Supply Value Management – A benchmarking study and a new theoretical approach show that procurement in the chemical, pharmaceutical and healthcare industry has only average performance

This article introduces three fundamental frameworks for procurement. Each of them targets different aspects of procurement. All three frameworks have been developed and tested in the III. Global Procurement and SCM Study which is part of the biggest global procurement study series conducted. The insights of this study and the relevant findings for the chemical, pharmaceutical and healthcare industry are discussed. The article will thus answer the question why the procurement performance of this industry is only average.

1 Introduction

The academic consideration of procurement is sometimes very simplistic. In many cases, procurement is neglected as an important value creation lever for the company or the definition and consideration is just not sufficient. This is illustrated by the fact that main definitions in academia limit procurement to a process focused department for sourcing goods in the right quality to the right place at the right time at minimum costs. Even in Porter’s value chain analysis concept (Porter, 1985), procurement is seen as a supporting activity which underlines the lack of importance for procurement in this framework. Procurement is by far more important than these definitions indicate and has for decades not been the main department for aspiring young professionals. This picture has changed recently and procurement is now more and more attracting young professionals. As procurement departments develop from an internal service provider to value champions, their need for qualified employees is increasing. A need that is difficult to satisfy.

This transition of procurement and the somehow insufficient academic consideration have been the reason to analyze procurement in a detailed empirical and scientific way. Therefore, three procurement studies have been carried out to give answers on questions that have been left unanswered up to now.

Based on this biggest procurement study series, new procurement frameworks have been developed which help professionals of all industries to find their way to more value creation in procurement. These frameworks are called Supply Value Management (SVM), Supply Infrastructure Management (SIM) and the Supply Value Maturity Model (SVMM). These are interlinked and will be further introduced in this article. While Supply Value Management describes how procurement can create value for a company, Supply Infrastructure Management places the spotlight on what a company needs to achieve this value creation. Finally, the Supply Value Maturity Model assesses whether a company’s procurement is rather seen as a basic internal service provider, a more mature value champion or something in between.

With the last study, the III. Global Procurement and SCM Study conducted in 2013, these frameworks could be empirically proved. The specific situation of the chemical, pharmaceutical and healthcare industry are analyzed using these frameworks to answer the question where the most important value creation potentials of this industry lie. In addition, the major differences of good and bad performing companies can be identified.

Based on the Supply Value Management, the chemical, pharmaceutical and healthcare industry shows a significant performance gap for all nine value creation levers of procurement. A specific value creation lever in this industry that is typically lower for other industries is risk (management).

The performance for all seven different aspects of the Supply Infrastructure Management is also significantly lower compared to other benchmark industries. The main performance gap for supply infrastructure, shown by the analysis for the industry, is the standing of procurement. This indicates that the main current problem for procurement departments in the focus industry is a low standing of procurement towards senior executives of other functions.

According to the Supply Value Maturity Model, the requested performance of procurement in the chemical, pharmaceutical and healthcare industry is quite high and mature. However, procurement is not able to deliver the desired value creation. This is mainly referring to the low standing procurement processes and the missing contribution to value creation by a good risk management and innovation management (with suppliers).

As these results indicate, the potential value creation levers of procurement go far beyond current typical definitions of procurement which see it as a function of acquiring the requested goods at the right cost with right quality to a determined point of time.

Before introducing the results concerning the three frameworks in more detail, the study design of the III. Global Procurement and SCM Study is displayed.

2 Study design

The III. Global Procurement and SCM Study was a follow up to the two biggest procurement studies ever conducted in 2009 and 2011 with about 1,800 participants from 82 countries. It was conducted by the Kellogg School of Management (one of the Top 5 Business Schools of the world), the American Purchasing Society, the International Chamber of Commerce and the Valueneer GmbH.

Based on a questionnaire with 47 questions, important topics of procurement were analyzed. The questions were clustered to the following procurement related topics:

- Trends

- Strategy

- Organization, Controlling and Processes

- Ethics and Chief Procurement Officer (CPO)

- Risk Management.

Exemplary questions that were asked in the previous studies as well as in this study are:

- Do you have a communicated procurement strategy in your company?

- Do you have a specific controlling of procurement activities in your company?

- Are procurement activities in your company standardized and documented?

New questions focusing on trends and risk management were included in the III. Global Procurement and SCM Study. To put an additional emphasis on sustainability and ethics, questions such as

- Which instruments do you use to create a sustainable procurement?

- Do you feel pressured at your company to behave in an unethical way to better achieve targets and goals?

were added.

For this study, more than 5,000 top executives of renowned international companies were contacted. In total, the III. Global Procurement and SCM Study can refer to participants from 555 companies from 66 countries around the globe. The entire study series had participants from 94 countries. Companies from the chemical, pharmaceutical and healthcare industry are representing 9% of the participants in the last study. The study participants originate from all continents. North America, Asia and Europe are represented to a similar extent. Also companies from Africa and South America participated and account together for around 16% of the sample. The study examines all different business sectors and company sizes.

