Open innovation and firmperformance in small-sized R&D active companies in the chemical industry: the case of Belgium

Abstract

This paper relates the practice of open innovation in small R&D active chemical companies to firm performance in terms of employment and financial position. This relationship is examined during a period of economic downturn and applied to the Belgian situation. The Belgian case is interesting since it is characterised by high economic importance of the chemical industry and a strongly developed national (eco-) innovation system in the sector. According to their different evolution over the last decade, a distinction is made between basic chemicals and pharmaceuticals. In terms of open innovation strategy, a distinction is made between companies innovating completely internally (closed innovators), firms engaged in R&D outsourcing, firms engaged in research cooperation, and firms integrating outsourcing and cooperation in their knowledge sourcing strategy. After controlling for a broad range of R&D characteristics, we found that firms engaged in outsourcing or having an integrated open innovation approach performed better in terms of the evolution of employment during the period 2005-2010. Also, the analysis revealed firms having a formal R&D manager and a long-term research vision more often combine average to strong employment growth with a prosperous financial position.

1 Introduction

Innovation becomes increasingly complex and budgets and risks related to innovation force companies to carefully consider the use of external knowledge as a complement to inhouse innovative activities. This challenges innovation management (Chesbrough, 2006) since innovation becomes increasingly ‘distributed’ over various partners (von Hippel, 1988; Coombs et al., 2003) and ‘open’ in a way that firms adapt their business model in favour of both outside-in and inside-out exchange of specialized knowledge (Chesbrough, 2003).

This paper addresses research cooperation and outsourcing of R&D in the chemical industry. More particularly it classifies the innovation strategy according to the degree of openness to external knowledge and brings it into relation with firm performance. The focus is on small-sized firms in the chemical industry with Belgium as test case. The chemical industry in Belgium and Europe is characterized by declining market shares in the worldwide production and an increased importance of pharmaceutical business compared to basic chemicals.

Narula (2004) highlights a duality small firms are faced with when deciding to engage in external knowledge exchange in their innovation strategy. On the one hand, there is a challenge of lack of internal critical mass to deal with increasing budget requirements, complexity and risk. On the other hand, the engagement in external knowledge interaction might turn these firms into a vulnerable position in terms of knowledge leakage. This fits into the quest for equilibrium between research cooperation, R&D outsourcing and internal R&D.

The central research question addressed is whether differences in the engagement in external knowledge interactions influence the firm’s performance. The analysis is based on a representative sample of small firms in the chemical industry in Belgium. The period under consideration covers the years 2005-2010. The companies’ research profile at the beginning of this period is brought into relation with firm performance during this period. Firm performance is accounted for by means of the evolution in terms of overall firm employment and in terms of the financial position at the end of the period. The specificities of small firms in the chemical industry in Belgium as well as the setting of a financial and economic crisis are accounted for.

The paper is organized as follows. Section 2 provides an overview of the actual insights and understandings related to the place of research cooperation and R&D outsourcing in the firm’s innovation strategy and the particularities of small firms in the chemical industry in Belgium. Section 3 presents the database. The empirical analysis on the relation between innovation behaviour and firm performance forms the subject of Section 4. Reflections on implications for R&D management in small firms in the chemical sector conclude the work (section 5).

2 Open innovation in small firms in the chemical industry

2.1 Research collaboration and R&D outsourcing

The literature on ‘distributed’ (von Hippel, 1988) and ‘open’ innovation (Chesbrough, 2003; Chesbrough et al. 2006; Hunter and Stephens, 2010) emphasizes research cooperation and R&D outsourcing as important forms of external knowledge to complement the internal research base. Howells et al. (2003) relate this to a mounting competitive pressure for developing new products and processes combined with growing complexity and increased knowledge intensity (for a more recent overview see Huang and Rice, 2009).

Cohen and Levinthal (1990) define research cooperation as formal and informal ways of collaboration in which knowledge is generated that contributes to the internal knowledge base or in which the exchange of internally developed knowledge takes place (see also Veugelers and Cassiman, 1999; Coombs et al., 2003). The firm’s motives to engage in research cooperation mainly are threefold. Primarily, research collaboration enables the exploitation of economies of scale and scope in R&D, hereby reducing innovation costs and allowing to share risks (Röller et al. 1997). However, Cassiman et al. (2002) emphasize that in order to successfully co-operate, a sufficient degree of benefits of the properly or jointly generated knowledge (issue of knowledge appropriability and protection) is required to reduce free-rider possibilities by outsiders (see also Kesteloot and Veugelers, 1995 and Martin, 2002). Second, research cooperation is expected to improve the learning efficiency in absorbing external knowledge which fosters knowledge spillovers and the impact on innovative performance of incoming spillovers (Arrow, 1962; Romer, 1990). Finally, according to Hagedoorn (1993), research cooperation may facilitate access to knowledge which does not spill over and cannot easily be contracted through market transactions, i.e. intangible or tacit knowledge and know-how (see also Katsoulakos and Ulph, 1998). R&D outsourcing refers to a broad range of activities involving procurement of routine services, technology acquisition, commissioned or joint research (Odagiri, 2003). During the past decades an upsurge in outsourcing R&D has taken place (Jones, 2000; Narula, 2004; Lai et al., 2009;Huang et al., 2009) and it is increasingly viewed as part of strategic decision making (Chesbrough et al., 2006 ; Howells et al., 2008). R&D outsourcing aims at capitalizing on external knowledge – that is internally not available or that can’t be produced internally in a cost-effective way (Mol, 2005) – which can be licensed or bought (Gassmann, 2006). An important distinction in R&D outsourcing activities relates to core and non-core R&D activities. Non-core activities (mainly codified and relatively simple – Kogut and Zander, 1992) offer the opportunity to direct managerial attention and resource allocation to those tasks firms do best (Narula, 2001). Outsourcing core activities facilitates access to new knowledge and new technology complementary to internal capabilities. Similar to cooperation, following Teece (1986) and Chesbrough et al. (2006), outsourcing core activities occurs only in case sufficient appropriation of outsourced R&D is guaranteed. In this respect, outsourcing process-oriented tasks can help the firm in attaining more innovative R&D for any given level of investment (Friedman, 2010).

An important element in firm decision to engage in cooperation or R&D outsourcing is the distribution of (research and innovation) competences at firm level between research cooperation, R&D outsourcing, and in-house R&D. This involves balancing the use of external knowledge relations to explore new research areas with relatively less capital and lower risk involvement in case of failure with the risks of knowledge leakage and a deterioration of technological competitiveness. To minimize the latter risks, successful cooperation and outsourcing can be supposed conditional upon a sufficient internal R&D absorptive capacity (Cohen and Levinthal, 1990).

