The future of chemical distribution in Europe: Customer relations as key value lever

About 10% of the overall output of chemical producers is distributed via independent chemical distributors. More than this pure figure indicates, chemical distributors bear a tremendous importance in distributing chemical products to an often very widespread customer base. Chemical distributors help the producers to lower the complexity of product distribution and customer management. In addition to the distribution function itself, they often offer technical support, laboratory or packaging/labelling services additionally.

Chemical companies increasingly realize the value of chemical distributors as valuechain partners and implement structured chemical dealer/distributor management functionalities in their organisations. Fuelled by headlines that are related to the success of chemical distributors- even in times of crisis as in the years 2008 and 2009 – this industry gains interest in the Chemical Community and related publications.

What are the key success factors of the chemical distribution industry? How can the current and future role of chemical distributors between producer and end customer be characterized? What is the outlook for the merger & acquisition (M&A) activities? These and further questions have been answered by a study with 62 participants from the chemical distribution industry in Germany, Austria and Switzerland. The study has been conducted by Grosse-Hornke Private Consult in close cooperation with the University of Münster at the end of last year.

Importance of face-to-face contact

Although 2/3 of the participants apply IT systems to support communication and interaction with their customers the personal and face-to-face contact is still of paramount importance–favoured by 92%. In particular in the specialty chemical business with complex products personal contact is the key to sales success. Personal customer contact is increasingly supplemented by sophisticated Customer Relationship Management (CRM) systems–mainly with the intention to analyse customer and market data. While the chemical distribution industry has been characterized by strong consolidations during recent years, many study participants claim that a further consolidation will lead to the risk of loosing a local footprint.

Chemical producer and chemical distributor as tandem

84% of the answers picture a cooperative relationship between chemical producers and distributors. Obviously, the role of chemical distributors as middlemen to the customers is well appreciated by the producers. This evaluation is most likely the reason why only 26% of the study participants assume that chemical producers will start to establish their own distribution entities in order to by pass the independent chemical distribution companies