The study covers all relevant decision levels, i.e. senior managers and procurement experts. Therefore, important operational and strategic questions can be analyzed from a complementary point of view. The data was gathered from July 2013 till December 2013.

Against the background of the III. Global Procurement and SCM Study, the insights on the three procurement frameworks will be described in the following for all industries in general. Additionally, the industry analysis for the chemical, pharmaceutical and healthcare industry will be shown in particular.

3 Supply Value Management (SVM)

General definitions of procurement limit its importance typically to a supply chain perspective. In this context, procurement is often defined as the acquisition of goods and services at the best possible total cost of ownership to meet the needs of the purchaser in terms of quality and quantity, time and location (van Weele, 2010). From our perspective, these definition are not complete as they neglect important value creation levers of procurement. The operational perspective of procurement is essential, but it shows just a part of the full value creation potential of procurement. A definition of procurement should take a more strategic perspective into account. How can procurement support the strategy of the company?

According to Porter (1996), (1) strategy is a logical concept to achieve a higher financial performance (e.g. ROCE) compared to competitors by (2) a unique value proposition, (3) a different tailored value chain, (4) activities that fit together and reinforce each other, (5) involving clear trade-offs and thus enabling (6) sustainable advantage. If procurement should support the overall business strategy, similar aspects have to be involved when defining the procurement strategy. Taking into consideration Porter’s definition of strategy, the following attributes could be derived easily for a company’s procurement strategy:

- Logically connected to the goal of long-term superior financial performance

- Maximizing value creation from supply and suppliers

- Fitting the company’s positioning and strategy

- Adapting to other parts of the entire value chain

- Defining clear trade-offs within potential procurement goals

- Striving for sustainability with continual improvement

If the goal of any strategy is to achieve a higher financial performance, one starting question for any procurement strategy should be, how procurement can influence financial performance.

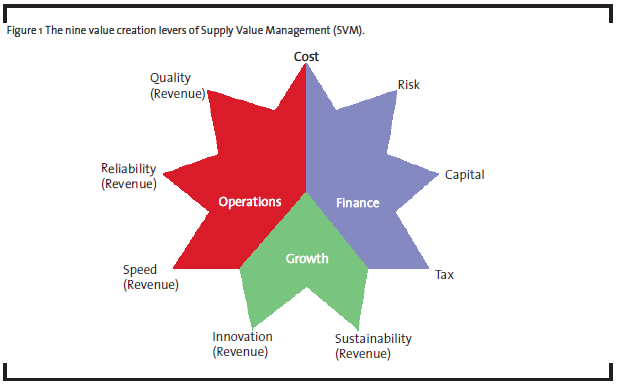

Generally speaking, procurement can influence a company’s financial performance by five key KPIs: margin, revenue, risk, capital and taxation. So, procurement can help a company in order to achieve a better financial performance by better managing Total Cost of Ownership (TCO) leading to higher margins, by increasing revenues through procurement, by reducing supply risks, by fewer required (working) capital and lower taxation.

These five key levers define the complete set of aspects how procurement can influence the financial performance:

Margin: The way in which procurement is directly influencing a company’s margin is by its various costs such as material costs, service costs, process costs and personal costs. Because procurement typically spends the largest cost block, procurement has a huge lever on a company’s total cost. Margin will therefore be called ‘cost’ in the Supply Value Management framework illustrated in Figure 1. Due to its high importance as a value creation lever, it is allocated to the operational as well as to the financial perspective of the SVM.

Revenue: The most important functions of a company influencing revenues are typically not procurement but sales, marketing or R&D. But procurement’s effect on revenue should not be neglected. Additionally, for a procurement person it is very hard to estimate how and to which extent he or she can influence a company’s revenue. Therefore, ‘revenue’ has to be represented by a set of levers which influence revenue and are easier to understand, observe and influence from a procurement perspective.

The first perspective on revenue is an operational one. The quality of the supplied goods definitely has an influence on the revenue. Additionally, procurement has an influence on whether important materials are available or not. Suppliers who can react fast and flexible are helpful for boosting sales when clients or business situations require short term adaptations to changes. Thus, ‘quality’, ‘reliability’ and ‘speed’ form the operational perspective on revenue in the SVM framework.

There is a second growth perspective which is also related to revenue and originating from differentiation. This perspective is associated with sourcing more innovative or sustainable products. While there is a positive effect of more sustainable products, there might as well be a negative effect if not considered, e.g. by negative press because a company is sourcing from a supplier that uses child labor. ‘Innovation’ and ‘sustainability’ represent the growth perspective in the SVM framework.

