Wealth effects of corporate spin-offs – An event study analysis of the chemical & pharmaceutical industry

Abstract

The present article studies wealth effects of global spin-off announcements of the chemical and pharmaceutical industry that were announced between January 2001 and October 2019. The cumulative average abnormal return over the 3-day event window is 3.91%. This result is significant at the 0.1%-level. Moreover, varying the event-window and utilizing a second statistical approach strongly supports these findings by yielding similar results at a 0.2% significance level which is rare for the event study methodology. This study strongly corroborates the hypothesis that wealth effects associated with spin-off announcements are very strong in the chemical and pharmaceutical industry.

1 Introduction

It has been widely proven in literature that spin-offs and spin-off announcements cause an increase of the shareholder value (see, e.g. Veld and Veld-Merkoulova, 2009; Veld and Veld-Merkoulova, 2004). The positive effects of spin-off announcements have been proven by several event studies focusing on the analysis of abnormal stock returns. Thus, different researchers who mainly focused on the US market provided evidence that, on average, the announcement of a spin-off causes significantly positive abnormal returns (Rosenfeld, 1984). Nevertheless, a small number of studies analyzing the European market (Sudarsanam et al.,1996; Veld and Veld-Merkoulova, 2004) show similar results. Thus, much more research is required to validate these results. However, some studies have proven that the height of wealth effects defined as abnormal stock price reactions varies among several industries based on the circumstance that the effect of diversification on performance is not homogeneous across industries (Santalo and Becerra, 2008; Vollmar, 2014). These findings, the large number of spin-off announcements in the chemical and pharmaceutical industry and the high degree of diversification, give reason to separately investigate spin-off announcements of the chemical and pharmaceutical industry. Therefore, the present article sheds light on the spin-off-based wealth effects within the chemical and pharmaceutical industry.

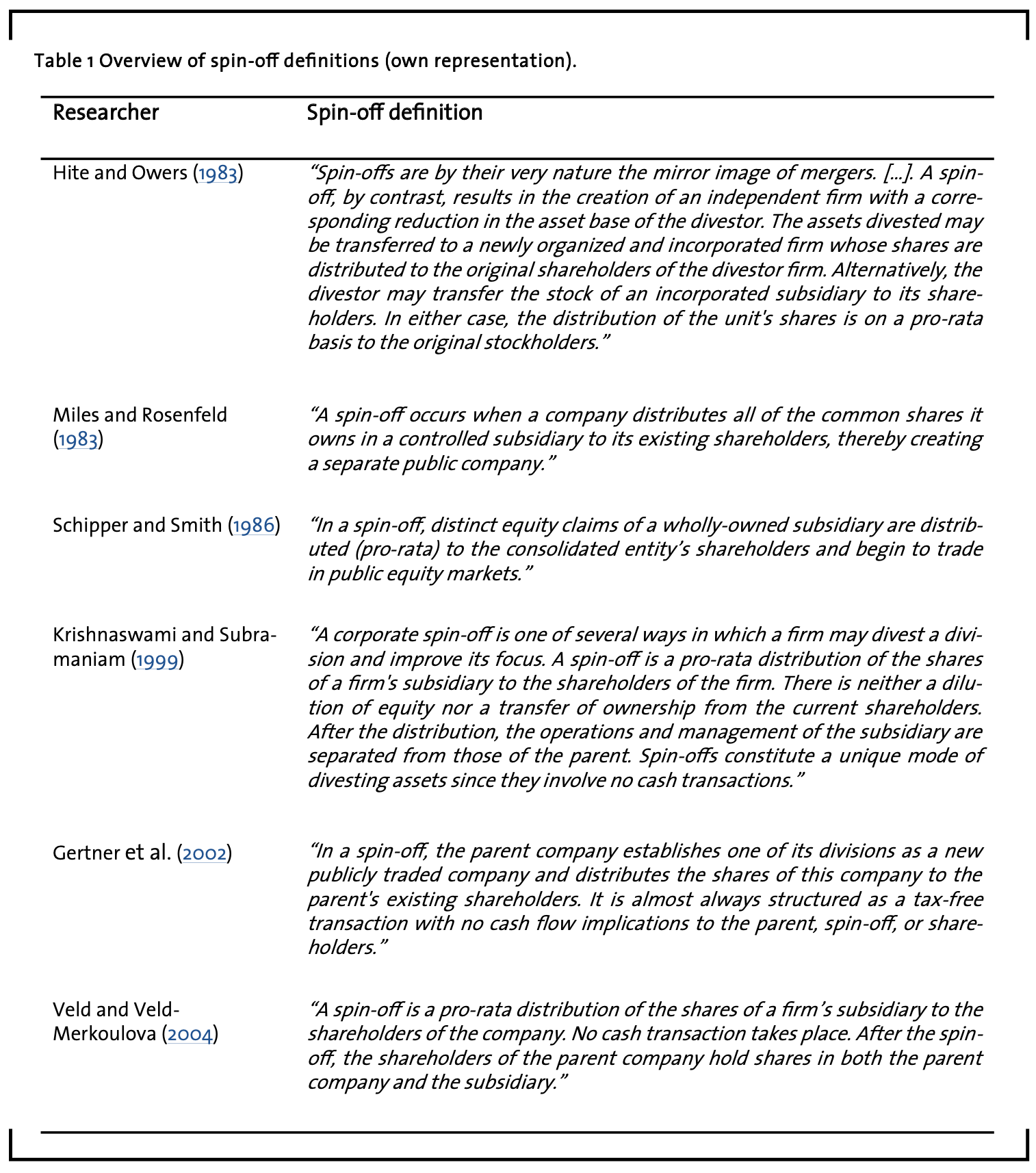

Spin-offs are defined as pro-rata distribution of the shares of a firm‘s subsidiary to the shareholders of the parent company (Veld and Veld-Merkoulova, 2004). Moreover, spin-offs are legally and economically independent companies (Ernst et al., 2005). Over the last decades diverse spin-off definitions arose in literature. Table 1 provides an overview of these definitions.

The definition spin-off can be reduced to the following five deliverables (Smolnik, 2020).

- Divestment of a subsidiary: Separation of subsidiary/corporate division.

- Legal and economic independence: Spin-off is an independent legal entity and affects own market performance.

- Continuance of parent company: After creating a spin-off, the parent company has to persist.

- Pro-rata distribution of shares: The shares are distributed pro-rata to the shareholders of the parent company.

- Absence of cash transactions: Divestment of assets without cash transactions.

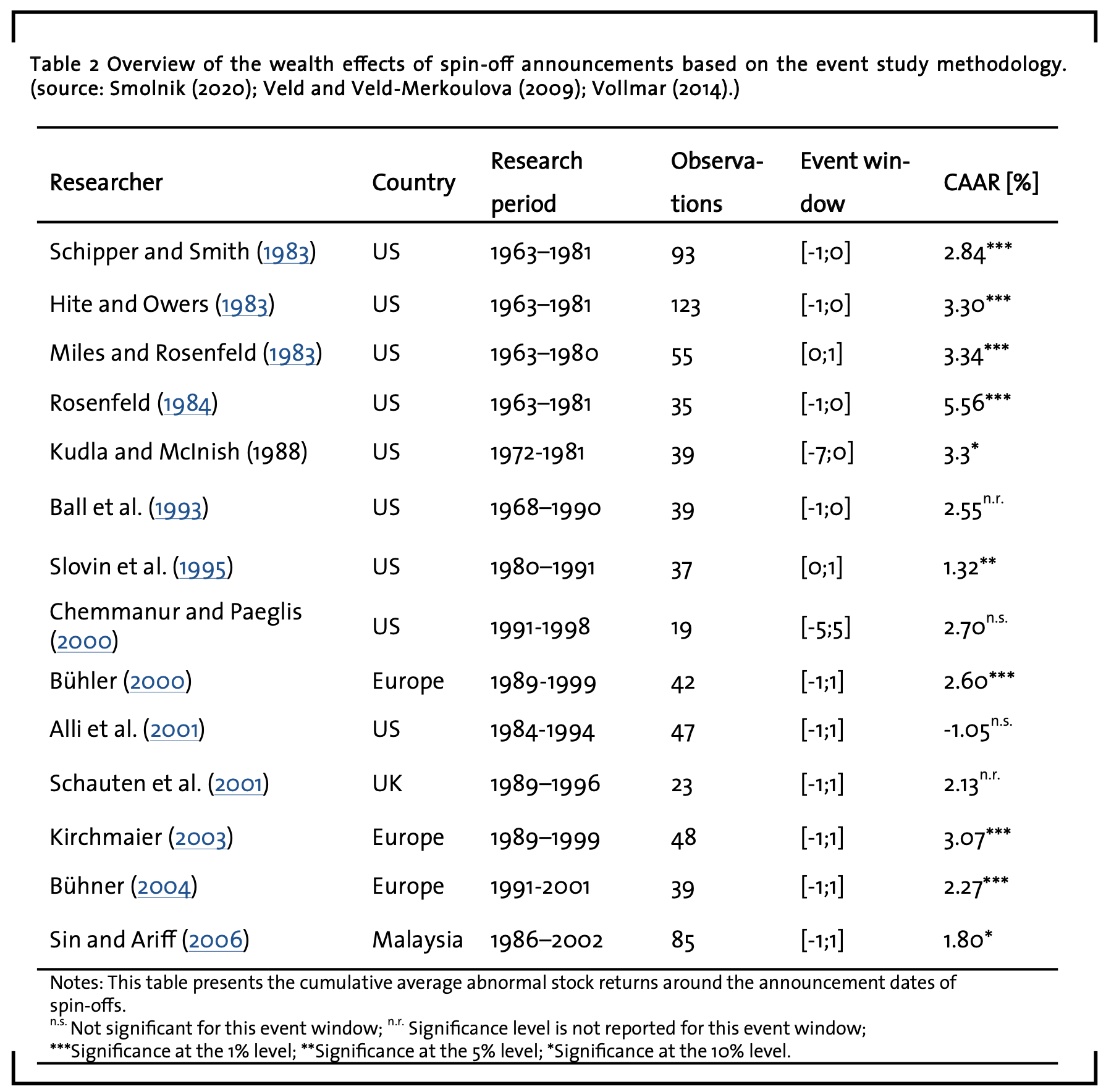

As previously mentioned, wealth effects of spin-off announcements have been mainly analyzed in the US. These analyses have shown that spin-off announcements result in cumulative abnormal returns of up to 5.56% (Rosenfeld, 1984). Thus, the highly positive abnormal returns represent the shareholder‘s expectation of future benefits which are based on the spin-off announcement. Additionally, some studies of spin-off announcements in the European market exist which are in line with the findings of the US market analyses (Sudarsanam et al., 1996). Table 2 gives an impression as to how spin-off announcements affect the shareholder-value by displaying the results of several event studies (for a more comprehensive list of event studies on the wealth effects of spin-off announcements (Smolnik, 2020). Event studies usually analyse short-term wealth effects for several reasons.

