Raw Material Excellence in the chemical industry, a game changer turning cost into value

Raw material spend across the specialty chemicals industry is accounting for approx. 35% to 40% of net sales, representing their single highest cost position. Across the entire chemicals industry sustainable raw material cost reduction is even wider and often competing with other objectives such as maximum security of raw material and indirectly own sales products supply, consistent quality, high supply chain flexibility, and the right level of complexity in the value chain. This article describes the evolution concept of value-chain oriented raw material management in the chemicals industry over the last 10 years, its individual components, and how first chemical companies have mastered their transformation to achieve the highest level of composite raw materials management performance, Raw Material Excellence. Procurement is no longer perceived as “cost center” but as “value driver” and hence instrumental for sustainable profits. In other words Raw Material Excellence is nothing less than a game changer.

1 Introduction

Over the last 10 years mid-size and large chemical companies have developed an innovative approach to raw material management. Additional functions along the value chain have accepted new roles in raw material management, e.g. quality control, product and application development, manufacturing, sales and marketing and controlling to name the key players. Cross-functionality is key to strive the balance between the above mentioned multi-dimensional objectives that have previously been perceived as incompatible (Leybovich, 2010; McPherson, 2016).

2 Raw material management – Raw Material Excellence

Exactly 10 years ago, some specialty chemical companies, e.g. manufacturers of coatings and additives, soon followed by companies serving other chemical segments such as fine chemicals, e.g. process flavors or vitamins, intermediates and pharmaceutical raw materials, e.g. high volume acids, alcohols or solvents, and even basic chemicals, e.g. fertilizers, have begun to transform the traditional way of sourcing.

The objective of this business model innovation has been to refine the role of raw materials from being a “pure cost” to the company associated with some latent to obvious risks to supply chain and sales of finished goods to own customers towards “value creating building blocks” (Gorin, 2016).

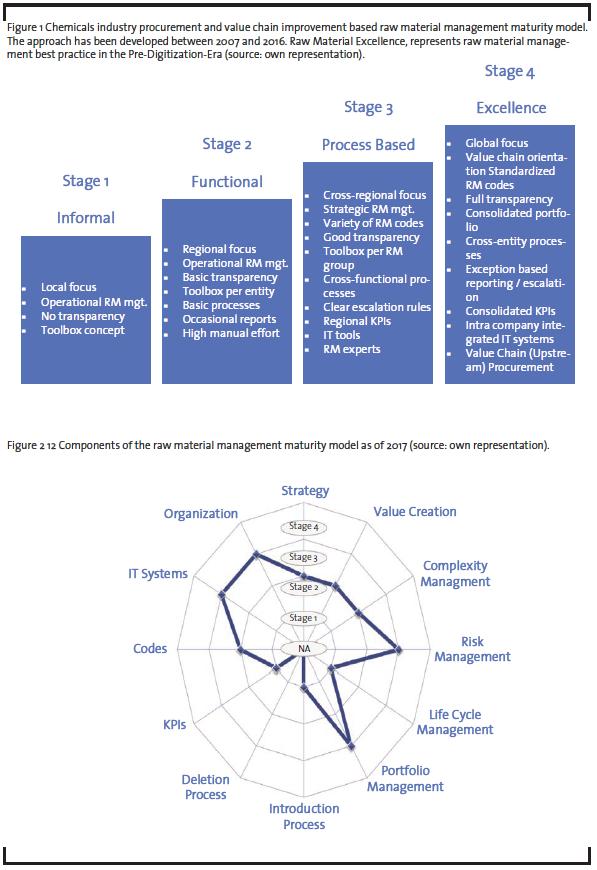

In a number of value chain and procurement performance improvement projects, the raw material management framework with its current highest level of performance, Raw Material Excellence has been developed, applied and increasingly become popular across the chemical industry.

What makes this innovative approach unique and successful is combining, aligning and integrating a number of value chain components that often enough have previously been treated independently (VCNI, 2017). Only by ensuring management’s commitment for a radical change towards a holistic approach, obtaining the buy-in of all affected players along the entire value chain and setting the expectation right that this transformation can easily take 24 months, the fundamental success criteria are put in place.

The model is currently covering 12 dimensions and is being applied throughout the transformation, from the initial performance assessment to define the status quo via target setting through implementation and post transformation reviews. The individual components are being introduced in the following paragraphs in detail. As with most models, the raw material management framework is a living model, undergoing steady expansions and extensions. Towards the end of this article, we will take a look at Raw Material Excellence 4.0 which is expected to be the next milestone or maturity stage thanks to the additional opportunities digitization will provide for the value creation out of raw materials.

2.1 Raw Material Strategy

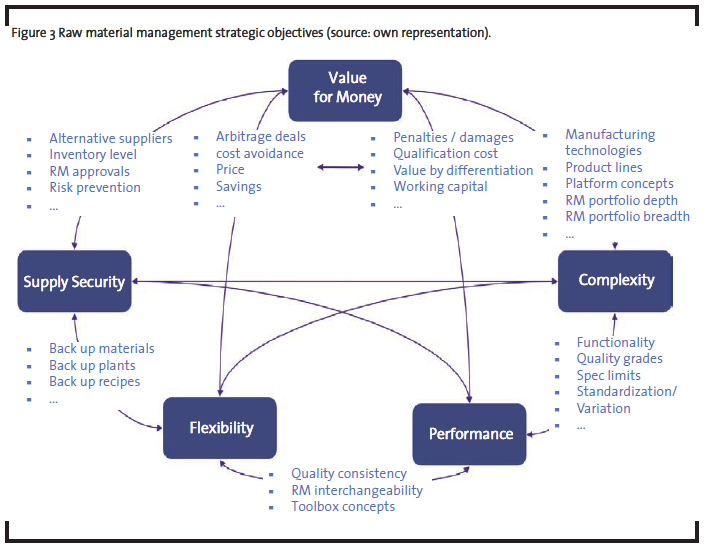

There are two success factors to succeed in raw material management and ultimately achieve the stage of Raw Material Excellence. The first one is to define a truly balanced set of raw material related strategic objectives (Heß, 2015). The second one is to be aware their interrelationships which often run counter to each other.

