Mergers & Acquisitions (M&A) in the Pharmaceutical and Chemical Industries: A Lighthouse in Choppy Waters

After record years in 2006 and 2007 that even topped the peak-year 2000, a cooling down of the international market for Mergers and Acquisitions (M&A) could be observed in 2008: Whilst the global transaction volume in 2007 reached about $ 4,400 bn. (2006: $ 3,600 bn.), the total for 2008 is expected to hit about $ 3,300 bn. The main reason for this development can be seen in the financial market crisis and the resulting problems for financial investors to raise outside capital. Consequently, these financial investors account for less then 10 % of the global M&A market and it’s up to strategic investors – often family-owned – to fuel the national and international M&A markets. Unlike financial investors, companies (strategic investors) are still able to embark on M&A activities in the $ bn.-range due to their often comfortable solvency situation.

Although it’s very likely that we are currently observing the final stage of the so-called 6th “M&A-Wave”, it should not be forgotten that the global M&A year 2008 was even stronger than the 5th “M&A-Wave”-peak in the year 2000. Strategic investors in the pharmaceuti- cal and chemical industries accounted for a major portion of the global M&A market during the last years. This article delivers a brief review of M&A in these industries, together with an outlook for the year 2009.

Strong market consolidation

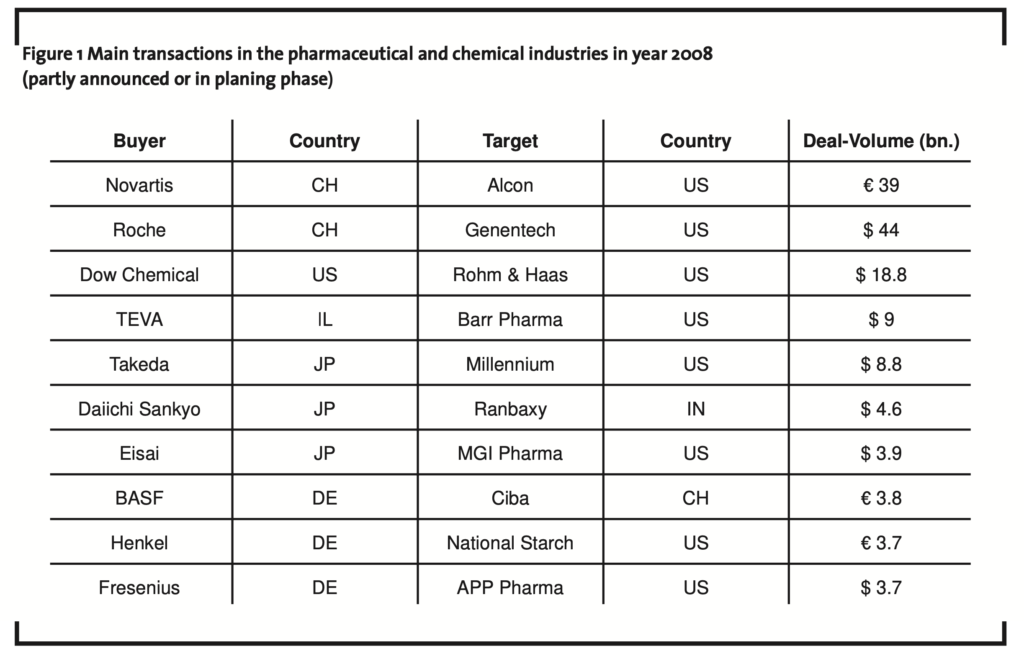

When looking at the big deals in the pharmaceutical and close-by chemical industry, it is evident that after mega acquisitions in 2006 (e.g. Bayer/Schering, Linde/BOC Group, Merck/Serono) and in 2007 (e.g. Akzo Nobel/ICI, Schering-Plough/Organon Bioscience), the year 2008 is once again proving that companies in the chemical and pharmaceutical markets are responsible for a large part of the global M&A volume. In the first half of 2008, the dominant role in the pharmaceutical M&A market was played by transactions with Japanese participation (e.g. Takeda/Millennium, Daiichi San- kyo/Ranbaxy, Eisai/MGI Pharma), accounting for a transaction volume exceeding € 17 bn (refer to figure 1). It is obvious, that in the rather saturated Japanese pharmaceutical market, which holds about 9 % of the global $ 712 bn. pharmaceutical market (year 2007), Japan-based pharma-suppliers are looking for growth opportunities in other geographical markets or are trying to improve their position in bio-tech and generics. Mega deals dominated pharmaceutical industry headlines at a later stage in 2008, such as those announced by Roche (takeover of US biotech company Genentech for about $ 44 bn.), Fresenius (takeover of US- based APP Pharmaceuticals for about $ 3.7 bn.) and Novartis (planned takeover of US-based contact lens specialist Alcon for € 39 bn.). Next to strategic product-driven considerations, the strong position of European currencies against the dollar supported this development. After the planned takeover of Barr Pharmaceuticals (USA) by the Israel-based global generics market leader TEVA, there are already speculations in the market, that the Germany-based generic producers Stada and Ratiopharm are the next takeover targets, which would lead to a further consolidation of the generic pharmaceutical market – or at least the pharmaceutical market in general.

