Digitalization in the process industries – Evidence from the German water industry

Research on the adoption of digital technologies has largely omitted the process industries. In this study, we address this research gap by presenting empirical evidence from a questionnaire survey comprising 86 responses from members of the German Water Partnership (GWP) association. Our results indicate that firms in the water industry lay emphasis on projects harnessing digital technologies, while the execution and implementation still faces significant challenges that we discuss below. Correlation analysis reveals that firms that have interlaced conventional business strategy with IT strategy stronger prioritize the development new business models in the course of digitalization than their counterparts who do not have a digital business strategy. Due to the new ways of value creation, delivery, and capture enabled by digital technologies, we evaluate the usefulness of a concept named the layered modular product architecture in context of the process industries and relate it to the need for developing a digital business strategy. We close this article by deducing several implications for managers.

1 Introduction

Recent developments in digital technologies bring about considerable business opportunities but also impose significant challenges on firms in all industries. While some industries, e.g., newspapers, have already profoundly reorganized the mechanisms of value creation, delivery, and capture during the course of digitalization (Karimi & Walter, 2015, 2016), many process-oriented and asset intensive industries have not yet fully evaluated and exploited the potential applications (Rigby, 2014). Although the process industries have successfully used advancements in technologies to optimize processes in the past (Kim et al., 2011), digitalization poses an unprecedented shift in technology that exceeds conventional technological evolution (Svahn et al., 2017). Driven by augmented processing power, connectivity of devices (IoT), advanced data analytics, and sensor technology, innovation activities in the process industries now break away from established innovation paths (Svahn et al., 2017; Tripsas, 2009). In contrast to prior innovations that were primarily bound to physical devices, new products are increasingly embedded into systems of value creation that span the physical and digital world (Parmar et al., 2014; Rigby, 2014; Yoo et al., 2010a). On this new playing field, firms and researchers are jointly interested in the organizational characteristics and capabilities that are required to gain a competitive advantage (e.g. Fink, 2011). Whereas prior studies cover the effect of digital transformation on innovation in various industries like newspaper (Karimi and Walter, 2015, 2016), automotive (Henfridsson and Yoo, 2014; Svahn et al., 2017), photography (Tripsas, 2009), and manufacturing (Jonsson et al., 2008), there is a relative dearth of studies that cover the impact of digital transformation in the process industries (Westergren and Holmström, 2012).

The process industries are characterized by asset and research intensity, strong integration into physical locations, and often include value chains that are complex and feature aspects of rigidity (Lager et al., 2013). Multiple sectors like the chemical industry, water industry, food and beverage, generic pharmaceuticals, utilities, as well as forest and steel fall into this category (Lager et al., 2013). Under conditions of rapid environmental developments like technological advancements, the process industries’ ability to respond to change is often limited in the short term (Lager et al., 2013).

In many countries, industry associations drive discussions about digitalization. In allusion to the concept of “Industry 4.0” the German Water Partnership (GWP) association defines the term “Water 4.0” as the application of digital technologies for the evolution of holistic cyber-physical-systems that enable efficient, real-time monitored, and reliable water supply with a maximum amount of transparency for producers and users [italics added by authors] (GWP, 2016, p.4). In order to evaluate how members of GWP translate the notion of Water 4.0 into their business reality, in this study we investigate the water industry’s status quo in digitalization.

In this paper, we pursue several objectives. First, we introduce the concept of the layered modular product architecture into the process industries and discuss its applicability. Second, we present descriptive data from a questionnaire survey conducted within the GWP to provide an overview of key digitalization priorities and challenges. Third, we analyze the relationship between digital business strategy and a firm’s propensity to engage in business model innovation in more detail. Finally, we discuss how business model innovation is related to a layered modular product architecture and conclude with implications for practitioners.

2 Digitalization in the water industry – A new innovation logic for the digital age

The interchangeable use of the terms digitalization and digitization is misleading in the debate about digital transformation. To clarify the meaning of digitalization and distinguish it from digitization, a group of renowned information systems scholars refer to digitalization as “the transformation of socio-technical structures that were previously mediated by non-digital artifacts or relationships into ones that are mediated by digitized artifacts and relationships. Digitalization goes beyond a mere technical process of encoding diverse types of analog information in digital format (i.e., “digitization”) and involves organizing new socio-technical structures with digitized artifacts as well as the changes in artifacts themselves” (Yoo et al., 2010b, p. 6). An example for digitalization-driven changes of socio-technical structures in the process industries is the transition from reactive maintenance towards predictive maintenance. In the latter, a network of connected sensors enables plant operators to determine the residual life distribution of a system’s critical components in order to optimize the maintenance schedule and improve the overall reliability of the system (Kaiser and Gebraeel, 2009). This kind of innovation affects socio-technical structure. For example, reliable water supply systems have a tremendous impact on social life and also affect the economic prosperity of entire regions (United Nations Report, 2016).

