Reducing the emissions Scope 1-3 in the chemical industry

1 Introduction

Since the European Emissions Trading Scheme (ETS) was installed in 2005, the operators of more than 11,000 emissions-intensive plants, including many in the chemical industry, have had to buy so-called emissions allowances for the release of their emissions. A central control instrument of the trading system is that the number of allowances is continuously reduced, i.e. the overall volume of emissions is capped. While the number of allowances was reduced by 1.7% per year in the 3rd trading period from 2013-2020, the reduction rate will accelerate to 2.2% in the 4th trading period from 2021. At the same time, the number of industries that will receive mitigating special rules to avoid the migration of these emission sources from the EU (carbon leakage regulations) will be reduced. From 2021, the manufacture of plant protection products, personal care products and pharmaceutical specialties, to name but a few, will no longer be specifically spared (EC, 2020; VCI, 2020).

Allowances are freely tradable; their market price has increased by a factor of six since the start of the ETS to EUR 32 per metric ton of carbon dioxide equivalent today, and a further increase is expected. Model calculations for the German chemical industry up to the year 2050 were based on an assumed price for allowances of EUR 100 per ton of carbon dioxide in 2050 (Dechema and FutureCamp, 2019). The ETS has already burdened the German chemical industry with EUR 1.34 billion annually in the 3rd trading period alone.

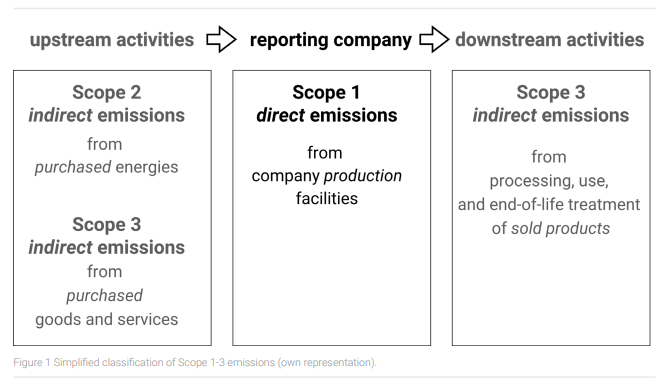

In terms of emissions reduction, the trading system has been and continues to be quite successful. Since 1990, emissions from the European chemical industry covered by the ETS have fallen by 58% to 135 million metric tons of CO2-equ. These are in particular the emissions arising from energy production (CEFIC, 2020). The sectors covered not only achieved the reduction target set for 2020, but actually fell short of it. The energy sector in particular contributed to this. The pressure on the other sectors involved to reduce emissions, including the chemical industry, will therefore tend to increase further, especially as climate change is accelerating despite global climate protection measures. Global warming of 1.5°C can no longer be ruled out as early as 2024, and there are therefore voices that believe a radical reduction in greenhouse gas emissions worldwide is necessary by 2030 (IPCC, 2018). In the near future, therefore, it cannot be ruled out that the political framework for reducing emissions will be tightened more drastically than previously planned. Industry would therefore be well advised to consider prophylactic options for action. So where could further measures be taken within the framework of the emissions trading system, which is in itself a successful concept? To address this question, the different emission sources and how the ETS treats them need to be considered (Fig. 1). A distinction is made between emissions generated by a company itself from its own facilities (Scope 1), emissions attributable to purchased energy (Scope 2) and emissions originating from purchased raw materials and the use or disposal of sold products (these are the largest sources of emissions; in fact, emissions are recorded in much greater detail).

2 Scope 1 and 2 emissions

First, the existing strategy of capping energy-related Scope 1 and 2 emissions and making the corresponding allowances more expensive could be further intensified. This would increase the already existing pressure to reduce energy-related emission sources. In principle, there are three options for doing this, namely 1. using emission-free energy, 2. switching to emission-free processes, and 3. capturing CO2 from emission gases:

- Many companies are focusing on the use of emission-free energies. For example, companies such as Bayer and Henkel have published plans to reduce their carbon footprint, particularly with the help of renewable energies (Bayer, 2019; Henkel, 2021). Special attention is paid to the largest source of emissions in the chemical industry, namely steam cracking, which accounts for 26%. The use of renewable energies could significantly reduce this emission source (Amghizar, et al., 2020).