The main reason focuses on the increasing influence of automated trading systems. Nowadays a majority of stock market transactions is based on automated trading systems and therefore most shares are sold within a two-day time window (Huang, et al., 2019).

Thus, a large number of factors that can probably explain the wealth effects of spin-off announcements have been identified. Extensive empirical research has shown that an increase in diversification results in equities that are traded at a discount (Mansi and Reeb, 2002). Separating from a corporate division is the simplest way to decrease a company‘s diversity and therefore avoid the diversification discount. Consequently, spinning-off a division with the aim to narrow the industrial focus could culminate in positive stock price reactions. Daley, Mehrotra, and Sivakumar (1997), Desai and Jain (1999) and Krishnaswami and Subramaniam (1999) analyzed this relationship and found that abnormal returns for firms that want to increase their industrial focus by spinning-off a division are significantly higher than for spin-offs which are not executed to narrow the industrial focus.

A second factor focuses on the improvement of the geographical focus. Thus, spinning-off a division abroad increases the company‘s geographical focus. However, researchers advance two antithetic views. While some researchers hypothesize a positive correlation between improving the geographical focus and abnormal returns, other researchers opine that narrowing the geographical focus by spinning-off a division negatively affects the abnormal returns (Bodnar, Tang, and Weintrop, 1997; Veld and Veld-Merkoulova, 2004). The positive effects should be based on the reduction of complexity and the decrease of risks, whereas the hypothesised negative effect should be rooted in the reduction of economies of scale, disadvantages with the competitors and the signal that the firm is not willing to expand (Bodnar et al., 1997; Boer et al., 2002; Hitt, et al., 1997). Until now the effect of narrowing the geographical focus on the abnormal returns is not enlightened because empirical results are as ambiguous as the hypotheses. Rüdisüli (2005) and Veld and Veld-Merkoulova (2004) could not prove a significantly positive relationship.

Furthermore, the hypotheses about the effect of the performance of the parent company on the abnormal returns are also diverse. One argumentation line contends that a positive market reaction follows the announcement of a spin-off, if there is a negative performance trend before the announcement. Thus Villalonga (2003) claims:

“Considered together with the findings about diversification, the findings about refocusing seem to indicate that, when firms are outperformed by their competitors, any change in their current strategy is welcome by the stock market”.

For this reason, announcing to spin-off a division, while facing a negative performance trend, should cause positive stock price reactions. However, the second hypothesis claims that the market perceives a spin-off announcement from firms with negative performance trends as “cry for help” in an unwinnable situation (Bartsch and Börner, 2007). So far no empirical study has proven significantly positive correlations between performance indicators and abnormal returns (Bartsch and Börner, 2007; Vollmar, 2014).

Additionally, the size of the spin-off and the parent company is found to cause larger wealth effects (Slovin et al., 1995). Veld and Veld-Merkoulova (2009) states that “This result is in line with intuition, since the impact of spinning-off a large division can be expected to be bigger than the spin-off of a relatively small division”. Moreover, the positive relationship could be based on the fact that larger companies and larger spin-offs create more attention because higher returns are expected. This effect is amplified by the fact that the equities of larger companies are traded more intensively.

Finally, the parent company‘s industrial sector could have an influence on the abnormal returns. Merely a few researchers analyzed the relationship between the industrial sector and the stock price reactions. Ostrowski (2008) and Stienemann (2003) could not identify dependencies of abnormal returns on the parent company‘s industrial sector. However, it was found that that the effect of diversification on performance is not homogeneous across different industries (Santalo and Becerra, 2008). This applies especially for the chemical and pharmaceutical industry which show a high complexity and degree of diversification (Hill and Hansen, 1991). This circumstance could be based on the unique characteristics of this industry which has been claimed as one of the most important sectors of the European economy (Chapman and Edmond, 2000). This industrial sector has been the most central focus of mergers and acquisitions activity since the 1980s which tend to be similar for the EU and the US market (Chapman and Edmond, 2000; Walter, 1993). Simultaneously, over the last decades chemical and pharmaceutical firms raised prominence as target for investors and private equity firms based on its fragmented industry holding high opportunities and threats in terms of high stock price reactions (Bee and Chelliah, 2013). These findings can be directly transferred to the topic of spin-offs. Since general attractiveness and promising de-/ investment strategy of the chemical and pharmaceutical industry has already been shown, spin-off announcements are expected to yield larger abnormal returns.

Nevertheless, more reasons exist as to why spinning-off a division is considered as trendsetting management tool. One of the most important characteristics of the chemical and pharmaceutical industry is “that it gave rise to many and diverse technologies which aimed at different markets, so that there are several sectors to be followed […]” (Achilladelis, Schwarzkopf, and Cines, 1990). Thus, chemical and pharmaceutical industry is highly connected to other industries and therefore has a huge influence on several industrial sectors. This industry represents a high complexity due to a high durability in numerous industrial classification schemes. Simultaneously, it undergoes a high demand for changing products and processes driven by ever-decreasing product lifecycles (Festel, 2014). Therefore, global competitiveness rises and the divestment of non-core businesses to narrow the industrial focus and to concentrate management activities in addition to financial resources on focus areas is becoming an imperative (Dewdney and Smith, 1998). Especially the increasing shareholder pressure demanding steady maximization of the gross-margin by optimizing the diversification strategy with the aim to ensure corporate growth causes the necessity of creating sophisticated spin-offs (Carnahan et al., 2010). However, previous empirical results merely give first evidence but serve as a starting point for further investigation of the wealth effects within the chemical and pharmaceutical industry.

In this paper spin-offs of the chemical and pharmaceutical industry are studied to amplify and substantiate the insights on wealth effects as a result of spin-off announcements. The number of spin-offs steadily increases from 1995 onward and the number of spin-off announcements before 1995 is small (Veld and Veld-Merkoulova, 2004). Since data availability until 2001 is rare, the period from January 2001 to October 2019 is investigated within the present study. Choosing this time period additionally ensures the timeliness and relevance of the present study. Thus, the findings can serve as guideline to decide whether and at which moment chemical and pharmaceutical companies should be included in present stock portfolios.

2 Hypotheses

Based on the variables that are described in section 1 the following hypotheses are deduced. All these hypotheses are derived from either spin-off or divestiture literature. Thus, there is already existing evidence that these factors could hypothetically affect the abnormal return‘s height.

Hypothesis 1: The cumulative average abnormal return in consequence of spin-off announcements in the chemical and pharmaceutical industry equals zero.

Hypothesis 2: The abnormal return is independent of the year of the spin-off announcement.

Hypothesis 3: Improving the industrial focus by spinning off company divisions which do not apply for the core business, has no impact on the CAAR.

Hypothesis 4: Increasing the geographical focus by spinning-off company divisions abroad, has no effect on the CAAR.

Hypothesis 5: A correlation between the parent company‘s performance before the spin-off announcement and the CAAR height exists.

Hypothesis 6: A correlation between the parent company‘s size before the spin-off announcement and the CAAR height exists.

Hypothesis 7: No correlation between the spin-off‘s size and the CAAR height exists.

3 Data description and methodology

3.1 Data description

The present study comprises a sample of spin-off announcements of the chemical and pharmaceutical industry. Thus, a spin-off of the chemical and pharmaceutical industry is defined as spin-off in which a company of the chemical and pharmaceutical industry separates from a specific division. The spin-off can be registered either in the same or in a different industrial sector. All spin-off announcements of the chemical and pharmaceutical industry are investigated irrespective of the operating country.

