A catalyst for change? How sustainable finance can support the transition of the chemical industry

Abstract

The chemical sector impacts close to the entirety of all manufacturing supply chains. Therefore, it could be a key driver of emission reductions, especially with regards to value chain emissions (Scope 3). Net zero solutions will require significant investment and innovative sustainable finance instruments could support by providing a mean to credibly signal transition plans. As the market for sustainable debt matures, it is key to address greenwashing concerns. Increasing investor attention as well as reporting requirements under upcoming regulations such as the EU Green Taxonomy further add scrutiny. This paper assesses current trends and outlines how sustainable finance can support the transition of the chemical industry.

Introduction

Chemistry is the study of matter – it is the study of everything. The periodic table contains the ingredients for making just about anything. This is also reflected in our economy: More than 95% of manufactured products rely on chemicals (European Commission, 2017). The European Union recognises the sector as an enabling industry which may play a “pivotal role” (European Commission, 2023a).

Yet at the same time, the chemical sector is the single biggest industrial energy consumer (IEA, 2023). The emissions stemming from the sector’s use of heat, steam, and power for compression and cooling account for roughly half of its total fossil fuel related emissions. The other half is linked to using fossil fuels as input to chemical reactions, for products such as plastic or fertilizer. Overall, the chemical sector takes third place in the ranking of industry subsectors when it comes to direct carbon dioxide emissions.

Given the urgent need to reach net zero and commitments such as the 2015 Paris Agreement and the EU Green Deal, the pressure for the chemical industry to decarbonise is mounting. In business terms, this means that so called transition risk, one form of climate risk, is building up. To demonstrate its materiality, looking at cost originating from the European Union Emission Trading System (EU ETS) is telling: Forecasts see costs quadrupling by 2030 (ICIS, 2021). Here, very obviously, reducing emissions is not only doing good for the planet, but also has direct financial benefits. Still, some chemical companies choose to further deepen their ties with fossil fuels by buying petrochemicals business from energy majors who are selling the assets as part of their transition efforts (Bousso, 2020; BBC, 2017) and continue to invest in them (Reuters, 2022; Ineos, 2018).The International Energy Agency’s (IEA) Fatih Birol has called the petrochemicals business a “key blind spot” while examining their future (IEA, 2018). The IEA sees the sector not on track, stating that carbon dioxide intensity has been stable over recent years for primary chemicals, yet the et Zero Emission by 2050 Scenario requires an 18% absolute emission reduction compared to 2022 by 2030, despite increasing production (IEA, 2023). This means decoupling emissions from production is urgently needed.

Sustainability and the chemical sector

“Chemistry is, well technically, chemistry is the study of matter. But I prefer to see it as the study of change” (IMDB, 2008)

And indeed, the chemical industry could be a key driver for transforming the real economy. In the TV show “Breaking Bad” Walter White goes one step further than portraying chemistry as the study of everything, by adding a forward-looking perspective to it. Given that chemical products are the basis for nearly all manufactured products, they need to be accounted for under so-called Scope 3 emissions for the respective manufacturers. The Greenhouse Gas Protocol, the most common emission classification system for corporate emission reporting, distinguish three scopes: Direct emissions (Scope 1), indirect emissions from purchased energy (Scope 2) and lastly emissions outside of a companies own boundaries, related to its value chain (Scope 3).

Up until today, most efforts and pledges revolve around Scope 1 and 2, often dubbed core emissions. Yet there is increasing attention shifting towards Scope 3[1] – not the least because they make up the majority share of all emissions and in fact the vast majority for most sectors (Hoepner & Schneider, 2022a). Indeed, Deloitte specifically lists sustainability as their number 1 trend and specifically mentions the carbon footprint of supply chains as their top 3 for the chemical sector (Deloitte, 2022). The chemical industry is in a unique position to drive major supply chain decarbonisation and thereby support Scope 3 emission reductions globally. Moreover, the transition involves a range of opportunities for chemistry, including batteries but also ammonia for shipping.