- It is not only the switch to emission-free energies that increases the climate compatibility of chemistry. The use of processes that replace fossil carbon sources with electricity can also reduce emissions. One example is the production of ammonia, which, with the processing of natural gas, now accounts for 39% of chemical emissions (2017) (CEFIC, 2020). The alternative process of solid state ammonia synthesis (SSAS), on the other hand, combines the electrolytic production of hydrogen and the Haber-Bosch synthesis into an integrated emission-free process (Holbrook and Leighty, 2009). However, processes that consume electricity and hydrogen are extremely energy-intensive. They will greatly increase the demand for emission-free energy from the chemical industry. Their introduction therefore depends on the provision of the corresponding capacities by the energy sector. Today, the European chemical industry consumes for energy purposes around 52.7 million tonnes of oil equivalent (toe) in total, of which 13% is renewable energy and biofuels (2017) (CEFIC, 2020).

- Alternatively, carbon capture and storage (CCS) offers an option for avoiding the emission of greenhouse gases into the atmosphere. In Europe, however, this process has so far only been used in Norway for the extraction of natural gas and has met with a lack of social acceptance in many countries (Cuéllar-Franca and Azapagic, 2015).

3 Scope 3 emissions

As part of the tightening of the EU emissions trading system, Scope 3 emissions, which have not yet been taken into account, could also be included. Although Scope 3 emissions are reported as part of the CSR (corporate social responsibility) reports, they are not subject to the emissions trading system.

Scope 3 includes all emissions attributable to purchased materials and services as well as to the further processing, use and disposal of sold products. Scope 3 categories 1 and 12 account for the most significant share of these emissions. Category 1 includes emissions from the purchase of chemical raw materials, packaging materials, and indirect goods. Among the raw materials of the chemical industry, fossil carbon sources account for 90% (petroleum 74%, natural gas 15%, coal 1%, biogenic 10%; EU, 2015) (CEFIC, 2016). This emission potential purchased from the supply chain is often referred to as the carbon backpack. Category 12, on the other hand, contains the emissions released during the disposal and recycling of products. In other words, this emission potential corresponds to the volume of carbon dioxide that can be released from organic chemical products during incineration. An order of magnitude can be estimated from the volume of fossil raw materials used as a carbon source of 74,717 million toe (EU, 2013) (Boulamanti and Moya, 2017). Assuming an average carbon content of 80% and accumulated process losses of 30%, the resulting products would have a potential for carbon dioxide emissions of around 150 million tons, i.e. in the order of magnitude of the Scope 1 and 2 emissions mentioned above. This corresponds to the ratio of Scope 1, 2 and 3 emissions to each other reported for the German chemical industry (Dechema and FutureCamp, 2019).

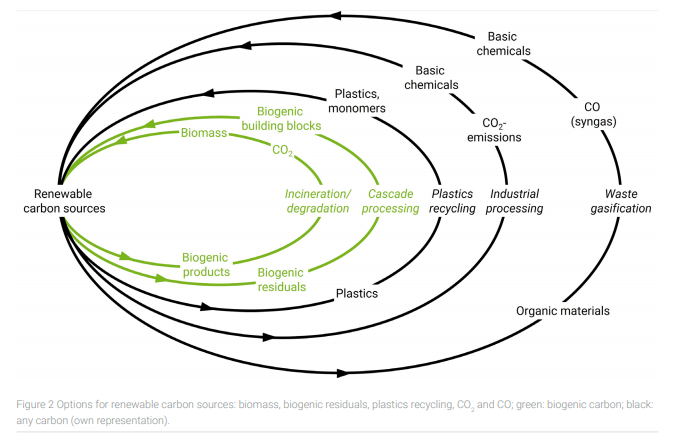

Basically, there are five options to reduce this emission potential by recycling and using non-fossil carbon sources (Fig. 2):

- Biomass: Biomass from agricultural and forestry products as well as from marine sources is considered an emission-neutral carbon source because the carbon bound in the biomass has been removed from the atmosphere in the course of the natural carbon cycle. The source of energy is the sun. Accordingly, bio-based products are basically considered to be climate neutral. Today, 10% of the carbon sources for the chemical industry are based on biomass. Examples of industrial practice are bio-based acrylic acid (Bio-based News, 2012) and polyurethan elastomers (European Plastic Product Manufacturer, 2020). However, limitations to the large-scale use of primary biomass must not go unmentioned. The production of biomass for industrial applications competes with land use for food, which is given priority in the general consensus of society. In addition, agricultural production of biomass also generates greenhouse gases. Its share of total European emissions is 10% (2015) (EC, 2017) and could be increased by intensifying agriculture for industrial purposes. An increased use of agriculture as a raw material supplier for the chemical industry is also limited by already partly damaged planetary boundaries (PIK, 2019).