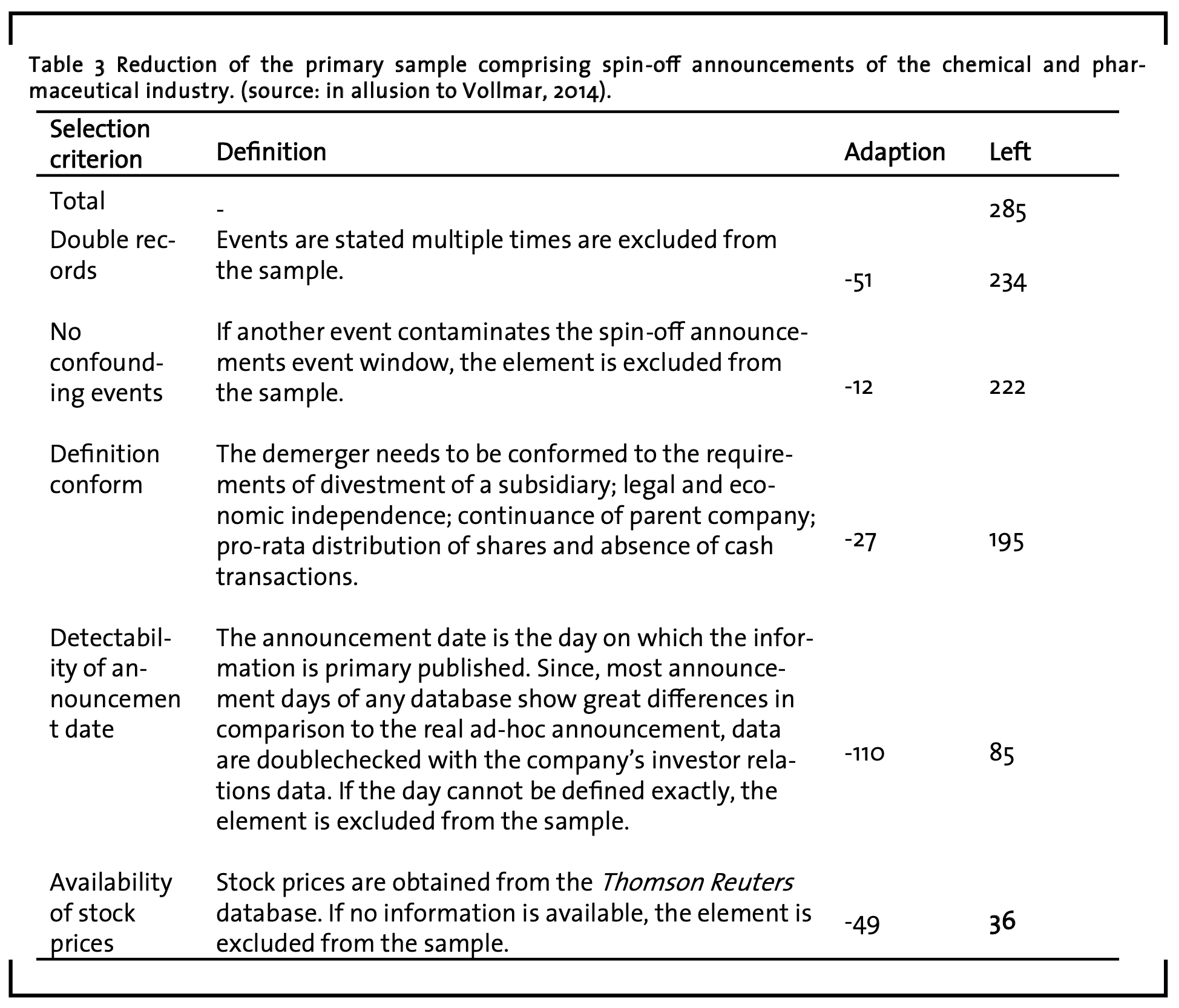

The sample contains all spin-off announcements from January 2001 to October 2019. The spin-off announcements are obtained from the Thomson Reuters Database, whereas exact announcement dates are derived from the investor relations of the respective parent company, since announcement dates in several databases are not accurate. Therefore, it is advised against using the exact dates from any database. It should better be assessed by the ad-hoc press releases of the respective companies which are published on the investor relations news. Data on stock prices, total assets, revenue, key performance indicators (KPI) and market indices are obtained from the Thomson Reuters Fundamentals Database. The market index chosen is the MSCI International World Price Index owing to its broad coverage of emerging markets (Neukirch, 2008). Classification of the industrial sector is based on the Global Industry Classification Standard (GICS®). GICS® codes are also derived from the Thomson Reuters database. The primary sample comprises 285 spin-off announcements of the chemical and pharmaceutical industry. However, a number of spin-off announcements had to be eliminated from the primary sample. Table 3 reports the reduction of the primary sample. First of all, the Databases sometimes list spin-off announcements several times. Therefore, double records have been identified and eliminated from the sample. Additionally, announcements where confounding events contaminate the event of interest were eliminated to ensure that stock price reactions are solely based on the spin-off announcement. The third reason why events are removed from the primary sample is that in some cases the spin-off did not conform the definition.

Moreover, spin-off announcements are excluded from the primary sample if the exact announcement date could not be identified, or no stock-price information are available for the parent company. The final sample contains 36 spin-off announcements of the chemical and pharmaceutical industry.

The final sample shows a large representation of spin-off announcements in the United States (US) with 18 observations (50%) which is based on two reasons. On the one hand, the US generally shows the highest number of spin-off announcements over all industries. On the other hand, the availability of stock price information and the detectability of the exact announcement date is more accurate in comparison to Eastern Europe and Asian regions (cf. Thomson Reuters Database). Moreover, Finland and the Netherlands are represented with three observations (8.5%), whereas Switzerland, Germany and Norway comprise two observations (6%) respectively. Out of these 36 spin-off announcements, six (17%) were announced in 2015 and five (14%) were announced in 2018 and 2019 respectively. A steady increase of spin-off announcements over the last two decades can be recorded and therefore the rising trend of spin-offs as strategic management and divestment tool (Wan, et al., 2011) can be proven.

3.2 Proxies

All variables that are utilized in the present study are related to the hypotheses listed in section 2.

Industrial focus

Narrowing the industrial focus is measured by using a dummy variable. The variable counts 1 if the GICS® code of the spin-off varies from the GICS® code of the parent company. The variable is 0 if both have the same GICS® code. The GICS® code is used because all observed companies trying to improve industrial focus spin-off a division that acts also in the chemical and pharmaceutical industry but in a sub-category. The GICS® code enables to detect these changes in industrial focus.

Geographical focus

An increase of the geographical focus can be measured by introducing a dummy variable. This variable is 1 if the headquarter of the spin-off is domiciled in a foreign country. The variable values 0 if the parent company‘s headquarter and the spin-off‘s headquarter are in the same country.

Size of parent company and spin-off

The size of the parent company has been measured by utilizing two variables. These two variables comprise the total assets and the revenue of the preceding account period before the spin-off announcement. Both variables are obtained from the Thomson Reuters Fundamentals.

Performance of parent company

The performance of the parent company is measured by two variables. The first variable is the Return on Assets (RoA) which has been widely proven as strong performance indicator (Selling and Stickney, 1989). The RoA is obtained from Thomson Reuters Fundamentals. The second variable is the change in RoA (the two preceding periods are taken as basis). This variable allows to monitor the current performance of the parent company right before the spin-off announcement.

3.3 Methodology

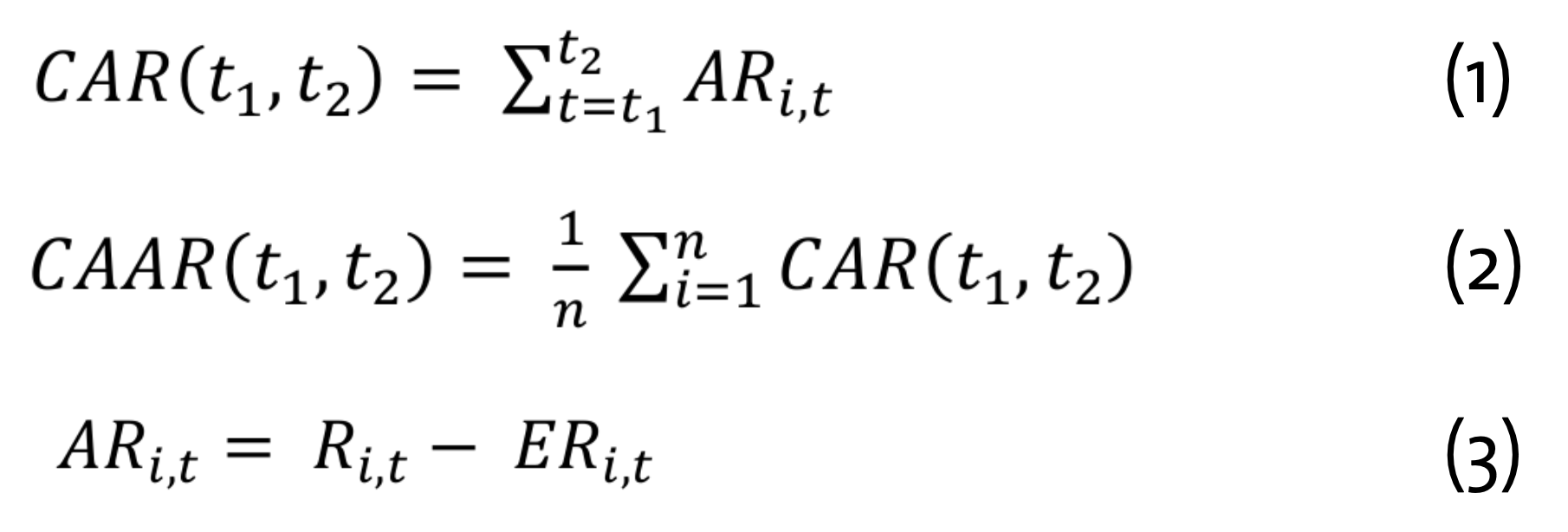

The wealth effects of spin-off announcements are measured using an event study methodology in the style of Hite and Owers (1983) and Miles and Rosenfeld (1983). Some adaptions and extensions are implemented in order to improve statistical power, validity and therefore explanatory power. However, the general calculation remains the same. The abnormal returns that represent market response to specific information measure all changes in shareholder value induced by the observed event (Fama et al., 1969). The abnormal return (AR) is the difference between the actual return (R) and the expected return (ER) based on the regression model (Campbell et al., 1997). Subsequently, the ARs of all of the days in the event window are cumulated and divided by the number of event days to calculate the cumulative abnormal return (CAR). Since most event studies analyze samples of more than one sample element, the cumulative average abnormal return (CAAR) is calculated by dividing the sum of all CARs by the number of sample elements. Since the sample covers a wide time frame with expansive and recessive market phases and also comprises a huge variety of companies, the actual return on average over the investigated event window equals zero.