As revenue can be broken down to a growth and an operational perspective, the influences are represented by quality, reliability, speed, innovation and sustainability in the SVM framework.

There is a third perspective in the SVM called the financial perspective. It is represented by ‘risk’, ‘capital’ and ‘tax’ in the framework. As these are common terms from a financial perspective and easy to understand, a substitution with other more observable terms from a procurement perspective is unnecessary.

Risk: Procurement can influence a company`s risks to a large extent. The volatility of material costs or exchange rates are examples for that. Additionally, it can be affected by the risk of suppliers going bankrupt or by the risk to be hugely affected from natural disasters or political unrest.

Capital: Procurement has mainly two ways to influence the capital needed: Accounts payable and stocks. Both are part of the working capital and influence a company`s liquidity. Moreover, procurement influences important make or buy or buy or lease decisions which have an effect on the need for capital.

Tax: Procurement can also influence a company’s taxation e.g. by using procurement offices in countries with lower taxation. Besides a potential negative press on doing or not doing so, this is influencing the financial performance of a company.

From these five key levers of procurement on the financial performance of a company, nine important value creation levers can be derived. These value creation levers are:

- Cost – Key lever: Margin

- Risk – Key lever: Risk

- Capital – Key lever: Capital

- Tax – Key lever: Tax

- Sustainability – Key lever: Revenue

- Innovation – Key lever: Revenue

- Speed – Key lever: Revenue

- Reliability – Key lever: Revenue

- Quality – Key lever: Revenue.

These nine value creation levers together form the SVM illustrated in Figure 1. This model has been developed and tested on the background of the procurement study series. The Supply Value Management is a framework to handle trade-offs and align the procurement strategy to the overall business strategy. Based on the SVM, a company can set up the main value creation levers for procurement, derive KPIs and e.g. decide which suppliers to choose. There might be a situation where suppliers have the same or similar cost for a good or service that is about to be bought. Additionally, qualitative aspects are also equal. However, the suppliers perform different on speed and reliability. As the importance for these two aspects has been defined in the SVM, the decision can be made more easily as either speed or reliability has been given a higher importance for sourcing decisions.

The framework is considering by far more aspects of procurement than typical supply chain and operation focused definitions of procurement. The operational perspective is of course an important one and therefore also considered in the framework, but there are additionally the financial and growth perspective that need to be taken into account.

3.1 Supply Value Management in the chemical, pharmaceutical and healthcare industry

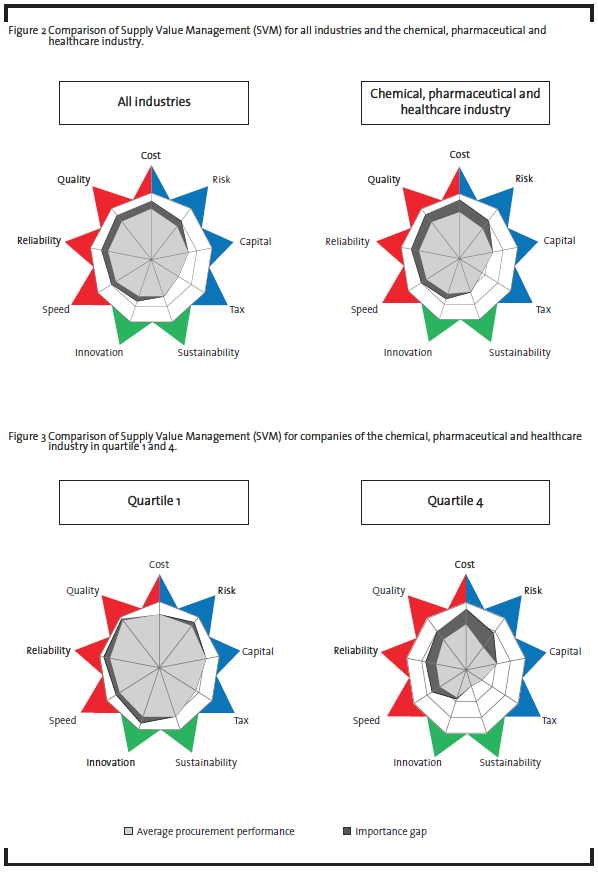

Based on the results of the III. Global Procurement and SCM Study, the performance regarding the nine value creation levers of all industries can be compared with the performance of the chemical, pharmaceutical and healthcare industry. Performances for all industries are illustrated in Figure 2. Shown in light grey is the average performance of the cross-industry benchmark for all participants in the study regarding the ability to create the specific value within procurement. The dark grey area shows the gap between the current performance and the aspiration target of each of the nine value creation levers. If the dark grey area is large, there is a significant difference between aspired and achieved performance for a value creation target.