In the transformation process of digitalization, practitioners and scholars alike are specifically interested in how the system of value creation and capture is changing (Barua et al., 2004). In this regard, a growing stream of empirical research focusses on the impact of digital technologies on value creation through new product development (Marion, et al., 2015). In this regard, the changing nature of product architectures is presented as a major challenge for innovation managers (Yoo et al., 2012; Yoo et al., 2010) but also entails tremendous business opportunities (Rigby, 2014).

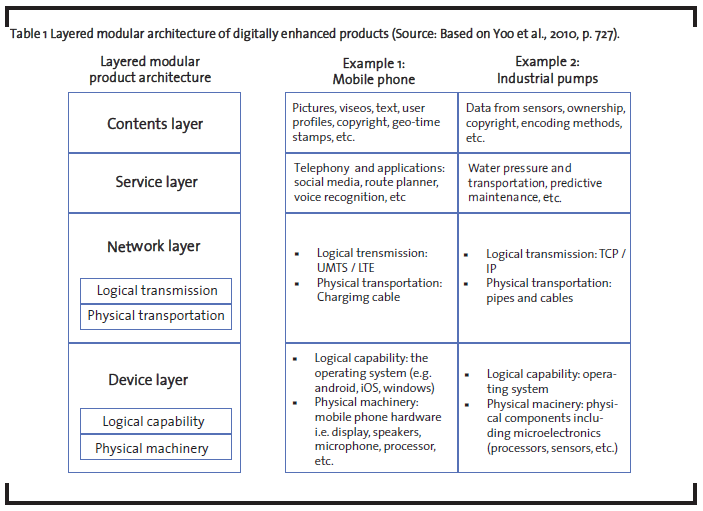

2.1 The layered modular architecture of digital technology

Product designs can be described following two types of product architecture: integral and modular (Henderson and Clark, 1990; Sanchez and Mahoney, 1996; Ulrich, 1995). While an integral product architecture is characterized by tightly coupled elements that are highly interdependent and aim at optimizing the product as a whole, a modular architecture is defined by standardized interfaces that allow for facile exchanges of the components, which, in turn, enables changes in the functionality of the product (Ulrich, 1995; Yoo et al., 2010a). Modular products are therefore popular in environments that require high levels of flexibility. In a new organizing logic that is driven by an increasing implementation of digital technologies into physical products, additional layers of value creation emerge that uncouple the functionality of a product from its physical components (Yoo et al., 2010a). As illustrated in Table 1, the additional layers comprise a network layer, a service layer, and a contents layer that build on top of the physical device (Yoo et al., 2010a). Each layer fulfills different functions in the product architecture. As Yoo et al. (2010a) delineate, the device layer includes a physical machinery layer (e.g. hardware components) and a logical capability layer (e.g. operating system) that provide control over the physical device and enable connections to other layers. Similarly, the network layer consists of two layers, one for physical transport (cables, pipes, transmitters, etc.) and one for logical transmission (e.g. TCP/IP, peer-2-peer). In the service layer all functionalities are bundled into an interface that serves the user (e.g. mobile applications, addressable pump in an operating system). This layer is supplied by the overarching contents layer that stores all data (text, video, sound, etc.) and metadata (copyright, geo-tags, etc.).

The evolution from integral to modular product architectures enabled innovators to create new products by combining modules in novel ways. Today, the layered modular architecture of digitally enhanced products provides firms with the opportunity to innovate and compete on each layer largely without affecting offers on other layers. But still, the layered architecture invites firms to offer integrated solutions that span more than one layer to leverage synergies between them. For example, a device producer might profit from offering solutions on the content layer in order to learn how clients use their content with the objective to further adapt the device to the clients’ needs.

Although being primarily applied in industries that fabricate electronic products, the layered modular product architecture also proves useful for the process industries, in which products are often raw materials rather than digital savvy components (Lager et al., 2013). However, due to the increasing engagement in services and platforms that are offered as complementary values to the initial physical product, firms find themselves competing and collaborating on new layers of the product architecture, possibly facing novel competitive landscapes (Bharadwaj et al., 2013a). The environment of rapidly evolving technologies requires continuous reflection about the firm’s position in the network of value-creation, which draws attention to the importance of strategic partnerships which enable the leveraging of network resources to boost firm performance (Lavie, 2006). Regarding the positioning of firms in value networks, Pagani (2013) proposes that firms who position themselves at what she refers to as control points i.e. the positions of greatest value and/or power in a system, are able to influence how profits are allocated and eventually obtain a competitive advantage. In a layered modular architecture, each layer comprises its own control points that distinguish the success between firms competing or collaborating on the same layer. Collaborating with firms that hold control points on different levels of the architecture might result in complementary resource configurations and, thus, unlock new market opportunities. Throughout all actions that a firm pursues in this product architecture, alignment between innovation activities and the position in the value network should be considered. In the course of digitalization, ensuring organizational alignment between internal activities and the external environmental circumstances is a task for strategic management, which is why firms should have a digital business strategy.