2.2 Small firms

In contrast with the ample attention paid to the study of open innovation in large (multinational) enterprises, relatively little is known about its implementation in small firms (Gassmann et al., 2010). Moreover, the benefits of open innovation in small firms are not straightforward. On the one hand, small sized firms present a higher R&D productivity because of their flexibility to exploit more efficiently knowledge generated outside the firm (see e.g. Audretsch and Vivarelli, 1996; Laursen and Salter, 2004). On the other hand, the absolute size limitations which may be enhanced by tendencies towards cross-border competition and multiple technological competences may be an important hampering factor for engaging in external knowledge interactions (Narula, 2004).

van de Vrande et al. (2009), using a sample of Dutch SMEs, put forward evidence that open innovation practices – among which external networking and R&D outsourcing – gained importance during the period 1999-2005. However, the implementation of open innovation practices is not without consequences. Compared to large firms, small firms are faced with balancing more limited resources to a wide range of aspects of the value chain in order to effectively market externally sourced and internally developed knowledge. Moreover, Narula (2004) clarifies that the potential loss of technological assets as a major issue particularly applies to research cooperation. This can be related to the necessity to guarantee and maintain outstanding internal competences in only a few or even a single technological area. Hence, R&D outsourcing and research cooperation involve certain risks in terms of losing leadership in scientific innovation and diminishing firm abilities to influence the direction of the innovation the R&D will aim at (Friedman, 2010). Another hampering factor for completely relying on internal innovation in small firms relates to restricted possibilities to recruit specialized workers (Rothwell and Dodgson, 1991). This drives small sized firms to rely on networks to identify and to make advantage of missing innovation resources (Vossen, 1998).

Gassmann et al. (2010) highlight a trend toward more R&D outsourcing and research cooperation which is reflected in an increased labour division in innovation. Simultaneously, a shift is witnessed from cost reduction to enhancement of value creation by means of inter-organisational relationships (Enkel, 2010). Small firms are challenged to cope with the induced trend of professionalising the internal processes to manage open innovation more effectively and efficiently in combination with limited internal resources. Narula (2004) refers to a threshold level of internal capacity to absorb the externally acquired information, involving both the availability of R&D experts and (in particular with regard to tacit knowledge developed and exchanged in research cooperation) managerial resources.

2.3 Small firms in the chemical industry in Belgium

During the period under study, the years 2005 till 2010, the world manufacture of ‘chemicals and chemical products (including pharmaceuticals)’ is characterized by an on average moderate but unequal growth rate across the globe. In this period, the world’s upand- coming economies (more specifically Asia- Pacific) have been gradually overtaking the US and EU and hence have been impacting heavily on the increased average world production (Cefic, 2011a; Datamonitor, 2011a).

The spill-over effects of the global economic downturn of 2008-2009 have had a strong impact on the overall chemical market. Data about the European chemical industry’s activity through 2009 indicate that some companies were experiencing a large pressure on their profit margins, which was particularly due to the lack in both customer demand and consumer spending (Cefic, 2011a). Except for Asia-Pacific, all regions had a negative growth rate in 2008 and 2009 in their production figures for the chemical industry as a whole (Cefic, 2011a). This negative trend, however, was not equal for all subsectors. In Europe, the economic crisis mainly affected the production of the subsectors inorganic base chemicals, petrochemicals and polymers, because these segments are much more dependent on business cycles than other chemical subsectors. In this respect, and in 2010, these subsectors experienced a stronger recovery than consumer and specialty chemicals (Cefic, 2011a). As in most other industrial sectors, the economic crisis caused many chemical companies as well as governmental institutions to diminish their activity and reconsider their R&D-projects related to the chemical industry. However, this approach always carries the risk of introducing too many short-term cost containment measures that importantly compromise the stability and predictability necessary for the chemical industry (and especially pharmaceuticals industry) to work efficiently (Efpia, 2010).

According to size classes, the European chemical industry consists of one fourth of small sized firms (i.e. 10 to 50 employees). Together with micro-sized firms (less than 10 employees) these firms accounted for over eighty (respectively seventy) percent of all companies in basic chemicals (respectively pharmaceutical), which means the total European chemical industry is characterized as an industry with many SMEs (Ecorys, 2009; Cefic, 2010). As SMEs typically lack the resources to conduct all steps in the ‘production’ of a good, from basic research through to marketing and distribution, they often specialize in innovation relating to a well-defined and narrow field. This also applies to the pharmaceuticals sector, where SMEs tend to focus on specific formulations of pharmaceutical products and often out-license or sell their innovations to larger companies that have the required resources, necessary for clinical trials and marketing (European Commission, 2009).

Belgium, one of the smallest European countries, is one of the largest world producers of chemicals and has been a home base for the chemical industry thanks to major innovations in the 19th and 20th century (Essenscia, 2011a). As a result, a diverse portfolio of chemistry-based industrial activities (including pharmaceutical activities) has developed in Belgium over the past two centuries (Essenscia, 2008). The basic chemicals segment was the largest segment in terms of value both in 2005 and 2010, followed by the pharmaceuticals subsector that had gained largely in importance in this five year period. This trend had been going on for some time (Essencia, 2008, Datamonitor 2005 and 2011b). The Belgian chemical industry has one of the highest degrees of specialization in the world and is one of the most integrated chemical clusters (FPS Economy, 2012). Belgium only represents about 2.7% of the European GDP and 2.1% of the total EU-27 population. However, the total Belgian chemical industry (including pharmaceuticals) covered in 2008 about 6% of the total EU-27 turnover, 6% of total investments, and 14% of the EU-27 total extra-European exports of chemical products (Essenscia, 2008). The comparatively very high level of Belgian chemical exports can be explained by the fact that many multinational firms use Belgium as an international transit centre, which implies that import-export trade in chemical products (especially pharmaceuticals) far outweighs the value of the domestic market (Ecorys, 2009). Furthermore, in 2009, Belgium was the number one country in the world producing chemical products (including pharmaceuticals) on a per capita basis and 11 of the world’s top 15 chemical companies had invested in Belgium by establishing production sites (Essenscia, 2011a). In 2010, the Belgian chemical industry (largely taken) accounted for a quarter of all the Belgian industrial activity, and employment in the sector remained stable in the past twenty years. The number of jobs in Belgian chemicals fell in 2009 – a year with difficult economic conditions – with 3.6% , to some 91,500 direct jobs. However, these job losses were lower than for the general manufacturing industry (-5.2%) (Essenscia, 2011b).