- Recycling of residual and waste materials: Agricultural and forestry waste (straw, residual wood), as well as residual and waste materials in densely populated and industrialized metropolitan areas (industrial residues, food waste, green waste, sewage sludge) have raw material potential for industrial processes in the context of cascade utilization. Straw for example is already used for the production of bio-ethanol (Clariant, 2020). Because the above-mentioned raw materials occur seasonally and with varying composition, they need to be standardized into a raw material that meets specifications. Biogas can play a key role in this field, because a large proportion of the waste and residual materials mentioned can be fermented anaerobically to form biogas and thus supply (bio)methane as a chemical raw material. Biogas fermentation of waste is state of the art. The microorganisms of the biogas fermentation obtain the energy required for the conversion from the raw materials.

- Plastic recycling: In Europe, 39% of plastic waste is incinerated, 31% landfilled and only 30% recycled (EU-Parliament, 2018). The European Commission asks for creating the capacity to recycle 55% of packaging plastics in the EU by 2030 (EC, 2018).

- Carbon dioxide: Carbon dioxide from industrial point sources of both fossil-based and bio-based processes (combustion, fermentation) can be used as a carbon source. Algae can photosynthetically metabolize carbon dioxide, but are costly to cultivate. Bacteria can produce more easily in steel boilers, but require hydrogen to reduce carbon dioxide. A corresponding process for butanol and hexanol will reach the pilot phase in 2021 (Evonik, 2020). Chemo-catalytic processes are already established. For example, Covestro produces polyols starting from carbon dioxide (Covestro, 2020). In the long term, carbon dioxide is even seen as having the potential to establish itself as a dominant raw material (Dechema and FutureCamp, 2019; nova-institute, 2020). A prerequisite is the development of sufficient emission-free energy capacities for the provision of hydrogen.

- Carbon monoxide: Organic residues and waste materials can be gasified to synthesis gas, which contains carbon monoxide as a carbon source. Both chemical-catalytic (Fischer-Tropsch) and biotechnological processes can use carbon monoxide as a raw material for the production of chemical products. One example is the biotechnological production of ethanol or ethylene from metallurgical gases (Lanzatech, 2020).

The raw materials and product examples mentioned show that the recycling of carbon in various forms is already practice and has further industrial potential. It should be taken into account that the raw material spectrum will change as the raw material shift from fossil to renewable carbon sources continues. The share of biomass and biogenic residues and waste will increase and that of fossil raw materials will decrease. As individual industries begin to switch to hydrogen and electricity, as can be seen in steel production (ArcelorMittal, 2020), the supply of metallurgical gases as a carbon source will also tend to decrease.

This is a process of change that will take decades. Nevertheless, industry and policymakers must prepare for this today because the development of the relevant processes, the adaptation of industrial plants and the infrastructure also takes time, investments, and requires the coordination of numerous players.

For the use of biomass, agriculture and forestry must be integrated into industrial value chains. The same applies to the use of agricultural residues, for which, because they do not compete with food, social acceptance can be more readily expected. In the recycling of plastics, waste management will become more important for closing this material cycle, and because this sector is often closely linked to public administration, so will it. The same applies to the gasification of waste into synthesis gas; here, too, the infrastructure of waste management is a fundamental prerequisite. The use of syngas and CO2 from industrial emission streams will require integration with the energy sector because of the high demand for reduction equivalents or energies.

The transition to the new economic structure thus created is in itself a major challenge. In addition, demand expectations are placed on individual sectors that will foreseeably reach their limits, particularly with regard to the provision of carbon sources and energies. Biomass and the residual and waste materials derived from it, which ultimately come from agriculture and forestry, are considered an important source of sustainable carbon. Their land areas cannot be expanded at will and are already so ecologically burdened today that conservation rather than even more intensive use would be recommended. The chemical industry should therefore not depend exclusively on biogenic carbon sources. Relief is offered by the use of CO2 and CO, which, however, also has its limits due to the high energy requirements for the production of the necessary reduction equivalents. Because plastics account for a large share of chemical production and thus also of Scope 3 emissions, there are justified calls to intensify plastics recycling. In fact, a roadmap for sustainable chemistry in Germany proposes to develop and implement all the options mentioned. According to this study, in order to achieve climate neutrality, CO2 will become the most important carbon source in the chemical industry in Germany by 2050, alongside biomass and plastics recycling.

