Pricing in the crisis? An empirical analysis

In an empirical survey on pricing, team steffenhagen GmbH analyzed the impact of the financial and economic crisis 2008 / 2009 on the chemical industry. 80 pricing managers gave insights into the effects of the crisis, the concernment triggered by the crisis and the countermeasures that were employed in the companies.

The analysis uncovers success factors which promise successful pricing in times of crises. These include, among others, a high pricing performance already before the crisis, a clear structure of the pricing processes, a result-oriented alignment of the pricing, a good knowledge of the advantage of the own products in the processes of the customers and in the competitive environment, as well as pro-active pricing approaches. During the crisis, it is vital to gain more information on the financial situation of the customers to substantially invest in marketing and distribution, to limit abatements, and to ensure professionalism in pricing despite the turbulences of the crisis. In summary, these factors denote sufficient reasons for an increase of professionalism of the pricing.

1 Background

Shortly after the first outcomes of the collapse of prices in the American real estate market in February 2007, it took about 1.5 years until the crisis left perceptible marks in the real economy and with that also in the chemical industry. Sales and profit collapsed, productions were closed down, and reduced working hours were the often documented consequences.

Although it remains unclear whether the crisis is over, many indicators point upwards. As an example, the orders of industries not directly linked to the automotive sector are increasing. Temporarily shut down chemical plants resume production at an increasing rate and the association of the chemical industry in Germany (VCI) expects a 5% production and 6% sales growth rate for 2010.

On the other hand, it is still a long way until the high values of the first half-year in 2008 will be in reach, and there are already new voices who indicate the risk of further bubbles. The weekly German magazine “Die Wirtschaftswoche”, for example, has already warned against a new bubble in the Chinese real estate and share markets – induced by trade cycle policies – in December 2009. Regardless of whether the light at the end of the tunnel is only in sight or already reached, the consequences of the financial crisis on the chemical industry were serious, and reason enough for team steffenhagen to investigate the details.

With regard to the financial crisis 2008 / 2009, team steffenhagen’s target was to identify arising challenges for companies in the chemical industry and to assess their impact on the firms’ pricing strategies. More specifically, the survey illuminated the following aspects in detail:

- Which pricing strategies did the companies have before the crisis?

- Which impact did the crisis have on the companies’ pricing strategies?

- How did the companies react?

- What can we learn from the crisis in terms of pricing?

2 The way into the crisis

In February 2007, the break in US-American real-estate prices left its first traces: The HSBC Bank in London had to release the first profit warning in its history because of the multi-million loan default of the US-daughter Household. Two weeks later, US-Boss Bobby Mehta lost his job because of this development. Hardly anybody suspected yet one of the biggest world economic crises was ringed in.

US-Finance Minister Hank Paulson only talked about „limited credit problems“. In May 2007, also the Federal Reserve Chairman of the US Ben Bernanke was sure about the crisis to be limited to the American real-estate market.

How wrong he was became clear in July 2007, when the IKB (Deutsche Industriebank KG) in Germany was hit, and the KfW bank group had to bail for 8.1 billion Euros, while Bear Steams in the USA had to announce two of its hedge funds as worthless. The customers of the British investment bank Northern Rock emptied their accounts in August 2007, until the British government declared to guarantee for the deposits.

In 2008, the crisis reached the real economy, and thus, the chemical industry. On January 21st, the DAX lost seven percent in only one day. Seven months later, also the biggest chemical enterprise BASF SE gave warning of hard times. Contemporaneously with the insolvency of Lehman Brothers, BASF cut back the plastics production to fight against the crisis. Likewise, Rhodia closed a polyamide plant in Italy as part of a huge cost reduction program. Besides Dow that proclaimed the recession in October 2008, several chemical companies in the US reduced their profit expectations.

The financial crisis turned into a world economic crisis. After the automotive sector was hit first, the automotive supplier industry was next. In December 2008, TMD Friction was the first German automotive supplier to apply for insolvency – the new car sales in Germany collapsed by 25%.

To cope with the crisis, the chemical industry sought to cut back labor costs through reduced production, as for example Bayer or Lanxess, or by means of staff reductions, e.g. Du Pont. In January 2009, Lyondell-Basell got into financial difficulties, whereas BASF sent 1800 employers into short-time work. In February, the association of the chemical industry in Germany (VCI) even referred to a catastrophe.