Based on national account data for Belgium (Belfirst – accessed August 2012) small firms (i.e. firms with less than 50 employees) accounted for 70% of all firms in the industry in 2005. During the period 2005-2010 their share remained relatively stable (1% increase). In terms of employment, by the year 2010, the firms categorised as small firms in 2005 increased their employment with 15% compared to an overall decrease with 3% in the sector over this period. In terms of number of firms, the weight of basic chemicals compared to pharmaceuticals is about five to one. Small firms in basic chemicals account for 72% of the number of firms and during the period 2005-2010 their employment increased with 10% compared to a sector reduction with 8%. Small firms in pharmaceuticals account for about three fifth of the enterprises and their employment increased with close to 60% compared to a sector average of 15%. As for the companies in the pharmaceuticals sector, Belgium had in 2010 more than 200 biotech and pharmaceutical firms, ranging from big pharmaceutical corporations to a large network of SMEs that specialize in all areas of biopharmaceutical fundamental and clinical research and manufacturing (FPS Economy, 2012). Because of these companies, Belgium was ranked in 2010 in the top 10 of most innovative (bio)pharmaceutical valleys in the world.

Six main reasons can be identified for Belgium being an attractive place for the chemical industry (Abrahamsen, 2011, Essenscia, 2011a and 2011b and FPS Economy, 2012): Belgium constitutes a unique logistical platform in the heart of Europe; it has a highly skilled labour force with world-class technical expertise for product and process technology and operational excellence; it provides attractive – including R&D – tax incentives for foreign investors; it developed a unique network to implement REACH (Registration, Evaluation and Authorisation of Chemicals) & CLP (Classification, Labelling and Packaging of substances and mixtures) which are both aimed at providing exchange of experience, knowledge and information between the chemical industry, the industry regulators and the service providers and at coordinating communication throughout the supply chain; it hosts and funds some of the major global and European research centres and a number of competence centres relating to the different segments of the chemical industry and there is a strong collaboration between the Belgian chemical industry and Belgian – and other countries’ – universities and top scientists, and there are many academic spin-off companies; and finally, the relatively high R&D investments in the Belgian chemical industry prepare the Belgian chemical industry for top-end innovation and are directed towards sustainable innovation, which in turn makes it possible for the many SMEs in the Belgian chemical industry to grow and innovate thanks to collaborating with other firms, research institutions and universities. The latter reasons refer to the strong regional innovation (eco)system – and more specifically the interactions with private and public research organizations – available in the Belgian chemical industry (see also Teirlinck and Spithoven, 2008) that is of crucial importance for the development of research and innovation (Cooke, 1992 and 2005) and for the enhancement of open innovation. As for knowledge sourcing and interaction, this ‘regional dimension’ is particularly important for the many SMEs within the chemical and pharmaceuticals industry because joint collaboration through all kinds of ‘open innovation’ initiatives carry substantially larger risks than is the case for larger companies (Incerti, 2008). The ample collaborations and synergies between the medical and academic worlds and the (bio) pharmaceutical research companies in Belgium generate a prosperous climate for the R&D of therapeutic innovations (Friedman, 2010), and the key contribution of this R&D in the pharmaceuticals sector is “to turn fundamental research into innovative treatments that are widely available and – even more importantly – accessible to patients” (Efpia, 2010, p. 5). Moreover, the ‘in-house’ research of SMEs is increasingly challenged because innovation often happens at the interface of several disciplines, with this scientific interdisciplinarity being extremely important for the innovative potential and hence future of the chemical industry (Essenscia, 2009).

2.4 Research focus

The focus in this paper is on R&D active small companies in the chemical industry. The central research question is whether differences in the engagement in external knowledge interactions influence these firms’ performances during a period of economic downturn. More specifically the R&D active small companies will be divided in closed innovators, innovators engaged in outsourcing, innovators engaged in cooperation, and integrated innovators (i.e. companies engaged both in R&D outsourcing and research cooperation).

Two aspects of economic performance will be taken into account. The main focus will be on the evolution of firm employment during the period under consideration. However, it is clear that the crisis also brought financial constraints, and this especially for risky and long-term oriented R&D activities in SMEs.

In Europe, most companies – large and small – reported large drops in demand since November 2008. However, most companies also had business areas that were less affected by this decrease in demand (European Parliament, 2009). The literature provides somewhat opposite and conflicting views with regard to the economic performance of small firms in times of crisis, and some researchers argue that small enterprises are more affected by the crisis than large firms. Generally speaking, because larger companies often have more potential for diversification, the economic crisis-related decrease in demand may not hit them as hard as is the case for highly specialized companies serving volatile markets. Moreover, while many large companies were finding it difficult and expensive to obtain major credit lines, SMEs were having even greater difficulties in obtaining guarantees and credit letters for imports and exports. As a result of the above, the credit ratings for a number of chemical companies have been downgraded, which has in turn prompted the banks to re-evaluate the entire industry (KPMG International, 2010).

However, according to others, and contrary to the general view above, in the chemical industry, the SMEs were less affected by the crisis than large chemical firms. In the chemical industry – and mainly this industry not including pharmaceuticals – the majority of the SMEs was not focused on a specific downstream industry at the beginning of the economic crisis and some SMEs were operating in niche markets, less affected by the crisis, which made them more ‘robust’ to overcome adversities in times of crisis. Moreover, to get over the crisis, the small chemical SMEs took fewer risks and they even used the recent boom to improve their capital base. On average, the chemical SMEs were also better equipped to deal with the consequences of the crisis than larger companies, because they were less active in the production of basic chemicals, the production segment that was affected the most by the crisis. The larger chemical companies were more strongly affected by the crisis, as due to past acquisitions, buyouts and stock buybacks, the chemical sector was more leveraged than before and therefore badly positioned to deal with these adversities, resulting in bankruptcy for some, while others were forced to sell their assets to pay their debts. In other words, it seems that SMEs in the chemical industry were better prepared for the adverse economic environment resulting from the crisis than some of their larger counterparts (European Parliament, 2009). These findings were confirmed in section 2.3.

3 Survey

The starting point for the empirical analysis is firm-level data on R&D in small enterprises in the chemical industry in Belgium in the year 2005. Following the EU definition (as from January 2005), a small firm is defined as a firm having less than 50 employees; an annual turnover or balance sheet not exceeding 10 million euro; and being autonomous in the sense that it is completely independent or has one or more minority partnerships (each less than 25%) with other enterprises. For the latter it should be noted that a company may still be ranked as autonomous in case the 25% threshold is reached or exceeded by public or institutional investors.

The empirical section in this paper puts into relation the openness of these companies for research cooperation and R&D outsourcing on the one hand and firm performance on the other hand. Data regarding research behaviour is provided by the bi-annual OECD business R&D survey for Belgium. This internationally standardized postal survey collects data regarding R&D (employment, cooperation, outsourcing …) and does so in a way to cover the population of permanent R&D active firms. Firms are classified into the chemical industry if (the bulk of) their R&D is performed in this business. The presented analysis is based on the R&D survey organized in the year 2006 and offering results for the period 2004-2005. The starting point is all permanent R&D active small firms in the chemical industry in Belgium in the year 2005. This information will help to create a profile of ‘openness’ to external knowledge for each company. The information is linked with information regarding firm performance from the annual account database (based on Belfirst) for the period 2005-2010. The aim is to identify differences in performance according to differences in research profile. In terms of performance, both the evolution in employment and the firm’s financial situation will be accounted for.