Admittedly, this goes hand in hand with an additional electricity demand almost equal to Germany‘s full consumption today (Dechema and Futurecamp, 2019).

4 What needs to be done to support this path towards a truly climate-neutral chemical industry that also reduces Scope 3-related emissions?

In my view, two measures are urgent here:

Firstly, Scope 3 emissions must be included in the ETS and burden either the producing or the disposing industry. Only then will the framework provide an incentive to reduce CO2 emissions from product-bound carbon and switch to renewable carbon sources. However, this tightening of the ETS will only have the desired effect if at the same time emission streams that are recycled are released from the ETS. Today, emissions subject to the ETS incur costs regardless of whether they are recycled or released into the atmosphere.

Secondly, the technical recycling of CO2 can only be scaled up if the necessary energies are available in sufficient quantities and without emissions. In Europe‘s most important chemical regions, such as North Rhine-Westphalia in Germany, Flanders in Belgium or the southern Netherlands, large capacities of bioenergy, solar and wind power are being built up. It is doubtful whether these regional and nationwide capacities are sufficient to cover the growing demand for electricity, not only for industry but also for mobility and heating. The European framework conditions should therefore encourage to build an Europe-wide infrastructure for renewable energies, linking the large energy consumers in the north – the example of the ARRR chemical region (Antwerp, Rotterdam, Rhine-Ruhr) has been mentioned only as an example – with locations for solar and wind energy in the sunny south of Europe that are to be developed. The electricity could also be distributed via the existing natural gas grid in the form of hydrogen, which is actually needed by the chemical industry for CO2 recycling. Further potential is offered by geothermal energy in Iceland, which is far from being fully exploited, and hydroelectric power in Scandinavia. Some countries, such as France and the Netherlands, are also keeping respectively reviving nuclear energy. Such regions could replace the currently dominant non-European suppliers of fossil energy sources and thus share in the value creation of the chemical sector. In fact, the implementation of this strategy has already begun; however, not in the EU, but further south, where large hydrogen capacities based on solar and wind energy are being built in Saudi Arabia (NEOM, 2020) and Morocco (DII, 2020) for export.

In summary, I believe that renewable carbon sources from biomass, plastics and CO2 recycling are technically feasible today and should be implemented vigorously. Inhibiting factors are i) insufficient and too expensive capacities for emission-free energies and ii) in Europe, the framework conditions, especially the ETS. The fact that distortions of competition with non-European markets must be avoided in the further development of the framework conditions adds further complexity. Nevertheless, in the interest of urgent climate protection, long-term prosperity and competitiveness based on sustainability, business and politics must face up to the task of removing the technical, economic and political obstacles and unleashing driving forces sooner rather than later. Time and climate change are pressing.

References

Amghizar, I., Dedeyne, J.N., Brown, D.J., Marin, G.B., Van Geem, K.M. (2020): Sustainable innovations in steam cracking: CO2 neutral olefin production, React. Chem. Eng., 5, pp. 239-257.

ArcelorMittal (2020): ArcelorMittal Europe to produce ’green steel’ starting in 2020: Hydrogen technologies at the heart of drive to lead the decarbo-nisation of the steel industry and deliver carbon-neutral steel, available at https://www.globenewswire.com/news-release/2020/10/13/2107279/0/en/ArcelorMittal-Europe-to-produce-green-steel-starting-in-2020-Hydrogen-technologies-at-the-heart-of-drive-to-lead-the-decarbonisation-of-the-steel-industry-and-deliver-carbon-neutra.html, accessed 22 January 2021.

Bayer (2019): Bayer to significantly step-up its sustainability efforts, available at https://media.bayer.com/baynews/baynews.nsf/id/Bayer-to-significantly-step-up-its-sustainability-efforts, accessed 22 January 2021.

Bio-based News (2012): Plexiglas® Rnew Bio-based Acrylic Resins from Arkema Surpass Performance of Traditional PMMA Products. available at https://news.bio-based.eu/plexiglas-rnew-bio-based-acrylic-resins-from-arkema-surpass-performance-of-traditional-pmma-products/, accessed 22 January 2021.