Value chain oriented raw material management requires a thorough understanding of the suppliers’ educts, their manufacturing technologies, the conversion of these chemicals in own manufacturing and formulation plants, own customers’ technologies and their products and applications. Here is one example why this is so important. When you look at the disastrous impact residual silicones can have in an automotive OEM’s paint shop, a coatings maker will do his utmost to ban silicone based lubricants from all his manufacturing, formulation and filling plants. The entire value chain however – and therefore the risk of silicone contamination, customer application failure and potential contractual penalties and damages – is much longer. Only if, for example, additives and resins suppliers’ manufacturing and filling technologies are also free of silicone based lubricants, this critical-to-quality parameter is sufficiently taken care of.

It is instrumental to understand that raw material related objectives are complementary to classic procurement strategies which are traditionally much more focusing on suppliers, supplier management, cost and – increasingly – security of supply.

Security of supply as part of raw material management is taking an end-to-end perspective from the supply of raw materials through the delivery of own sales products to the customers and its implications along the entire value chain. We will discuss the details in the risk management section.

Complexity is addressing the number and types of materials used to manufacture own products and formulations. One key consideration is the trade-off between opportunities through standardization and specific quality requirements. Depth and breadth of raw material portfolio are without doubt two helpful but not exhaustive metrics to characterize complexity associated with raw materials in a meaningful manner, as we will see in the paragraphs dealing with complexity and metrics.

In order to ensure the desired performance, raw materials have not only to match own raw material, product and manufacturing process specifications. While some of them serve as process aid with no impact on the final product, others are crucial for customer’s applications, most typically so called functional additives. One trade-off here is the need to differentiate, e.g. one material for one effect, vs the toolbox or platform approach, qualifying and maintaining fewer “multi-purpose” items. This is a good example for tensions in the overall raw material management strategy. Multi-purpose items may be more expensive but offer synergies of scale. Effect or application specific materials will be sold in lower volumes, potentially at better cost, but they blow up the portfolio and increase complexity cost. We will see more in the portfolio, material introduction, deletion and life-cycle sections of this article.

The same sections will provide more insights into the often desired but rarely fully achieved supply chain or value chain flexibility, the objective of which being to have a meaningful number of backup solutions qualified. These include raw materials from other sources, those with slightly different specifications that still allow making products and formulation acc. to customers’ needs, use of solids vs solutions and vice versa, if the – validated – process is allowing for that and so forth. While validated back-up options provide solutions to bottlenecks and technical issues, they increase portfolio size and complexity.

Value for money is probably best demonstrating the paradigm change when talking about raw material management instead “purchasing” or “procurement” of chemicals: The total-cost-benefit-perspective looks at one-off qualification, change over effort and ongoing acquisition cost of raw materials on the one hand side and on the total economic benefit they generate through their conversion to intermediates, products and formulations. Without taking the entire value chain into consideration, financial benefits from complexity cost reduction in sourcing, quality, production and product management and sales price elasticity would be left out (Kerkhoff et al., 2009).

A complete raw material management strategy requires additional components which we will discuss under organization addressing new and additional, internal and cross-company, value chain oriented roles and responsibilities, IT tools and systems referred to as e-Procurement that are serving the same objectives and scope, and last not least performance management demonstrate the successes of raw material management/ Raw Material Excellence.

Another way of looking at the new approach how to deal with raw material management is the following: “Historically, procurement has looked in the rear-view mirror and out of the back window; now we can look out through the windscreen at the road ahead,” says Andrew Coulcher, director of membership and knowledge at the Chartered Institute of Purchasing and Supply (Gascoigne, 2017).

2.2 Raw material management

Value Creation The second component of the framework is dealing with the financial objectives of raw material sourcing and the value creation through its use in the company’s value chain, encompassing some classic elements such as cost savings and cost avoidance as well as some more advanced objectives, e.g. complexity cost reduction and business profit increase (Gabath, 2010; Hofmann et al., 2012; Schuh et al., 2008).

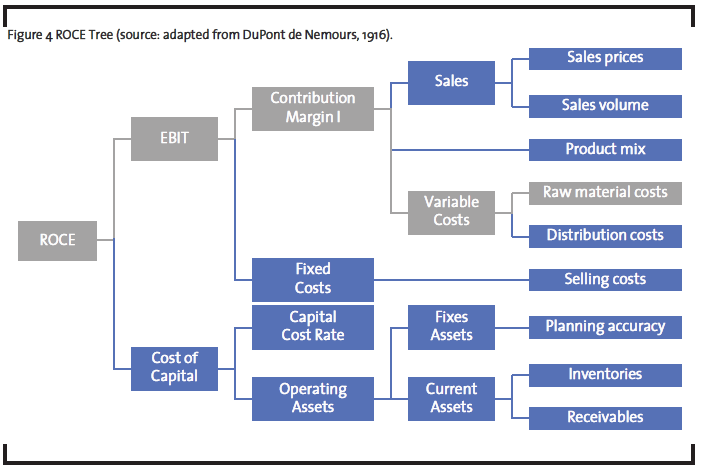

Since exactly one century DuPont’s ROCE tree has become the role model to qualitatively and quantitatively visualize value creation in chemical and other companies. Raw material management is complementing this proven, “output-oriented” approach by putting special emphasis on one of its inputs, raw material cost, and defining the mutual interdependencies to all other branches of the ROCE tree. For example, operating assets are being linked to raw material cost via “fixed assets”, i.e. technology platforms and process technologies, since all of them are converting raw material in one or the other way. More apparent is the link of raw materials to “current assets” via inventories which are in turn a variable in the company’s value chain risk management. Even the impact of raw materials on revenues needs to be considered: Sustainable cost reduction of raw materials may in some instances provide Product Management and Sales opportunities to win additional business and to sell additional volumes via adjusted sales prices without compromising on margin (Falter et al., 2017).