By looking at the Supply Value Management for all industries, the highest gaps are shown in the areas of cost, quality and reliability. Although these topics might be seen as the ‘old perspective on procurement’, the average of all companies is still struggling in achieving the aspired value creation targets. In addition to the mentioned levers, there is also a relevant average gap for risk, speed and innovation. Regarding capital, tax and sustainability, the average of the participants state that they do not have a huge gap between performance and importance for these levers.

Taking a look at the analysis for the chemical, pharmaceutical and healthcare industry shows that the importance gap regarding most of the value creation levers is higher than compared to the crossindustry analysis. This means that in comparison to the industry average, this industry has a much higher performance problem regarding desired and achieved value creation. In addition to that, the importance and subsequently the required value contribution for the value creation levers are expected to be higher compared to an analysis for all industries.

The highest gaps for value creation are in the fields of cost, quality and risk. While reliability already shows a significant gap, the gap for risk is even higher. The high importance of risk management in the chemical, pharmaceutical and healthcare industry should not be surprising. However, the large gap for such an important topic in this industry is an important negative indicator. Additionally to the already mentioned aspects, the industry can improve on reliability, speed and innovation.

Taking a closer look at the performance and importance in the chemical, pharmaceutical and healthcare industry for good and bad performing companies regarding procurement shows significant differences for the Supply Value Management. The different importance and performance for quartile 1 and quartile 4 companies are illustrated in Figure 3. The companies have been grouped into four quartiles based on their average procurement performance. Quartile 1 therefore represents participants with a good procurement performance. Quartile 4 comprises companies with the worst procurement performance. Each quartile represents 25% of the survey participants.

It becomes obvious that the problems for good and bad performing companies in the chemical, pharmaceutical and healthcare industry are quite different. Good performing companies from this industry meet their cost targets and can refocus their attention to areas like quality, reliability, risk and innovation. Companies from quartile 4 do not achieve their targets regarding their most basic KPI, i.e. cost reduction. As a result, they have fewer resources to focus on other value creation levers. Subsequently, they have a bad performance concerning quality and reliability and a very bad performance regarding risk (management) compared to their (already low) aspiration.

Another interesting aspect is also revealed. Growth aspects in general seem, on average, to be less important for bad performing companies. The good performing companies even see innovation as one value creation lever which they need to improve while this is almost completely unrealized by bad performing companies. What both quartiles have in common is the fact that they state they need to improve on risk.

In total, the importance of all value creation levers for good performing companies in the chemical, pharmaceutical and healthcare industry is significantly higher and good performing companies consider more different aspects they need to work on.

4 Supply Infrastructure Management (SIM)

Supply Value Management covers all levers by which procurement directly creates value for a company. But there are indirect ones as well, i.e. aspects that define procurement’s infrastructure. Therefore, another framework has to be developed. This framework considers the supporting aspects and resources of procurement for value creation. This framework is called Supply Infrastructure Management. The SIM framework has like the SVM framework been set up on the empiric findings of the three global procurement studies conducted.

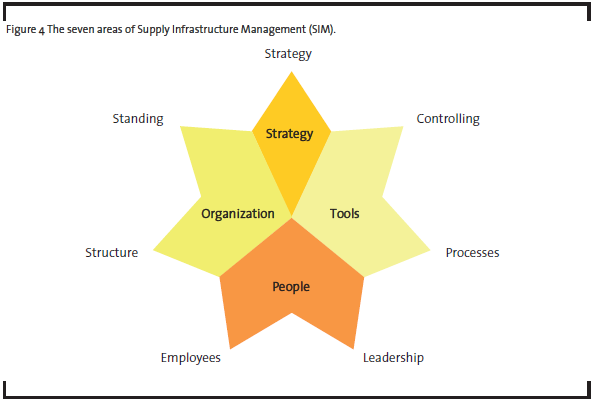

There are seven different aspects that this framework takes into account which can be grouped into four different areas: strategy, tools, people and organization. It is noteworthy that this framework is not about direct value creation. Each of the aspects that is part of this framework is supporting or reinforcing the value creation levers of the SVM, but none of the aspects is creating value by itself. For example, standardized processes, a new IT systems or more or better employees are not creating any value by their existence. However, they can provide the necessary resources, transparency etc. for procurement to e.g. better achieve cost targets by higher transparency or reduced time and effort spent on managing tenders.

The four areas of procurement’s infrastructure are described in the following:

Strategy: Based on the performance analysis of the study series, strategy is the most important aspect supporting the value creation of procurement. The strategy defines clear trade-offs for the nine value creation levers and provides guidance e.g. on whether quality is more important than cost or vice versa. This is highly important as not all value creation levers have the same importance for a company. Once these trade-offs are defined, they enable the company and procurement to better create value as they support the decision-making process. A lot of companies lack these and have problems to find optimum solutions when they have to choose between suppliers with different advantages and disadvantages. Additionally, it is important to link the procurement strategy to the overall business strategy.