2.2 The role of digital business strategy

During the last decades, IT strategy has been subordinate to, and in the best case, in alignment with conventional business strategy (Bharadwaj et al., 2013a). Over a long period of time, influential decision makers perceived information technology as a supporting factor that was not designed to grant a competitive advantage over competitors, and therefore neglected it as an integral component of business strategy at the corporate level. In recent years, products have increasingly become digitally connected and are now able to be embedded into systems of value creation that exceed physical boundaries (Rigby, 2014). Scholars argue that IT, and, more specifically, an integrated IT strategy has become a potential source of competitive advantage (Bharadwaj et al., 2013a; Bharadwaj et al., 2013b; Pagani, 2013). In this context, digital business strategy refers to an “organizational strategy formulated and executed by leveraging digital resources to create differential value” (Bharadwaj et al., 2013a, p. 472). Due to the new technological and personnel requirements and the uncertain returns that the implementation of digital technologies bring about, formulating a digital business strategy can produce internal consistency between digital transformation activities. In this study, we therefore investigate how many firms in our sample have developed a digital business strategy and who is in charge of it.

3 Methodology

Data collection was performed among members of the German Water Partnership (GWP), which includes original equipment manufacturers, plant operators, consultancies, construction firms, chemical providers, research institutes, and financing partners. GWP forwarded our questionnaire survey to one contact person inside each of the 350 member companies and reminded them with two mails to participate. After five weeks, 86 respondents completed the survey, resulting in a response rate of 24.6% calculated in relation to the number of members in the association. Respondents mainly hold the position of chief executive officer, head of department, and related functions that qualify them as appropriate respondents for the topics covered in this survey. On average, respondents further bring over 17 years of industry experience, while they spent 13.5 years in the company they currently work for.

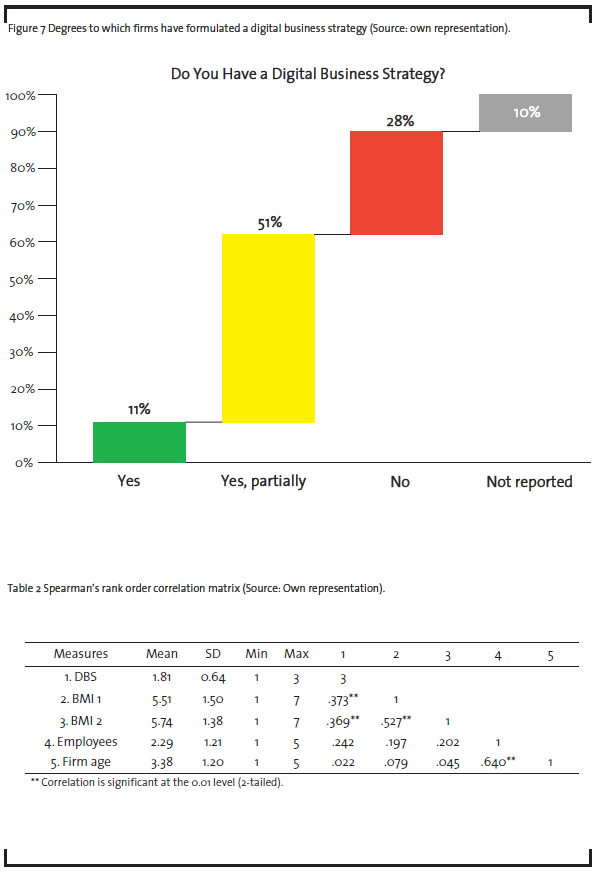

We operationalized our measurements as follows. In order to evaluate the current key aspects of digitalization in the water industry, we draw on a survey previously conducted by Siemens among its clients in Germany and adapted the wording of some items (Siemens, 2014). Concerning digital transformation, the survey covers the topics of firm priorities, potential benefits, internal and external resistance, and digital business strategy. Respondents evaluated firm priorities on a seven-point Likert scale offering continuous degrees of importance: 1 = very important to 7 = not important at all. Potential benefits as well as internal and external sources of resistance were equally assessed on a Likert scale using a range of agreement from 1 = fully agree to 7 = fully disagree. We were also interested in how far respondent firms had formulated a digital business strategy, for which we offered four different choices: 0 = No response, 1 = No, 2 = Yes, partially, 3 = Yes. Further, we investigated who was responsible for developing a digital business strategy and assessed if the respondents’ firms had set up a central unit for digitalization related issues. Additionally, we performed Spearman’s rank order correlation between the perceived importance of business model innovation and the degree to which a digital business strategy exists. The results were calculated using SPSS version 23.