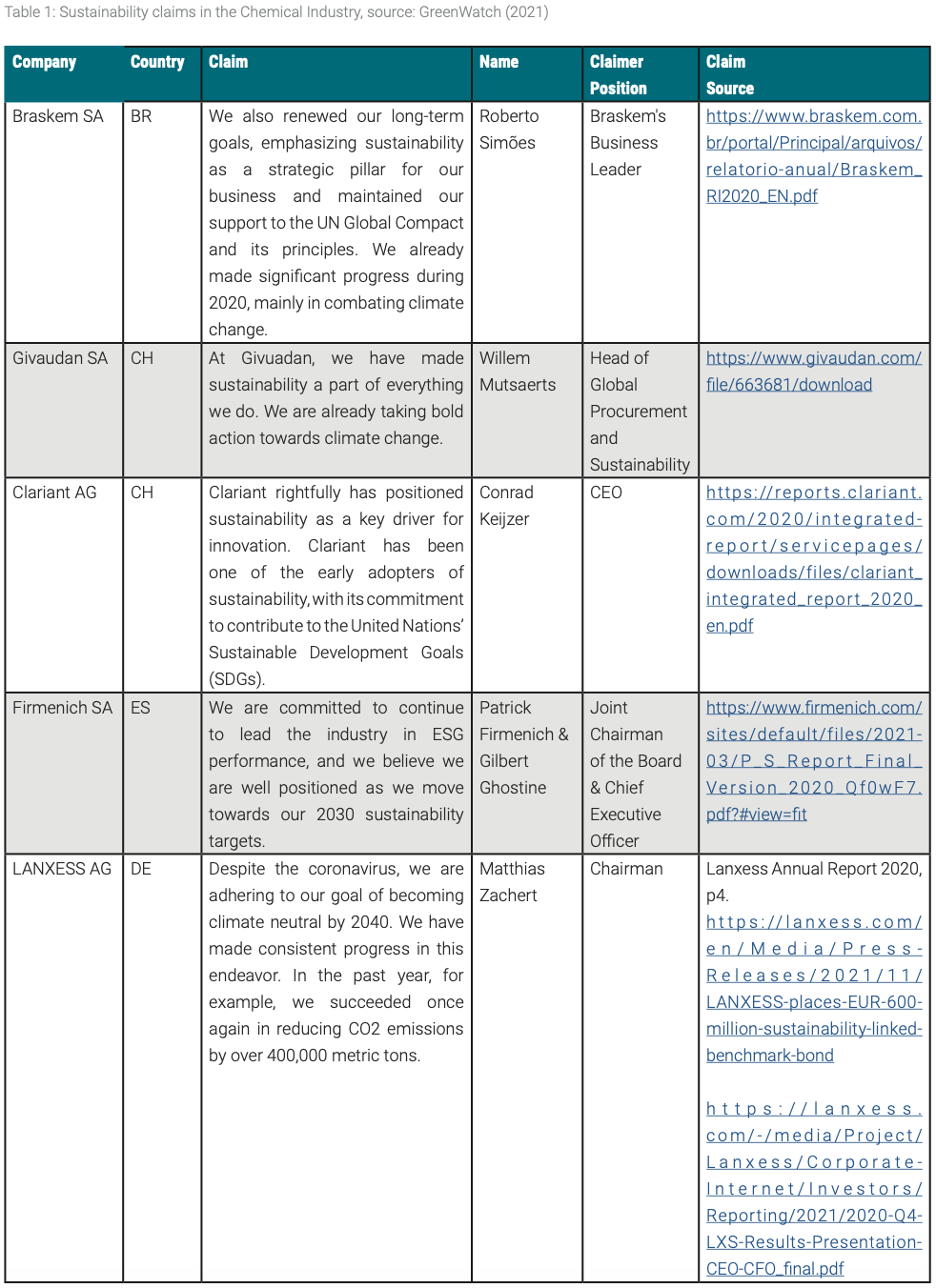

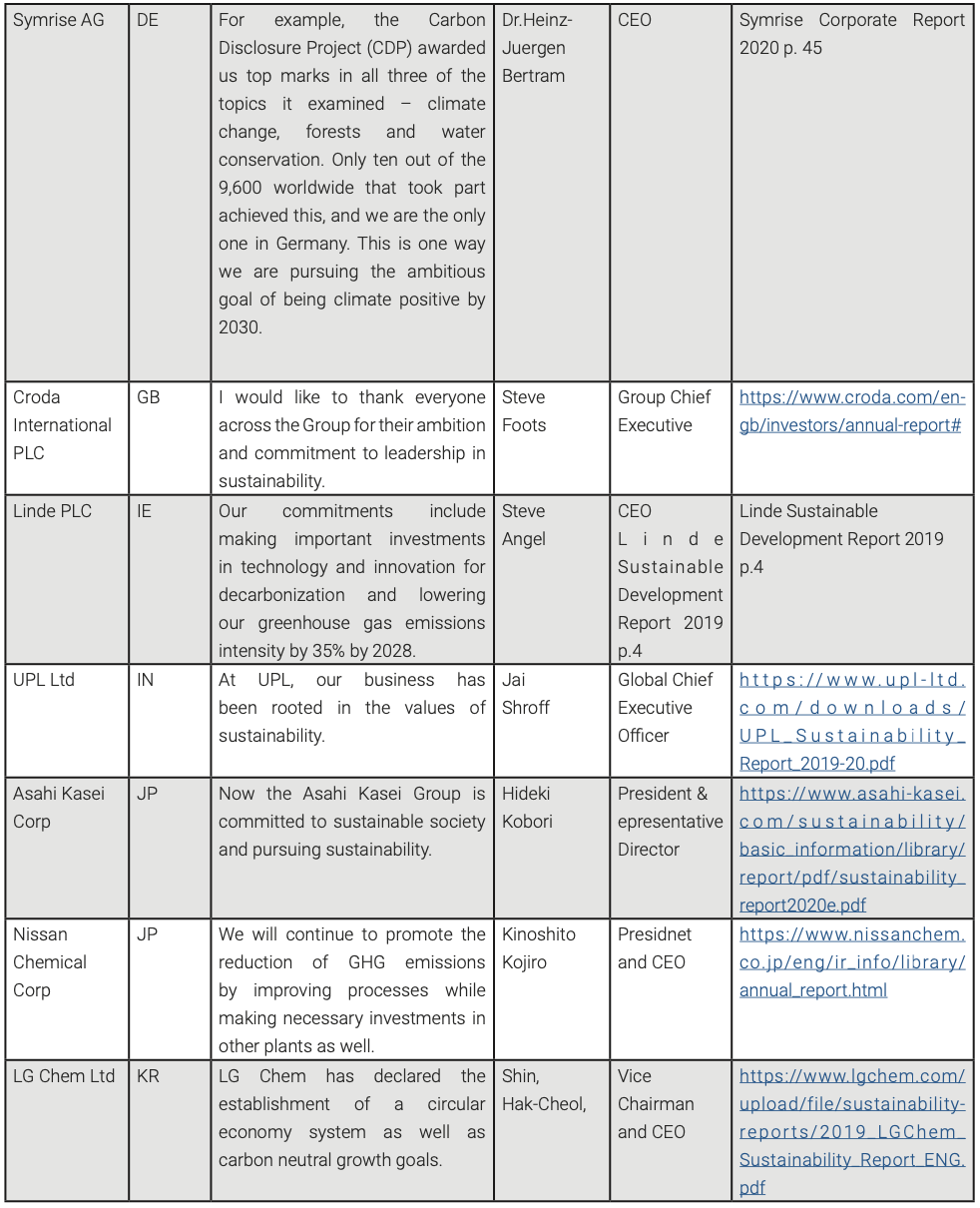

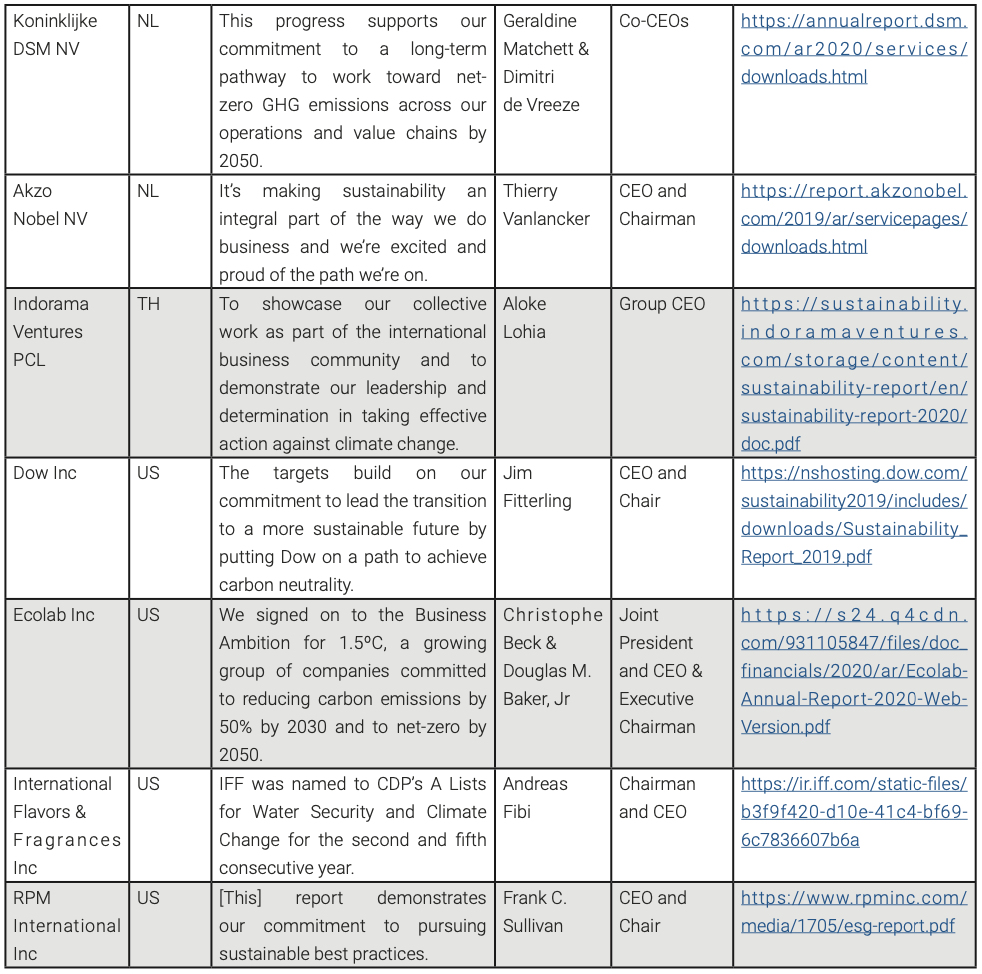

Thus, it is little surprising that firms in the sector signal their sustainability ambitions via bold claims in their corporate reporting and public statements. Table 1 gives an overview of different sustainability statements made by senior executives of firms from the sector. It becomes obvious, that statements vary in their level of ambition but also scope and time perspective. It is important to recognise differences in forward-looking (plans and pledges) and backward-looking (actually achieved performance, that can be evidenced) claims. Some firms may choose to highlight their standing relative to their peers, others make absolute claims. The distinction between relative emission targets, in the form of intensities (ie emission reduction per revenue or unit of output) and absolute ones is likewise crucial.

Yet any claim needs to translate into tangible actions, otherwise firms run risk of engaging in greenwashing. The table above is part of the GreenWatch[2] database, which compares corporate claims across sectors with actual emission performance. For alignment with the Paris Agreement and the 1.5°C target absolute emissions must be reduced 7% year on year. Anyone making bold sustainability claims should at least meet this basic metric. At GreenWatch, Artificial Intelligence (AI) is used to classify sustainability claims in terms of their boldness and then compared to absolute core emission reductions. A differentiation between no claim, a moderate claim and a bold claim and between an emission reduction in line with the Paris Agreement, a weak emission reduction and an emission increase is made. Importantly, carbon offsets are not factored in[3]. Should a company make a strong sustainability claim while in fact increasing their absolute emissions, a high likelihood of greenwashing is assigned.

Today many forms of greenwashing have developed. Given the obvious commercial incentive to be perceived as green, sophisticated strategies to mislead customers and investors have evolved. PlanetTracker portrays greenwashing as a beast with many heads in their Hydra report. The analysis outlines six distinct types of greenwashing (PlanetTracker, 2023, p.3-8):

