innovation strategies” include existing and new players (1) working within existing global value chains, (2) engaging with other globally focused industries, (3) developing an integrated packaging concept for their products and services and (4) leveraging the knowledge of others.

In other words, the evidence suggests that the preferred mechanism for sustained development of an Australian identity in the chemicals sector will best be achieved through the adoption of niche strategies. Australia cannot afford to be complacent about its “chemical future”. The task at hand is an urgent one, and the urgency is for Australian industry to be more innovative in order to ensure its future global competitiveness.

From a policy perspective, we suggest that the most important lesson is that the chemical sector should not be considered as the conglomerate that statistical data collections have tended to impose on the analyses, but rather as a series of distinctly different components such as those delineated by the segmental analysis. There is a need to nurture a well connected and relevant research base, from which entrepreneurs and companies can be born with the agility and foresight to capture the oppor- tunities that arise. Not only that, but government policies should aim to provide a supportive environment for the growth of new and emerging born global companies, and new born global activities taken up by existing companies.

We suggest that the strategies for innovation that emerge from this study are also applicable to any small country that is unlikely to be the subject of major foreign investments in the manufacture of bulk or special purpose chemicals, but which possesses a strong research infrastructure.

References

[1] Gross, R. M., (1999), Growing through innova- tion, Chemical and Engineering News, Octo- ber 25, p5.

[2] Gross, R. M., (2003), Overview of Trends in In- novation in the Chemical Industry, Reducing the Time from Basic Research to Innovation in the Chemical Sciences, A Workshop Report to the Chemical Sciences Round Table, National Academy of Sciences, p7-17.

[3] Arora, A, Landau, R, and Rosenberg, N, (1998), Chemicals and Long-term Economic Growth: Insights from the Chemical Industry, John Wiley and Sons, USA..

[4] Arora, A, (1997), Patents, licensing, and market structure in the chemical industry, Research Pol- icy, 26, 391-403.

[5] Arora, A, Fosfuri, A, and Gambardella, A., (2001), Markets for Technology: the economics of innovation and corporate strategy, MIT Press, Cambridge, USA.

[6] Sinclair, G, Klepper, S, and Cohen, W., (2000), What’s Experience Got to Do With It? Sources of Cost Reduction in a Large Specialty Chemicals Producer, Management Science, 46 (1), p24-45.

[7] Wood, A, and Scott, A, (2004), Licensing Ac- tivity is on the Rise, Chemical Week, March 24, Access Intelligence, USA..

[8] Swift, T. K., (2006), The Global Business of Chemistry: Prospects and Challenges, Journal of Business Chemistry, 3(1) p2- 12.

[9] EIMS, (1996), Innovation in the European Chemical Industry, European Monitoring Sys- tem (EIMS), Publication 38, WZB 1996.

[10] Houlton, S., (2002), Speciality Chemicals, European Chemical Industry Council (Ce- fic), Paris, see: http://www.users.globalnet.co.uk/~sarahx/ articles/cefic.htm.

[11] Harries-Rees, K., (2005), Getting the Balance Right, Chemistry World, Royal Society of Chemistry, UK, February 2005.

[12] Daemmrich, A, and Mody, C., (2004), Re- search Frontiers for the Chemical Industry, Report of the First Annual CHF-SCI Innovation Day, September 2004, Chemical heritage Foundation, Philadelphia.

[13] Johnson, J., (2004), Greater Industry Innovation, Chemical and Engineering News, May 11. see: http://pubs.acs.org/cen/news/8219/8219i ndustry.html.

[14] Chemical Industry Vision 2020 Technology Part- nership, (2004), see: www.chemicalvision2020.org.

[15] Halford, B., (2005), Nano Database Goes Online, Chemical and Engineering News, 83(42), October 17, p33.

[16] Houlton, S., (2003), Innovation: the lifeblood of the chemical industry, Chem@Cam, Spring 2003, see http://www.users.globalnet.co.uk/~sarah/a rticles/caccigt.htm.

[17] Imanari, M., (2003), Innovation in the Japanese Chemical Industry, IUPAC Chemrawn XVI 2003, see:

http://www.iupac.org/symposia/conferences/chemrawn/crXVI/crXVI-N32- Imanari.pdf.

[18] Ren,T.,(2003)AnOverviewofInnovationinthe Chemical Industry: Process Innovation and product innovation, Danish Research Unit for Indus- trial Dynamics, Druid Conference Paper, January 19, 2 pages.

[19] Tidd, J, Bessant, J, and Pavitt, K., (1997), Managing Innovation: Integrating Technological, Market and Organizational Change, John Wiley & Sons, London.

[20] Chesborough, H., (2003), Open Innovation: The New Imperative for Creating and Profiting from Technology, Boston: Harvard Business School Press, 2003.