Boulamanti, A., Moya, J.A. (2017): Energy efficiency and GHG emissions: Prospective scenarios for the Chemical and Petrochemical Industry, JRC Science for Policy Report, p.7, available at https://publications.jrc.ec.europa.eu/repository/bitstream/JRC105767/kj-na-28471-enn.pdf, accessed 22 January 2021.

CEFIC (2016): Bioeconomy available at https://cefic.org/policy-matters/bioeconomy/, accessed 22 January 2021.

CEFIC (2020): 2020 FACTS & FIGURES of the European chemical industry, available at https://cefic.org/app/uploads/2019/01/The-European-Chemical-Industry-Facts-And-Figures-2020.pdf, accessed 22 January 2021.

Clariant (2020): CELLULOSIC ETHANOL FROM AGRICULTURAL RESIDUES – THINK AHEAD, THINK SUNLIQUID, available at https://www.clariant.com/en/Business-Units/New-Businesses/Biotech-and-Biobased-Chemicals/Sunliquid, accessed 22 January 2021.

Covestro (2020): Driving with CO2, available at https://www.covestro.com/press/driving-with-co2, accessed 22 January 2021.

Cuéllar-Franca R.M., Azapagic A., (2015): Carbon capture, storage and utilisation technologies: A critical analysis and comparison of their life cycle environmental impacts, Journal of CO2 Utilization, 9, pp. 82-102.

DII (2020): Dii Desert Energy, available at https://dii-desertenergy.org, accessed 15 January 2021.

Dechema and Future Camp (2019): Roadmap Chemie 2050, available at https://dechema.de/chemie2050.html, accessed 15 January 2021.

EC (2017): Agri-environmental indicator – greenhouse gas emissions, available at https://ec.europa.eu/eurostat/statistics-explained/pdfscache/16817.pdf, accessed 22 January 2021.

EC (2018): Factsheets on the European strategy for plastics in a circular economy, available at https://ec.europa.eu/commission/publications/factsheets-european-strategy-plastics-circular-economy_en, accessed 22 January 2021.

EC (2020): EU Emissions Trading System (EU ETS), available at https://ec.europa.eu/clima/policies/ets_en, accessed 9 December 2020.

European Plastic Product Manufacturer (2020): LANXESS launches bio-based prepolymer line Adiprene Green, available at https://www.eppm.com/materials/lanxess-launches-bio-based-prepolymer-line-adiprene-green/, accessed 22 January 2021.

EU-Parliament (2018): Plastic waste and recycling in the EU: facts and figures, available at https://www.europarl.europa.eu/news/en/headlines/society/20181212STO21610/plastic-waste-and-recycling-in-the-eu-facts-and-figures, accessed 22 January 2021.

Evonik (2020): TECHNICAL PHOTOSYNTHESIS, available at https://corporate.evonik.com/en/technical-photosynthesis-25100.html, accessed 22 January 2021.

Holbrook, J.H., Leighty W.C. (2009): Renewable fuels: Manufacturing ammonia from hydropower, available at

https://www.renewableenergyworld.com/storage/renewable-fuels-manufacturing/, accessed 22 January 2021.

Henkel (2021): Climate Protection Strategy and Targets, available at https://www.henkel.com/sustainability/positions/climate-positive, accessed 22 January 2021.

IPCC (2018): Global Warming of 1.5 ºC., available at https://www.ipcc.ch/sr15/, accessed 22 January 2021.

Burton, F. (2020): LanzaTech, Total and L’Oréal Announce a Worldwide Premiere: The Production of the First Cosmetic Packaging Made From Industrial Carbon Emissions, available at https://www.lanzatech.com/2020/10/27/lanzatech-total-and-loreal-announce-a-worldwide-premiere-the-production-of-the-first-cosmetic-packaging-made-from-industrial-carbon-emissions/, accessed 22 January 2021.

NEOM (2020): The future of energy, available at https://www.neom.com/en-us/sector/energy/, accessed 15 January 2021.

nova-institute (2020): THE RENEWABLE CARBON INITIATIVE, available at https://renewable-carbon-initiative.com, accessed 22 January 2021.

PIK (2019): Planetary boundaries: Interactions in the Earth system amplify human impacts, available at https://www.pik-potsdam.de/en/news/latest-news/planetary-boundaries-interactions-in-the-earth-system-amplify-human-impacts, accessed 22 January 2021.

VCI (2020): Emissionshandel: Umsetzung, available at https://www.vci.de/vci/downloads-vci/top-thema/daten-fakten-emissionshandel.pdf, accessed 22 January 2021.