“Greencrowding is built on the belief that you can hide in a crowd to avoid discovery; it relies on safety in numbers. If sustainability policies are being developed, it is likely that the group will move at the speed of the slowest.

Greenlighting occurs when company communications (including advertisements) spotlight a particularly green feature of its operations or products, however small, in order to draw attention away from environmentally damaging activities being conducted elsewhere.

Greenshifting is when companies imply that the consumer is at fault and shift the blame on to them.

Greenlabelling is a practice where marketers call something green or sustainable, but a closer examination reveals that their words are misleading.

Greenrinsing refers to when a company regularly changes its ESG targets before they are achieved.

Greenhushing refers to the act of corporate management teams under-reporting or hiding their sustainability credentials in order to evade investor scrutiny.”

A lot of the greenwashing that is happening in the market is not explicitly illegal and hard to proof. But climate litigation is growing in momentum and posing a real risk to climate offenders. And these lawsuits have very material financial risk for the respective companies: Sato et al. (2023) find that climate litigation filings or unfavourable court decisions on average lead to reduction in firm value by -0.41%. These lawsuits can also result in transparency and climate action obligations (Weller and Tran, 2022).

While climate litigation for the moment focuses on energy firms and the carbon majors, the chemical industry is also subject to substantial pressure due to environmental concerns. Pollution prevention is an additional key environmental objective as recognised by the European Commission (European Commission, 2023b). Around 40 laws regulate chemicals in the EU, which reflects ongoing concern among EU Citizens: 90% of Europeans worry about the impact of chemicals in everyday products on the environment and 84% about its impact on their health (European Commission, 2023c).