Statistical model

In comparison to most event studies on wealth effects of spin-off announcements the present study consults the results of two separate statistical models in order to validate the findings. Thus, results of the market model and the market adjusted model are considered. The market model introduced by Sharpe (1963) is the most prominent statistical model for event studies. This statistical approach assumes a linear correlation between the company‘s return and the return of the market portfolio. In order to calculate the regression parameters an estimation window which does not overlap with the event window needs to be defined (Strong, 1992). In addition to the market model, the market adjusted model is utilized to verify the results of the market model and to improve the explanatory power of the present study. The market adjusted model postulates that the expected returns of the sample elements equal the returns of the market model (Campbell et al., 1997). For this reason, the necessity of defining an estimation window can be avoided. Both models on its own already demonstrably show a high statistical power (Brown and Warner, 1985; MacKinlay, 1997; Strong, 1992) but considering the results of both models increases the validity of the present findings.

Estimation window

Contrary to Hite and Owers (1983) which used a 200-day estimation window, within the present study a 250-day estimation window is defined as basis for the calculation of the regression parameters for the market model. The decision of adapting the estimation window for the market model is based on empirical results which demonstrate that a 250-day estimation window ensures stable model parameters and therefore the conduction of an appropriate regression analysis (MacKinlay, 1997). Thus, the regression parameters can be seen as market and risk adjusted (Brown and Warner, 1980).

Event window

The present work aims to provide for all contingencies by covering a wide range of event windows. These contingencies comprise the incorporation of information leaks about the event and deferred market reactions regarding the observed event (Acquisti, Friedman, Telang, and Alessandro Acquisto, 2006). Therefore, the event windows of [0], [-1;0], [0;1] and [-1;1] are used in this study.

Statistical/Significance tests

In contrast to most event studies, within this work two significance tests are conducted. Since Harrington and Shrider (2007) proved that merely about 5% of all event studies contain tests that are robust to cross-sectional variation, results of a parametric and a non-parametric test are compared. The parametric test is the Cross-sectional test and the non-parametric test is the Wilcoxon signed rank test. The Cross-sectional test is conducted as described in, e.g. Boehmer, Masumeci, and Poulsen, 1991, whereas the Wilcoxon signed rank test is applied to the present data sample as described in, e.g. Wilcoxon (1945) and Wilcoxon (1947). Blair and Higgins (1980) demonstrated that the Wilcoxon signed rank test perfectly complements parametric tests, such as the Cross-sectional test. Thus, conducting both significance tests and comparing the results strengthens the explanatory power of the present event study findings.

Moreover, the significance of the impact factors presented within section 1, are tested by a multiple linear regression analysis and the WELCH-test. Multiple linear regression analysis is a well-proven and commonly used tool for assessing the impact of several factors on the dependent variable (Myers and Myers, 1990). In this case the dependent variable is the abnormal return. However, the WELCH-test methodology is used because of its well-founded results for samples with a high variance heterogeneity (Tomarken and Serlin, 1986) and is conducted as described in, e.g. Welch (1947).

4 Results

4.1 Wealth effects

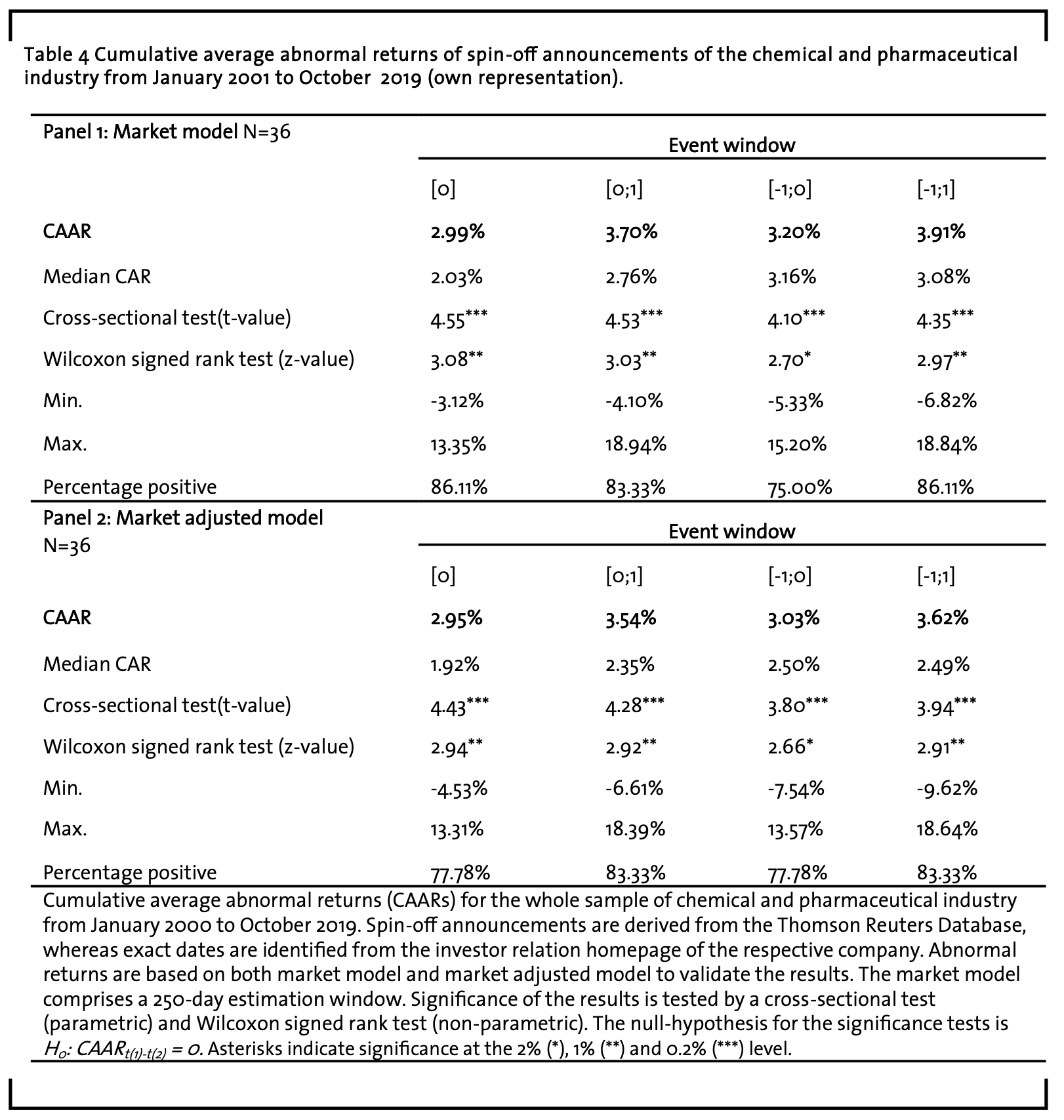

Table 4 summarizes the event study results for the whole sample of spin-off announcements of the chemical and pharmaceutical industry. The results show a cumulative average abnormal return of 3.91% for the event window from day -1 to day 1 within the market model. This result is significant at the 0.1%-level. These findings are proven by the market adjusted model which shows a cumulative average abnormal return of 3.62% for the same event-window which is also significant at the 0.1%-level. The abnormal returns for the other event windows are also significantly positive at the 0.1%-level.

This is a strong factor proving the validity of the present study, since many event studies can merely show one significant result for one single event window (Rosenfeld, 1984). However, these results are also confirmed by the non-parametric Wilcoxon signed rank test displaying a significance level of 2% for all event windows. Therefore, the present findings can be considered valid and hypothesis 1 can be declined.

Finding 1: Spin-off announcements of the chemical and pharmaceutical industry can be associated with significantly positive abnormal returns.

The present findings are in line with the previous results for the European and American market.

Furthermore, the first tendencies showing that especially the chemical and pharmaceutical industry shows high abnormal returns for spin-off announcements are supported by the present findings. In comparison to the abnormal returns calculated over all industries (c.f. Table 2), the chemical and pharmaceutical industry yields higher abnormal returns with merely one exception (Rosenfeld, 1984). Therefore, it can be assumed that spin-off announcements of the chemical and pharmaceutical industry raise higher expectations in terms of future stock price performance in comparison to other industries. This circumstance could be due to the characteristics of the chemical and pharmaceutical industry. These characteristics comprise the facts that the chemical and pharmaceutical industry is one the most prominent in America and Europe, that this special industry has many other industries to be followed and that this industry is already of major interest as target for investors and private equity firms (Bee and Chelliah, 2013; Chapman and Edmond, 2000). This favored position mainly based on the high opportunities in terms of higher-than-average returns (Scherer, 1993), draws interest of many investors. These promising opportunities are accompanied by high threats (Bee and Chelliah, 2013) which are often neglected given the potential of high market returns. However, in the case of spin-off announcements, the likelihood of surpassing returns for an investor is high when relying on the chemical and pharmaceutical industry. These findings are strongly in line with the topic of mergers and acquisitions, since this industrial sector has been the most central focus of mergers and acquisitions activity from the 1980s on and therefore offers the same surpassing opportunities (Chapman and Edmond, 2000; Walter, 1993). Nevertheless, further research is needed to detect the reasons why especially spin-off announcements in the chemical and pharmaceutical industry cause higher investor expectations. Although the present study provides first evidence on the effects of several impact factors by using multiple linear regression analysis and the WELCH-test, more research is required to, e.g. investigate the relationship of the different factors affecting the abnormal return‘s height.