Just after the first glimpses of hope seemed to rise in July 2009 and – in accordance to Financial Times Germany (09.07.2009 and 22.07.2009) – reliance came back to the chemical industry, DSM already called the boom into question in August 2009. Süd-Chemie confirmed the negative perspective, too.

However, in September optimism became accepted on a broader base. For the year 2010, the VCI, as mentioned in the beginning, expected a production growth rate of 5% and a sales growth rate 6%, even if it has been assumed on a low base level.

The survey was conducted in the chemical industry by team steffenhagen during the summer of 2009, i.e. between the first boom tendencies and the relapse into negative perspectives. So the shock from the crisis was still enormous, but, dependent on the industry sector, the first glimpses of hope were observable.

3 The survey

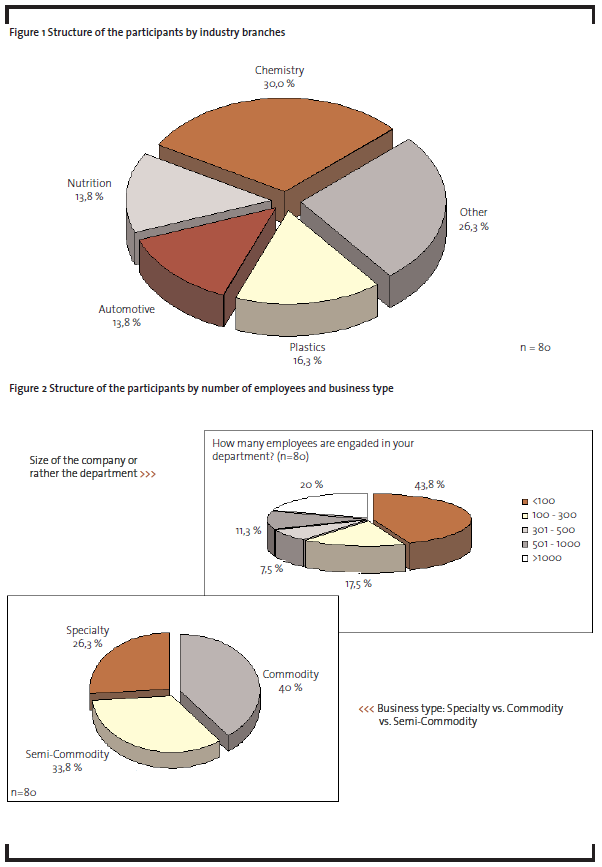

In 2005, team steffenhagen was able to uncover many weaknesses in the pricing management of companies, who participated in a first pricing survey focused on the chemical industry. In the current survey, again 80 pricing managers from different segments of the chemical industry gave response to our questions.

The participants of this survey mainly worked in the marketing and sales department, representing companies and departments of all sizes with different application areas of chemical products, such as petrochemistry, plastics, automotive, construction, or nutrition (c.f. Fig.1). Moreover, participating companies were located in different markets, including the specialty market, the commodity market, as well as the so called semi-commodities market (c.f. Fig.2).

It has to be noted that, although the survey indeed covers different segments of the chemical industry, it cannot raise the claim to be representative. It seems obvious that the evaluations presented in the survey show an image which is slightly distorted into a positive direction of the crisis and its consequences.

The following figure highlights the distribution of participating firms with regard to size and business types.

4 Pricing before the crisis

In their self-evaluation, the participants provide a clear picture in terms of their pricing behavior: About three quarters of them indicated to have implemented both transparent pricing processes and clearly defined pricing strategies.

It is precarious though that nearly 70% of the participating companies (and departments) still gear their pricing towards maximum EBIT. That implies that the majority of companies are still in danger of taking pricing decisions on the basis of overhead costs.

This apprehension is supported by the survey: For about 50% of the companies the overhead costs are crucial for price decisions to a high degree. This is an approach that verifiable leads to wrong decisions! Only for 12% of the companies the overhead costs play a merited minor role.

One can find a strong orientation towards sales volume or market share within 15% of the companies. As expected, the suppliers of semi commodities and commodities are overrepresented here.

Furthermore, it attracts attention in the analysis of the survey that the competition orientation comes off badly in terms of pricing. Only 36% of the interviewees claimed that before the crisis they used systematic methods for competition analyses.