One class of chemicals has recently received considerable amounts of attention[4]: Per- and polyfluoroalkyl substances (PFAS), commonly referred to as “Forever Chemicals” which are used when manufacturing fluoropolymer coatings and products that resist heat, oil, stains, grease, or water. The EU is taking actions to phase out their use where it is not essential (European Commission, 2023d). American multinational 3M announced the end of their PFAs production for 2025, which will incur initial cost of up to $1 billion and more later on. Yet longer-term legal liabilities are estimated to be over $30 billion This compares to the roughly $1.3 billion in annual sales generated from PFAs at 3M (Kary & Beene, 2022). Needless to say, PFAS litigation is not limited to 3M. DuPont and Chemours settled to pay $670 million in a lawsuit filed by thousands of people in Ohio (Maher & McWhirter, 2017) and $1.18 billion following complaints from drinking water providers (Flesher, 2023). In total, DuPont has been named in over 6000 PFAS related lawsuits (ChemSec, 2022). Other cases involve Tyco Fire Products LP and Chemguard Inc (SEC, 2020).

Following the idea of a carbon footprint, NGO ChemSec published chemical footprint for the 54 biggest chemical firms. In 2022, only four of them published a strategy to phase out hazardous chemicals from their product portfolios (ChemSec, 2022).

This risk is not going unnoticed by investors. In November 2022, 47 asset managers with a combined $8 trillion assets under management issued a call to phase-out PFAS. Besides the financial and litigation risk, the call cites the danger it poses to future generations (ChemSec, 2022).

Given that the most recent update on planetary boundaries established that the safe boundary for chemical pollution, “novel entities”, has been crossed (Richardson, et al., 2023), the pressure can only be expected to increase going forward.

Defining a path to sustainability

While there are many challenges to be overcome, most solutions don’t require major breakthroughs. For example, it is already feasible to produce plastic bottles with emissions-free chemicals at a price increase of those bottles by 1% (Energy Transition Commission, 2020). Overall, Deloitte postulates that 15 technologies can abate 90% of industry emissions (Deloitte, 2022).

Still, developing solutions at the scale and speed we need require significant investments. While there is growing investor appetite, it creates the need to be able to distinguish credible transition plans from greenwashing to avoid capital misallocation.

The first step is defining what green or sustainable really means. That is exactly what the EU Taxonomy for Sustainable Activities sets out to do (European Commission, 2020). The EU Taxonomy focuses on environmental sustainability, covering six objectives: Climate change mitigation, climate change adaptation, sustainable use and protection of water and marine resources, transition to a circular economy, pollution prevention and control, and protection and restoration of biodiversity and ecosystems. By design, all environmental objectives are equally important. The EU Green Taxonomy is designed to act as a market transparency tool and transition enabler. It is rooted in EU law as part of the EU sustainable finance framework; the Taxonomy Regulation went into force in July 2020.

Technically, the EU Taxonomy allows to assess the sustainability of economic activities, which means that entities can be assessed as a sum of their often numerous activities. It is important to note, that Taxonomy reporting will be mandatory for a large number of firms, but that does not mean that companies must comply with the criteria nor that investors must invest in a specific manner. Taxonomy reporting is carried out in terms of revenue, operating expenses (opex,) and capital expenditure (capex). If an economic activity meets all the criteria set out in the regulation, it is considered “aligned”. A company may for example report that it generates X% of its revenue from taxonomy-aligned activities or that it spends Y% of its capex on taxonomy-aligned activities.

The first step to alignment is checking whether an activity is included in the Taxonomy regulation, termed “eligibility”. If an activity is not (yet) included in the EU Taxonomy, there are no criteria to compare against and an activity cannot be aligned. Activities not covered remain out of scope for now. Once eligibility is established for an activity, three levels must be passed in order to achieve alignment. First, substantial contribution to at least one of the six environmental criteria must be proven by complying with activity specific criteria. Next, “Do No Significant Harm” (DNSH) criteria must be passed for all the other environmental objectives of the EU Taxonomy. This is to ensure that while the activity may support progress in one area it does not jeopardize achieving the other. Lastly, even though the EU Taxonomy focuses on the environment, minimum social safeguards must be met. In total, the process therefore encompasses four stages that an activity must pass to demonstrate EU Taxonomy alignment: Eligibility, substantial contribution to at least one objective, no significant harm to the other objectives and meeting minimum social safeguards. It is noteworthy that “not aligned” does not mean harmful, it simply equals not meeting the criteria to be considered substantially contributing to environmental objectives.