The starting point of the analysis is the official population of small firms engaged on a (quasi-) permanent basis in R&D activities mainly related to the chemical industry in Belgium in the year 2005. Based on the official OECD biannual business R&D survey for Belgium a population can be derived consisting of 100 enterprises. For each of these enterprises the R&D budget and personnel is known or can be accurately estimated based on previous and more recent information (for more details see: Commission Coopération Fédérale, 2001). These companies’ performance is investigated during the period 2005-2010. In order to give an accurate picture, firms that were part of a merger or acquisition during this period are excluded (6 companies are involved). Eight companies (or one out of twelve) went bankrupt. Apparently, small firms in the basic chemicals sector have been severely hit by the economic crisis since all of these bankruptcies took place in the period July 2009-December 2010. This is in line with the earlier observation that since November 2008 the economic situation for ‘manufacture of chemicals and chemical products (including pharmaceuticals)’ has deteriorated dramatically for Europe as a whole as well as in the European countries separately. Since we have full information for these companies for the period 2005-2010 they remain in the analysis. This leads to a target population of 94 R&D active small firms in the chemical industry.

The focus of this work is on the link between the firm’s openness to external knowledge interactions and economic performance. Information regarding these items is available for 67 companies. With respect to the 94 firms in the target population this is a 70% response rate. A comparison of the R&D personnel, R&D expenditures, overall employment and financial position (current ratio), and firm age revealed no significant differences between the cases included in the analysis and those excluded. Therefore, we can assume there is no response bias. We differentiate basic chemicals (41 companies) from pharmaceuticals (26 companies) because of their particularities both in terms of activities and evolution (see section 2.3).

Compared to the population of small companies in the chemical industry in Belgium in 2005 which consisted of 287 companies, the 100 R&D active enterprises represented 40.5% of the 6730 employees. During the years 2005- 2007 the total labour force of SMEs in the sector increased with over 5%, stagnated in 2008 and reached in 2010 a level almost 7% lower than in 2005. The share in employment of the R&D active small firms rose in that period to 44.5%. It is explained by a longer growth period (+12% in the period 2005-2008) and a decrease afterwards to arrive at a level slightly (-1%) below the employment level in the year 2005 (based on national account data).

4 Empirics

4.1 Profile of small R&D active companies in the chemical industry

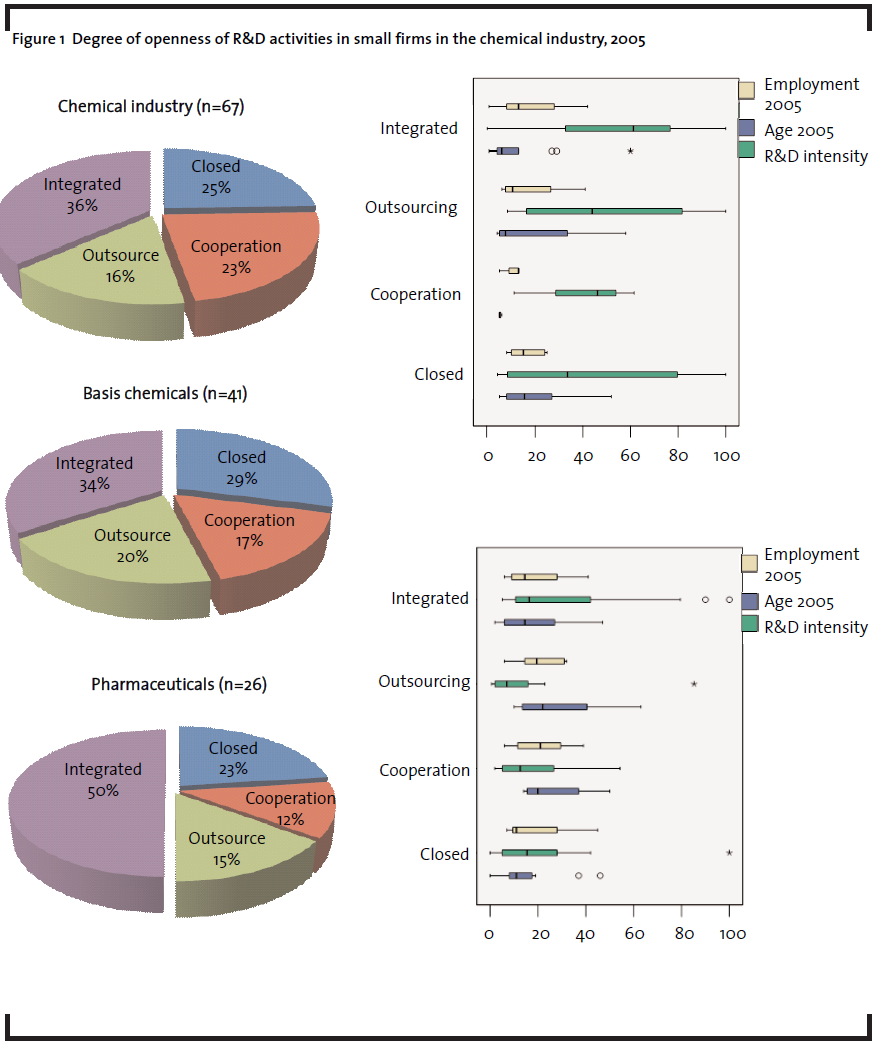

Figure 1 categorizes the companies according to four degrees of openness for external knowledge. A classification is made according to companies that perform research in collaboration with third parties, companies that outsource part of their R&D activities, companies that combine research collaboration and R&D outsourcing (referred to in this paper as companies with an integrated networking strategy), and closed innovators (neither engaging in research cooperation nor R&D outsourcing). Research cooperation involves both formal and informal knowledge development and knowledge exchange in research cooperation. R&D outsourcing relates to the outsourcing of parts of the R&D process since only companies are considered having an internal R&D base (i.e. having at least a certain level of absorptive capacity – Cohen and Levinthal (1989)).