Before the crisis, a strong orientation towards the competitors’ prices was crucial for barely a quarter of the interviewees. That would have been plausible for specialties, but it is precarious that even with commodities not more than a third of the involved companies are using systematic competition analyses. However, 45% of the commodity providers try to anticipate the reactions of competitors when setting their prices.

Moreover, a quarter of the interviewees revealed no competitor orientation regarding the pricing before the crisis.

In terms of customer orientation the situation was better before the crisis, although further optimization is essential. 60% of the interviewees had a good knowledge of the benefits of their products in the processes of their customers before the crisis. The least knowledge about the value in the processes of the customers could surprisingly be observed in the specialities market (48%).

Because of the weaknesses associated with competitor orientation, only 50% of the interviewees – according to their own statements – had a good knowledge of the customer value at their disposal compared to their competitors.

The orientation of the prices towards the provided customer value was found in 45% of the participating companies. However, only 17% were able to quantify the customer value before the crisis. Regarding the specialty providers, there were only 10% able to do so. Commodity providers revealed – as expected – the lowest orientation of the prices towards the customer value as well as the lowest efforts to quantify the customer value.

In the same way, there was already before the crisis the need to implement the customer value in price negotiations: Less than 50% were able to demonstrate the customer value in price negotiations before the crisis. Only for 38% the customer value was at the core of their price negotiations.

In terms of the price implementation, it is striking that around 60% of the companies were well prepared during the crisis regarding existing pricing competences and argumentation support for the sales people. But despite all that, the targeted price was achieved only by a third of the companies, and particularly specialty providers seem to have difficulties here.

Only 35% of the interviewees reported a proactive pricing before the crisis. Apparently, this is much easier for specialty providers, of which nearly the half realized a pro-active pricing already before the crisis.

Regarding price controlling more than 85% of the companies used systematic and established tools before the crisis. When asked about specific tools, interviewees named only rarely established tools like price scatter plots or profitability calculations. They mostly emphasized general analyses and tools, for example data bases and benchmarking.

So it is not very astonishing that only 40% of the interviewees claimed to be able to prepare better price decisions thanks to specialized tools before the crisis. Even the impact of pricing decisions on the own performance is perceived positively only by 56% of the companies.

A kind of oath of disclosure regarding the price consciousness was revealed in the end of the survey. The participants were asked for the biggest lever for the financial result and they could choose between the price, the variable costs, the fixed costs, and the sales volume. Surprisingly, only 35% were right and named the price.

Against the background of these mediocre results in terms of pricing quality, the following questions have to be asked: To what extent did the crisis negatively affect the companies? And, which companies were eminently hit and why?

5 The impacts of the crisis

5.1 Immediate impacts of the crisis

Certainly, the primary impact of the crisis was the customers’ reluctance to buy. Declining demands and quantities of sales are on the 1st place of our survey in the “charts” of the distinct changes contingent upon the crisis. More than a third spontaneously thought of this when they were asked for the clearest changes caused by the crisis. In terms of internal consequences, on the contrary, the focus on costs remains unchallenged on the first place (11%).

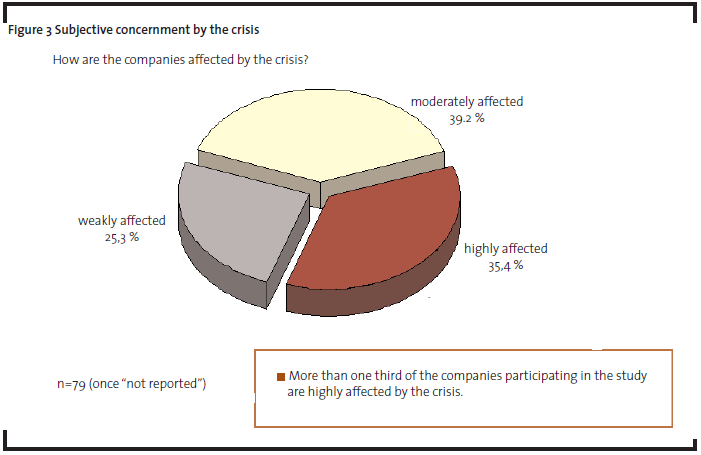

Both facts are not very remarkable. Elsewhere it was reported that sales collapsed by 50% (or in single cases even up to 80%) and that cost cutting programs were at the top of any firm’s agenda. Because of this development more than a third of the interviewees assessed themselves as being highly affected by the crisis. A quarter of the participants were on the contrary only weakly affected (cf. Fig.3).