[21] ABS, (1993), ANZSIC93 Division C Manu- facturing, Subdivision 25, Australian Bureau of Statistics, Canberra.

[22] Chemicals and Plastics Action Agenda Steering Group, (2001), Underpinning Austra- lia’s Industrial Growth, Canberra, Australia.

[23] Pharmaceuticals Industry Action Agenda Team, (2002), Local Priority – Global Partner, Department of Industry, Tourism and Re- sources, Canberra, Australia.

[24] Eisenhardt, K. M., (1989), Building theories from case study research, Academy of Manage- ment Review, 14: 532-550.

[25] Upstill G, Spurling T and Simpson G., (2005), Innovation and the Australian Chemical Industry, CSIRO, Melbourne, Australia.

[26] Jones, A.J., (2005), Industry Profiles, Chem Aust, Vol 72, (7) 20-21, (8) 14-15, (9) 9-13 and 25-27, (10) 17-19 and 22-24, (11) 16-18.

[27] Kolm J., (1988), Chemical Industry – Australian contributions to chemical technology, in Technol- ogy in Australia 1788–1988, chapter 9, Aus- tralian Academy of Technological Sciences and Engineering, Canberra, Australia.

[28] ABS, (1983-84), Input by Industry and Final Demand by Category and Supply by Commodity Goods, Australian Bureau of Statistics, Cata- log Number 5209.0.55, TB20.Y8384, Com- monwealth of Australia, Canberra, Australia; ABS (1998-99), Input by Industry and Final Use by Category and Supply by Product, Australian Bureau of Statistics, Catalog Number 5209.0.55.001, TB60.Y9899, Commonwealth of Australia, Canberra, Australia.

[29] Chen, S and Jones A. J., (2006), Do born global companies learn faster? Findings from Australian chemical and biotechnology companies, Proceedings of the San Fran- cisco-Silicon Valley Global Entrepreneur- ship Research Conference, March 2006.

[30] ABS, (2005), Research and Experimental Devel- opment, Businesses Australia,2003-04, Aus- tralian Bureau of Statistics, Catalog Number 8104.0, Commonwealth of Australia, Can- berra Canberra, Australia; ABS, (2004), Re- search and Experimental Development, Government and Private Non-Profit Organisations 2002-03, Australian Bureau of Statistics, Catalog Number 8109.0, Com- monwealth of Australia, Canberra, Australia. For commentary see: Jones, A. J., (2005), Business Expenditure on R&D: latest fig- ures, Chemistry in Australia, Vol 72, No 11, December 2005, p 19.

[31] IPRIA, (2005), R&D and Intellectual Property Scoreboard 2004, Intellectual Property Re- search Institute of Australia, University of Melbourne, Australia.

[32] ISI, (2004), Essential Science Indicators (http://www.isinet.com/products/evaltools /esi/ accessed 10 January 2005).

[33] Scott-Kemmis D, Holmen M, Balaguer A, Dalitz R. P, Bryant K.H.J, Jones A. J, and Matthews, J. H., (2005), No Simple Solutions: How Sectoral Innovation Systems can be Trans- formed, National Graduate School of Man- agement, ANU, 60 pages, June 2005.

[34] CSIRO media release 97/243, (1997), Scien- tists hailed for $5 billion gold discoveries, 9 De- cember 1997.

[35] Simpson G.W and Spurling, T.H., (2005), Chemistry in Pasteur’s Quadrant, Aust. J. Chem. 58, p823-824.

[36] Balaguer, A, (2005), private communication.

[37] Simpson G.W, Spurling T.H, Upstill G., (2002), The global technology revolution and the chemical industry: an Australian perspective, Pro- ceedings of the International Symposium on Management of Technology and Innovation (ISMOT), 2002, Hangzhou, China.

[38] Budde, F., Elliott B. R., Farha, G., Palmer, C. R,, and Rudiger, S., (2000), The Chemistry of Knowledge, McKinsey Quarterly, no. 4, pp 99-107.

[39] Jones, A. J, Fry, P, Hsu, S and Dowie N., (2003) The Importance of Strategic Alliances to Innovation in Australian Firms, Department of Industry, Tourism and Resources, Canberra, Australia.

[40] Balaguer A, and Holmen M., (2003), A The- matic Characterisation of Innovation in Australia: An Interpretative Overview of the Australian Inno- vation System, Working Paper Number 2, In- novation Management Policy and Program, National Graduate School of Management, ANU, 2003.

[41] Jones, A.J., (2006), Case Study – work in progress.

[42] Allen Consulting Group, (2005), The Eco- nomic Impact of Cooperative Research Centres in Australia, Canberra, Australia.