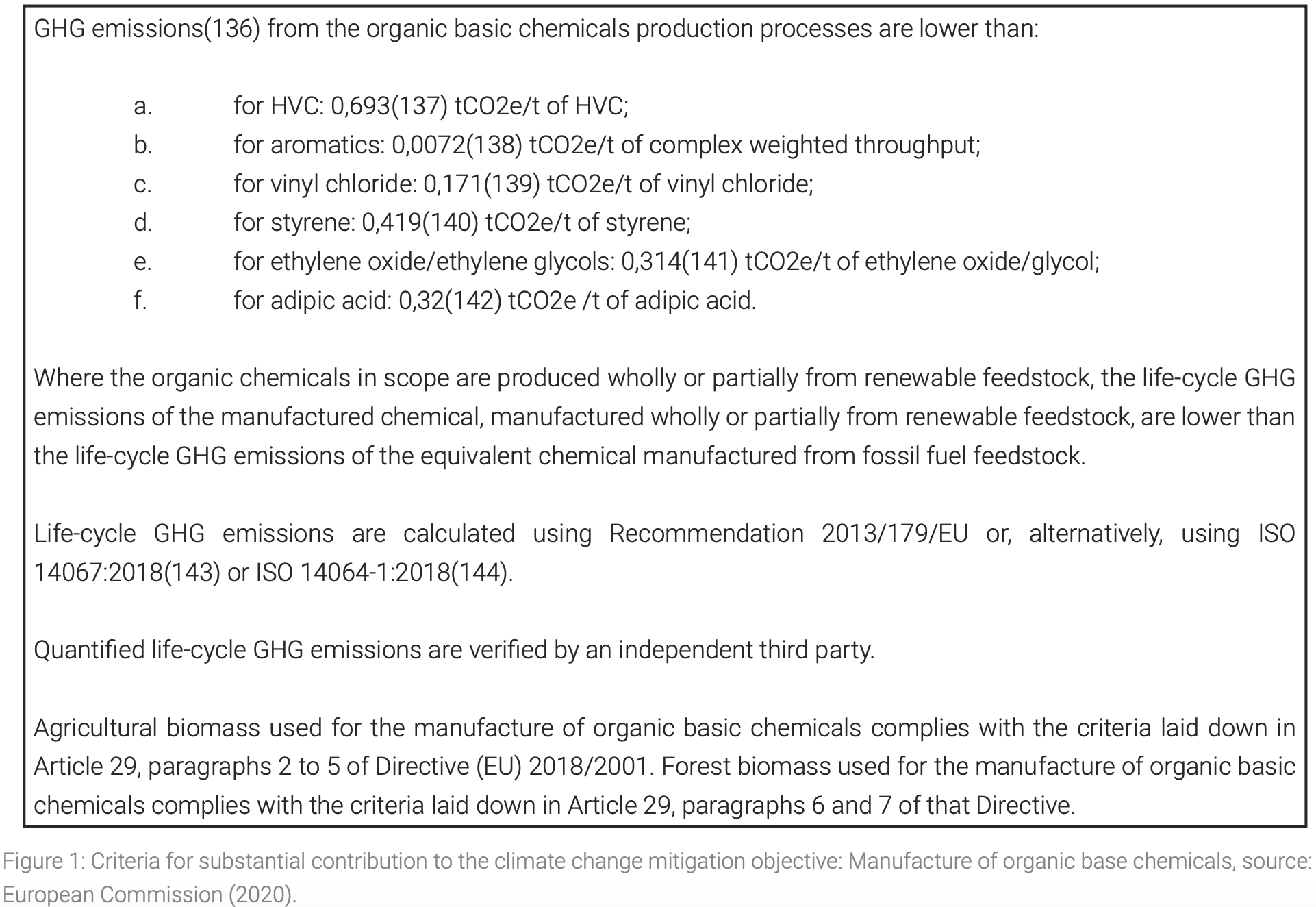

The European Commission offers the EU Taxonomy Compass tool for easy access and navigation of criteria. For the chemical sector, a range of activities is eligible. Figure 1 shows the substantial contribution criteria for climate change mitigation from the EU Navigator for the manufacture of organic basic chemicals. Other examples include the manufacture of plastics in primary form, the manufacture of soda ash, chlorine, aluminium, or ammonia.

In advance of the pollution prevention delegated act for the EU Taxonomy being published in 2023, the Investor Initiative on Hazardous Chemicals (IIHC), representing some of the biggest institutional investors, published an open letter addressed to the European Commission calling for robust chemical criteria (IIHC, 2023). Lobbying to weaken policy is found across sectors. For example, in the UK, lobbying efforts have been noted on fracking and exempting the chemicals sector from climate taxes (ClientEarth, 2023). InfluenceMap compiles a lobbying scorecard by analysing engagement from corporations and industry associations on climate policy. Of the 25 assessed corporations none got the highest score A, only one firm was scored B (InfluenceMap, 2023). Naturally, the EU is not alone in creating a classification system for sustainability in this regard. Indeed, in 2022 around 20 countries were at different stages of developing their version of a taxonomy. These vary widely in scope, design, and level of ambition. A noteworthy exception among the 20 countries is the US. Other large players such as China, Russia, Brazil, Canada, and Australia as well as smaller players such as the Dominican Republic or Mongolia have been more proactive.

Facilitate transition: Sustainable Finance

Corporate net zero pledges for 2050 are becoming popular; globally around 70 chemical firms have set targets (Deloitte, 2022). The UN Race to Zero Data Explorer offers a concise platform to explore the net zero targets of 500 firms globally. The tool allows to view the year when a firm aims to reach net zero and distinguishes between absolute emissions and emission intensities. A net zero emission intensity target takes the form of a “per unit” pledge, for example revenue or product. This approach may lead to a firm’s absolute emissions increasing despite intensities decreasing if the company grows. From a climate science perspective, we need absolute net zero in order to halt global warming.

Besides the pledge, the tool also contains information on whether the firms that pledge do have a transition plan on how to achieve their goals. Additionally, it gives an indication of progress on proceeding with the plan by showing emission reduction trends for Scope 1 and Scope 2 emission, and how many Scope 3 emission subcategories are disclosed. Alignment numbers for revenue, capex and opex are available as well.

While transition plans are needed to understand how a company envisions to be part of the future net zero economy, forward looking plans are no guarantee. Greenrinsing (PlanetTracker, 2023), where a firm silently drops a target which it previously published, is unfortunately emerging as a greenwashing practice. Only relying at backwards- looking measures such as past emission reductions likewise is not optimal for gauging future performance.

A big concern for both, companies with robust transition plans is therefore how to credibly communicate these. On the flipside of the coin, investors looking to invest in firms that will be profitable in a net zero economy need a way to ensure investee firms indeed transition.

This is where sustainable finance can offer remedy. Different innovative financial instruments have evolved in the green and sustainable finance space. The general idea is instead of just publishing words and plans, to “put your money where your mouth is” and link financing to sustainability.

A more established instrument are green bonds, which are supposed to directly finance green activities. Academic research finds that these are considered a credible instrument to communicate commitment to the environment (Flammer, 2021). Flammer (2021) finds benefits both on the environmental side – lower emissions and higher environmental ratings – as well as on the financial side, in the form of a diversification of the investor base and more long-term ownership.

One particularly suitable instrument for transitioning is sustainability-linked debt. First it is noteworthy that the debt market has a key role to play in supporting the transition as primary market transactions occur periodically, according to refinancing cycles. This is not the case for equity, where the majority of transactions occur between investors on the secondary market. In this case, the corporate cash flow is not directly affected (Hoepner & Schneider, 2022b).