4 Results

In order to assure the fit of our findings with the water industry’s general perspective on digitalization, we included all respondents in our analysis. Although we herewith accept answers from heterogeneous industry segments in our data set, this approach has the advantage of retaining a broad scope of perspectives and therefore contributes to a more holistic view on the state of digitalization in the water industry. In the descriptive representations below, the graphs consider the top two boxes from the Likert scale i.e. “important” and “very important”.

4.1 Digital transformation priorities

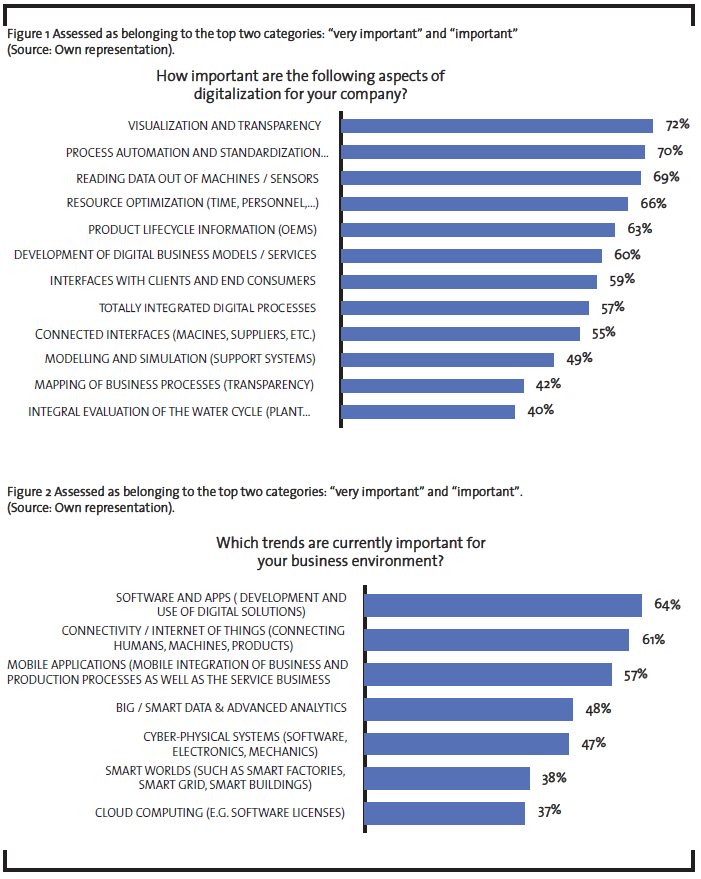

First, respondents classified which functions or purposes they address with digital technologies and which of them are most relevant for their firm. According to the results depicted in Figure 1, more than two third of all respondents prioritized visualization and transparency, process automation and standardization, and data extraction from machines and sensors as key functional areas that are currently addressed. Companies further underline the optimization of resources and the use digital solutions to gain transparency in their product lifecycles.

Figure 2 presents the major digitalization-related trends that are currently important for the respondents’ firm environment. Most notably, the development of software and apps is a major topic in conjunction with machine connectivity i.e. the internet of things, and mobile applications that enable the integration of production processes with other functional areas. Further, cloud computing is perceived as an important digital solution in the business environment by 37% of respondents.