Since it has already been shown that spin-off announcements of chemical and pharmaceutical companies cause significantly positive cumulative average abnormal returns and the present study comprise 50% US spin-off announcements, it can be assumed that abnormal returns are independent of the country of spin-off announcement. For this reason, the present study does not contain an analysis on the influence of the country of the parent company.

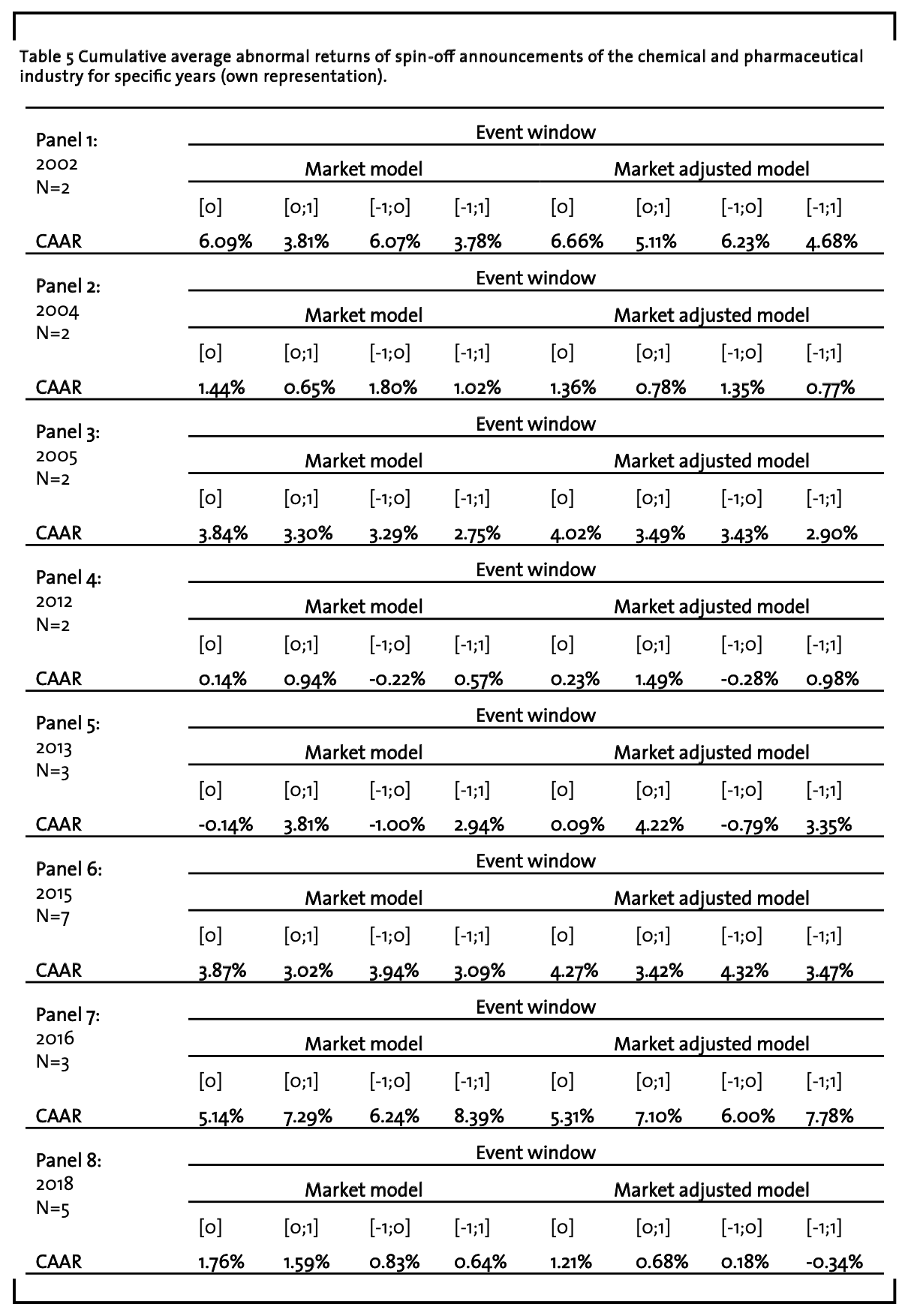

Positive cumulative average abnormal returns are found for every year in which minimum two spin-off announcements of the chemical and pharmaceutical industry took place. This is highly in line with the previous findings on the US and European market (Vollmar, 2014).

Finding 2: The abnormal return‘s height is independent from the year of spin-off announcement.

Several years are excluded from the analysis owing to a lack of observations. Additionally, some years do not show significant positive results which could be based on the fact that many years contain merely two spin-off announcements which decreases the statistical power of the test. This circumstance cannot be avoided when focusing on solely one industry because the number of observations is consequently smaller. Table 5 displays the abnormal returns for the years of the observations period separately. However, abnormal returns of up to 8.39% in 2016 and 6.74% in 2019 for the event window from day -1 to day 1 which is significant at the 5%-level support the general findings of high stock price reactions of chemical and pharmaceutical companies (Scherer, 1993).

These high returns which can be expected from spin-off announcements persuade investors to take the initiative risk and buy shares of chemical and pharmaceutical firms that want to spin-off a specific division. In consideration of the fact that maximum 22.5% of the chemical and pharmaceutical spin-off announcements (c.f. Table 4) for the event window comprising day 0 yield negative abnormal returns the risk of loss can be considered small. The fact that nearly all cumulative average abnormal returns are positive highly corroborates the conclusion based on the results of the whole sample. Thus, the conclusion contains the recommendation for investors to evaluate the possibility of integrating spin-off announcing company‘s stocks into current stock portfolios and investment funds. In order to validate and support this conclusion a long-term event study on the sustained effects of these companies is required.

4.2 Impact factors

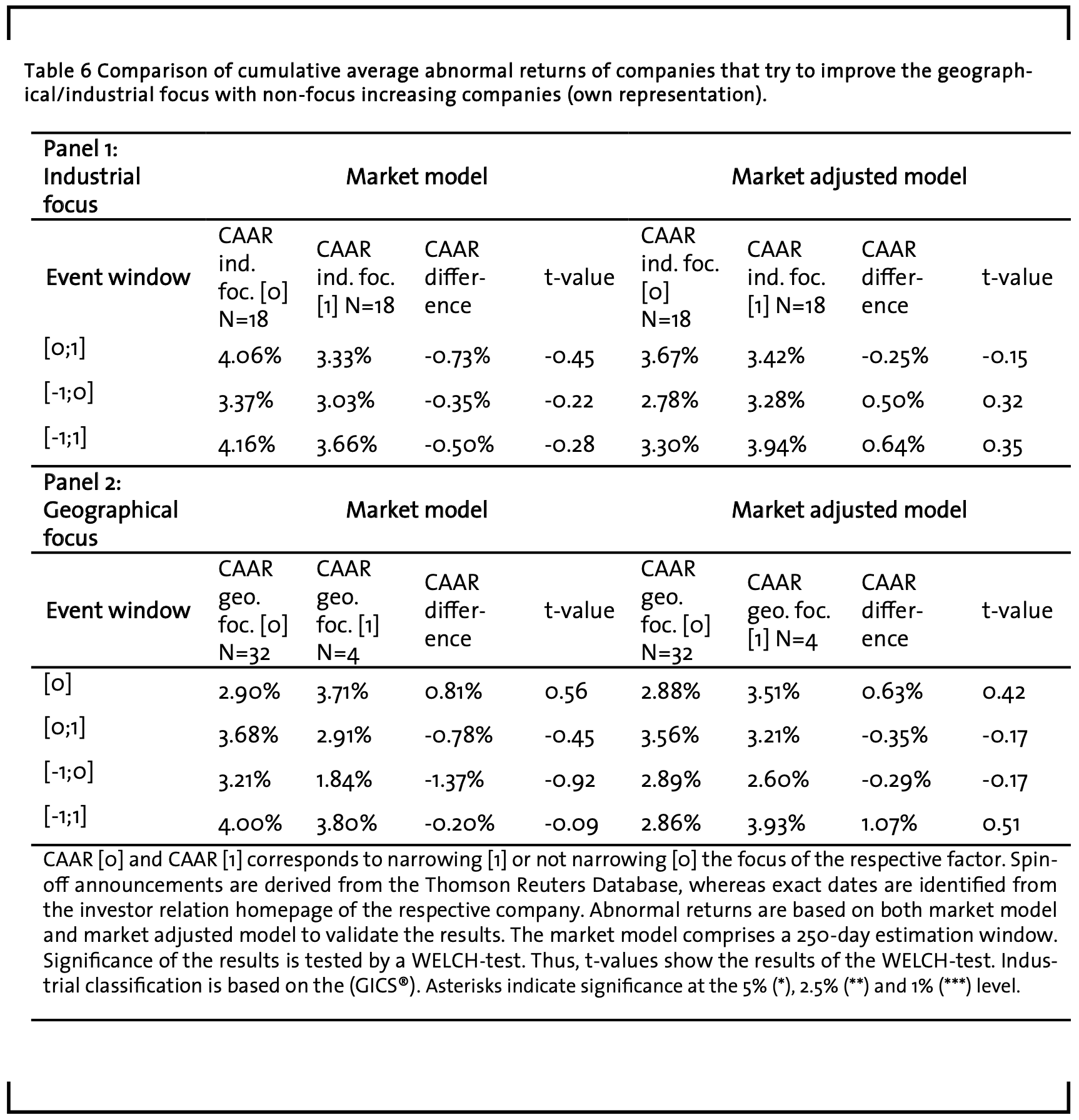

In Table 6 the event study results are presented for companies which try to improve either the industrial focus or the geographical focus by spinning-off a specific division. In panel 1 the cumulative average abnormal returns for companies that want to increase the industrial focus by separating from a division and for firms that do not want to increase the industrial focus are compared. It is shown that 18 firms pursue the goal to increase the industrial focus by spinning-off a division that works in another market. In contrast 18 companies do not intend to narrow their industrial focus in an analogous manner. Nevertheless, it should not be withheld that all 18 focus-increasing companies spin-off a division that are registered in a sub-category of the chemical and pharmaceutical industry. The GICS® code enables to detect these differences, since it also incorporates information on the sub-industrial registration of companies.