Product training as key sales tool

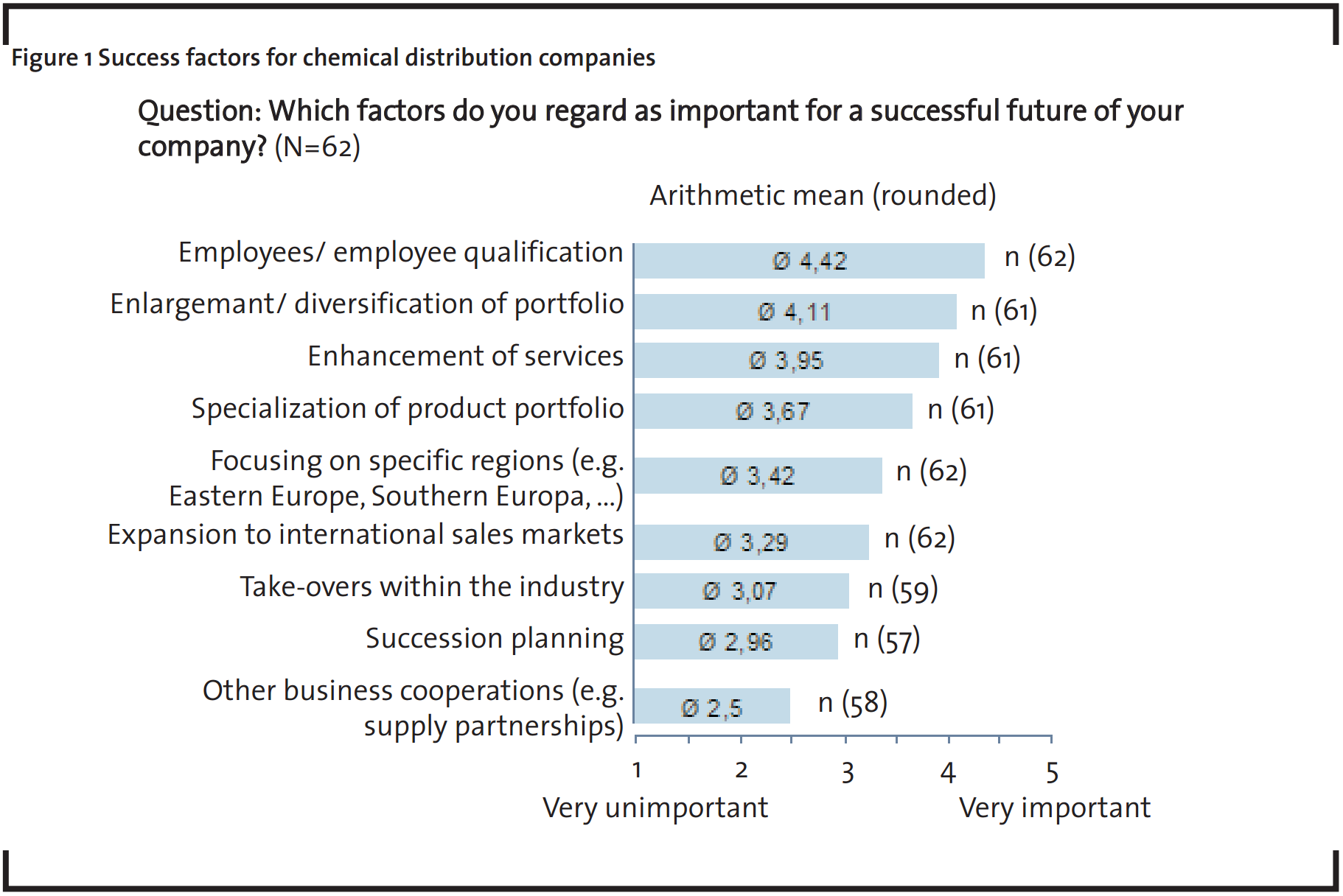

Success in the specialty chemical industry strongly depends on know-how about products and their application–often closely linked to a specific industry. Therefore, product trainings provided by producers are rated “important” by 85% of the study participants. An increased focuson enlarged product and service portfolios (refer to figure1) will in the future further grow the need for dedicated product and service trainings. One quarter complains that dedicated “distributor development programs” should be stronger pursued. The study results indicate that there is still room for improvement regarding better aligned marketing efforts between the chemical producers and their distributors.

Increasing focus on employee qualification programs

The growing shortage of highly skilled workers is often discussed and also our study proof (refer to figure 1). Getting the right people and keeping them is more and more becoming a challenge for often rather small chemical distribution companies. Accordingly, retention programs and employer branding are getting more important–this applies especially for rural areas.

Mergers and Acquisitions (M&A) activity staying strong

Due to the fact that the chemical distribution industry has seen strong M&A activity in the last years, big deals are getting more and more unlikely–not least due to anti trust regulations. For example, 55% of the study participants expect a constant M&A level and 34% a slightly increasing one for the German market. For family owned chemical distributors the acquisition by another distributor is often the only way to ensure business continuity.

Procurement in Asia growing

Asking which markets are of strong importance regarding procuring chemical products, 87% of the study participants named China and India and 61% voted for Asia in general (excl. China and India). However, for entering new markets, companies are well aware of key hurdles like strong market saturation (60%), missing human resources (44%) or currency exchange risks (45%).

Outlook: Value of strong customer contacts in challenging times

For the year 2012 a growth of more than 4% of the world-wide chemical production is assumed by industry experts. However, for the EU-countries a heterogeneous picture is drawn. Due to the continuing Eurocrisis, especially in Southern Europe, the outlook remains unsecure. In such challenging times a direct and quick feed back from the market regarding product demand is of high value. Therefore, only those chemical distributors will continue to play an important role that further professionalize their middlemen position by relieving the chemical producers from sales activities and gaining knowledge about the final source of revenue – the end customer.