4.2 Potential benefits of digital transformation

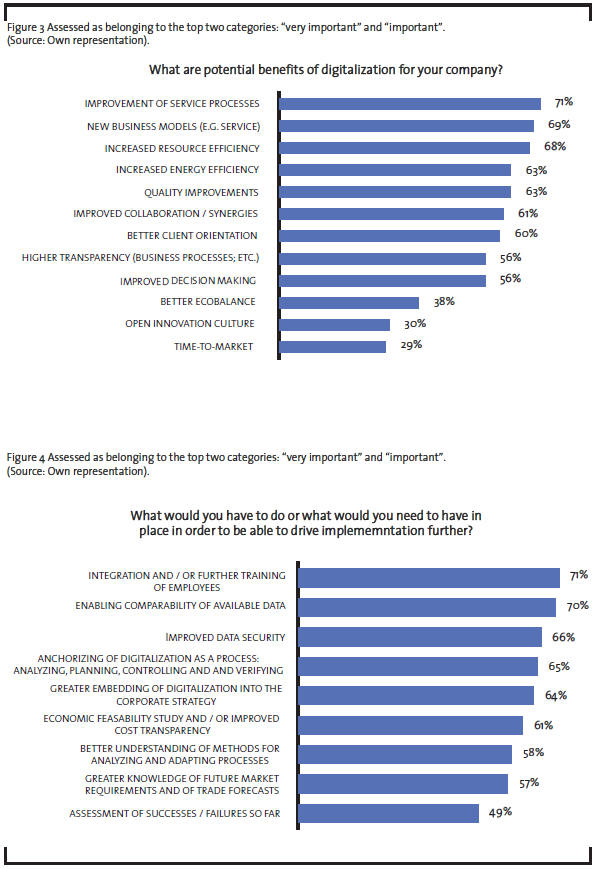

By engaging in digital transformation, GWP members aim to achieve various benefits for their companies, which are shown in Figure 3. According to the results, more than two out of three respondents expect to improve their service processes. Further, the participating companies see digitalization as a means for developing new business models and gaining higher resource and energy efficiency. In addition, digitalization of communication and interaction between parties is expected to not only increase collaboration efficiency but also enhance the relationship between firms and their clients by enabling stronger client orientation (60%). The unprecedented amount of available data enables firms to gain higher process transparency (56%), which, in turn, facilitates managerial decision-making (56%). Respondents have lower expectations when it comes to increasing environmental performance, establishing an open innovation culture, and shortening time-to-market.

Figure 4 summarizes which circumstances would facilitate the implementation of digital technologies. In this context, 71% of all firms agree that the training and inclusion of employees is the most relevant shortcoming. In addition, data should be made compatible between applications and platforms (70%) and improved data security (66%) is supposed to increase confidence in the application of digital technologies. Implementing digitalization as a process of analyzing, planning, directing, and controlling/verifying is perceived to be an additional driver (65%). Respondent firms acknowledge that digitalization needs to be further included in business strategy (64%) and support that evaluation of prior successful and failed projects might support implementation of digitalization.

4.3 Resistance to digital transformation

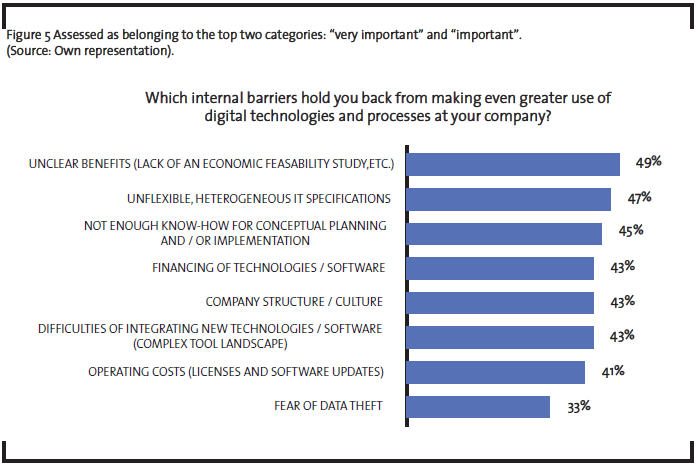

Besides the drivers and enabling technologies for digital transformation, we assessed the most influential internal and external barriers. As Figure 5 indicates, the most important internal barriers are unclear benefits (49%), ambiguous IT specifications (47%), and a lack of sufficient internal knowhow for planning and implementation (45%). Fear of data theft is a considerable impediment for one third of the companies in our sample.

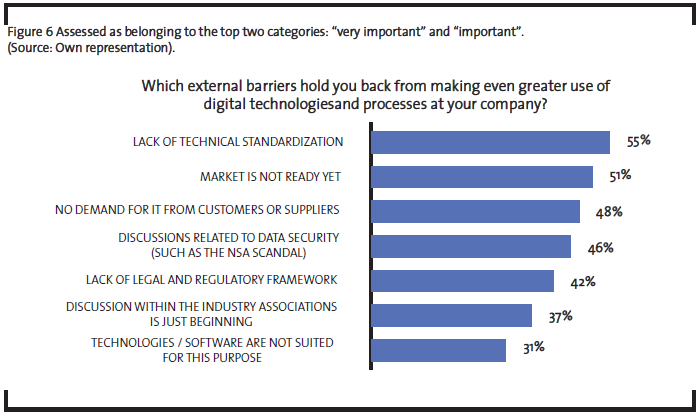

The barriers that reside within the organizations’ external environment are summarized in Figure 6. Most prominent in this respect is the lack of technical standardization (55%). The following two barriers, namely the missing demand for digital solutions from customers and suppliers (51%), and the perception that the market is not ready yet (48) suggest that producers and clients in the water industry are more hesitant to apply digital technologies when being compared to other industries (Siemens, 2014). The unsatisfying progress in discussions within associations and the lack of a legal and regulatory framework are moderately important barriers. Only 31% of respondents think that technology itself is the bottleneck for implementation.