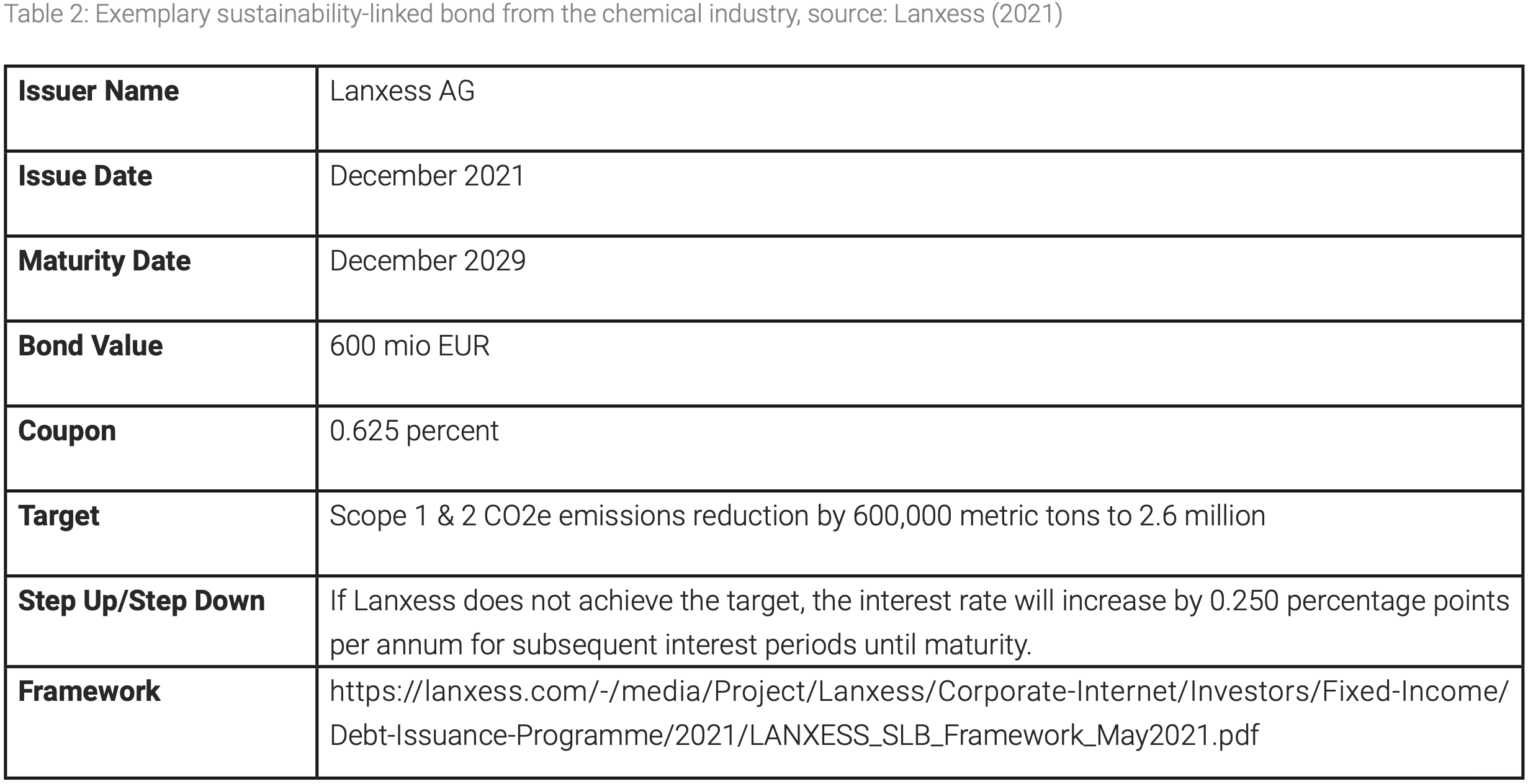

Sustainability-linked bonds (SLBs) are one type of sustainability-linked debt, which the International Finance Corporate (IFC, World Bank Group) recently called “one of the fastest-growing corners of finance” (IFC, 2023). Their unique feature is that future sustainability targets are directly linked to cost of capital through coupon step up (or down) payments. Effectively that means that a borrower commits to certain sustainability targets in the future and incurs a financial penalty when missing them. For the investor on the other hand, it means that in case the issuer does not follow through on their promise they get financially compensated. Table 2 shows an example of a sustainability-linked bond from the chemical industry.

SLBs are general purpose financial instruments and differ conceptually from green bonds, which are use-of-proceeds type of instruments. The difference in design allows sustainability-linked bonds to be applied more generally and to finance the transition of not yet green activities (forward looking Key Performance Indicators for sustainability performance). On the other hand, the proceeds of a green bond must be allocated to activities which are already green (backwards looking). This likewise means that while a SLB can be used for refinancing of any maturing security, a green bond can only refinance green activities. Overall, the hypothetical amount of issuance for SLBs is unlimited – any bond issued could be sustainability-linked – while the amount feasible to be issued as green bonds is limited to the volume of existing green activities. Other important differences include how the greenness is priced: While the Greenium for green bonds is determined in the market, SLBs have step up (or down) or penalty payments as legally enforceable covenants. Covenants are by no means a new concept in finance, predating their use in SLBs, and therefore easily applicable.

Still, in the nascent markets greenwashing concerns are not negligible. Unambitious or irrelevant targets may delay real progress. For climate change, especially in energy related sectors, all three emission scopes should be addressed. Absolute emission reductions should be prioritized over emission intensity improvements. In Signalling Theory (Spence, 1973), a signal must be costly to be credible.

Thus, imposing substantial penalties for missing targets are key. Here the devil may be in the detail: Do payments occur throughout the duration of the bond and accumulate when targets continue to be unmet or is there only a once off payment close to maturity? Ul Haq and Doumbia (2023) point out structural challenges while Erlandsson et al. (2022) offer a risk-neutral present value scenario approach for the pricing of step-down structures.

There are some support resources available to foster SLB uptake and ensure their integrity, though so far these are voluntary. For example, the International Capital Market Association (ICMA) has published Sustainability-Linked Bond Principles including an illustrative KPIs registry (ICMA, 2023). It is notable that the language around penalties for missing targets is soft and indicates optionality, despite being recognised as a key feature:

“The cornerstone of an SLB is that the bond’s financial and/or structural characteristics can vary depending on whether the selected KPI(s) reach (or not) the predefined [Sustainability Performance Target(s)], i.e. the SLB will need to include a financial and/or structural impact involving trigger event(s).“ The Climate Bonds Initiative (CBI) also issues guidance for sustainability-linked bonds as transition finance instruments (CBI, 2022a). These specifically stress the importance of strong structures around call dates and KPI observation dates.