For the chemical industry in its totality, close to two-fifth of the firms has an integrated innovation strategy. Over one-fourth has a closed innovation strategy. However, differences can be noted between basic chemicals (only one in three companies has an integrated strategy) and pharmaceuticals (half of the companies has an integrated strategy). Differences in the share of firms with a closed strategy are more modest. With regard to overall firm characteristics the box plots on the right-hand side of Figure 1 present the median (middle observation) and interquartile (50% of middle values) for firm age, average employment, and the share of R&D employment in the overall firm employment. Differences in firm profile in terms of age and average firm employment in relation with degree of openness are modest. In terms of employment, the median both in basic chemicals and in pharmaceuticals and for each of the four different degrees of openness is around 20 employees. In terms of age, a notable difference is that SMEs in pharmaceuticals that cooperate tend to be relatively younger firms whereas cooperation in basic chemicals rather takes place in longer-established small firms. The R&D intensity (share of R&D personnel in overall firm employment) is higher in pharmaceuticals and in firms engaged both in R&D outsourcing and research cooperation (integrated strategy). Also, R&D outsourcing in the basic chemical industry tends to be related to small firms with a lower R&D intensity. The findings with regard to R&D intensity could point to outsourcing of more routine tasks and are a first indication for the necessity of absorptive capacity to valorise external knowledge, or can also refer to complex or more advanced research activities which necessitate input from outside the company.

4.2 Company performance

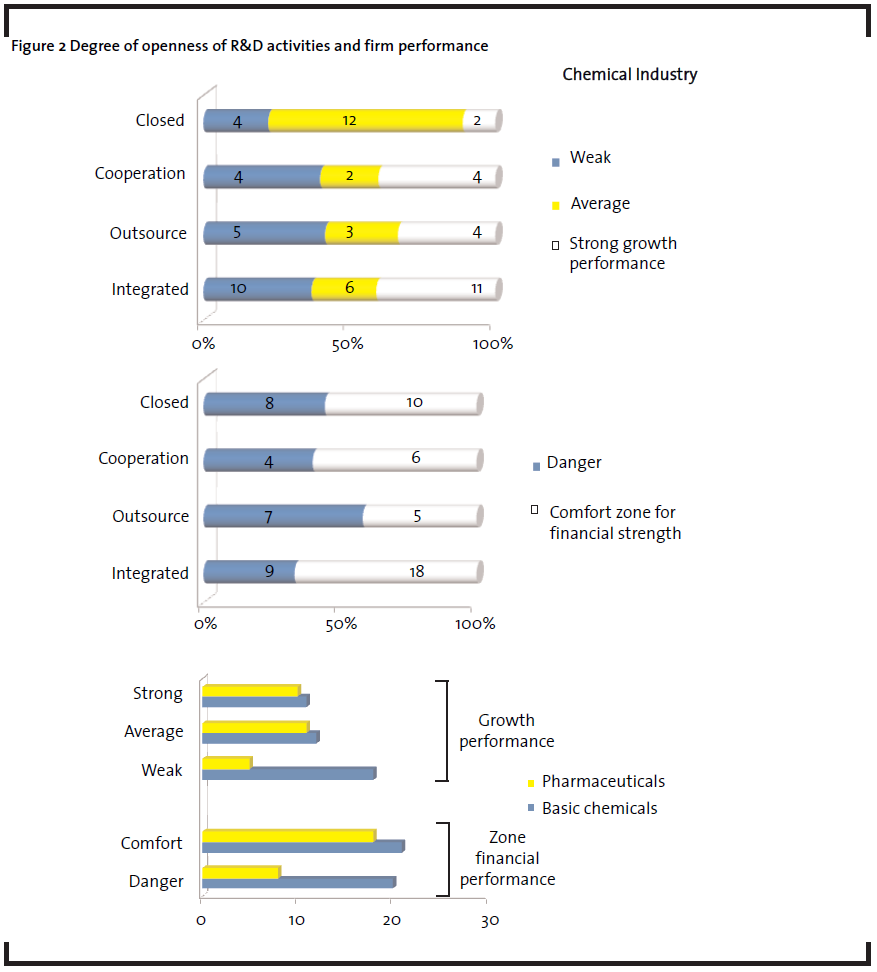

In the literature review, the evolution of firm employment and the firm’s financial position have been identified as important factors of firm survival. Figure 2 associates the different forms of openness in innovation strategy in the year 2005 with firm performance in the period 2005-2010. The lagged values for research compared to firm performance indicators account for the fact that good firm performance could lead to a particular behaviour in the innovation strategy with regard to the use of external knowledge relations.

Firm employment is measured as the evolution of the overall firm employment between the year 2005 and 2010. The firm’s financial situation is approximated by the current ratio (total current assets/total current liabilities) which is one of the best known measures of financial strength. The main question this ratio addresses is whether or not a firm has sufficient current assets to meet the payment schedule of its current debts with a margin of safety for possible losses in current assets, such as inventory shrinkage or collectable accounts. A generally acceptable current ratio amounts to 2 to 1. The optimum level can be sector depending but the minimum acceptable current ratio is obviously 1:1. In order to avoid strong fluctuations due to exceptional situations, the current ratio is calculated as the average ratio for the years 2009 and 2010. This ratio is of particular interest during a period of economic and financial downturn. Other financial indicators in terms of profitability and market share have been taken into consideration. However, based on the national account data for Belgium these indicators are lacking for close to half of the firms, and the indicators turned out to largely fluctuate from one year to another. This can be related to the fact that (unless some exceptions) small firms in Belgium have limited reporting duty in terms of annual accounts and balance sheet.

Figure 2 visualizes the evolution of the firms’ performances. In terms of employment, a distinction is made between weak performance (negative growth – including the eight companies that went bankrupt), average growth (increase of employment between 0 and 33%), and strong growth (increase with over one third in the period 2005-2010). For the financial position, the companies are divided in a group of companies situated in a comfort zone (current ratio of two and more) and those below this threshold.

An important difference exists between companies with a closed and those with a more open innovation strategy. The majority of firms that were relying solely on the internal R&D forces in the year 2005 experienced an average employment growth during the period 2005- 2010. Firms with a more open innovation strategy tend to be characterized by a more extreme growth performance. This both in a negative (weak growth) and a positive (strong growth) sense. As such, firms that relied on a closed strategy were more stable in terms of employment during the period 2005-2010. In terms of financial position, firms with an integrated innovation strategy mainly are situated in the comfort zone (propensity of 2:1). Firms engaged in outsourcing or cooperation solely as well as closed firms have a more or less equal propensity to be in the danger zone compared to the comfort zone.

The right hand part of Figure 2 reveals companies in the pharmaceutical industry being more successful both in terms of employment and in terms of financial situation. This is in line with the general economic tendencies for these industries as presented in section 2.3. Companies with a closed R&D strategy perform relatively better in terms of the evolution of employment in the basic chemicals whereas outsourcing activities seem to be positively related both to performance and to a financial buffer in the pharmaceutical industry (as presented in Table 1). With regard to the financial buffer it should be seen whether R&D outsourcing helps to create an additional buffer due to cost-effective reasons or whether a financial buffer creates room for outsourcing. Despite the relatively low number of observations in each cell these results indicate that a strong engagement in external knowledge relations is not a guarantee for economic success at firm level and confirm Narula’s (2004) findings with regard to protection of internal knowledge and preference for outsourcing activities rather than cooperation.