4.4 Digital business strategy

In order to assess whether our respondents were sufficiently knowledgeable to be considered for further analysis, we analyzed their functions in the company in a key respondent check. According to the respondents’ position in the company, respondents mainly hold top-level management functions but also middle management and other functions that account for substantial knowledgeable about the firm’s strategy are included in the analysis. Figure 7 depicts the number of firms in the sample that have completely or partially formulated a digital business strategy. The responses show that while half of the firms have partially formulated a digital business strategy only 11% have already accomplished this task. Besides 10% of non-reported answers, 28% of the companies in the sample have not yet developed a strategy that integrates digital transformation objectives.

In a consecutive question not shown in the figure, we were interested who is responsible for formulating the digital strategy for the company. In 52% of responses, the executive board is responsible for creating a digital business strategy in collaboration with IT experts. In addition, 15% have established a digitalization team to implement digitalization as a process into the company while in other firms corporate strategy (6%), the executive board alone (6%), IT (5%), and others (15%) are responsible for this task.

4.5 Correlation analysis

With the aim to explore the relationship between digital business strategy and the propensity to engage in business model innovation in more detail, we performed an additional correlation analysis. As we use both ordinal and continuous scales for our measures, we use Spearman’s rank order correlation and present the results in Table 2. To perform correlation analysis, we used the degree to which firms have formulated a digital business strategy (DBS) as well as indicators for the willingness to pursue business model innovation (BMI). The latter includes “Development of digital business models / services” (BMI1) from the list of digitalization opportunities in Figure 1, and “New business models (e.g. service)” (BMI2) from the list of digitalization priorities in Figure 2. Further, we include the number of employees and the firm age. We find that having a digital business strategy has a weak/moderate positive correlation with prioritizing business model innovation as an opportunity (ρ=.373; p<0.01) and internal priority (ρ=.369; p<0.01).

5 Discussion

In the German water industry, digital technologies are regarded as important drivers for achieving superior results in diverse functional areas. In congruence with the concept Water 4.0 the gathering, transmission, and analysis of homogenized data is used for process automation, optimization, and improved decision making, among others. As the results from our study indicate, firms in our sample consider efficiency-related innovations as important cornerstones of digitalization, but at the same time acknowledge novel business opportunities. Specifically, offering new services and developing novel business models are important objectives. In this concern, correlation analysis revealed that developing new business models is more important to firms that have formulated a digital business strategy. As a business model can be best described by the process of value creation, delivery, and capture (Teece, 2010) it is evident that in the course of digitalization the business model of almost every industry will encounter significant changes in one or all of the three dimensions. Only through formulation of a digital business strategy that aligns digitalization efforts across multiple organizational functions, firms will be able to sustain advantages that were gained through business model innovation, as business models are sufficiently generative and easy to imitate (Teece, 2010).

Car manufacturer Volvo has demonstrated the value of developing a digital business strategy in its “connected cars” initiative from 2010, in which they included guidelines for the use of platforms and cloud technology (Svahn et al., 2017). Despite the success in transformation, the profound implementation of digital technologies into Volvo’s DNA made the car manufacturer experience organizational resistance that was caused by a shift in organizational culture and identity (Svahn et al., 2017; Tripsas, 2009). In a study based in the camera industry, Tripsas (2009) concludes that coping with changes in firm identity can be catalyzed by firm strategies that connect the use of novel technologies to internal capabilities, routines, and beliefs.

In the GWP, the majority of firms state that investments in integration and training of employees (71%) would accelerate the implementation of digital technologies. At the same time, 45% indicate that internal know-how about new technologies is not sufficient. The numbers support the impression that the speed of technology development is faster than what organizations are able or willing to implement. Research on technology acceptance delineates that the speed of technology adoption is a function of the technology’s perceived usefulness and ease of use (Venkatesh & Davis, 2016). Coining an organizational culture that embraces technological advancements with curiosity and playfulness is the duty of top-level management, while communication of achievements and use-cases throughout the company might foster the perceived usefulness.

Digital technologies offer numerous opportunities for business model innovation. Formulating a digital business strategy might serve as a starting point for developing novel business models that might even be multi-sided. Multisided business models are not only interesting for digital leaders (e.g. Google, Facebook, YouTube) but for almost every other company. The multi-sidedness of a business model can be perceived as a firms ability to capture value from one business through various revenue streams, possibly residing within different layers of the product architecture. In the example of an industrial pump, the manufacturer might generate sales not only by selling the pump (device layer) but also by offering additional value like predictive maintenance as a service, which, in turn, is nurtured from the content layer through analyzing a continuous stream of real-time data (Bharadwaj et al., 2013a).