Tools: The two aspects of the area ‘tools’ are controlling and processes. The controlling enables procurement to measure its performance and also shows the value contribution to other departments. The improvement of processes e.g. by standardization frees capacity that is currently blocked by operative tasks which are not creating any value for the company. The capacity can then be used for more value creation tasks e.g. by leveraging new potential suppliers for value creation.

People: The CPO and the employees are of course an essential part of the supply infrastructure. And for a lot of companies today, lacking good people and a strong leadership in procurement are main bottlenecks when willing to improve procurement performance and realize increased value creation.

Organization: The organizational structure of procurement does as well influence how procurement’s infrastructure can contribute to a better value creation. For example, the standing of procurement is important as it influences at which process step procurement is involved in buying decisions. A centralized or decentralized procurement organization also affects how procurement can or cannot create value e.g. by bundling supplies.

The framework of SIM is illustrated in Figure 4 and consists of the following seven areas:

- Strategy

- Controlling

- Processes

- Leadership

- Employees

- Structure

- Standing.

The Supply Infrastructure Management is an easy to use framework illustrating the current and aspired status quo for the supporting aspects of Supply Value Management. Therefore, the two models should ideally be considered in combination and not isolated.

4.1 Supply Infrastructure Management in the chemical, pharmaceutical and healthcare industry

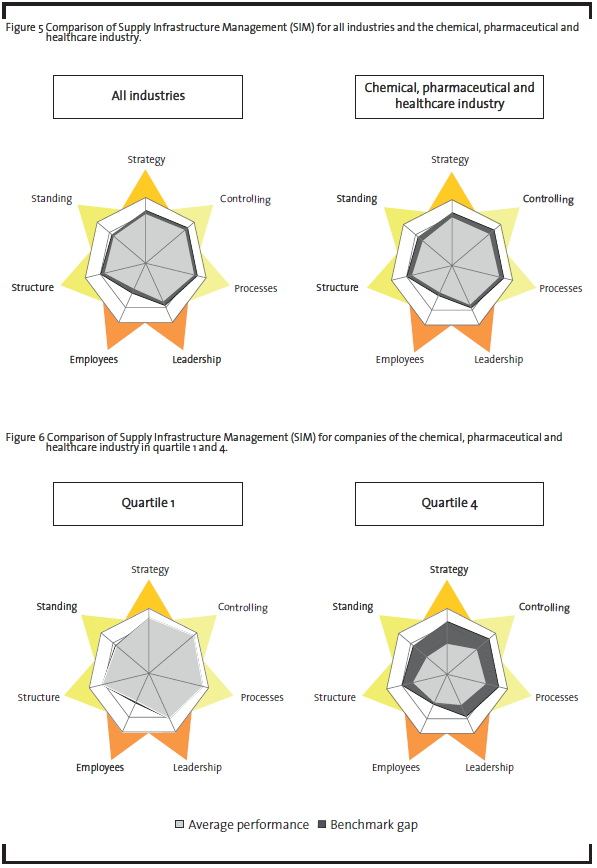

The analysis of the III. Global Procurement and SCM Study shows that there is a significant gap between importance and performance for all seven supporting aspects of the SIM for all industries. As for the Supply Value Management, the dark grey areas indicate the gaps which show that the average performance is lower than the average importance. In case there is no dark grey area, the importance and performance have been evaluated as being equal.

As illustrated in Figure 5, companies perform best regarding processes, controlling and (to a lower extent) strategy. This is not surprising because the same definitions that focus the value contribution of procurement in the areas of cost, quality and reliability define the core of procurement by its nature of optimizing material flows. Taking this process focused approach as a starting basis for procurement is very common across all industries.

The gap is highest for employees, structure and leadership within the cross-industry sample. The analysis illustrates one of the major problems that procurement is currently facing. In general, there are too few employees with the right skills available and subsequently many companies state that they would need additional resources. In addition, employees are rather not having the expected qualification level. Most companies also miss an incentive structure supporting the value creation of procurement e.g. in the field of cost. Providing incentives in reliance to cost saving targets would be a smart approach to increase the performance of these employees and procurement as a whole.

But also procurement’s interface to senior executives is something that needs to be improved. Procurement many times misses to have a voice in the board of directors which is an indication on the limited power procurement has in a company. This fact is also linked to the leadership capabilities of the CPO. Strong CPOs will manage to improve this interface and direct more attention towards procurement. The leadership capabilities are also linked to the fact that the CPO often originates from operations. This would shape the mindset of the CPO to a large extent, so that the operational value creation levers push other levers into the background. Subsequently, some value creation potential is left unexploited.