4.3 Broader set of R&D determinants for company performance

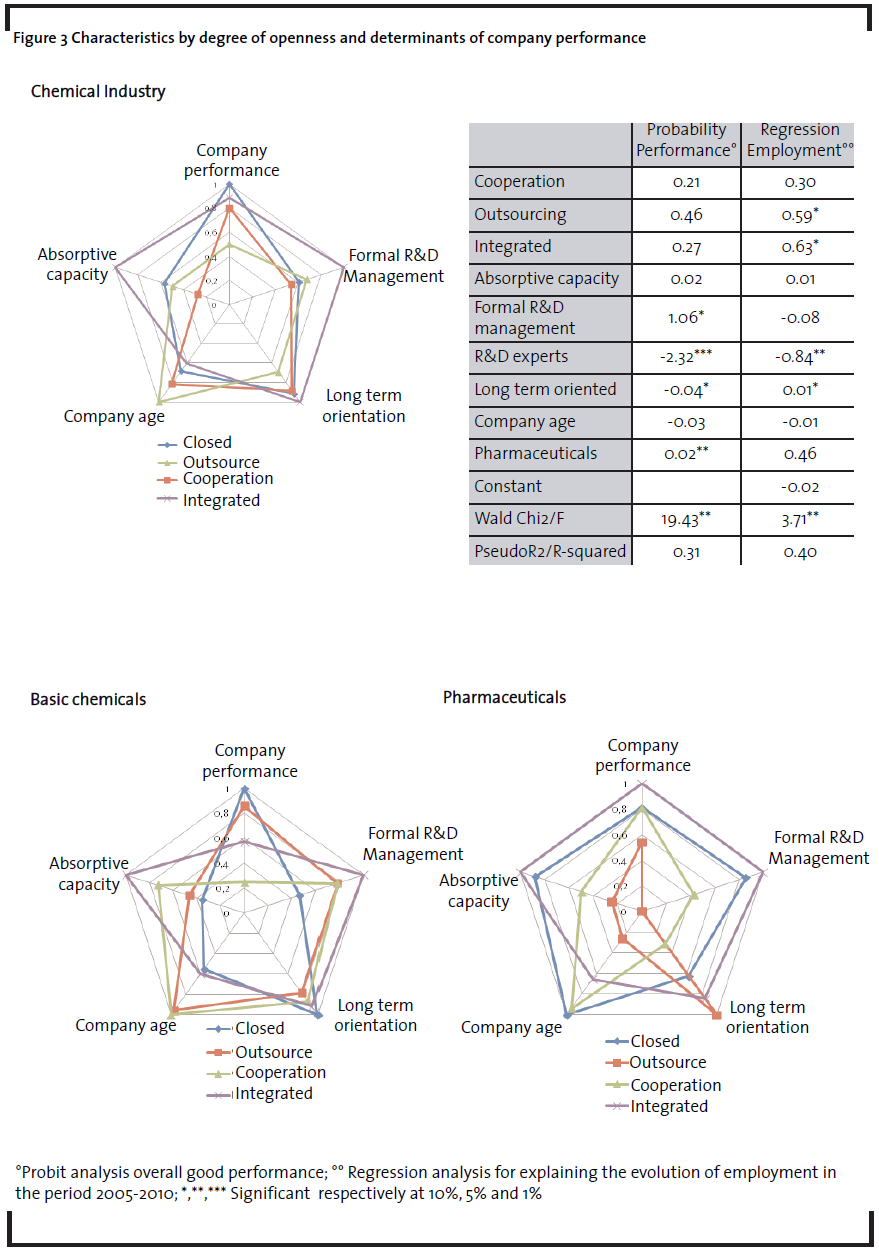

A main objective of this paper is to relate company performance to the degree of openness of the innovation strategy. A good company performance is related to a combination of a comfortable financial position and an average to strong growth in terms of evolution in employment. For the total of the chemical industry the upper left drawing in Figure 3 indicates the relation between different aspects of the company’s (research) profile with differences in openness in the innovation strategy. Account is taken of firm age, formal management (relates to the presence of an R&D manager), absorptive capacity (share in overall employment and the absolute number of R&D employment), and long-term orientation (share of research – versus development – in the R&D expenditures).

Firms with an integrated R&D strategy score high on all factors, except company age (these firms are on average younger companies). Also closed innovators on average are younger than firms engaged in cooperation or – in particular – outsourcing. Companies engaged in cooperation turn out to be more long term oriented. However, this picture is somewhat different for companies in basic chemicals compared to pharmaceuticals. First, important differences can be noticed in terms of cooperation. Companies in the basic chemicals engaged in cooperation are relatively more engaged in formal R&D management, are older and perform better compared to pharmaceutical companies engaged in cooperation. Also closed innovators in basic chemicals perform better and are more long term oriented in their R&D. By consequence, in the pharmaceutical industry cooperating firms are relatively younger, have less absorptive capacity and perform relatively worse. Also, firms in the pharmaceutical industry that are engaged in outsourcing rely relatively less on formal R&D management and firms with an integrated strategy perform relatively better. As could be seen from Table 1 the latter mainly is related to a good position in employment growth. On the right hand side of Figure 3, a probit regression analysis presents in a more analytical way the relationship between these variables and the firm’s performance. As explained before, a good company performance (binary variable: yes-no) is related to a combination of a comfortable financial position and an average to strong growth in terms of employment. The probit analysis is complemented with a regression analysis explaining the evolution of firm employment over the period 2005-2010.

The probit analysis reveals openness of the innovation strategy to exert no significant influence on firm performance (combined employment growth and financial position). Turning to the R&D related variable, the presence of formal R&D management and longer term oriented research positively influence the firm’s performance. By contrast, company age and especially the share of experts in the internal R&D personnel negatively influence firm performance. The latter is surprising but could be linked to the economic and financial crisis. The overall measurement of absorptive capacity (a combined measurement of critical mass of R&D employment and the intensity of R&D employment in overall firm employment) has no significant influence on firm performance. Of course, this should be seen in light of the fact that only (quasi-) permanent R&D active companies are part of the target population.