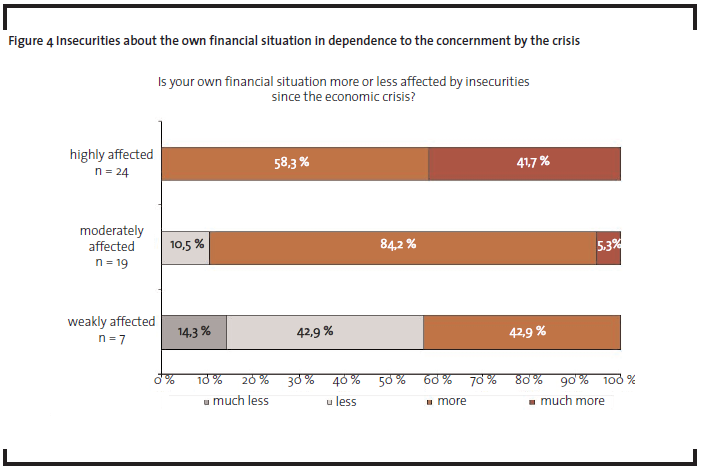

The companies that were according to their statements strongly affected by the crisis likewise felt strongly insecure regarding the own financial situation. About 42% of them noticed in this regard an increase in uncertainty since the beginning of the crisis. Contrasting this, more than 50% of the less crisis-affected companies felt substantially less insecure. The uncertainty has strongly increased since the beginning of the crisis, especially for commodity providers. (Annotation: the subjective concernment was measured as an approval to the statement “Our company is strongly affected by the current economic crisis” on a six-point rating scale. The answers were clustered into “weakly affected”, “moderately affected” and “highly affected”.)

An increased uncertainty in the judgement of the financial situation of the customers, which was detected by nearly all the participants, has to be added. Specialty providers, however, seem to assess the situation a bit better.

Another effect of the crisis can be led back to the considerably stronger fixation of the negotiation processes on the price, especially at commodities and semi-commodities. In this regard increasing efforts are undertaken to convince the customer of the added value of the own products.

The implementation of a successful pricing in and despite of the crisis is therefore achieved especially in companies which were only slightly affected by the crisis: While 75% of the weakly affected companies implemented a successful pricing, the ratio decreases for highly affected companies to a maximum of 50%. In regard to the type of business, it is remarkable that commodity providers reveal the most difficulties. However, 44% of them believe that they have a successful pricing in the crisis.

A vicious circle is initiated. Especially not well-prepared companies regarding the pricing will be affected by the crisis. The concernment is illustrated by greater uncertainty about the own situation and the situation of the customers. If this uncertainty is followed by a stronger price fixation resulting from incompetent acting on the market, the concern will increase even more. Accordingly, successful pricing will be impossible and, in turn, the sensitivity of firms against crisis-induced threats will increase. Against this background, an accurate overview of the factors, which increase the concernment and in the worst case denote first the step into this vicious circle, are worth it.

Therefore, the question arises which factors lead to a higher or high concernment.

5.2 Where and when is the concernment eminently high?

The diversification of the concernment into industry sectors was expectable. We could find high concernment especially in companies which supply the automotive sector as well as the plastic sector. Following the motto “people will always eat“ we find only a slight concernment in companies with customers affiliated to the nutrition industry.

Surprisingly clear was the difference between specialty and commodity or semi-commodity providers. Only 14% of the specialty providers are strongly concerned, while the share runs up to 38% for semi-commodity providers and up to even 48% for commodity providers. Especially a high market transparency and low differentiation ability seem to be the driving factors which make them vulnerable to the crisis.

Since less concerned companies can be found in the less price-driven sectors, we conclude that less price-driven industries denote a solid market even in the crisis.

Which countermeasures did the companies in the chemical industry employ to protect themselves from the effects of the crisis?