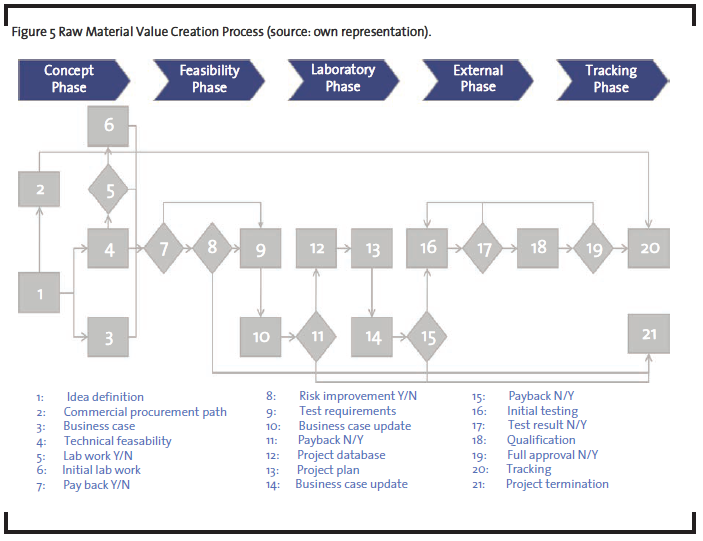

Over the last 10 years a best practice process to “turn cost into value” has emerged. Similar to the Stage Gate Process in innovation management, a multi-disciplinary approach is required here, too. Starting with the assessment of ideas to cut Total Cost of Ownership (TOCO) or to increase the value the raw material can provide to the company, two pathways are simultaneously pursued. Procurement experts are conducting classic supply market research to identify supply alternatives. Once they are successful and materials can easily be exchanged, the process is cut short. More likely, though, is the second route. Since the emphasis of the process is on value creation, the definition of an early business case and its iterations throughout the process are crucial. Once the initial business case has been confirmed, technical feasibility, impact on security of supply and customer involvement, e.g. for qualification and approval of modified final products are being defined. If after these checks the implementation still proofs beneficial for the company, the concept is changing status and becoming an official project. To keep control over the portfolio of raw material value creation projects, the standard approach to multi-project-management is applied. Standardized metrics and stage gate decisions ensure the best projects to continue while others might be put on hold or stopped, e.g. in case of scare resources. Timelines of the process depend a lot on the level of customer approval, quite popular in case of semiconductor industry customers buying electronic chemicals, automotive OEMs purchasing coatings, pharmaceutical or food industry customers sourcing chemicals that might be critical-to-patient or consumer.

In any case, if a value creation project has achieved the desired return on invest can only be demonstrated, if the company is tracking sales and margins on the one hand side and total cost, i.e. including one-off changeover cost and ongoing cost base reduction, for the period defined in the business case.

2.3 Raw Material Complexity Management

One of the first and most popular statements you are coming across when talking about complexity of value chain, supply chain, product or raw material portfolio is “we have to reduce it” (VCI, 2012). Raw material management is taking a different, much smarter approach instead (CCI, 2013).

The main issue with complexity is the lack of ways to measure it accurately, a consequence are poor transparency and non-fact based judgments on good or bad, value adding or value destroying complexity (GEP, 2017).

The proven approach taken by a number of chemical companies is to first get transparency on the number and type of raw material variations, such as grades, packaging size and type, chemical and/ or trade name, potentially in several languages etc. (Fang, 2017). The second step is to get control over the use of the true “chemical building blocks” in the value chain with a chemical building block meaning the essential characteristics of a raw material, e.g. chemical identity (CAS in case of pure chemicals) and purity or concentration. One of the most impressive examples for unrecognized, costly complexity has been a quite popular solvent, Butyl acetate 98% to 100% used by a coatings manufacturer in 4 regions. 37 product lines in 4 Business Units have been using no less than 22 variations of one and the same solvent without seeing the obvious in their already largely harmonized enterprise resource planning (ERP) system.

Besides the sheer number of raw materials and variants as one driver of complexity, an often neglected facet of raw materials’ use needs to be taken care of, the level of sharing raw materials across sites, plants, manufacturing technologies and processes, products and formulations. To understand the concept and impact of raw material toolboxes, technology and product platforms, “raw material family trees” are helpful models. Looking at the usage lists of raw materials, i.e. from an early stage in the value chain to a late one, and then at the BOMs (bills-of-material), i.e. taking look the other way round, you can derive very comprehensive “raw material family trees” to visualize the fortune of a raw material in a chemical company’s value chain. Once conducted right, the number of “independent raw material family trees”, i.e. those without or with very limited overlaps to others, and the position and number of “branches” and “crotches” in the family trees point out main complexity drivers. Under the lead of so called raw material experts, the impact on complexity cost but also on other parameters such as cycle times and inventory levels can be assessed and ultimately the right measures taken to get control over unwanted complexity. However we need to keep in mind that for very good reasons there is also some intended or mandatory complexity. If final product or application performance is enabled by a functional molecule, replacing it for the sake of standardization and complexity reduction is a no-go. Toll manufacturers may not be able to pull this lever either, if they rely on the BOMs of their customer. Manufacturers of fine chemicals for pharmaceutical use may be obliged to use pharmacopeia grade raw materials for some products, while other product lines benefit from lower cost alternatives.

By defining a lead parameter, e.g. the CAS number, and understanding the contents behind occasionally poor master data material group owners/ lead buyers have been recognizing commonalities and differentiators among the 22 Butyl acetate variants, e.g. identical suppliers offering different prices to different plants. Not only bundling opportunities as a procurement lever have been obtained by this exercise, also supplier competition has been increased, better prices have been achieved and last not least by becoming aware of different approved suppliers, risk mitigation measures have come on top – for free.

What sounds straight forward is in reality depending on some conditions that are today not always in place as required yet. Comparability and transparency require a mature ERP system, a well set-up and maintained Business Warehouse and – often the key issue – high quality master data.

2.4 Raw Material Risk Management

Already 10 years back raw material sourcing risk management has been a high to very high priority for specialty and fine chemical companies – if you listened to procurement managers and Chief Product Officers (CPOs). Taking a closer look into their organizations has revealed a slightly different picture, though. Only 40% of companies have had sufficient expertise in house, 35% of them explicit risk management processes in place and none of them dedicated risk management IT tools or systems implemented to successfully identify, evaluate and mitigate raw materials risks at that time (Keller, 2008).

More and more chemical companies have recognized the importance of value chain risk management (Schuh et al., 2012). Few of them are explicitly highlighting their efforts in the raw material area, though. A good exception is Givaudan, “to be forewarned is to be forearmed, which is why the comprehensive raw material risk management system is an excellent tool for Givaudan. At Givaudan, raw materials sourcing risk is a cross-functional consideration. Identifying and mitigating risk is integral to securing supply and satisfying customer needs” (Rogaar, 2017).