The challenges for the chemical, pharmaceutical and healthcare industry are similar to the overall industry sample but showing different centers of gravity. However, what becomes obvious from Figure 5 is that the performance gaps for most aspects of SIM are higher than in the analysis of all industries. Only for employees and leadership, there is a performance gap that is not as high as for the cross-industry sample. As indicated for the SVM, the gaps for the chemical, pharmaceutical and healthcare industry are also for the SIM significantly higher than for the cross-industry average (with exception of employees and leadership). The highest benchmark gaps are present in the fields of controlling, standing and structure. Most obvious, the standing of procurement in this industry is below the average cross-industry benchmark.

As indicated earlier in this article, the lower standing of procurement in the chemical, pharmaceutical and healthcare industry should not be a big surprise as the standing of departments like sales and especially R&D is quite high in this industry. The interface to senior executives is also not as good as in the cross-industry benchmark. This might to some extent also be related to the gap existing for controlling. Once the value contribution of procurement is not measured and communicated transparently, the standing is weakened. Although all aspects of the SIM show significant performance gaps, the gaps for employees and leadership are smaller than for the cross-industry analysis. The chemical-related sector with a lot of large multinationals seems to be better than average able to attract good people in sufficient numbers who are led by a CPO with adequate leadership capabilities. Nevertheless, the chemical, pharmaceutical and healthcare industry still needs to improve on these aspects.

A closer look at what good and bad performing companies in the chemical, pharmaceutical and healthcare industry are doing differently is illustrated in Figure 6. The good performing companies of this industry do not show any significant benchmark gaps in the field of SIM. They are meeting almost all performance targets for the seven aspects of SIM. Only slight necessary improvements for standing and employees for the top performers can be identified.

The picture for the bad performing companies in the chemical, pharmaceutical and healthcare industry is completely different. These companies show a very high benchmark gap for all areas of the SIM. These gaps are highest for strategy and standing. If we compare this with Figure 3, we can identify that bad performing companies do not seem to really have a procurement strategy as procurement for them mainly focusses on two aspects, i.e. cost and quality. Again, the gap for employees is even quite low for bad performing companies which underlines the fact that employees do not seem to be one of the major infrastructure problems for this industry.

5 Supply Value Maturity Model (SVMM)

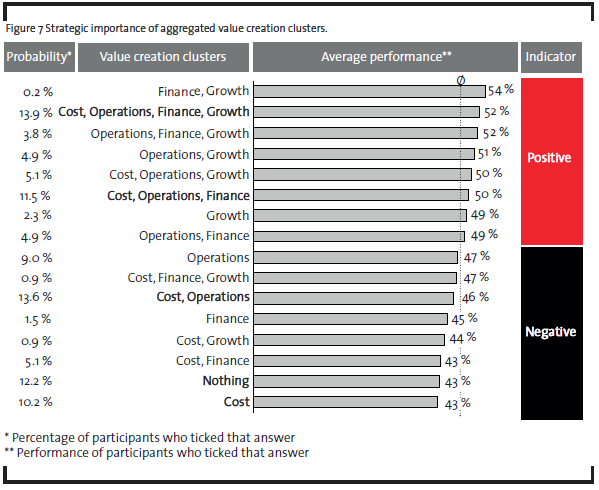

A lot of the discussion has been led by the fact whether a company is performing good or bad. Based on the SVM framework, there are four key value creation clusters how a company can generate value in procurement: cost, operations, finance and growth. The question is which value creation cluster is the best indicator for an excellent performing company.

Figure 7 displays the average performance for different value creation strategies. These strategies are clustered into four value creation cluster mentioned above (cost, operations, finance and growth). A procurement strategy is thus defined as the sum of the value creating clusters which a company perceives to be very important for its procurement. As illustrated, there are 16 different combinations like ‘cost and operations’ or ‘cost, operations, finance and growth’ possible. Figure 7 shows the average procurement performance of companies choosing a certain strategy cluster. In addition, listing the probability of the value creation clusters reveals how common a certain value creation cluster is.

From the bottom to the top of Figure 7, the average performance of a company is increasing. The graphic also shows that the better the performance, the more complex the strategy becomes as more value creation clusters are considered.

Figure 7 shows that companies with a higher procurement performance do not take completely different value creation clusters into account. The main distinction between good and bad performers is that the good performers see their strategy and their everyday work as being more complex.

There are five common combinations, each with a probability above 10%, which are marked in bold. What might be somewhat surprising is the fact that a company that is only focusing on cost as value creation target is performing similar to a company that has not defined any value creation target at all. So, cost alone cannot be the solution for a good procurement. Figure 7 also shows an interesting pattern: the more cluster a strategy contains, the better the performance. And there seems to be natural order when adding any cluster, starting with cost, then operations, then finance and finally growth.