Increased scrutiny can be observed as the sustainable debt market is maturing. This is for example evident in increasing amount of green bonds being rejected by CBI because of quality concerns (CBI, 2022b): 1 in 4 US Dollars did not meet their standards. The majority of the excluded bonds originated from China.

Yet the bond market is not the only place where sustainability metrics get linked to cost of capital. Sustainability- linked loans (SLLs) are similarly becoming popular. In 2019, specialty chemical firm Kemira agreed on three sustainability KPIs for its five year 400 mio EUR revolving credit: emission efficiency, generating half its revenue from products enhancing customers’ resource-efficiency and maintaining the highest rating from external rater EcoVadis (Kemira, 2019). Other examples of industrial firms taking SLLs include DSM, Indorama Ventures, Solvay, and Stora Enso.

The flexible design of linking capital cost to sustainability indicators naturally allows to factor in different facets of sustainability, beyond climate change mitigation. For the chemical industry, indicators revolving around recycling and pollution prevention seem sensible – a conceivable KPI could be the phase out of PFAS. The example of Lanxess’ 1 bn EUR revolving credit facility demonstrates that also social goals are feasible: Interest rates are not only linked to the successful reduction of its CO2e emissions (Scope 1) but also raising the share of women on the top three management levels (Lanxess, 2021). This case also highlights that multiple targets can easily be featured in the same sustainable debt instrument.

Even if a company does not participate in the sustainable finance market, the traditional corporate financing of a firm will also be affected by sustainability. “ESG” – the acronym for environmental, social, and governance factors – is considered by rating agencies when assessing credit worthiness (see for example Moody’s scorecard (Moody’s, 2022).

Conclusion

Overall, the chemical industry could play a key enabler role in the sustainable transition of our economy. While there are many challenges to be resolved, the chemistry underlying supply chains especially in the manufacturing industries could be the engine of innovation.

Greenwashing poses a real threat and must be managed as a risk. The underlying targets for sustainability-linked debt must be ambitious and relevant, and penalties for missing targets substantial. While the sector in the past had been “a blind spot” (Hawker, 2021) for investors, the increased interest will also bring more scrutiny. Additionally, changing regulation is adding to pressure in transition risk.

To unlock the power of the sector, significant investment is needed. Innovative sustainable finance instruments when applied appropriately could hereby be a catalyst for change. Sustainability-linked debt has successful been obtained by firms in the sector. It could be a key tool to both raise funds for the transition and credibly communicate transition plans to capital providers.

References

BBC (2017). BP sells Forties North Sea pipeline to Ineos. BBC News. https://www.bbc.com/news/uk-scotland-scotland-business-39476674

Bousso, B. (2020). BP sells petchems arm for $5 billion in energy transition revamp. Reuters. https://www.reuters.com/article/us-ineos-bp-petrochemicals-idUSKBN2400WQ

CBI (2022a). Guidance for sustainability-linked bonds as transition finance instruments. https://www.climatebonds.net/market/slbs

CBI (2022b). 3 in every $4 dollars of green bonds issuance meets standards https://www.climatebonds.net/resources/reports/3-every-4-dollars-green-bonds-issuance-meets-standards

ChemSec (2022). https://chemsec.org/investors-with-8-trillion-call-for-phase-out-of-dangerous-forever-chemicals/

ClientEarth (2023). Greenwashing Files – Ineos. https://www.clientearth.org/projects/the-greenwashing-files/ineos/ (accessed 17.09.2023)

Deloitte (2022). 2023 Chemical industry outlook. https://www2.deloitte.com/us/en/pages/energy-and-resources/articles/chemical-industry-outlook.html (accessed 16.09.2023)

Energy Transition Commission (2020). Making Mission Possible. https://www.energy-transitions.org/wp-content/uploads/2020/09/Making-Mission-Possible-Full-Report.pdf

European Commission (2017), Joint Research Centre, Boulamanti, A., Moya, J., Energy efficiency and GHG emissions – Prospective scenarios for the chemical and petrochemical industry, Publications Office, 2017, https://data.europa.eu/doi/10.2760/20486 (accessed 16.09.2023)

European Commission (2020). EU Taxonomy Regulation. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32020R0852

European Commission (2023a). Chemicals. https://single-market-economy.ec.europa.eu/sectors/chemicals_en (accessed 16.09.2023)

European Commission (2023b). Delegated Regulation C(2023) 3851. https://finance.ec.europa.eu/system/files/2023-06/taxonomy-regulation-delegated-act-2022-environmental_en_0.pdf

European Commission (2023c). Environnent – Chemicals. https://environment.ec.europa.eu/topics/chemicals_en (accessed 16.09.2023)

European Commission (2023d). Chemicals strategy. https://environment.ec.europa.eu/strategy/chemicals-strategy_en (accessed 16.09.2023)

Flammer, C. (2021). Corporate green bonds, Journal of Financial Economics, 142 (2), 499-516. https://doi.org/10.1016/j.jfineco.2021.01.010.

Flesher, J. (2023). 3M reaches $10.3 billion settlement over contamination of water systems with ‘forever chemicals’. AP News. https://apnews.com/article/pfas-forever-chemicals-3m-drinking-water-81775af23d6aeae63533796b1a1d2cdb

GreenWatch (2022). See https://greenwatch.ai/ for more information.

Hawker, E. (2021). Chemicals sector faces the acid test. ESG Investor. https://www.esginvestor.net/chemicals-sector-faces-the-acid-test/

Hoepner, A. & Schneider, F. (2022a). Disclosure without Solution: First Evidence from Scope 3 Reporting in the Oil and Gas Sector. Michael J. Brennan Irish Finance Working Paper Series Research Paper No. 22-13, http://dx.doi.org/10.2139/ssrn.4100089.

Hoepner, A. & Schneider, F. (2022b) Exit vs Voice Vs Denial of (Re)Entry: Assessing investor impact mechanisms on corporate climate transition. Working Paper. https://dx.doi.org/10.2139/ssrn.4193465.