One can say a paradigm change has taken place. The number of companies within and beyond the chemicals industry with explicit and IT enabled risk management capabilities or the intention to implement it short-term has more than doubled to 85% in the meantime (McGovern, 2014). Business and procurement managers are no longer looking at risk management effort as – in the worst case – “nice-to-have” insurance premium. Fortunately, the perspective has widened to the better. Securing the supply from raw material through delivery of sales products along the entire value chain has become a business priority. There is a number of good reasons for this, e.g. service and security of supply becoming a differentiation against low cost market intruders form Middle and Far East, avoidance of contractual penalties and damages, reputation as reliable partner and ultimately shareholder value.

What has dramatically changed towards the better in raw material risk management is a consistent approach going far beyond the traditional, fragmented approach, focusing often on a handful of metrics only, such as material ABC analysis by volume or value and the business impact in case of value chain interruptions. One successful, more holistic risk management process is encompassing of 4 process steps owned by a dedicated individual, often but not necessarily a member of the raw material management organization. Once a significant enough raw material risk is being detected, a well-trained task force representing all affected value chain functions is switching mode from stand-by to active and is taking care of the activation of the cross-functionally created specific risk mitigation plan, the short term, i.e. problem solving, and long-term, i.e. avoidance of recurrence and lessons learned, mitigation plan. In order not to waste cost and time of raw material experts and representatives from procurement, product development, manufacturing, quality control (QC), commercial and finance it is vital to maintain and update a raw material risk database regularly. In recent risk management implementations a number of 8-12 metrics has become best practice to characterize raw material related risks and their impact on the value chain.

Looking at the different types of risk management metrics it becomes obvious that multi-disciplinary expertise is required to make the process successful, mainly for the non-data based and hence somewhat subjective parameters.

Along the risk probability dimension, “the upstream functions” of the value chain are primarily asked for their judgment. Raw material QC knows best about the “number of standard and back-up approvals” for material-product–combinations, procurement will take a perspective on the “existence of alternative suppliers”, “supplier relationship” and “market situation” and raw material experts on “availability of alternative materials” not only in the market but also across product lines, sites, businesses and region within the own company – transparency provided. Depending on responsibility for different types of inventory in the chain, procurement, supply chain, commercial or finance will cover the “stock levels”.

The business impact dimension will require more contribution from the value chain “downstream functions” such as product management, sales/ key account management and finance. They’ll assess the impact of a materialized risk on – lost – sales products “volume”, “revenue”, and “margin” and on the “number and size of affected customers”. The latter parameter and the “competitive threat”, i.e. the ongoing loss of business as a consequence of a customer changing an unreliable supplier, are particularly important for key business decisions, e.g. the allocation of remaining stock to the privileged customers.

Here is a good example for the benefits of raw material risk management addressing the entire value chain. A fine chemicals company has conducted a thorough risk assessment of their approx. 350 raw materials and has been very much surprised about the top scoring item. The fact that purified water has scored highest is mainly due to two aspects. First, it is literally being used in 100% of all products manufactured in that site. Therefore 100% of sales revenue and margin are affected, i.e. the business impact can’t be higher. Secondly there is a very modern, high throughput water purification unit on site. Unfortunately, there is no back up. Should the unit fail, no effective risk mitigation measure is in place to secure deliveries to customers.

Thanks to the implementation of the holistic risk management process at the client, a back-up facility has been built shortly after the assessment.

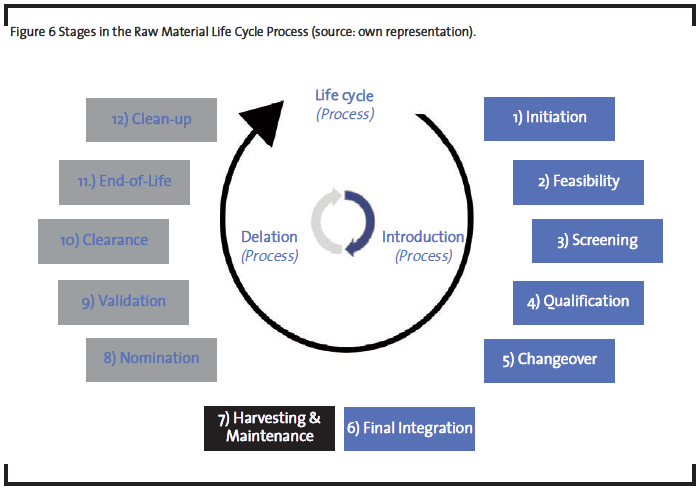

2.5 Raw Material Life Cycle Management

One of the least known, most ignored but increasingly important processes in raw material management is life cycle management (Mancini et al., 2013). The rationale is simple. When you look at raw material portfolios across chemical companies and interview procurement managers and technical raw material experts more than 90% of them are stating, their material portfolio has been growing over the last years, but exact numbers are not available, though.

In other words, the proliferation of raw materials in chemical companies is due to a lack of portfolio and of life cycle management, both processes being closely connected. The main difference is that classic raw material processes such as raw material introduction, the main use of raw materials (i.e. their conversion in manufacturing processes) and raw material deletion are event-based processes, whereas portfolio management is timebased (i.e. taking a perpendicular view at raw materials or a snapshot at the month end or end of the quarter in order to analyze the performance of the entirety of raw materials, make decisions and initiate further raw material options).

The life cycle of a raw material is spanning the entire period from the concept to introduce a new material within a chemical company through its termination (Lacy et al., 2013), i.e. the deletion of all master data in the ERP system. A raw material’s life cycle can range from a few weeks, e.g. when making a limited number of batches of a seasonal product as toll manufacturer for a customer, through decades and even longer, often applying to commodities such as acids, salts and solvents.

We are taking a closer look at the raw material introduction process and the material deletion process separately. These processes can be considered as “Investment phases” in the ROI equation. The center part of the life cycle process, the “Harvesting & Maintenance” represents the “Return phase”. It is the phase of value creation off the raw material. It includes the entire period a company is using the material for the production of intermediates and finished goods and to modify the material itself or its specification to serve changing technical, regulatory or finished goods customers’ requirements or other additional purposes.

2.6 Raw Material Portfolio Management

Chemical raw material portfolios often show the same characteristic as entropy. Both of them tend to continuously grow. However, chemical companies can keep their raw material portfolios well under control, if they implement proper portfolio management processes, tools and metrics to detect trends early and confirm the effectiveness of measures approved (Ulber et al., 2010; Beiersdorf, 2017; Rajagopal, 2014).