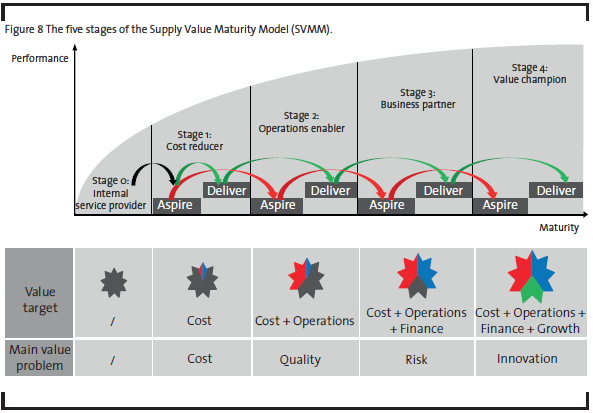

The SVMM is a framework which combines these different strategies for value creation and their related average performances. The different dimensions that are added as value creation levers form different stages a company can pass through. The SVMM shows the following five value stages with typically increasing overall performance:

0) No strategy

1) Cost focus

2) Cost & operations focus

3) Cost, operations & finance focus

4) Cost, operations, finance & growth focus.

However, stating that there is a specific value creation strategy in a company is not necessarily reflecting whether a company is also able to achieve the value creation targets that have been put in place. Therefore, the value creation strategies have to distinguish aspired and delivered value creation targets. The stages with the value targets added and the main value creation problems of each strategy are illustrated in Figure 8.

As it becomes clear from the illustration, there is a different main value problem for each of the stages. Subsequently, not all aspects of a supply value creation category are in focus once a new dimension is added to the value target. For stage 1, the main value problem is cost. In the next stage the operational perspective is added as a value cluster while the main value creation problem lies now in quality. For stage 3, the new dimension is finance and the main value creation lever most companies in this stage are struggling with is risk. In the last stage where procurement is seen as ‘Value Champion’, the added dimension is growth. Companies in this final stage of the Supply Value Maturity Model are mainly facing challenges in terms of innovation in order to achieve their value creation targets.

There is another interesting aspect of the SVM Model shown in Figure 8. Stage 0 is maybe the level where procurement has had its starting point. Based on the analysis, only 13% of companies are located at that stage (see Figure 9), so that most of the companies have already passed it by adding cost as a first value creation lever. However, there are companies who do or did deliver on this value creation target while others are or were unable to do so. Therefore, stage 1 and all following stages distinguish between aspired and delivered value creation. Comparing what companies aspire and what they are able to deliver shows that only the minority is able to deliver. Once a company proceeds from one stage to another without having been able to achieve the value creation targets of the previous stage, it is clear that company will have huge problems in delivering regarding the value creation targets of that new stage. As a consequence, a company will not be able to move directly from stage 0 to stage 5 but rather has to proceed stagewise along the maturity model.

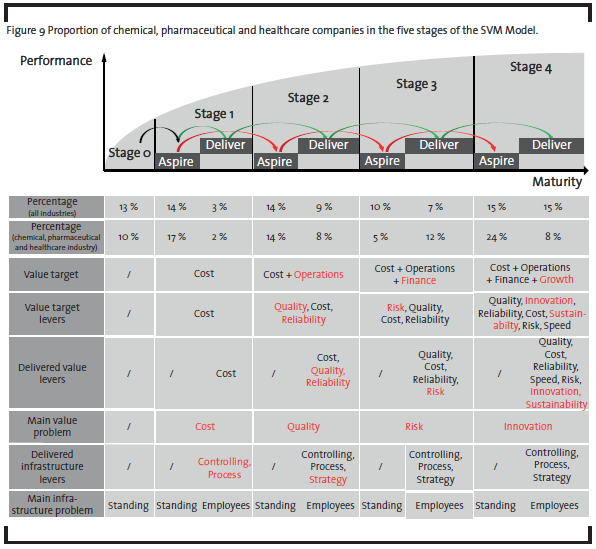

5.1 Supply Value Maturity Model for the chemical, pharmaceutical and healthcare industry

Taking a closer look at where companies in general are positioned in the Supply Value Maturity Model and where the chemical, pharmaceutical and healthcare industry in particular is situated is shown in Figure 9. Looking at the average of all companies shows that most companies are either in stage 2 with cost and operations or in stage 4 with cost, operations, finance and growth as value creation targets.

The illustration also shows that not all value creation levers of a specific value creation category are added once another cluster added. In case of adding finance, typically only risk is added as a value creation lever to the already targeted levers.

Comparing the distribution of the chemical, pharmaceutical and healthcare industry to the different stages of the SVM Model shows that the companies are almost spread in the same way as the cross-industry sample. The analysis also shows that the main differences can be found in stages 3 and 4. Here, the aspired value creation of procurement is quite high but the procurement departments of the chemical, pharmaceutical and healthcare industry are not able deliver highly on the expected value creation.