ICIS (2021). European chemicals industry faces €1.5bn carbon bill. https://www.icis.com/explore/resources/news/2021/05/06/10635840/european-chemicals-industry-faces-1-5bn-carbon-bill/ (accessed 17.09.2023)

ICMA (2023). Sustainability-linked Bond Principles. https://www.icmagroup.org/sustainable-finance/the-principles-guidelines-and-handbooks/sustainability-linked-bond-principles-slbp/

IEA (2023). Chemicals. https://www.iea.org/energy-system/industry/chemicals (accessed 16.09.2023)

IEA (2018). The future of petrochemicals. https://www.iea.org/reports/the-future-of-petrochemicals

IFC (2023). Making Sustainability-Linked Bonds More Impactful. https://www.ifc.org/en/insights-reports/2023/making-sustainability-linked-bonds-more-impactful#:~:text=The%20market%20for%20sustainability%2Dlinked,billion%20issued%20globally%20in%202021.

IIHC (2023). Open Letter. https://chemsec.org/app/uploads/2023/09/Open-letter_Ensuring-progressive-and-truly-sustainable-chemical-criteria-within-the-EU-Taxonomy-Regulation.pdf

IMDB (2008). Breaking Bad. https://www.imdb.com/title/tt0959621/characters/nm0186505 (accessed 16.09.2023)

Ineos (2018). INEOS completes $80m investment to extend the life of Clipper South, its Southern North Sea gas field. https://www.ineos.com/news/ineos-group/ineos-completes-$80m-investment-to-extend-the-life-of-clipper-south-its-southern-north-sea-gas-field/

InfluenceMap (2023). Lobby Map Scores. https://lobbymap.org/LobbyMapScores (accessed 17.09.2023)

Kary, T. & Beene, R. (2022). 3M Will Stop Producing ‘Forever Chemical’ PFAS by End of 2025. Bloomberg News. https://www.bloomberg.com/news/articles/2022-12-20/3m-mmm-will-stop-producing-forever-chemical-pfas-by-end-of-2025

Kemira (2019). Kemira signs revolving credit facility linked to sustainability targets. https://www.kemira.com/company/media/newsroom/releases/kemira-signs-revolving-credit-facility-linked-to-sustainability-targets/

Lanxess (2021). News Release. https://lanxess.com/-/media/Project/Lanxess/Corporate-Internet/Media/Press-Releases/2021/11/211123_LANXESS-successfully_places_EUR_600_million_sustainability_bond.pdf

Maher, K. & McWhirter, C. (2017). DuPont Settlement of Chemical Exposure Case Seen as ‘Shot in the Arm’ for Other Suits. The Wall Street Journal. https://www.wsj.com/articles/dupont-chemours-settle-teflon-chemical-exposure-case-for-671-million-1486987602

Moody’s (2022). Rating Methodology. https://ratings.moodys.com/api/rmc-documents/389870 (accessed 17.09.23)

Oliver Wyman (2023). The Climate Action Navigator. https://climateactionnavigator.oliverwymanforum.com/home (accessed 16.09.2023)

Oliver Wyman (2021). Chemical industry outlook for 2022 and beyond. https://www.oliverwyman.com/our-expertise/insights/2022/jan/chemical-industry-outlook-for-2022-and-beyond.html

PlanetTracker (2023). Greenwashing Hydra Report. https://planet-tracker.org/wp-content/uploads/2023/01/Greenwashing-Hydra-3.pdf (accessed 16.09.2023)

Reuters (2022). INEOS offers to develop test shale gas site in Britain. https://www.reuters.com/business/energy/ineos-offers-develop-test-shale-gas-site-britain-2022-04-10/

Richardson, K., Steffen, W., Lucht, W., Bendtsen, J., Cornell, S.E., Donges, J.F., Drüke, M., Fetzer, I., Bala, G., von Bloh, W., Feulner, G., Fiedler, S., Gerten, D., Gleeson, T., Hofmann, M., Huiskamp, W., Kummu, M., Mohan, C., Nogués-Bravo, D., Petri, S., Porkka, M., Rahmstorf, S., Schaphoff, S., Thonicke, K., Tobian, A., Virkki, V., Weber, L. & Rockström, J. (2023). Earth beyond six of nine planetary boundaries. Science Advances 9, 37. DOI: 10.1126/sciadv.adh2458

Sato, M. Gostlow, G., Higham, C., Setzer, J. & Venmans, F. (2023). Impacts of climate litigation on firm value. Working Paper. https://www.lse.ac.uk/granthaminstitute/publication/impacts-of-climate-litigation-on-firm-value/

SEC (2023). Commitments and Contingencies Environmental Matters. https://www.sec.gov/Archives/edgar/data/833444/000083344421000011/R28.htm

Spence, M. (1973). Job Market Signaling. The Quarterly Journal of Economics, 87 (3), 355-374. https://doi.org/10.2307/1882010

Ul Haq, I. & Doumbia, D. (2023). Structural Loopholes in Sustainability-Linked Bonds. Policy Research Working Paper. https://documents1.worldbank.o r g / c u r a t e d / e n / 0 9 9 2 3 7 4 1 0 0 6 2 2 2 3 0 4 6 / p d f /IDU0e099a50307f86045a80b33201d0b7057cedf.pdf (accessed 17.09.2023)

Weller, M.-P. & Tran, M.-L. (2022). Climate Litigation against companies. Climate Action, 1(14). https://doi.org/10.1007/s44168-022-00013-6

* University College Dublin (UCD), Dublin, Ireland.

** Platform on Sustainable Finance, Brussels, Belgium.

[1] See for example recent developments of regulation adopted in California or the phase in of Scope 3 as part of Paris-Aligned Benchmarks (PABs).

[2] The author is research co-lead at GreenWatch.

[3] This is in line with the recent publication of the Sustainable Finance Disclosure Regulation (SFDR) Regulatory Technical Standards (RTS), see paragraph 39 here: https://www.esma.europa.eu/sites/default/files/2023-12/JC_2023_55_-_Final_Report_SFDR_Delegated_Regulation_amending_RTS.pdf

[4] See the European Chemicals Agency (ECHA)’s website for more information, where PFAs are aptly listed as a “Hot Topic”: https://echa.europa.eu/hot-topics/perfluoroalkyl-chemicals-pfas.