There is quite a number of different types of reasons that drive portfolio size and hence value chain complexity if left unaddressed. Acquisitions and mergers add raw materials to the existing pool of raw materials. Cost reduction and risk mitigation measures associated with partial replacement of expensive or risky raw materials is also driving the material numbers up. Commoditization of existing or introduction of new sales products may require raw materials with new or better functionality, again increasing the number of items in the toolbox.

A two-edged measure is the introduction of multi-purpose “one-size-fits-all” raw materials and similar approaches such as toolbox, platform or shared materials concepts. While the idea is obvious, some practical implications are often insufficiently considered. Instead of pursuing a “two-out-one-in” policy to reduce the number of items in the portfolio, chemical companies often face subtleties such as existing contracts with customers, that may refuse the material change in a formulation and hence the termination of the raw material. Another classic issue is the cost burden commodity type sales products will face if the average cost for the new material is slightly higher than before. Product managers often find good reasons to not subsidize the higher raw material cost at the expense of their products’ contribution margin. One of the most obvious obstacles is of course longer term contractual obligations with suppliers, e.g. volume or take-or-pay clauses.

Portfolio management’s front end process, raw material introduction, is rather popular in chemical companies (Cordis, 2017), since it is so similar to innovation processes. At the back end of the portfolio process, the raw material termination or housekeeping process is far less popular. Successful portfolio management implementations are telling us, the weight of the termination process must be equivalent to the weight of the material introduction process. If it is less, the company is managing growth of item numbers but not a portfolio of value creation building blocks. Opportunities to cleanup the portfolio include for example complexity reduction programs, standardization or harmonization approaches driven for example by requests from the business to pursue more cost-efficient bundling opportunities, sales product or manufacturing technology end-of-life and others more.

Regular snapshots looking at the number of active raw materials, the ones being introduced and the ones being terminated help monitor the portfolio trends and its target achievement and – together with other portfolio metrics discussed in the KPI chapter – define corrective actions such as speeding up new material introduction, raw material rationalization waves, standardization or harmonization projects etc. These snapshots have often been used for monthly or quarterly reports and are now being applied more regularly. This is mainly due to two reasons. One is the need to keep the portfolio of value creating items better under control, since it offers significant technical and commercial opportunities for chemical companies. The other one is the increasingly automated creation of multi-dimensional portfolio reports that can now be done within minutes but what has been taken days only 10 years ago. The use of the snapshots for monthly or quarterly business reviews is why we look at portfolio management taking a time-based, perpendicular management view compared to the primarily event-based, i.e. milestone or gate oriented, introduction, deletion and other raw material related processes.

Since raw material performance data beyond their sheer number are coming from a number of value chain functions, e.g. procurement, raw mate rial experts, production, product management, sales and finance, it is clear that raw material portfolio management, too, has to be a cross-discipline approach, often orchestrated by raw material experts.

A role model raw material portfolio rationalization approach has been undertaken by a diversified specialty chemicals company consisting of 4 – with regard to raw material handling – autonomous business units (BU), almost 20 manufacturing sites in 4 regions and 5 core manufacturing technologies each. The overall raw material portfolio consisted of 4.000 items structured in 5 standard material groups. By implementing portfolio management guidelines such as “two-out-one-in”, material introduction and deletion processes, clearly defined targets, the consequent application of “toolbox” concepts and – most importantly, the crossfunctional approach, the company has achieved an overarching success within 18 months. Step 1 has led to a reduction of 24.6% by sharing materials across different manufacturing technologies within every single BU. Step 2, the sharing of raw materials across business units with every single region has increased that reduction to 38.4%. After step 3, the sharing of key raw materials across the regions, the number of raw materials taken out of the portfolio has reached an impressive mark of 46.1%.

2.7 Raw Material Introduction Process

New raw material introduction is a cross-functional process very similar to the well-established stage gate innovation process (Cooper, 2002) or its alternative, the Phase Gate process (McGrath, 1996) addressing additional business perspectives. The main benefit of this process is to allow control over the raw material portfolio, in particular about its Total-Cost-of-Ownership vs its total value add to the company and its complexity, to name a few.

When adapting the stage gate or better the phase review process to raw material management, chemical companies have to define their phases and objectives by phase first. What sounds trivial is the opposite in fact. Through intelligent definition of milestones Procurement may benefit from an early combination of commercial and technical levers. Once the proof of concept is available, Procurement is well prepared for negotiations with current and alternative suppliers. The current one will recognize the seriousness of the customer, when he is showing the progress made in the qualification of alternatives. Alternative suppliers will recognize that his sales price has to not only to beat that of the competition. It must also allow the customer of finance the one-off qualification cost.

A proven process model, implemented in almost 10 projects in fine, specialty and even in one base chemical company has evolved, consisting of 6 phases. In the Initiation Phase (1) basically the idea and the necessity to introduce a material to the portfolio are assessed. Key points are the initial check with the global portfolio which in turn requires the transparency mentioned before and the decision at the gate which pathway to pursue. Pathway 1 is the voluntary choice to modify or create at least one new product formulation through the use of a new raw material – supplier combination with the required performance. Pathway 2 pursues the voluntary approval of a new raw material – supplier combination with the raw material ideally being identical to an already existing raw material, a so called „one-to-one“ exchange. Pathway 3 is a reactive, firefighting approach to solve a business issue through a flexible approval of a new raw material – supplier combination, e.g. via a short track.

The Feasibility Phase (2) aims to prove the economic and technical feasibility. Key is the qualification approach to be taken. This very much depends on the criticality of the raw material to own products and formulations as well as the number of affected products, technologies and customers. Its end point is the Go or No-go decision to qualify the raw material at business level.

In the Screening Phase (3) potential materials and supplier are being assessed through samples, pre-defined key analytical and formulation tests. End point is the decision whether or not to pursue the qualification at lower Business Team and/ or Product Line level. Typically preliminary material IDs are used in the ERP system for test materials in order to save some effort and not to blow up the number of active materials in the portfolio.

In the Qualification Phase (4) the suitability of the material-supplier combination for specific business areas, e.g. entire Business Units or underlying Business Teams, product lines or technologies is being confirmed. The phase endpoint is the decision to start the changeover and the scale up. A soon as the decision is made to introduce the material, a permanent material code needs to be assigned.

In the Changeover Phase (5) the material is being transferred from lab scale to own and customer plants. The approval of the predefined pilot or target customers marks the phase end. The Final Integration Phase (6) ends with a proper project closeout, lessons learned and business case review once the raw material has officially been introduced in the value chain and all supporting IT systems. Strict discipline is required to assign and change the master data, e.g. the different status of raw ma-terial codes to ensure transparency on the raw material portfolio and its pipeline.

