Responsible Use – The Social License-to-Operate: A business approach towards sustainability in chemicals & materials

Chemicals & materials are key ingredients in food, health, housing, mobility, communications, leisure, and many more applications. Especially polymers have enabled material welfare for large societal groups since the middle of the 20th century until today. The unwanted side effects of chemical & material mass production and consumption are visible in form of waste, emissions, resource consumption, human & environmental toxicity, land use, and reduced biodiversity. The industry has adopted the UN 2030 agenda for Sustainable Development (UN-SDG, UN Global Compact), the Paris Agreement to reduce greenhouse gas emissions (COP 21) and supports the aims of the European Green Deal (Chemicals Strategy for Sustainability) towards a safe, resource efficient, circular, low-carbon society.

In line with those targets chemical & material companies increasingly decarbonize energy generation, lower resource consumption across operations and global value chains, reduce waste and emissions, and prevent harm to humans and the environment throughout the entire life cycle. They report on their environmental and social achievements and invest in green technologies. Irrespective of those activities to make chemicals and materials “greener”, the image of the chemical industry stays poor and partly even worsens. Chemistry is associated with “artificial/ synthetic”, “toxic”, “pollution” and “dangerous”. This has been true for a long time and there is probably not much to do about it. What is new is the fact that the chemical and material industry increasingly loses support also by their own customers. Take for instance the cosmetics industry, which explicitly excluded chemical cosmetic ingredient producers from their initiatives to define what sustainable and green cosmetics should be.

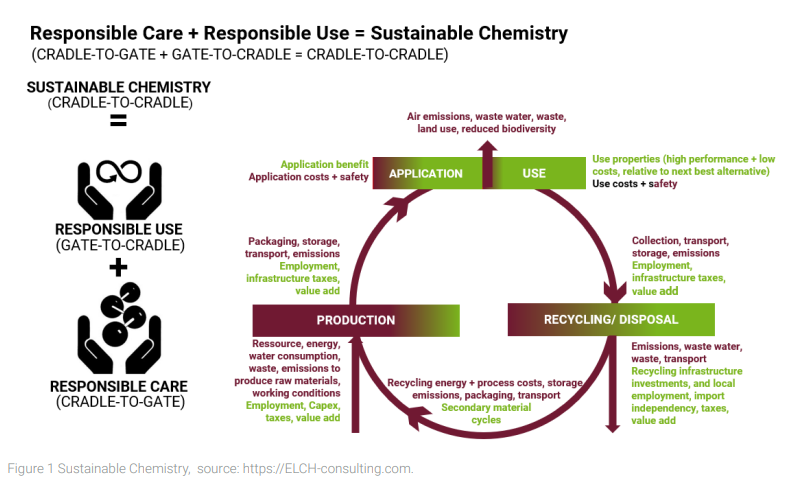

So how did it happen that the chemical and material experts are increasingly excluded by their customers to define a sustainable future? We believe it is the too narrow product scope. The chemical industry has based its sustainability charter and activities on the principles of Responsible Care. Responsible Care was introduced in 1984 and is today the guiding principle for the industry globally to achieve environmental, social, safety, and do no harm goals that reach beyond legal requirements (License-to-Operate”). The product scope of Responsible Care is “Cradle-to-Gate”, starting with raw materials and energy through supply chain and production to the factory gate of the chemical or material company. It also includes end-of-life treatment, be it disposal, burning, or recycling. This is fully reflected in the sustainability activities and reporting of the companies.

The application and use of chemicals & materials (“Gate-to-Cradle”) are not explicitly addressed. The pure product focus of Responsible Care disregards other mechanical, biological, physical, or other chemical and material solutions a user may consider. We see this narrow product focus as a fundamental shortcoming and a missed opportunity for the industry to gain more social acceptance.

The Cradle-to-Gate (“footprint”) approach looks at the unwanted environmental and social costs in the production and supply chain of a chemical or material, but not at the social benefits of chemicals and materials in use (“handprint”). Minerals, crude oil, air, salt, and other resources are transformed with energy and labor to produce chemicals & materials. There is a social benefit for only a few, directly involved investors and operators, but unwanted environmental and social costs for many. From that perspective, the pure production of chemicals and materials is per se not sustainable. This is by the way also the case with most other products and thus not very noteworthy. It explains however the image issue of the industry. Reducing environmental and social costs may help to make products less unsustainable (“greener”), but it will never be able to fulfill “net zero” requirements and thus continue to disappoint expectations, which are probably unrealistic in the first place. Only the use brings social acceptance and benefits that justify or outweigh the unwanted environmental and social costs.

Take for instance smartphones and battery electric vehicles (BEV). They have significantly higher environmental and social costs compared to former blackberries and internal combustion engine (ICE) vehicles, which they substitute. Neither factual environmental and social costs nor scientific decision criteria from cradle-to-gate, but merely societal acceptance in the gate-to-cradle application define, if it is responsible to use those products or not.

In the case of smartphones, more than 1.2 billion people (c. 15% of the global population) decided to buy a new one last year and BEV sales rose to 7.8 million (c. 10% of global passenger car production) in 2022. Society has implicitly decided that the many more benefits and functionalities of a smartphone compared to a blackberry or the lower net operating costs and lower local emissions of BEVs compared to ICEs justify the higher financial, as well as environmental and social, product costs. With chemicals & materials it is a bit more complicated than with smartphones and BEVs, but in principle, it is the same.