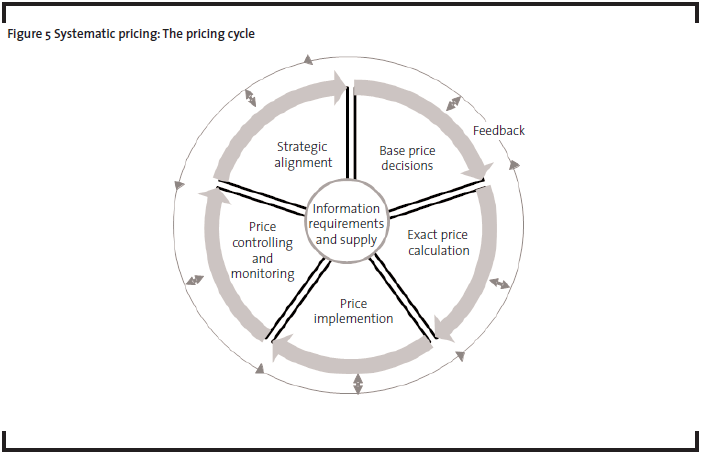

This question will be pursued in the following for the different phases of the pricing process (cf. Fig. 5).

6 Which countermeasures were employed?

6.1 Countermeasures related to costs and information procurement

The reduction of costs is one of the first crisis- induced reflexes. The following means to reduce the costs were used intensively:

- Stronger focus on production costs: 95% of the participating companies have urged their efforts to optimize the production costs since the beginning of the crisis. A third of the interviewees even reported strongly enforced measures.

- More pressure on the commodity prices: There is no exception here. The crisis induced all companies to increase the pressure on their suppliers to reduce commodity prices. Remarkable strong pressure was exerted by providers of commodities and semicommodities.

- More pressure on payment terms: More than 72% also employed shortened periods of payment, which increased the burdens on the suppliers even more. Especially commodity providers are not very willing to compromises.

Contrasting cost related saving effects, investments in information procurement are vital. The following investments were enforced since the beginning of the crisis:

- More market intelligence / market observation: All participating companies conduct more market observations since the beginning of the crisis to reduce existing uncertainties. There are also no companies which have not enhanced observations of the competitors.

- All interviewees are using more external information sources since the beginning of the crisis to be able to more reliably estimate the financial situation of their customers.

- More resources in marketing & sales: While a third of the companies are saving their money, two thirds invest more into marketing and sales than before the crisis.

We also detected a polarization of companies with regard to the investments in technical staff. While slightly more than half of the companies tend to reduce investments in technical staff, the “smaller half” tends to expand their investments.

6.2 Strategic countermeasures and measures of base price decisions

Due to the crisis, participating companies are now comparatively more oriented towards their competitors, they have enforced the structuring of their pricing processes and they conclude contracts with shorter durations:

- Increased competitor orientation: Since the beginning of the crisis more than 80% of the interviewees orientated their price decisions more towards their competitors.

- Enforced structuring of pricing processes: Three out of four companies have enforced the structure of their pricing processes since the beginning of the crisis. Every forth company even indicated a considerably higher structuring.

- Shorter contract duration (especially at commodities): Overall, more than 85% of the interviewees rely on shortened contract durations. With reference to commodity providers, now even 95% employ shorter contract durations.

Regarding the question, if companies have parted from unprofitable business segments in consequence of the crisis, we once again identified two groups.

6.3 Measures at pricing decisions

The following reactions were apparent regarding pricing decisions:

- In correspondence to the tendency of shorter contract durations, more than 80% implemented more short-dated price alignments since the beginning of the crisis. This tendency is very high for commodity providers and companies with a low pricing performance. (Annotation: The pricing performance was deduced as an indirect indicator out of different questions of the questionnaire.)

- More than 75% reacted on the crisis by means of more price reductions to keep up the sales volume. Even if this reaction is rarely employed by specialty providers, this reflex has to be scrutinized critically:

- On the one hand the outstanding importance of the price advises caution.

- Furthermore, the question arises, if the resulting price wars are grounded on a real demand in times of the crisis-induced decrease of needs. Does it make any sense to fight with reduced prices for a demand which does not exist anymore?

- Besides that, price reductions can be easily copied by competitors. While price wars are often initiated by price reductions, firms often employ this mechanism without a verification, if there is a realistic chance to win based on the own costs position, and with fatal consequences for the own profitability.