2.8 Raw Material Deletion Process

The Raw Material Deletion process is the counterpart to and at least as important as the raw material introduction process for the company, the portfolio and the life-cycle process. In other words, it is the main means to keep raw material complexity under control and its absence in many chemical companies is the main driver for their proliferated material portfolios.

Its design and implementation principles, e.g. organization, phase structure, KPIs and IT systems have to be closely aligned with the portfolio and introduction processes.

Starting points for the deletion process can either be time-based, e.g. as result from monthly or quarterly portfolio reviews, or event-based, e.g. upon termination of sales products at the end of their life cycle, inventory and subsequent portfolio reduction of no- and slow-movers, portfolio rationalization programs, the divestiture of a business and others more.

The nomination Phase (8) serves at defining and validating the opportunities and rationale for raw material deletion. All candidates are put on a long list of to-be-terminated raw materials and ideally marked in the ERP system accordingly.

In the Validation Phase (9) all candidates are assigned a “restricted use” status, i.e. the material shall not be used for new product and formulation recipes, purchasing orders need to be double checked with the remaining demand for sales products etc. The business impact of all candidates needs to be assessed relating to supplier obligations, own sales product life-cycles, need for customer information/ approval, risk, and cost, to name the most important ones. The confirmed list of deletions is the main deliverable of this Phase.

Clearance Phase (10) is rather operational, focusing on aligning known demand with purchase orders, using the remaining stock at hand for production or otherwise, e.g. reselling or disposal. The objective and end point of this Phase is zero stock. In the End-of-Life Phase (11) the official life cycle status is set to “terminated”. This status can typically not be assigned in an ERP system if there is any remaining stock anywhere in the business; this is why the endpoint of Phase (10) is so important. Once a material is officially terminated and marked as such in the ERP system, the portfolio count is reduced by one. This way ensures transparency on the correct number of materials in the portfolio but requires proper master data management.

2.9 Raw material management

KPIs When establishing raw material management in a chemical company it is instrumental to provide a meaningful set of key performance indicators (KPIs) for several reasons (Eschinger, 2014; Wagner and Stephan, 2007). Metrics and KPIs already existing in a chemical company should be leveraged to the extent possible. New ones should only be added if add additional insights and value can be created.

A typical dashboard of raw material experts is containing KPIs reflecting their main areas of responsibility. For complexity and raw material portfolio control, the number of active raw materials, those in the new material introduction pipeline, the number of to be terminated ones and the number of deletions have proven very effective. These data can be used to characterize raw material portfolio depth, i.e. the number of different grades within a raw material group, and portfolio breath, i.e. the number of different raw material groups, relatively simple at corporate, business unit or regional level. All of these data are relatively simple, well defined data and should be readily available in IT systems.

Regarding cost and value creation it gets slightly more difficult. Exact definitions for cost savings, cost avoidance and sustainable reduction of the raw material cost base are required. This requires a solid alignment with procurement on the one hand side and product management or sales on the other side. The organization must agree to distinguish between the impact of a particular measure and the bottom line impact. For example a material cost reduction multiplied by a year’s purchasing volume results in a COGS (Cost Of Goods Sold) reduction that can be seen tracked in the product cost calculation and the P&L. In year one the impact of the measure and the savings are identical. In sub-sequent years, there is no further bottom line impact. However the impact of the measure is a permanent new material cost base. Remember, raw material cost is often the single highest cost in a chemical company. A reduction from 40% to 38% or even lower is one of the most attractive objectives of implementing raw material management and achieving the Excellence stage.

Risk management performance measurement is getting even more complex, since it is not only data and convention based, it is to a certain extent subjective. The first set of risk related data is straight forward, i.e. the numbers of monopoly, single, and dual sourced and that all other raw materials. They are helpful for initial risk profiles. The best practice risk management approach is rather comprehensive and builds on the combination of risk probability and business impact. The description of risk probability requires a set of hard data, such as the number of alternative materials and suppliers in general, the number of approvals and inventory levels. Judgment regarding the market demand-supply-balance and the supplier relationship or reliability regarding this particular raw material is subjective.

Business impact calculations include besides the data based volume of finished products affected, revenue impact, contribution margin impact and number of customers impacted the subjective pa-rameter “competitive threat”. It represents an estimate how likely competitors can take advantage from the situation by being able to supply alternative products to the customers and steal business.

Since raw material management includes also a number of different project types, e.g. to reduce raw material cost, increase raw material value creation, introduce new raw materials, delete obsolete ones to name the most common ones, a set of project management metrics is also required. Companies applying leading project management practices including project controlling should not have an issue to provide standard project management data covering the classic dimensions time, cost, quality and risk. Only if these basics are not in place, raw material management will have to apply these metrics to justify new projects and prove their success.

A common challenge in various implementations in about 10 different chemical companies has been the quality of raw data used to calculate the KPIs, databases and systems operated in isolation, e.g. LIMS systems, project databases, several ERP modules, CRM systems, business warehouses and not to forget a lot of Excel datasheets. Performance measurement and reporting have often at the beginning of the improvement projects been pulled together manually. Despite during the implementation major progress regarding the level of automation is typically been achieved, monitoring and re-porting is expected to significantly benefit from progress in digitization.

2.10 Raw Material Codes

One main reason for unwanted and unrecognized complexity at the front end of the value chain is the lack of consistent raw material coding systems. The implications are twofold.

Firstly, transparency on raw material portfolio and raw material value potential is limited. Recall the example of 22 different Butyl acetate SKUs (Stock Keeping Unit) in one chemical company. Commercial procurement levers such as the chance to bundle demand and increase supplier competition through standardization and harmonization cannot be pulled, if there is no visibility up front. Since any improvement opportunity is addressing only a fraction of the overall potential the likelihood that it be will be turned down is high.

Secondly, it drives unwanted downstream complexity and associated complexity cost. A company unknowingly maintaining multiple identical items, so called “clones”, and several extremely similar and in principle exchangeable items, so called “twins” in their portfolio, spends a lot of wasted effort on material related master data in ERP systems, e.g. material master file, bills-of-material of products using the clones and twins, quality control specifications and tests, safety data sheets, split purchase orders, labels, warehouse space, inventory value, customer notification and approvals and so forth.