Evidence from academic literature highlights the importance of customer and supplier readiness for increasing firm performance through digitalization (Barua et al., 2004). Respondents in our study indicate that a lack of market readiness (51%) and customer demand (48%) are major barriers for implementation of digital technologies. This raises the question in how far firms should engage in developing innovative digital solutions in the face of uncertain market conditions. As digitalization is a basic technology that affects all industries (Brynjolfsson and McAfee, 2014) it is only a matter of time until the entire market will be more familiar with digital solutions. Until then, firms that develop viable digital solutions might be able to profit from the early stage in the technology life cycle and strengthen their strategic position in this field.

The development of holistic and integrated solutions requires most firms to engage in collaboration with partner firms, because companies rarely cover all relevant layers in the digital product architecture on their own. Harnessing the resources of alliance partners i.e. network resources can provide firms with a competitive advantage and is a powerful tool for firms in uncertain environmental conditions (Lavie, 2006). An example for this is the collaboration of the utility company Eon and Google who together provide solar energy solutions for real estates in Germany. While the locally established company Eon is responsible for the hard ware, Google’s satellite data has all the information about the sun exposure of roofs. Potential customers are thus able to get a realistic calculation of the power generated by potential solar panels on their roofs. The joint service combines the hardware competence from a local incumbent (device layer) with meteorological and geographical data (content layer) into a convenient user experience. Eventually, Eon’s and Google’s complementarity of resources on different levels of the product architecture enables them to unlock new revenue streams.

6 Managerial implications

This study provides several implications for managers. First, firms that do not have a digital business strategy yet, should start to align and integrate IT strategy and business strategy to tackle implementation of digital technologies in a structured approach. Second, firms are not self-sufficient in the digital age and need strong collaboration partners. Therefore, managers might use the layered modular architecture as a starting point for identifying potential partner firms on different layers of the product architecture with the joint goal of developing holistic customer solutions. Third, firms across all industries have shown that digital technologies enable novel ways of creating, delivering, and capturing value. To position themselves, firms might experiment with novel business models themselves or gain access to them through acquisitions or collaborations. Fourth, digital transformation requires a shift in firm culture and identity, both of which are most notably coined by the firm’s top-management. Providing space for experimentation with new technologies and communication of prior results are viable means for increasing acceptance among employees.

7 Conclusion

In this work, the authors present a study on the state of digitalization in the water industry. We discuss the applicability of the layered modular product architecture in the process industries and assess the importance of having a digital business strategy. The results from our questionnaire survey indicate that the use of digital technologies is perceived as an important opportunity for business development in the future, while real-world implementation still faces significant challenges. Our results further support that firms who have formulated a digital business strategy are more inclined to develop new business models in the course of digital transformation.

8 Acknowledgements

We would like to speak out our special thanks to the German Water Partnership (GWP) for their support during the conception and data gathering phase of this study. The GWP is a joint initiative of the German private and public sectors, combining commercial enterprises, government and non-government organizations, scientific institutions and water-related associations. The fundamental aim of the GWP is to make the outstanding German engineering, know-how and experience in the water sector easily available to partners and clients all over the world (for further information visit http://www.germanwaterpartnership.de/).

Furthermore, we would also like to thank our interview partners for their valuable feedback and insightful comments.

References

Barua, A., Konana, P., Whinston, A. B., & Yin, F. (2004): An Empirical of Investigation of Net-Enabled Business Value. MIS Quarterly, 28(4), pp. 585–620.

Bharadwaj, A., El Sawy, O. A., Pavlou, P. A., & Venkatraman, N. (2013a): Digital Business Strategy: Toward a Next Generation of Insights. MIS Quarterly, 37(2), pp. 471–482.

Bharadwaj, A., El Sawy, O. A., Pavlou, P. A., & Venkatraman, N. (2013b): Visions and Voices on Emerging Challenges in Digital Business Strategy. MIS Quarterly, 37(2), pp. 633–635.

Brynjolfsson, E., & McAfee, A. (2014): The second machine age: Work, progress, and prosperity in a time of brilliant technologies, WW Norton & Company.

Fink, L. (2011): How do IT capabilities create strategic value? Toward greater integration of insights from reductionistic and holistic approaches. European Journal of Information Systems, 20(1), pp. 16–33.

GWP (2016): Brochure “Water 4.0.” Retrieved August 18, 2017, from http://www.germanwaterpartnership.de/fileadmin/pdfs/gwp_materialien/GWP_Brochure_Water_4.0.pdf

Henderson, R. M., & Clark, K. B. (1990): Architectural innovation: The reconfiguration of existing product technologies and the failure of established firms. Administrative Science Quarterly, 35(1), pp. 9–30.