Since all focus-increasing companies solely announce spin-offs that will be registered in cognate industrial sectors, the focus-increasing effect is small. Therefore, the perception of an improvement of the industrial focus is weaker when a pharmaceutical company separates from a biotechnological company in comparison to a mining company that spins-off a real estate agency.

This is probably the main reason, why no significant differences between focus-increasing and non-focus increasing companies can be identified. The cumulative average abnormal returns of both sub-samples are very similar and thus the marginal differences that value from -0.73% to 0.64% are not significant. Consequently, hypothesis 3 can be rejected, as the aim of improving the industrial focus has no significant effect on the abnormal returns.

Finding 3: Aiming to improve the industrial focus by separating from a specific division has no significant effect on the abnormal return‘s height.

Thus, it can be hypothesized that the higher the difference of the spin-off‘s industrial sector to the core business of the parent company, the more positive is the shareholders‘ response to a spin-off announcement. This hypothesis is in line with the findings of Daley et al., (1997), Desai and Jain (1999) and Krishnaswami and Subramaniam, (1999) who identified positive effects of the aim to improve the industrial sector by analyzing solely the main industrial sectors according to the SIC code.

In panel 2 of Table 6 the abnormal returns of firms that increase their geographical focus by spinning of a company abroad and companies that do not want to narrow their industrial focus are compared. The geographical focus-increasing subsample comprises 32 spin-off announcements, whereas the non-increasing subsample merely contains 4 observations. However, the sub-sample of focus-increasing companies is associated with a mean cumulative average abnormal return of 3.06% over all event-windows and the non-focus increasing subsample exhibits a mean cumulative average abnormal return of 3.45% averaged over all event windows based on the market model. The market adjusted model shows similar results, as the mean cumulative average abnormal return is 3.05% for the companies that aim to increase the geographical focus and 3.31% for the firms that do not want to narrow the geographical focus. Therefore, hypothesis 4 can be seen corroborated.

Finding 4: The aim to improve the geographical focus by spinning-off a foreign subsidiary has no significant effect on the abnormal return‘s height.

These findings are in line with the results of Rüdisüli (2005) and Veld and Veld-Merkoulova (2004), who also could not find significant effects of changing the geographical focus on the abnormal returns. This could be based on the fact that the negative effects outweigh the positive effects. On the one hand, trying to increase the geographical focus creates the impression that the parent company is not willing to take initiative risks and expand to foreign markets (Bodnar et al., 1997; Boer et al., 2002). This behaviour represents a conservative corporate strategy, which is often associated with a decelerated company growth and constant but lower stock price amplitudes. On the other hand, by increasing the geographical focus risks can be minimized, complexity can be controlled and the cross-subsidization of company divisions abroad can be avoided (Hitt et al., 1997).