A first complication is that chemicals and materials are often building blocks that have multiple applications and uses. Epoxy resins for instance are produced from toxic precursors. It is probably very responsible to apply epoxy resins under controlled conditions and use them to make windmill rotors larger and more efficient, car coats more scratch and park decks more oil resistant. On the other hand, there may be better alternatives than using the same epoxy resin to coat the inside of beverage cans or drinking water containers. The companies in the chemical & material industries and their associations are however generally organized by products and technologies. Another current example are PFAS and fluorinated polymers. There are probably sustainable applications, like catheters, 5G equipment, semiconductors, lithium ion batteries and green hydrogen electrolysis cells, where it is very difficult or impossible to find adequate substitutes. But there are other applications, like make-up, lipstick, frying pan coatings and outdoor rain protection, where less performing substitutes are good enough to do the job without the unwanted side effects. They want to utilize their assets and thus have a strong incentive to sell their products into all application areas that are legally allowed to serve, irrespective of the responsibility in the application and use areas. A second complication comes from indirect sales via distributors, traders or agents. Routes-to-market are often not very transparent and it is not always clear, who the final user really is.

Another complication is the fact that the societal acceptance of what are responsible or not so responsible uses varies by groups as well as countries or regions and over time. Some societal or regional groups accept the use of nuclear energy, the capturing and storage of carbon dioxide or the use of blue or turquoise hydrogen as a sufficient contribution to climate change and sustainable businesses. Other groups require a complete ban of fossil hydrocarbons, both as a source of energy generation and feedstock, or the active removal of carbon dioxide from the atmosphere or the extensive use of green hydrogen to couple transportation, heat, and industrial sectors. How should industry deal with those partly conflicting and changing societal sustainability demands?

Complaining about an increasingly volatile, uncertain, complex, and ambiguous business environment does not help. Responsible Use of chemicals and materials should be done as a complementation of Responsible Care, not as a substitute. The process and steps of Responsible Use are the same as with Responsible Care, but the scope is enlarged from Cradle-to-Gate (product focus) by Gate-to-Cradle (use focus) and thus covers Cradle-to-Cradle (responsible products for responsible use along a value ring), see figure 1.

The additional Gate-to-Cradle “Responsible Use” part needs to cover all relevant uses of a given chemical or material in order to fully understand the risks and opportunities. Chemical & material companies and their distribution partners should implement Responsible Use in three sequential steps:

1. Regulatory compliance

Protecting regulatory License-to-Operate to stay in business

Fulfilling national and regional ESG requirements is the required minimum activity to stay in business. Those requirements cover non-financial reporting, supply chain transparency, greenhouse gas emissions, distribution permits, etc. Larger chemical & material companies are already fully covering those aspects at least Cradle-to-Gate, but small and medium-sized companies are often reluctant and should consider the deadlines, especially on non-financial reporting (CSRD, ESRS), supply chain transparency (supply chain due diligence law, TfS, EcoVadis) and EU taxonomy (REACH/ CLP). Regulatory compliance is often carried out along ISO 14001 (Environmental), 26000 (Social) and 37000 (Governance) standards, but it should go beyond current product stewardship and Responsible Care of a chemical & material. It should explicitly cover the Responsible Use of chemicals & materials. Understanding regulatory compliance issues of chemical & material users and their alternative problem solutions is important to understand fully, what is needed to stay in business. This may already confront managers with some unpleasant truths. Think for instance about a fine chemical that is used to reduce blood pressure and at the same time it is an active ingredient used in pesticides to kill insects. In the latter use it will be soon forbidden in some application areas and countries. In one application the fine chemical is the best problem solution with high responsible use and in another it may soon no longer been sold.

2. Financial impact

Achieving Social License-to-Operate by managing ESG- and diminishing sustainability-risks

Double materiality is the standard approach to managing ESG risks and opportunities. Inside-out the impact of the business on the environment and society is mirrored against the outside-in financial sustainability impact on the business. This is largely done for products with the consequence of easily ignoring or overemphasizing risks and opportunities. Doing the same for all relevant applications and uses helps to get a more balanced profile about the ESG- and sustainability risks and opportunities and their material and immaterial financial impact short, medium, and long-term on the specific applications and uses of the product.

Understanding this in detail is needed to maintain a competitive position and secure financial performance in an increasingly volatile, uncertain, complex and ambiguous environment, where greenwashing is the norm rather than the exception. Let´s assume a morally and ethically acceptable use. When there is no better technical and/or commercial solution to fulfill this specific needed application and use, then this is the sweet spot for the specific chemical or material. This is what the chemical and material industry should focus on and encourage customers to use. At the same time, they should not be shy to discourage or even ban applications and uses, where there are better alternatives and they should actively fight against no use and misuse. This can build trust and create additional sustainable businesses.

3. Business opportunities

Social License-to-Lead by offering societally preferred sustainable businesses

This is about taking an inside-out perspective to solve sustainability challenges better than competitors and other problem solutions. This allows for higher positive sustainability outcomes, enlarged product opportunities, more efficient, measurable environmental and/or social impact, preferred by various stakeholders. This is about being better and faster than competitors to effectively solve sustainability issues of key stakeholders, typically customers. This often comes with new technologies, solutions, and approaches that help to reduce environmental and/or social costs. Timing is often the key to be ready just in time to capture the opportunities of the regulatory framework (CO2-prices, taxes, duties, bans, incentives, subsidies, …) and the customers‘ willingness to pay for more sustainable solutions. Those companies that properly differentiate structural sustainability trends from mere greenwashing hypes or green fashions and those that are neither too early nor too late in capturing the business potential of sustainability needs will successfully grow sustainable businesses and take market shares from their peers.