Henfridsson, O., & Yoo, Y. (2014): The Liminality of Trajectory Shifts in Institutional Entrepreneurship. Organization Science, 25(3), pp. 932–950.

Jonsson, K., Westergren, U. H., & Holmström, J. (2008): Technologies for value creation: An exploration of remote diagnostics systems in the manufacturing industry. Information Systems Journal, 18(3), pp. 227–245.

Kaiser, K. A., & Gebraeel, N. Z. (2009): Predictive maintenance management using sensor-based degradation models. IEEE Transactions on Systems, Man, and Cybernetics Part A:Systems and Humans, 39(4), pp. 840–849.

Karimi, J., & Walter, Z. (2015): The role of Dynamic Capabilities in responding to digital disruption: A factor-based study of the newspaper industry. Journal of Management Information Systems, 32(1), pp. 39–81.

Karimi, J., & Walter, Z. (2016): Corporate Entrepreneurship, Disruptive Business Model Innovation Adoption, and Its Performance: The Case of the Newspaper Industry. Long Range Planning, 49(3), pp. 342–360.

Kim, G., Shin, B., Kim, K. K., & Lee, H. G. (2011): IT Capabilities, Process-Oriented Dynamic Capabilities, and Firm Financial Performance. Journal of the Association for Information Systems, 12(7), pp. 487–517.

Lager, T., Blanco, S., & Frishammar, J. (2013): Managing R & D and innovation in the process industries. R&D Management, 43(3), pp. 189–195.

Lavie, D. (2006). The Competitive Advantage of Interconnected Firms: an Extension of the Resource- Based View. Academy of Management Review, 31(3), pp. 638–658.

Marion, T. J., Meyer, M. H., & Barczak, G. (2015): The influence of digital design and IT on modular product architecture. Journal of Product Innovation Management, 32(1), pp. 98–110.

Pagani, M. (2013): Digital Business Strategy and Value Creation: Framing the Dynamic Cycle of Control Points. MIS Quarterly, 37(2), pp. 617–632.

Parmar, R., Mackenzie, I., Cohn, D., & Gann, D. (2014): The New Patterns of Innovation. Harvard Business Review, 92(1), pp. 1–14.

Rigby, D. K. (2014): Digital-Physical Mashups. Harvard Business Review, 92(9), pp. 84–92.

Sanchez, R., & Mahoney, J. T. (1996): Modularity , Flexibility , and Knowledge Management in Product and Organization Design. Strategic Management Journal, 17, pp. 63–76.

Siemens. (2014): Germany 2014 Digitalization. Retrieved August 2, 2017, from https://m.siemens.com/en/about/core-topics/digitalization/media/pdf/20151119_SI_Kundenbefragung_Germany_EN.pdf

Svahn, F., Mathiassen, L., & Lindgren, R. (2017): Embracing Digital Innovation in Incumbent Firms: How Volvo Cars Managed Competing Concerns. MIS Quarterly, 41(1), pp. 239–253.

Teece, D. J. (2010): Business models, business strategy and innovation. Long Range Planning, 43(2–3), pp. 172–194.

Tripsas, M. (2009).:Technology, Identity, and Inertia Through the Lens of “The Digital Photography Company.” Organization Science, 20(2), pp. 441–460.

Ulrich, K. (1995): The role of product architecture in the manufacturing firm. Research Policy, 24(3), pp. 419–440.

United Nations Report. (2016): The United Nations World Water Development Report 2016 – Water and Jobs.

Venkatesh, V., & Davis, F. D. (2016): A Theoretical Extension of the Technology Acceptance Model: Four Longitudinal Field Studies. Management Science, 46(2), pp. 186–204.

Westergren, U. H., & Holmström, J. (2012): Exploring preconditions for open innovation: Value networks in industrial firms. Information and Organization, 22(4), pp. 209–226.

Yoo, Y., Boland, R. J., Lyytinen, K., & Majchrzak, A. (2012): Organizing for Innovation in the Digitized World. Organization Science, 23(5), pp. 1398–1408.

Yoo, Y., Henfridsson, O., & Lyytinen, K. (2010): The New Organizing Logic of Digital Innovation: An Agenda for Information Systems Research. Information Systems Research, 21(4), pp. 724–735.

Yoo, Y., Lyytinen, K., Boland, R., Berente, N., Gaskin, J., Schutz, D., & Srinivasan, N. (2010): The Next Wave of Digital Innovation-Opportunities and Challenges. Digital Challenges in Innovation Research, pp. 1–37.