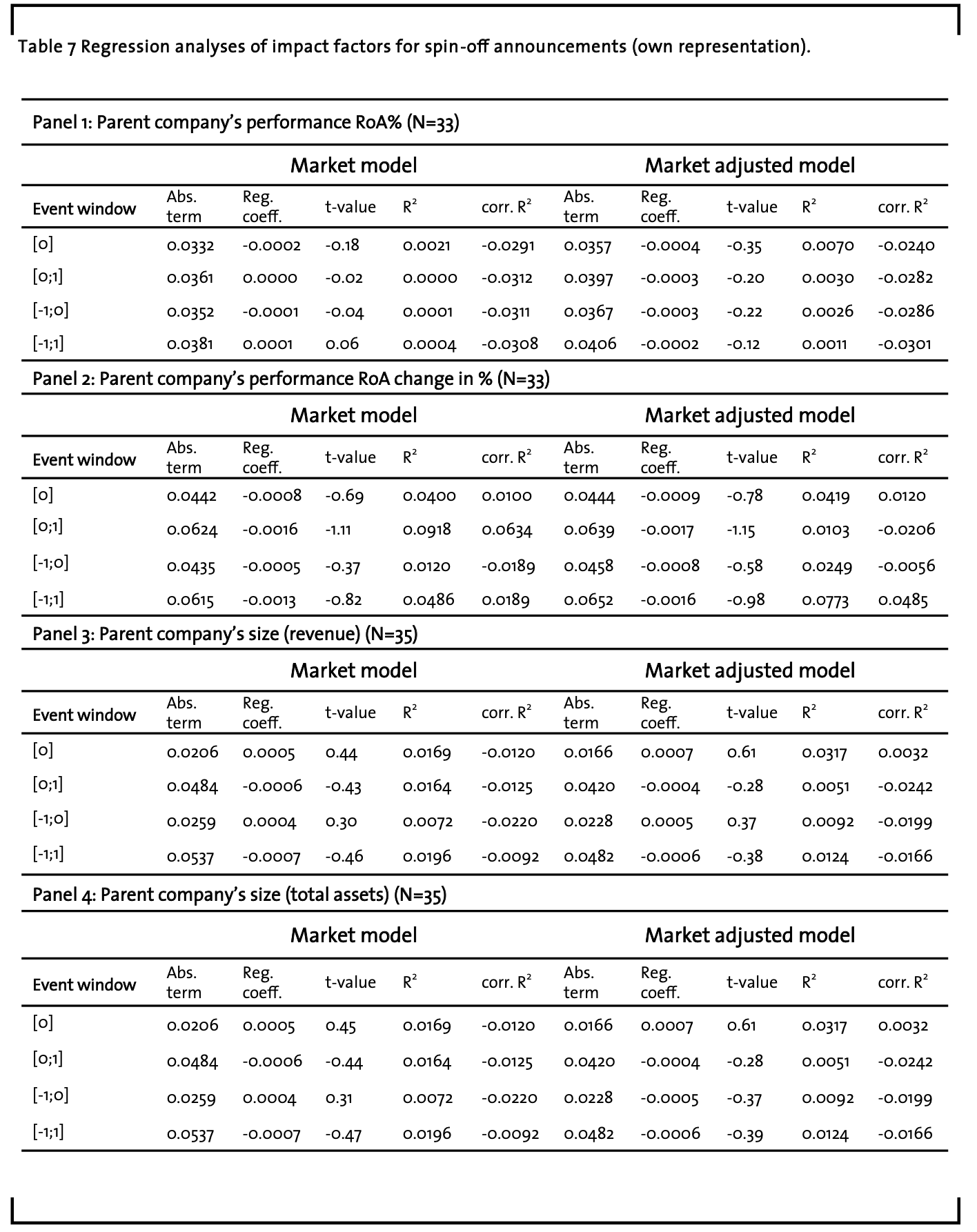

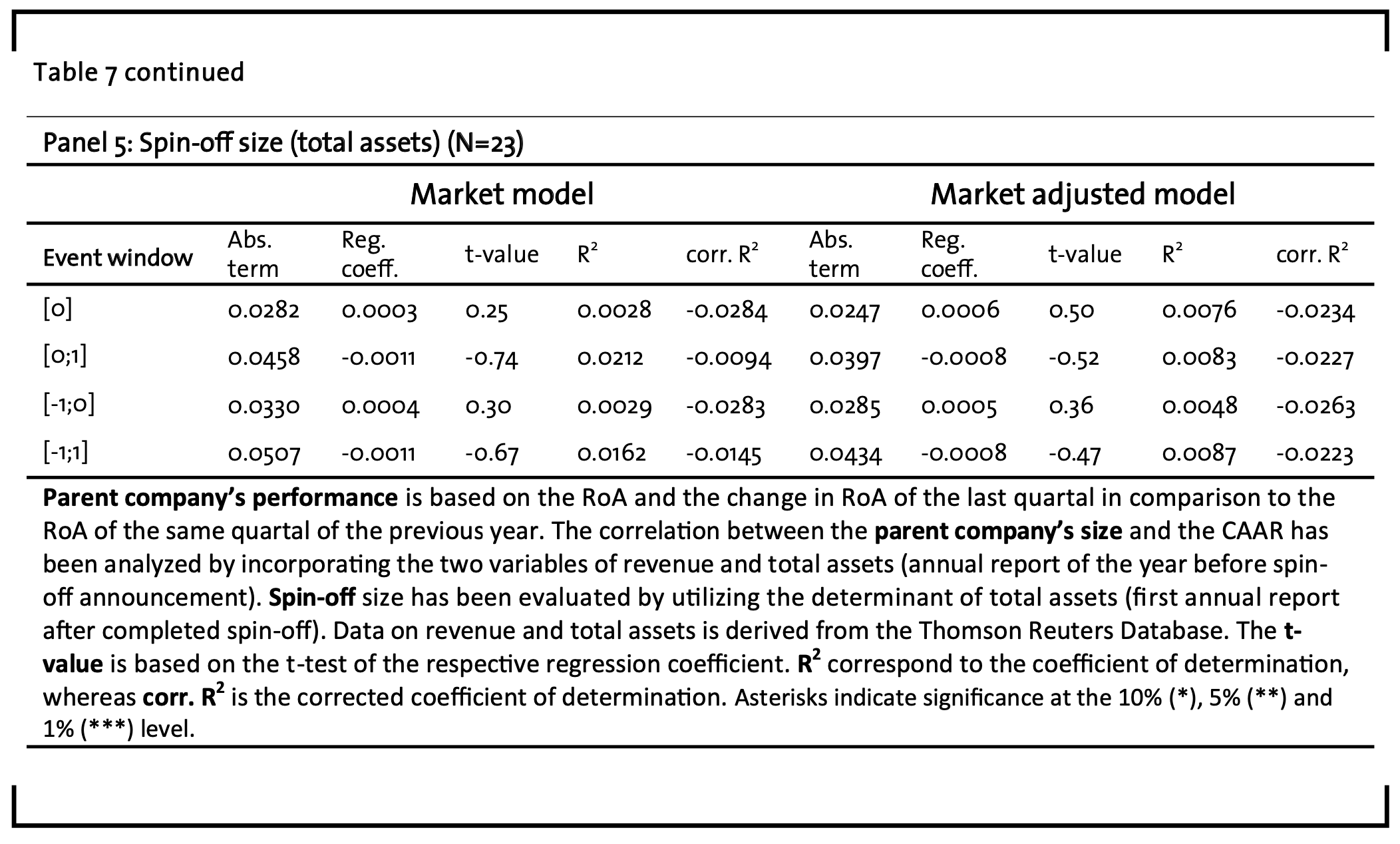

Table 7 presents the results of the regression analysis of factors that could potentially affect the abnormal returns. Unfortunately, some variables are only available for a limited number of observations of the sample. Especially, the variable spin-off size shows a lack of data. Therefore, merely 23 observations are incorporated into the regression analysis. The reason for this circumstance is that this variable is only available if the spin-off is already completed and spin-off size is deposited in the Thomson Reuters Database.

The first regression analysis presented in panel 1 and 2 of Table 7 shows that the parent company‘s performance has no significant regression coefficient, neither associated with the independent performance, which was measured by incorporating the RoA nor associated with the relativized performance analyzed by the change in RoA. The regression coefficient values nearly zero and is very similar for the market model and the market adjusted model. Hypothesis 5 therefore needs to be rejected.

Finding 5: The parent company‘s performance previous to the spin-off announcement has no effect on the abnormal return‘s height.

Similar to the factor of narrowing the geographical focus it can be assumed that negative and positive effects that accompany with the parent company‘s performance equalise each other.

The positive effects that are based on capital markets rewarding the corporate strategy adaption of weak performing firms in terms of announcing to spin-off a division (Villalonga, 2003), is countervailed by the perception of spin-off announcements as “cry for help” in an unwinnable situation of these firms (Bartsch and Börner, 2007). These findings are congruent with the previous results of Bartsch and Börner (2007) and Vollmar (2014). To date there is no evidence showing that a significant relationship between the parent company‘s performance and the abnormal returns exists. However, it again needs to be mentioned that all these studies have analyzed all industrial sectors, whereas the present study focuses solely on the chemical and pharmaceutical industry, which is already an industry with high margins and special characteristics, which are mentioned in section 1. This result again constitutes the necessity for further analysis of impact factors besides the regression analysis.

In panel 3 and 4 of Table 7 the influence of the parent company‘s size on the height of the abnormal returns is demonstrated. Similar to the regression analyses in the first two panels, the regression coefficient is not significant. This result is proven by both statistical models and over all event windows. For both variables the regression coefficients are nearly equal zero. This applies to both statistical models as well as for all event windows. Consequently, hypothesis 6 is rejected.

Finding 6: The parent company‘s size previous to the spin-off announcement has no effect on the abnormal return‘s height.

While the present findings support the results of Ostrowski (2008) and Vollmar (2014), the findings of Slovin et al. (1995) cannot be proven. Reasons why larger firms could yield higher abnormal returns are rare. The most prominent reason comprises the fact that larger companies gain more prominence and their shares are traded more intensively. This effect can be relativized nowadays because the ongoing development of information technology for trading and the continuous improvement of the required data lake, enable equity trading which is independent of the company‘s prominence (Vanstone and Finnie, 2009). Additionally, most shares traded on international stock exchanges come from automated trading systems (Huang et al., 2019).

In panel 5 regression parameters for the correlation between spin-off size and abnormal returns are presented. No significance for the regression parameters can be shown. This applies to all event windows and the two statistical models. Similar to the previous regression analysis the regression coefficient nearly equals zero. Therefore, hypothesis 7 cannot be proven.

Finding 7: The previous size of the spun-off subsidiary has no effect on the abnormal return‘s height.

However, it needs to be considered that a long observation period is analyzed. For this reason, several changes in the market environment are incorporated and therefore the likelihood of cross-correlations between the impact factors increases. The present analysis investigates each factor separately, whereas more research on the relationship between these factors is needed in order to provide more precise information as to how impact factor combinations could affect the abnormal returns. Especially for long observation periods the effects of these factors could compensate each other.

5 Summary and conclusion

The present study analyses the wealth effects in consequence of global spin-off announcements in the chemical and pharmaceutical industry. This work provides evidence that wealth effects of spin-off announcements vary across different industrial sectors. Therefore, the wealth effects are measured by event study analysis of spin-offs that were announced between January 2001 and October 2019.

The cumulative average abnormal return is significantly positive for all event windows and for both statistical models. The cumulative average abnormal return fluctuates between 3.91% for the three-day event window (market model) and 2.95% for the one-day event window (market adjusted model). In comparison to event study analysis incorporating all industrial sectors (c.f. Table 2) the present findings on chemical and pharmaceutical spin-off announcements provide evidence that wealth effects are higher for this industry which is probably linked to the high degree of diversification of chemical and pharmaceutical companies. All results are minimum significant at the 2.5%-level, whereas actually most abnormal returns are significant at the 0.1%-level which is rare for the event study methodology. It has to be mentioned that market model and market adjusted model strongly corroborate each other and that the cumulative average abnormal returns are invariably significantly positive. Moreover, the Cross-sectional test and the Wilcoxon signed rank test yield similar results with merely small deviations. These findings prove the statistical and explanatory power of the present study.

The present study also proves via multiple regression analysis that the cumulative abnormal returns are independent of the individual factors of parent company‘s performance, parent company‘s size and spin-off size. The first two factors are cross-checked by utilizing two variables for each factor. The results are the same for each variable. The findings on the parent company‘s performance and the parent company‘s size are in line with previous results of the European and American market. Indeed, in contrast to previous findings the present analysis shows no significantly positive correlation between the spin-off size and the abnormal returns. This could be based on the fact that this study comprises a long observation period and therefore the likelihood of crosscorrelations increases. It should not be withheld that the multiple regression analysis is not able to detect these cross-correlation and much more research is required to prove whether these impact factors affect the abnormal returns in combination.

Finally, the present article provides substantiated evidence on the outstanding wealth effects in consequence of spin-off announcements in the chemical and pharmaceutical industry. The findings of the present study give reason for investors and companies to prove either the integration of shares of these companies into present stock portfolio or to scrutinise how spinning-off a specific division could be beneficial for the current corporate strategy.

6 Limitations and outlook

A limitation of the present study is based on the low number of observations, which is due to the investigation of spin-off announcements from one single industrial sector. Nevertheless, there are no options to increase the sample size, since increasing the observed event-window to the years before 2000 is not possible because data availability for these years is very limited. The sample size is comparable to previous studies on this topic, which conducted a cross-industry study and the highly significant results prove that already an analysis with a sample size of 36 can provide reasonable evidence for the special position of the chemical and pharmaceutical industry. Another limitation is the small event-window of the analysis, which is not useable to prove sustained wealth effects of spin-off announcements. This would require a separate study since a different analysis approach needs to be applied. However, it has been shown that the majority of stock transactions is based on automatic systems and therefore the average time a stockholder owns a share values less than two days (Huang et al., 2019). Consequently, the short-term wealth effects are more relevant for shareholders and investors.

Previous research on spin-offs focuses mainly on the short-term stock price effects in the US. Therefore, much more research is required to investigate specific industries as well as other economic areas beside the US market. Furthermore, researchers should also analyse the advantages and disadvantages for the other two participants of a spin-off transaction, namely the mother company and the spin-off itself.

References

Achilladelis, B., Schwarzkopf, A., and Cines, M. (1990). The dynamics of technological innovation: The case of the chemical industry. Research Policy, 19(1), pp. 1–34.

Acquisti, A., Friedman, A., Telang, R., and Alessandro Acquisto, A. (2006). Is There a Cost to Privacy Breaches? An Event Study. In International Conference on Information Systems (ICIS) pp. 94.

Alli, K., Ramirez, G. G., and Yung, K. K. (2001). Withdrawn spin-offs: an empirical analysis. Journal of Financial Research, 24(4), pp. 603– 616.

Ball, J., Rutherford, R., and Shaw, R. (1993). The wealth effects of real estate spin-offs. Journal of Real Estate Research, 8(4), pp. 597–606.

Bartsch, D., and Börner, C. J. (2007). Werteffekte strategischer Desinvestitionen — Eine empirische Untersuchung am deutschen Kapitalmarkt. Schmalenbachs Zeitschrift Für Betriebswirtschaftliche Forschung, 59(1), pp. 2–34.

Bee, T. K., and Chelliah, J. (2013). Why Are Private Equity Firms Acquiring Chemical Distributors Worldwide? Journal of International Management Studies, 8(1), pp. 108–113.

Blair, R. C., and Higgins, J. J. (1980). The Power of t and Wilcoxon Statistics: A Comparison. Evaluation Review, 4(5), pp. 645–656.

Bodnar, G. M., Tang, C., and Weintrop, J. (1997). Both sides of corporate diversification: The value impacts of geographic and industrial diversification. National Bureau of Economic Research.

Boehmer, E., Masumeci, J., and Poulsen, A. B. (1991). Event-study methodology under conditions of event-induced variance. Journal of Financial Economics, 30(2), pp. 253–272.