Taking the SVM Model step by step starting with stage 0 shows that only 10% of the companies from this industry are still in the earliest stage. At this stage, procurement is seen as an internal service provider and its value contribution is very limited. In stage 1, which is focusing only on cost as a value creation lever, there are 19% of the companies in total. Although cost as the main value creation lever is not that sophisticated, only 2% of the companies from the chemical, pharmaceutical and healthcare industry are able to deliver the aspired value creation target, so that the effective value creation of companies in stage 0 and 1 is very similar.

A little more companies are located in stage 2 where the focus of value creation additionally lies on the value creation levers quality and reliability. In this stage, 8% of a total of 22% of the companies are able to deliver on the value creation target. In stage 3, with risk as additional value creation target, are most of the achievers. 12% of the companies are able to deliver the aspired value creation. The main value creation problem is that companies of the chemical, pharmaceutical and healthcare industry are not able to deliver the aspired value creation for risk. This is again underlining the fact that the industry is having a major problem with this value creation lever as already elaborated before.

Finally, there is stage 4 where most of the companies do find themselves in. Almost one third (32%) of the companies states that according to their strategy they are at this maturity stage. However, only 8% of the companies are able to really deliver the aspired value from a procurement perspective. In other words, only 8% of the companies in this industry are really ‘value champions’ – for the average cross-industry sample, this number increases to 15%. The main problem in stage 4 is innovation (and to a lesser extent sustainability) which is added to the (sometimes still unsolved) value creation problem of stage 3. The companies try to increase procurement’s value creation by sourcing innovate products or technologies from their supplier but miss to exploit the power for growth opportunities from existing and potential new suppliers. This fact has its root cause in the Supply Infrastructure Management where procurement is struggling with achieving the necessary standing for having the necessary power to drive value creation.

In total, the number of ‘Value Champions’, i.e. those companies who are able to deliver on all value creation clusters in stage 4, is quite low. But at the same time, the aspired value creation of procurement in the chemical, pharmaceutical and healthcare industry is quite high. That way, most companies are not able to deliver the aspired value creation targets. This is already based on the results derived by analyzing the Supply Value Management and Supply Infrastructure Management where risk management and the standing of procurement have already been outlined as major bottlenecks.

6 Conclusion

There are three frameworks for procurement provided in this article. First, there is Supply Value Management that is clearly defining which value creation levers procurement really has. It is a framework that helps any company to choose what is really important for procurement in a specific industry and company e.g. to decide which suppliers to choose.

In addition to this framework, there is Supply Infrastructure Management, which is combining all relevant supporting aspects for value creation by the SVM. Its seven aspects are supporting the nine value creation levers and are not value creating by themselves. The SIM answers which resources are needed to create value with procurement.

Finally, there is the Supply Value Maturity Model. This framework allows to allocate a company regarding its procurement maturity to five potential stages. From stage 0 where procurement is seen as an internal service provider to stage 4 where procurement is value champion delivering on the cost, operations, finance and growth value creation clusters. Each of the stages additionally distinguishes whether a company only aspires or really delivers on the value creation clusters.

A close look at the Supply Value Management framework for the chemical, pharmaceutical and healthcare industry revealed major value creation potentials in the field of cost, risk and quality. In comparison to all industries, it becomes obvious that the performance for all value creation levers is significantly lower. For most companies in this industry, it would therefore be a good advice to improve on risk, quality and cost to achieve a better value contribution of procurement.

The main reason why companies are struggling with achieving higher value creation resulting in a better procurement performance can be found in the Supply Infrastructure Management. As mentioned, the chemical, pharmaceutical and healthcare industry has to improve on all aspects of the SIM. The activities to improve SIM are concerning a better connection to the executive management and increasing the standing of procurement within the company. Before doing so, an improved controlling with more transparency of procurement’s value contribution should be implemented.

Most of the companies of the chemical, pharmaceutical and healthcare industry are to be found in stage 2 and stage 4 of the Supply Value Maturity Model, meaning they focus to a minimum on cost and operational aspects. However, the differences for the aspired and delivered value creation in the SVM Model are highest in stages 3 and 4. From a value creation perspective, the major problem has to been seen in the field of risk while from an infrastructure perspective, the main problem is the standing of procurement within the company.

The chemical, pharmaceutical and healthcare industry is an industry with high aspirations regarding procurement but only average performance, which has its root cause in a too low standing of procurement by senior executives, leading to a situation where procurement has huge problems to deliver on advanced procurement value creation levers like risk and innovation management of suppliers.

References

Porter, M. E. (1996), What Is Strategy?, Harvard Business Review, November-December, p. 61-78.

Porter, M. E. (1985): Competitive advantage: Creating and sustaining superior performance, Free Press, New York.

Van Weele, A. J. (2010): Purchasing and Supply Chain Management: Analysis, Strategy, Planning and Practice, 5th ed., Cengage Learning, Andover.