Although the M&A market start in 2008 for the chemical industry was not as dynamic as that of the pharmaceutical one, the announced takeover of the US specialty chemistry company Rohm & Haas by Dow Chemical in July 2008 (transaction volume: $ 18.8 bn.) or National Starch by Henkel for about € 3.7 bn. and Ciba by BASF for € 3.8 bn. made clear that chemical players are also going through a rearrangement phase and taking their chances. However, the strong M&A activity of the chemical industry in 2008 should not delude that, during the last 3-4 months, the financial crisis had massive impact on chemical companies’ customers – especially the automotive industry (for example: in the USA, November 2008 carsales with – 37 % were the lowest since 1982). Massive demand reductions are already leading to reduced production in many chemical companies. While disease-linked demand for pharmaceutical products is relatively stable, investments in chemical (derived) products can – to a large extent – be postponed or even completely abstained. This situation over the last 3-4 months is certainly leading to extreme cautiousness regarding M&A in the chemical industry.

Key M&A market drivers in chemical and pharmaceutical markets

The recently observed takeover premiums indi- cate a clear value creation deal logic. For example, referring to the stock price at announcement date, the takeover premium at the Takeda/Millennium deal was at 53 % and Dow Chemical is willing to pay a premium of about 70 % for the planned Rohm & Haas takeover, to be followed later in 2008 by premiums for example of 32 % for the BASF/Ciba and 42 % for the TEVA/Barr deal. Such high premiums can only be justified by massive cost synergies or revenue/profit-growth expectations. Since revenue synergies are difficult to quantify and most value calculations are therefore based on cost synergies, the reason for such premiums is very often seen in cost synergies in areas such as administration, procurement, sales and R&D. Examples for targeted cost synergies p.a. are $ 750 – 850 mill. for the Roche/Genentech deal, € 240 – 260 mill. for the Henkel/National Starch deal and about € 220 mill. for the BASF/Ciba deal. Since acquisition prices of the above mentioned takeovers were negotiated before the stock market crash in October 2008 the pressure to reach – or even exceed – the targeted cost-synergies is undoubtedly growing. This is especially true given that market-oriented revenue synergies are unlikely to be realized in the current economic slump.

Especially for pharmaceutical companies, the realization of cost synergies is the main approach to further realize high margins, while many patent-related “super margins” will erode during the next years – according to the researchers company Datamonitor, pharmaceuticals which will lose patent protection between the years 2007 and 2012, will lead to a revenue decrease of $ 115 bn. sales. When “blockbusters” with their $ bn sales volume disappear, generic pharmaceutical companies will expand their market power and will themselves strive for economies of scale by means of M&A. Moreover M&A is seen as an adequate means to create “critical mass” for cost-intensive active pharmaceutical ingredient research – on average it costs $ 800 mill. and takes twelve years to develop a new drug. This “Herculean task” can only be achieved by big and financially strong companies. While managing the costs on the production part is hard enough for many companies, additional pressure comes from the revenue part. Governmental efforts target to reduce drug prices in order to unburden the public health care systems. This increased cost pressure implicates further consolidation pressure, also for the generic pharmaceutical industry.

Acquisitions driven by strong revenue growth expectations – or at least substitutions for lost “blockbuster” revenues – most certainly play a major role in the acquisition of biotech companies like Serono, Millennium or Genentech. Likewise, macroeconomical factors such as demographic changes and resulting shifts in the demand structure in the traditional triad regions (USA, Europe and Japan), lead to the necessity to capture new markets.

2009 is predicted to be another strong M&A year for the pharmaceutical industry

Given the above mentioned factors, the pharmaceutical industry will remain under cost pressure. It is therefore assumed that M&A activity in the pharmaceutical industry will continue to be high in the year 2009, in order to meet global market needs and to reduce costs in parallel – this might even be accelerated by the separation of generic business parts and a shift in business models towards companies which are either focused on low-cost generic production or on R&D-intense production of patented drugs.

For the chemical industry, the further development of raw material prices and product demand will be a key driver regarding the M&A level. Should raw material price levels start to rise again M&A will be an option in order to further reduce costs and to secure profits. Furthermore, low product demand levels might lead to a new arrangement of critical masses in the chemical industry, resulting in M&A activity.

It can be summarized that the current conditions are keeping the M&A wheel turning, not only in the chemical but especially in the pharmaceutical industry and the M&A market volume for the year 2009 stands a good chance to reach a high level again. However, it should not be forgotten that about 2/3 of all transactions do not meet the expectations. Therefore, apart from a careful target-setting and target-selection process, post merger integration (PMI) remains a key issue. A carefully managed PMI with a strong focus on cost/revenue synergy realization, helps to justify the acquisition and to ensure a “happily ever after marriage, once the excitement of the wedding party has worn off”!