A refinement of the results in the regression analysis explaining employment growth provides a different picture. The analysis reveals both R&D outsourcing and an integrated innovation strategy at the beginning of the period to positively influence the evolution of overall firm employment during the period 2005- 2010. R&D outsourcing positively affects firm employment. These findings are in line with earlier findings by Teirlinck et al. (2010) concluding that R&D outsourcing does not negatively influence internal R&D employment. Also a longer term oriented research focus positively influences overall firm employment. By contrast the share of highly qualified experts in total R&D employment negatively influences employment evolution. This could be related to missing opportunities to valorise research findings within the company or to highly specialized or niche market activities in small firms heavily relying on this type of employee profile for R&D. Further qualitative research in this field is advisable. Finally, a similar regression model to explain the financial position of the company did reveal no significant influences of the variables under consideration. This does not necessarily mean that the influence is absent since the measurement of a good financial position remains a difficult endeavour. Both a below average and above average current ratio may point to a weakness. The former since there clearly is a lack of short term financial means. The latter could point to management incapability to make appropriate use of financial slack (Cyert and March, 1963).

5 Reflections on implications for R&D management in small firms in the chemical industry

This paper examined the relation between the use of external knowledge interactions and performance in small firms in the chemical industry. In a sector increasingly characterised by internationalisation of knowledge and research, small firms are disadvantaged due to their absolute size limitations which may be enhanced by tendencies towards multiple technological competences and cross-border competition (Narula, 2004). Moreover, high risk and uncertainty involved in research is hard to bear on the shoulders of small firms. Therefore, adapting an open innovation model with engagement in research cooperation and R&D outsourcing may – partly – compensate limited internal resources.

In an empirical analysis of a representative sample of R&D active small firms in the chemical industry in Belgium, the relationship between the extent of engagement in open innovation practices and firm performance has been examined.

The Belgian chemical sector is characterised by a strong economic importance, a high export orientation and the presence of a broad range of big multinational companies and research centres and a well developed (eco) innovation system. Like most of the other developed economies the sector is confronted with increasing international competition and decreasing market shares in the world production. The period under consideration covers the years 2005-2010, a period initially characterized by economic prosperity turning into a financial and economic crisis since the year 2008. The openness of research activities in the year 2005 is brought into relation with the firm’s economic performance in terms of employment growth as well as its financial position.

Differentiating according to the degree of open innovation, one fourth of the firms follows a closed R&D approach, compared to two-fifth combining both outsourcing and collaboration in research. About one sixth of the firms engages in outsourcing solely and almost one fourth does so in research cooperation. Firms active in basic chemicals tend to be less (one third) engaged in a combined cooperation-outsourcing approach compared to firms in the pharmaceutical industry (one out of two firms).

In line with the dominant tendency in Europe of a more positive evolution of pharmaceuticals compared to basic chemicals in the period 2005- 2010, firms active in basic chemicals turned out to perform weaker in terms of employment growth and more often face a danger zone in terms of ability to pay short term debts. In terms of openness of the innovation strategy, closed firms tend to perform at a more constant and average growth rate whereas firms more open for external knowledge interactions tend to perform further away from the average (very well or rather badly).

Taking into account a broad range of additional factors, openness of the innovation process is found to exert a positive influence on the evolution of firm employment; however only in case R&D outsourcing is involved. Firms solely engaged in research cooperation do not outperform firms following a closed R&D strategy. In terms of a combined successful employment evolution and a healthy financial position, no significant influence is noted by the degree of openness of the firm’s R&D strategy. Elements that do matter are the presence of formal R&D management and a long-term vision in research activities. Also, compared to more established firms, younger firms face more difficulties to perform well during a period of economic downturn. Taking the empirical findings presented in this paper into account, the answer to the central research question is not straightforward: the engagement of SMEs in open innovation practices in the chemical industry is not a priori a reason for later successful performance. It seems that companies that formally manage, have a long term orientation in R&D, and that outsource (non-core) R&D activities outperformed their counterparts not having these characteristics. These results should be seen in light of the particularities of the Belgian context and a period of economic downturn.

References

Abrahamsen, M., Acar, O., Brinded, B. and Rainisch, V (2011): The Belgian Pharmaceutical Cluster, Harvard Business School: Institute for Strategy and Competitiveness, Cambridge, Massachusetts.

Arrow, K. (1962): Economic welfare and the allocation of resources for invention, in: Nelson, R. (ed.), The Rate and Direction of Inventive Activity, Princeton University Press, Princeton, p. 609-626.

Audretsch, D. and Vivarelli, M. (1996): Firm size and R&D spillovers: evidence from Italy, Small Business Economics, 9, p. 249-258.

Cassiman, B. and Veugelers, R. (2006): In search of complementarity in innovation strategy: internal and external knowledge acquisition, Management Science, 52, p. 68-82.

Cassiman, B., Perez-Castrillo, D., Veugelers, R. (2002): Endogeneizing know-how flows through the nature of R&D investments, International Journal of Industrial Organization, 20, p. 775-799.

Cefic, (2010): Facts and figures 2010: The European chemical industry in a worldwide perspective, Cefic, Brussels, p. 1-13.

Cefic, (2011a): Facts and figures 2011: The European chemical industry in a worldwide perspective, Cefic, Brussels, p. 1-51.

Chesbrough, H. (2003): Open Innovation: The New Imperative for Creating and Profiting from Technology, Boston, Mass: Harvard Business School Press.

Chesbrough, H., Vanhaverbeke, W. and West, J. (2006): Open Innovation: Researching a New Paradigm, Oxford University Press, Oxford.

Cohen, W. and Levinthal, D. (1989): Innovation and learning: the two faces of R&D, Economic Journal, 99, p. 569-596.

Cohen, W. and Levinthal, D. (1990): Absorptive capacity: A new perspective on learning and innovation, Administrative Science Quarterly, 35, p. 128-152.

Commission Coopération fédérale, Groupe de concertation, Groupe ad hoc Profit (2001): Méthodologie pour l’estimation de l’effort de R&D des entreprises, Rapport interne SSTC: Brussels.

Cooke, P. (1992): Regional innovation systems: comparative regulation in the New Europe, Geoforum, 35, p. 365– 382.

Cooke, P. (2005): Research, knowledge and open innovation: spatial impacts upon organization of knowledge-intensive industry clusters, Paper presented at the conference of the Regional Studies Association ‘Regional Growth Agendas’, Aalborg, 28–31 May, p. 1–27.

Coombs, R., Harvey, M., Metcalfe, S. (2003): Analysing distributed processes of provision and innovation, Industrial and Corporate Change, 12, p. 1125-1155.

Cyert, M. and March, DJ. (1963): A Behavioral Theory of the Firm, Englewood Cliffs, Prentice-Hall: New York.

Datamonitor, (2005): Industry Profile: Chemicals in Belgium, Datamonitor US, NY.

Datamonitor, (2011a): Industry Profile: Global Chemicals, Datamonitor US, NY.

Datamonitor, (2011b): Industry Profile: Chemicals in Belgium, Datamonitor US, NY.

Ecorys (European Commission, DG Enterprise & Industry) (2009): Competitiveness of the EU: Market and Industry for Pharmaceuticals: Volume II: Markets, Innovation & Regulation, Ecorys, Rotterdam, p. 1-112.