- On the other hand, nearly 25% of the queried companies are able to enforce higher prices since the beginning of the crisis; even 36% of the specialty providers are able to do so.

- More than 57% of the companies separate the pricing of service features to a lesser extent. On the contrary, other companies reacted by means of an enforced direct pricing of the services.

6.4 Measures of price implementation and price controlling

In order to meet the challenge of price enforcements successfully, 80% of the participating companies are using more and more trainings of their own sales employees.

Nearly a third of the companies do not use variable remuneration models that are in line with the price implementation to incentivize sales people. Within much more than a third of the companies, which work with performance-based remuneration models, the performance criteria have no direct connection with the outcome.

92% of the companies, which use more decision supporting tools, rely on a more intense price controlling. However, the question about the professionalism of these efforts remains unanswered.

With all used measures and reactions on the crisis the question about the efficiency arises. Which success factors can be derived for a pricing in the crisis?

7 Success factors for a pricing in the crisis

7.1 A high pricing performance is the best prevention for a crisis

Of course a high pricing performance, per definition, provides the best premises to control the most important outcome driver – the price. This is not very surprising.

The survey proves that a high pricing performance is indeed the best premise to survive a crisis like the world and economic crisis which started in 2007/2008. In conformity with the rule „Prevention is better than cure“, a high pricing performance protects from the effects of the crisis. The amount of companies that were only slightly affected by the crisis is as double as high for companies with a high pricing performance (29%) than for companies with a low pricing performance (14%). And you don’t even have to be counted to the best in pricing to prepare well for crisis times. Even companies with a medium pricing performance (26%) are only weakly affected.

A high pricing performance therefore leads to being less affected by the crisis. A low pricing performance before the crisis on the other hand appears to be enforcing the crisis related uncertainties, for example regarding the estimation of the own financial situation.

7.2 A high pricing performance allows for successful pricing even in the crisis

Companies with a lower pricing performance are not only hit stronger by the crisis, but they have also more difficulties in or despite the crisis to implement a successful pricing. Accordingly, only 40% of the companies with a low pricing performance are able to implement a successful pricing, while 55% of the companies with a medium or high pricing performance are able to do so.

Moreover, the companies that reveal a successful pricing even in the crisis are not hit by the crisis that strong. The negative impact of the crisis is further reduced by a successful pricing.

7.3 Pro-active and clearly structured pricing strategies are paying off

Our survey emphasizes how important proactivity is for pricing: With increasing pro-activity the effects of the crisis decline. Highly affected companies claim that their own price behavior is only for 25% distinctly pro-active. Therefore the weakly affected companies indicate a percentage of 45%.

A stronger structuring of the pricing processes during the crisis results in more relief. Only weakly affected companies have more structure in the pricing since the beginning of the crisis. On the contrary, highly affected companies are losing more than 42% of structure in their pricing processes.

7.4 Enforcement of the market related activities brings success in the crisis

Companies, which were hit only weakly by the crisis,

- are using, by trend, more information sources for the assessment of the financial situation of the customers since the beginning of the crisis,

- invest much more into marketing and sales resources,

- orient the prices more towards their competitors since the crisis started,

- are aware of the value of their own products in the competitive environment as well as in the processes of the customers and

- experience much less increase in the competitive pressure than strongly affected companies.

7.5 Price controlling and result-orientation.

Even in the crisis. Companies that were only weakly affected by the crisis, enforce the exit from non-profitable deals more than highly affected companies. Crisis-torn companies use more price reductions since the beginning of the crisis, to be able to keep up the sales.

So, it doesn’t surprise that among the strongly crisis-affected companies, we find a lot of companies with pricing strategies geared towards the maximization of the EBIT (82% versus 63% of less strong affected companies). The overemphasis of not decision relevant fixed costs leads apparently towards wrong decisions.

The companies however, who were well prepared for price decisions with systematic price controlling, until the crisis began, were hit less hard by the crisis: Only 35% of the strongly affected companies used such a systematic price controlling, while 53% of the less affected companies did so, too.

8 Lessons learned? What we should learn from the crisis

8.1 What you should do right now and therefore before the next crisis

The results of the survey give clear evidence on pricing-related needs for optimization that should be taken seriously.