Both upstream and downstream complexity and their implication on the business have often been a reason to standardize coding systems in chemical companies. One of the leading practices for a value chain oriented classification addressing materials, intermediates and products has been developed in 2000 by about 10 companies, most of them chemical ones, such as BASF, Bayer, Evonik (Degussa, one of its predecessor organizations), Solvay and Wacker, called eCl@ss.

In a number of implementations eCl@ss and in house developed solutions have been introduced in chemical companies over the last 10 years. In house solutions are often not quite as comprehensive as the industry standard. What most of them have in common is the recognition that only properly defined and maintained master data ensure transparency and control over the raw material portfolio and if wanted over intermediates and finished products, i.e. the downstream value chain.

A positive side effect of state of the art coding systems and industry standard is the impact on post-merger and post-acquisition integrations. Often enough it has taken years to fully harmonize materials and downstream intermediates and products. With recent progresses in classification standards, IT systems and the level of automation, a lot of effort and time has been saved. Since a lot of raw material information is hard data, expectations are high, that progress in digitization will add further significant value.

2.11 Raw material management Organization

The preferred organizational set-up for raw material management is a unit of raw material experts that understand the entire value chain from the suppliers’ materials and technologies through the customers applications (Radziwona et al., 2014; Feldmann, 2015), often referred to as upstream procurement or technical upstream.

Their key contribution is ensuring that only materials will be identified, qualified, sourced and used that fulfill all downstream value chain requirements, i.e. for the own company’s products and formulations requirements as well as those of customers’ applications. These requirements cover numerous different dimensions that may, if not being addressed in a holistic manner by taking a value chain view, run counter to each other. Other objectives they pursue are security of inbound and thereby indirectly outbound supply, low Total-Cost-of-Ownership, agility and flexibility of operations by providing approved alternatives to standard materials, control over raw material portfolio complexity and its impact on the downstream value chain.

The new raw material experts function requires a unique, mixed skillset. A new manager’s challenge is to motivate and recruit candidates from various functions, e.g. product management or key account management that have insights in customers’ applications and requirements, R&D and application development that understand the functionality and impact of raw materials on finished products, and procurement that have intimate knowledge on supplier markets, market intelligence, relationships and so forth. Developing raw material experts is not a matter of weeks and is a major investment (Gaiziunas, 2009). It rather takes 18 to 30 months as several implementation projects in the chemical industry show.

A multi-dimensional matrix structure has proven to be the most efficient organizational set up for the raw material expert unit. The matrix is typically composed of five to six parameters such as business units, raw material groups, regions or countries, processes and IT tools or systems. This set-up ensures dedicated and high quality raw material group specific know how, strategies, utilization guide-lines, specifications, introduction, deletions and so forth. Clearly defined and communicated objectives and manageable, i.e. limited scopes for each expert are not only crucial for the success of the experts, they are also fundamental for the buy in and ongoing support of other value chain functions.

Raw material experts must not be considered as a competition to commercial procurement (Widmann et al., 2015). Instead they provide additional, complementary capabilities to the company under the roof of upstream procurement or technical procurement. In most cases they are a part of the procurement organization. Nevertheless establishing this new function and assigning key value chain responsibility to it is often a major cultural challenge to chemical companies that must not be underestimated.

3 Conclusion

To turn “cost” into “value”, nothing less than a business transformation is required. Over the last ten years a number of innovative and proactive chemical companies has recognized this potential of raw materials as value creating building blocks (Royal Dutch Shell, 2017) instead of looking at them as a sheer cost.

Key element for raw material management is the assignment of dedicated raw material experts that understand the external and internal value chain from own suppliers educts through own customers applications. They take responsibility for raw material management processes, tools, systems and metrics. They are an instrumental link in a chemicals company’s value chain.

A good summary for a successful transformation of the procurement function and the achieved mindset change is David Powell’s statement ”Procurement has gone from being the poor cousin, to a partner at the heart of business decision“ (Powell, 2016).

Management commitment requires a professional state-of-the-art change management and communication along the value chain, i.e. across the entire organization, assign sufficient resources and allow the time required, often between 18 to 30 months.

Once chemical companies are ready and committed to this innovative approach and have achieved the highest stage of maturity, Raw Material Excellence, they can expect to significantly increase EBIT, e.g. from 10% to 12% or 13%. The full benefit of holistic raw material management is going far beyond financial savings. Improved inbound and outbound supply performance service, complexity adjusted to the right level required for a particular business while being agile and responsive are additional benefits from this business model innovation.

Raw material management is an option that pays out. It is a dynamic approach invented and applied in numerous value chain improvements in the chemical industry (GDCh et al., 2016). It is expected to develop further in parallel with the progress of digitization towards a new maturity stage, Raw Material Excellence 4.0 within the next five years (Glas and Kleemann, 2016; Schmidt et al., 2015).

References

Beiersdorf AG (2017): Project Manager Raw Material Portfolio, available at https://career.beiersdorfgroup.com/sap(bD1lbiZjPTAwMg==)/bc/bsp/sap/hrrcf_wd_dovru/application.do?ARAM=cmNmdHlwZT1waW5zdCZwaW5zdD0wMDUwNTY5NTNCRjAxRUQ2OTdDMTk3MENGRDJCNTVFNg%3d%3d, accessed July 19, 2017.

CCI (2013): Leading chemical companies standardise and integrate best practice to reduce costs, increase flexibility, and sustain growth, in TRACC Chemicals Industry Trends Report 2013, p. 3.

Cooper, R.G. (2002): Top oder Flop in der Produktentwicklung. Erfolgsstrategien: von der Idee zum Launch, Wiley-VCH, Weinheim.

CORDIS, European Commission (2017): A roadmap for the chemical industry to a bioeconomy, available at http://cordis.europa.eu/programme/rcn/702215_en.html, accessed July 30, 2017.

Eschinger S., Geyer O., Freimanis T. (2014): Das Kompendium der Einkaufskennzahlen, Eschinger Consulting GmbH, Frankfurt.

Falter W., Wehberg G., Wiedling, M. (2017): Procurement in the Chemical Industry – Key Challenges for CPOs, in Deloitte. 2017 (2), pp. 4-13.

Fang, H. (2017): Das Talent unter Beweis stellen, available at http://www.basfcoatings.com/global/ecwebPreview/ de_DE/content/careers/why_join_basf_coa tings/Erfahrungsbericht_Helen-Fang, accessed 3 August 2017.