Efpia (European Federation of Pharmaceutical Industries and Associations) (2010): The Pharmaceutical Industry in Figures, Efpia, Brussels, p. 1-41.

Enkel, E. (2010): Attributes required for profiting from open innovation in networks, International Journal of Technology Management, 52, p. 344 – 371.

Essenscia, (2008): Facts and figures: The Chemical and life sciences Industry in Belgium, Essenscia, Brussels, p. 1-42.

Essenscia, (2009): Skills for innovation in the European chemical Industry, Essenscia, Brussels.

Essenscia, (2011a): Belgium, a world champion for chemicals and plastics, Essenscia, Brussels, p. 1-49.

Essenscia (2011b): Sustainable Development Report, Essenscia, Brussels,p. 1- 97.

European Commission, DG Competition, (2009): Pharmaceutical Sector Inquiry, final report, European Commission, Brussels, p. 1-533.

European Parliament: Policy Department Economic and Scientific Policy (2009): Impact of the Financial and Economic Crisis on European Industries, European Parliament, Brussels, p. 1-65.

FPS Economy, SMEs, Middle Classes and Energy (2012): Belgium: Important Industries and Innovative Companies, available at http://ib.fgov.be/en/ important_industries/, accessed at 17 May 2012.

Friedman, Y. (2010): Location of Pharmaceutical Innovation: 2000-2009, Nature Reviews: Drug discovery, 9(11), p.835-836.

Gassmann, O. (2006): Opening up the innovation process: towards an agenda, R&D Management, 36, p. 223-228.

Gassmann, O., Enkel, E., and Chesbrough, H. (2010): The future of open innovation, R&D Management, 40, p. 213-221.

Hagedoorn, J. (1993): Understanding the rationale of strategic technology partnering: interorganizational modes of cooperation and sectoral differences, Strategic Management Journal, 14, p. 371-385.

Howells, J., James, A. and Malik, K. (2003): The sourcing of technological knowledge: distributed innovation process and dynamic change, R&D Management, 33, p. 395-409.

Howells, J., Gagliardi, G. and Malik, K. (2008): The growth and management of R&D outsourcing: evidence from UK pharmaceuticals, R&D Management, 38, p. 205- 219.

Huang, F., Rice, J. (2009): The role of absorptive capacity in facilitating “open innovation” outcomes: a study of Australian SMEs in the manufacturing sector, International Journal of Innovation Management, 13, p. 201-220.

Huang, Y., Chung, H. and Lin, C. (2009): R&D sourcing strategies: determinants and consequences, Technovation, 29, p. 155-169.

Hughes, B. (2010): Evolving R&D for emerging markets, Nature Reviews: Drug discovery, 9(6), p.417-420.

Hunter, J., Stephens, S. (2010): Is Open innovation the way forward for big pharma?, Nature Reviews: Drug discovery, 9(2), p.87-88.

Incerti, C. (2008): An audience with Carlo Incerti, Nature Reviews: Drug discovery, 7(8), p.638.

Jones, O. (2000): Innovation management as a postmodern phenomenon: the outsourcing of pharmaceutical R&D, British Journal of Management, 11, p. 341-356.

Katsoulakos, Y., Ulph, D. (1998): Endogenous spillovers and the performance of research joint ventures, Journal of Industrial Economics, 46, p. 333-354.

Kesteloot, K., Veugelers, R. (1995): Stable R&D cooperation with spillovers, Journal of Economics of Management Strategy, 4, p. 651-672.

Kogut, B., Zander, U. (1992): Knowledge of the firm, combinative capabilities, and the replication of technology, Organisation Science, 3, p. 383-397.

KPMG International (2010): The Future of the European Chemical Industry, available at http://www.kpmg.com/BE/en/IssuesAndInsights/ArticlesPublications/Documents/201001%20EuroChem_Europe_Final.pdf, accessed at 23 May 2012.

Lai, E., Riezman, R., Wang, P. (2009): Outsourcing of innovation, Economic Theory, 38, p. 485-515.

Laursen, K., Salter, A. (2004): Searching high and low: what types of firms use universities as a source of innovation?, Research Policy, 33, p. 1201-1215.

Martin, S. (2002): Spillovers, appropriability, and R&D, Journal of Economics, 75, p. 1-32.

Mol, M. (2005): Does being R&D intensive still discourage outsourcing? Evidence from Dutch manufacturing, Research Policy, 34, p. 571-582.

Narula, R. (2001): Choosing between internal and noninternal R&D activities: some technological and economic factors, Technology Analysis and Strategic Management, 13, p. 365-387.

Narula, R. (2004): R&D collaboration by SMEs: new opportunities and limitations in the face of globalisation, Technovation, 24, p. 153-161.

Odagiri, H. (2003): Transaction costs and capabilities as determinants of the R&D boundaries of the firm: a case study of the ten largest pharmaceutical firms in Japan, Managerial and Decision Economics, 24, p. 187-211.

Roach, M., Sauermann, H. (2010): A taste for science? PhD scientists’ academic orientation and self-election into research careers in industry, Research Policy, 39, p. 422-434.

Röller, L., Tombak, M., Siebert, R. (1997): Why firms form research joint ventures: theory and evidence. CEPR Discussion Paper, no 1654.

Romer, P. (1990): Endogenous technological change, Journal of Political Economy, 98(5), p. 71-102.

Rothwell, R., Dodgson, M. (1991): External linkages and innovation in small and medium-sized enterprises, R&D Management, 21, p. 125-138.

Teece, D. (1986): Profiting from technological innovation, Research Policy, 15, p. 285–305.

Teirlinck, P., Dumont, M., Spithoven, A. (2010): Corporate decision-making in R&D outsourcing and the impact on internal R&D employment intensity, Industrial and Corporate Change, 19, p. 1867-1890.

Teirlinck P., Spithoven A. (2008): The spatial organisation of innovation: open innovation, external knowledge relations and urban structure, Regional Studies, 42 (June 2008), p. 689-704.

Jones, A., Spurling, T., Simpson, G. (2006): Innovation strategies for the Australian Chemical Industry, Journal of Business Chemistry, 3(3), p. 9-25.

van de Vrande, V., De Jong, J.P.J., Vanhaverbeke, W., de Rochemont, M. (2009): Open innovation in SMEs: Trends, motives and management challenges, Technovation, 29, p. 423-437.

Veugelers, R., Cassiman, B. (1999): Make and buy in innovation strategies: evidence from Belgian manufacturing firms, Research Policy, 28, p. 63-80.

von Hippel, E. (1988): The Sources of Innovation. New York: Oxford University Press.

Vossen, R.W. (1998): Relative strengths and weaknesses of small firms in innovation, International Small Business Journal, 16, p. 88-94.