The survey results suggest how to prepare yourself for the next crisis:

- Care for a high pricing performance already before the crisis! A high pricing performance will substantially reduce the effects of the next crisis.

- Structure your pricing processes! The stronger the structure of the pricing processes, the smaller the effects of a crisis on your processes.

- Align your pricing with the results and the really relevant costs! Consequently use a pricing that is orientated towards the marginal income and avoid grounding your pricing decisions on fixed costs, EBIT or market shares. This also offers you further protection on wrong decisions in the crisis (and, of course, already before the crisis).

- Care for a good knowledge of your own products in the processes of your customers and in the competitive environment! This also will result in less vulnerability in the crisis.

- Focus on pro-active pricing! Pro-active pricing also leads to less vulnerability in the crisis.

- Increase the competitor orientation of your pricing! More orientation on the competitors leads to less effects of the crisis on you as well.

- Focus on a systematic price monitoring and controlling for a better preparation of price decisions! Less problems result in crisis times.

- Finally, care quickly for a systematic professionalization of the pricing, because after the crisis is before the crisis. No instrument has a comparable direct and strong impact on the result than pricing!

8.2 What has to be done in the next crisis?

If the next tangible economic or sector crisis knocks on your door, you can derive the following suggestions from our survey:

- Use systematic information sources about the financial situation of your customers in the crisis! Fewer problems will affect you in the crisis.

- During the crisis, invest also or especially more into marketing and sales!

- Be cautious and conservative in terms of price reductions, also in the crisis! More crisis-induced price reductions lead to more impact of the crisis.

- Don’t let the pricing performance suffer! Companies, which are even in a crisis able to implement a successful pricing, won’t be hit so hard by the crisis.

9 Conclusion

It is undeniable that the economic and world crisis had and still has a dramatic impact on the companies in the chemical industry. Decline in sales, shutdowns of production sites, profit setbacks, job cuts and insolvencies didn’t spare the chemical industry.

The survey results suggest that the perceived effects were especially high for manufacturers of commodities and semi-commodities as well as for companies who supply the automotive industry.

But the situation is not hopeless at all: Especially a professional price management also in times of crises offers good possibilities to survive the crisis without unnecessary losses.

The survey shows that a high pricing performance indeed protects from fatal effects. The companies, who are able to stick to their pricing even in a crisis, are less affected by it.

A pro-active pricing, a professional price controlling and an enforced supply of the pricing process with information of customers, of their financial situation, and the value of the own products additionally act as a brake on the crisis- related risks.

The consistent optimization of the price management in all stages of the pricing process offers the best equipment for the purpose of prevention to protect yourself from the effects of the crisis, for the purpose of a better and result-oriented steering through the crisis and of course beyond the times of crises, because no other instrument has a comparable effect on the results than pricing.

Therefore implement as quickly as possible a consistent professional price management:

- Value-driven instead of cost-based pricing

- Focus on profits instead of volume or market share orientation

- Pro-active instead of reactive pricing

Unfortunately there are still too many companies – also in the chemical industry – who have not yet implemented these principles and the identified success factors of this survey consistently and consequently. This is also shown by the results of the survey.

The following figure summarizes the systematic pricing process in an overview. At the bottom you can find measures for the different stages of the pricing process.

Strategic alignment

- Strategic binding of the pricing

- Clarification of the business model

- Strategic objectives

- Price / Value positioning

- Behavior in cost / performance competition and in the product life cycle

Base price decisions

- Clarification: Value advantage in the competition (e.g. PSR2)

- Definition of pricing methods (e.g. Value Pricing, Competitive Pricing, Performance Pricing, price tactics)

- Price definitions

- Pricing guidelines

- Pricing rules

Exact price calculation

- Definition of the price range and price boundaries

- Unit price decisions and transaction prices

- Incoterms

- Price contracts

Price implementation

- Price argumentation and price negotiations

- Pricing and negotiation trainings (incl. MBTI®)

- Roles & Responsibilities

- Pricing processes

- Incentive systems

Price controlling & monitoring

- Price reporting

- Tools for price controlling

- Pricing Toolbox Price -, quantities-, and CM-monitoring

- CM-simulator

- Price Scatter Plots (price clouds)

- Customer Box Plots

- Cost Development Calculator

- Waterfall Analyses

- Customer result calculation

- Knowledge Toolbox