Feldmann, C. (2015): Speech on the annual summit of the BME, available at https://www.bme.de/feldmann-einkauf-vorgewaltigen-herausforderungen-1315, accessed 15. July 2017.

Gabath C. (2010): Risiko- und Krisenmanagement im Einkauf: Methoden zur aktiven Kostensenkung, Gabler, Wiesbaden.

Gaiziunas, N. (2009): Qualifizierung im Supply- Chain-Management: Vom Einkäufer zum Suppy-Chain-Manager, Finanzbuch Verlag, München.

Gascoigne, C. (2017): Procurement: looking ahead to a digital future, available at https://www.raconteur.net/business/procurement-looking-ahead-toa-digital-future accessed August 2, 2017.

GDCh, DECHEMA, DGMK, VCI (2010): Change in the Raw Materials Base, Position Paper.

GEP (2017): How to Reduce Complexity in Procurement Management, available at https://www.gep.com/white-papers/how-reducecomplexity-procurement-management, accessed August 1, 2017.

Glas, A., Kleemann, F. (2016): The impact of industry 4.0 on procurement and supply management: A conceptual and qualitative analysis”, International Journal of Business and Management Invention, 5 (6), pp. 55-66.

Gorin, D. (2016): Rising cost of raw materials – forging strategies to address its impact, in Traccsolution, Competitive Capabilities International (Pty) Ltd, Ireland.

Heß, G. (2015): Reifegradmanagement im Einkauf: Mit dem 15M-Reifegradmodell zur Exzellenz im Supply Management, Springer Gabler, Wiesbaden.

Hofmann E., Maucher D., Kotula M., Kreienbrink O. (2012): Erfolgsmessung und Anreizsysteme im Einkauf: Den Mehrwert der Beschaffung professionell erheben, bewerten und darstellen in Advanced Purchasing & SCM, Springer, Berlin Heidelberg.

Keller, W. (2008): The war of raw materials – Global Benchmarking Study, available at Wolfram Keller Management Consulting.

Kerkhoff, G., Michalak, C., Schäfer, D., Jäger, G., Heidbreder, C., Kreienbrink, O., Penning, S., Rüter, M. (2009): Einkaufsagenda 2020: Beschaffung in der Zukunft – Wettbewerbsvorteile durch einen visionären Einkauf sichern und ausbauen, Wiley VCH, Weinheim.

Lacy P., Keeble, J., McNamara, R. (2014): Circular Advantage – Innovative Business Models and Technologies to Create Value in a World without Limits to Growth, available at https://www.accenture.com/t20150523T053139__w__/us-en/_acnmedia/Accenture/Conversion-Assets/DotCom/Documents/Global/PDF/Strategy_6/Accenture-Circular-Advantage-Innovative-Business-Models-Technologies-Value-Growth.pdf, accessed July 19, 2017.

Leybovich, I. (2010): New Ways to Offset Raw Materials and Labor Costs, in Industry Market Trends, Thomasnet.com.

Mancini, L., Ardente, F., Goralczyk, M., Pennington, D., Sala, D. (2013): Perspectives on managing life cycles, Proceedings of the 6th International Conference of Life Cycle Management, pp. 520-523.

McGovern, M. (2014): Chief Procurement Officer (CPO) Study, The IBM Institute for Business Value (IBV), Armonk.

McGrath, M. (1996): Setting the PACE in Product Development, Routledge, London.

McPherson, T. (2016): 2016 Raw Materials and Chemicals Roundtable, ASI Adhesives & Sealants Industry.

Powell, D. (2016): The modern art of buying for pharmaceutical CPOs, available at http://www.tungsten-network.com/pharma/articles/article-modern-art-of-buying, accessed July 15, 2017.

Radziwona, A., Bilberga, A., Bogersa, M., Skov Madsen, E. (2013): The Smart Factory: Exploring Adaptive and Flexible Manufacturing Solutions, 24th DAAAM International Symposium on Intelligent Manufacturing and Automation, in Procedia Engineering, Elsevier, 69, pp. 1184-1190.

Rajagopal, R. (2014): Sustainable Value Creation in the Fine and Speciality Chemicals Industry, John Wiley & Sons, Hoboken.

Rogaar, J. (2017): Creating an exceptional end-to-end supply chain with raw material sourcing risk management, available at https://www.givaudan.com/sustainability/sourcing/our-approach/optimising-supply-security, accessed July 12, 2017.

Royal Dutch Shell plc (2017): Chemicals products portfolio, available at http://www.shell.com/business-customers/chemicals/our-products.html, accessed August 12, 2017.

Schmidt, R., Möhring, M., Härting, R. -C, Reichstein, C., Neumaier, P., and Jozinovic, P. (2015): Industry 4.0 – Potentials for Creating Smart Products: Empirical Research Results in Business Information Systems 2015, pp. 16-27.

Schuh C., Kromoser R., Romero, P.R., Strohmer M., Alenka T. (2008): Das Einkaufsschachbrett: Mit 64 Ansätzen Materialkosten senken und Wert schaffen, Springer Gabler, Wiesbaden.

Schuh C., Kromoser, R., Romero, P.R., Strohmer, M., Alenka, T. (2011): Der agile Einkauf. Erfolgsgarant in volatilen Zeiten, Springer Gabler, Wiesbaden.

Tieman, R. (2013): Chemicals: Science views waste in role as raw material of the future, Financial Times, available at https://www.ft.com/content/2ef57b06-2c26-11e3-acf4-00144feab7de, accessed July 25, 2017.

Ulber, R., Sell, D., Hirth, T. (2010): Renewable raw materials – new feedstocks for the chemical industry, Wiley-VCH, Weinheim.

VCI Germany (2010): Position paper, available at https://www.vci.de/langfassungen-pdf/vci-position-zur-zertifizierung-der-nachhaltigkeitnachwachsender-rohstoffe-in-der-chemieindustrie.pdf, accessed August 3, 2017.

VNCI (2017): Dutch chemical industry, available at https://www.vnci.nl/english, accessed August 3, 2017.

Wagner M. S., Weber, J. (2007): Beschaffungscontrolling – Den Wertbeitrag der Beschaffung messen und optimieren, Wiley-VCH, Weinheim.

Widmann, B., Langer, E., Menrad, K. (2015): Company profile, Konaro – Center of excellence for renewable resources.