Boer, D., Brounen, D., and Op ’t Veld, H. (2002). Corporate Focus and Stock Performance Evidence from International Property Share Markets. The Journal of Real Estate Finance and Economics, 31(3), pp. 263–281.

Brown, S. J., and Warner, J. B. (1985). Using daily stock returns: The case of event studies. Journal of Financial Economics, 14(1), pp. 3–31.https://doi.org/10.1017/CBO9781107415324.004

Brown, Stephen J., and Warner, J. B. (1980). Measuring security price performance. Topics in Catalysis, 8(3), pp. 205–258.

Bühler, R. (2000). Der spin-off als Instrument zur Unternehmensumstrukturierung: Darstellung unter Gesichtspunkten der Wertsteigerung. Verlag nicht ermittelbar.

Bühner, T. (2004). Unternehmensabspaltungen als Wertsteigerungsinstrument: eine empirische Untersuchung von Equity Carve-outs und Spin-offs in Europa. Kovac: Kovač.

Campbell, J. Y., Lo, A. W., and MacKinlay, A. C. (1997). The econometrics of financial markets. Princeton University press.

Carnahan, S., Agarwal, R., and Campbell, B. (2010). The Effect of Firm Compensation Structures on the Mobility and Entrepreneurship of Extreme Performers. Business, 801(January), pp.1–43.

Chapman, K., and Edmond, H. (2000). Mergers/acquisitions and restructuring in the EU chemical industry: Patterns and implications. Regional Studies, 34(8), pp. 753–767.

Chemmanur, T. J., and Paeglis, I. (2000). Why Issue Tracking Stock? Insights From a Comparison With Spin-offs and Carve-outs. Journal of Applied Corporate Finance, 14(2), pp. 102–114.

Daley, L., Mehrotra, V., and Sivakumar, R. (1997). Corporate focus and value creation: Evidence from spinoffs. Journal of Financial Economics, 45(2), pp. 257–281.

Desai, H., and Jain, P. C. (1999). Firm performance and focus: Long-run stock market performance following spinoffs. Journal of Financial Economics, 54(1), pp. 75–101.

Dewdney, J. M., and Smith, R. A. G. (1998). Putting a new spin on RandD assets in the pharmaceutical industry. Drug Discovery Today, 3(8), pp. 353–354.

Ernst, H., Witt, P., and Brachtendorf, G. (2005). Corporate venture capital as a strategy for external innovation: An exploratory empirical study. R and D Management, 35(3), pp. 233– 242.

Festel, G. (2014). Reasons for corporate research and development spin-outs – the chemical and pharmaceutical industry as example. R and D Management, 44(4), pp. 398–408.

Gertner, R., Powers, E., and Scharfstein, D. (2002). Learning about internal capital markets from corporate spin-offs. Journal of Finance, 57 (6), pp. 2479–2506.

Harrington, S. E., and Shrider, D. (2007). All Events Induce Variance: Analyzing Abnormal Returns When Effects Vary Across Firms. Journal of Financial and Quantitative Economics, 42 (1), pp. 229–256.

Hill, C. W., and Hansen, G. S. (1991). A longitudinal study of the cause and consequences of changes in diversification in the US pharmaceutical industry pp. 1977–1986. Strategic Management Journal, 12(3), pp. 187–199.

Hite, G. L., and Owers, J. E. (1983). Security price reactions around corporate spin-off announcements. Journal of Financial Economics, 12(4), pp. 409–436.

Hitt, M. A., Hoskisson, R. E., and Kim, H. (1997). International Diversification: Effects on Innovation and Firm Performance in Product-Diversified Firms. Academy of Management Journal, 40(4), pp. 767–798.

Huang, B., Huan, Y., Xu, L. Da, Zheng, L., and Zou, Z. (2019). Automated trading systems statistical and machine learning methods and hardware implementation: a survey. Enterprise Information Systems, 13(1), pp. 132–144.

Kirchmaier, T. (2003). The performance effects of European demergers. Centre for Economic Performance Discussion Paper, (566).

Krishnaswami, S., and Subramaniam, V. (1999). Information asymmetry, valuation, and the corporate spin-off decision. Journal of Financial Economics, 53(1), pp. 73–112.

Kudla, R. J., and McInish, T. H. (1988). Divergence of opinion and corporate spin-offs. Quarterly Review of Economics and Business, 28 (2), pp. 20–29.

MacKinlay, A. C. (1997). Event Studies in Economics and Finance. Journal of Economic Literature, 35(1), pp. 13–39.

Mansi, S. A., and Reeb, D. M. (2002). Corporate diversification: what gets discounted? The Journal of Finance, 57(5), pp. 2167–2183.

Miles, J. A., and Rosenfeld, J. D. (1983). The Effect of Voluntary Spin-off Announcements on Shareholder Wealth. The Journal of Finance, 38 (5), pp. 1597–1606.

Myers, R. H., and Myers, R. H. (1990). Classical and modern regression with applications (Vol. 2). Duxbury press Belmont, CA.

Neukirch, T. (2008). Alternative indexing with the MSCI World Index. Available at SSRN 1106109.

Ostrowski, O. (2008). Erfolg durch Desinvestitionen: Eine theoretische und empirische Analyse. Springer-Verlag.

Rosenfeld, J. D. (1984). Additional Evidence on the Relation Between Divestiture Announcements and Shareholder Wealth. The Journal of Finance, 39(5), pp. 1437–1448.

Rüdisüli, R. (2005). Value Creation of Spin-offs and Carve-outs. University_of_Basel.

Santalo, J., and Becerra, M. (2008). Competition from specialized firms and the diversification-performance linkage. Journal of Finance, 63 (2), pp. 851–883.

Schauten, M. B. J., Steenbeek, O. W., and Wycisk, E. M. (2001). Waardecreatie door spin-offs: aankondigingseffect en post-spin-off performance. Financieel Management, 21, pp. 69– 77.

Scherer, F. M. (1993). Pricing, Profits, and Technological Progress in the Pharmaceutical Industry. Journal of Economic Perspectives, 7(3), pp. 97–115.

Schipper, K., and Smith, A. (1983). Effects of recontracting on shareholder wealth. The case of voluntary spin-offs. Journal of Financial Economics, 12(4), pp. 437–467.

Schipper, K., and Smith, A. (1986). A comparison of equity carve-outs and seasoned equity offerings. Share price effects and corporate restructuring. Journal of Financial Economics, 15 (1–2), pp. 153–186. https://doi.org/10.1016/0304- 405X(86)90053-X

Selling, T. I., and Stickney, C. P. (1989). The Effects of Business Environment and Strategy on a Firm ’ s Rate of Return on Assets. Financial Analysts Journal, 45(1), pp. 43-52+68.

Sharpe, W. . (1963). A Simplified Model for Portfolio Analysis Author ( s ): Published byč: INFORMS Stable URLč: Management Science, 9 (2), pp. 277–293.

Sin, Y. C., and Ariff, M. (2006). Corporate spin-offs and the determinants of stock price changes in Malaysia. Working Paper, Monash University, February.

Slovin, M. B., Sushka, M. E., and Ferraro, S. R. (1995). A comparison of the information conveyed by equity carve-outs, spin-offs, and asset sell-offs. Journal of Financial Economics, 37(1), pp. 89–104.

Smolnik, T. (2020). Abspaltung einer umsatzgenerierenden Division – Welcher Wert geht von einem Spin-off aus? Corporate Finance, 1(2), pp. 53–60.

Stienemann, M. (2003). Wertsteigerung durch Desinvestitionen. Cuvillier.

Strong, N. (1992). Modelling Abnormal Returns: a Review Article. Journal of Business Finance and Accounting, 19(4), pp. 533–553.

Sudarsanam, S., Holl, P., and Salami, A. (1996). Shareholder wealth gains in mergers: Effect of synergy and ownership structure. Journal of Business Finance and Accounting, 23(5– 6), pp. 673–698.

Tomarken, A. J., and Serlin, R. C. (1986). Comparison of anova Alternatives Under Variance Heterogeneity and Specific Noncentrality Structures. Psychological Bulletin, 99(1), pp. 90–99.

Vanstone, B., and Finnie, G. (2009). An empirical methodology for developing stockmarket trading systems using artificial neural networks. Expert Systems with Applications, 36(3), pp. 6668–6680.

Veld, C., and Veld-Merkoulova, Y. V. (2009). Value creation through spin-offs: A review of the empirical evidence. International Journal of Management Reviews, 11(4), pp. 407–420.

Veld, C., and Veld-Merkoulova, Y. V. (2004). Do spin-offs really create valueč? The European case. Journal of Banking and Finance, 28(5), pp.1111–1135.

Villalonga, B. (2003). Research roundtable discussion: The diversification discount. Available at SSRN 402220.

Vollmar, J. (2014). Spin-offs, Diversifikation und Shareholder Value. Eine theorie- und hypothesengeleitete empirische Analyse europäischer Unternehmensabspaltungen.

Walter, I. (1993). The role of mergers and acquisitions in foreign direct investment. In The Global Race for Foreign Direct Investment pp. 151–175.

Wan, W. P., Hoskisson, R. E., Short, J. C., and Yiu, D. W. (2011). Resource-based theory and corporate diversification: Accomplishments and opportunities. Journal of Management, 37(5), pp. 1335–1368.

Welch, A. B. L. (1947). The generalization of “Student‘s” Problem when several different population variances are involved. Biometrika, 34(1/2), pp. 28–35.

Wilcoxon, F. (1945). Individual Comparisons by Ranking Methods. Biometrics, 1(6), pp. 80– 83.

Wilcoxon, F. (1947). Probability Tables for Individual Comparisons by Ranking Methods. Biometrics, 3(3), pp. 119–122.