The growing importance of covering payment risks in the chemical industry

The first dark clouds are gathering on the economic horizon of the chemical industry and may cause an unattractive dip in otherwise impressive growth. With the oil price remaining high, concerns that global economic growth is cooling and ever fiercer competition, the outlook is gloomy. There is also uncertainty about the reform of the European Community Regulation on chemicals, REACH, the financial impact of which is still impossible to predict for most companies. Such lists of possible causes of an economic slowdown often fail to mention the risk of bad debts, which may result in considerable financial difficulties for companies or, in the worst case scenario, lead to insolvency. However, providing security against the risk of payment default should always be on the agenda. This is particularly relevant in view of the growing importance of trade credit, a fact reflected by the winter 2007 Payment Practices Barometer recently published by Atradius. In addition, payment practices have deteriorated in some countries and sectors in Europe.

Trade credit as a competitive factor

More and more frequently, customers do not pay for goods supplied until such time as they have sold them on and have therefore posted their own sales. This means that in some cases suppliers have to wait a long time for their money. During this time, they are faced with the risk of non-payment. According to the survey findings, guarantees and delivery upon advance payment have become less common. Only 15% of the companies surveyed in Germany insist on advance payment whereas eighteen months ago, this figure amounted to 37%. Guarantees are now relevant in only 4% of business transactions (summer 2006: 14%). The findings of the survey also highlighted the effects of increasing competitive pressure at national and international level. Suppliers need to adapt to the payment terms of their customers if they want to keep customers.

These and other findings of the Atradius Payment Practices Barometer underscore once again how important it is for companies to secure receivables due, in order to prevent financial distress in the event of non-payment by their customers. This also applies to the chemical and pharmaceutical sectors, especially since – as described at the beginning prospects for the coming years are no longer as promising as they have been in the past. Accordingly, a rise in the incidence of non-payment is to be expected.

Deterioration in payment practices in the chemical industry

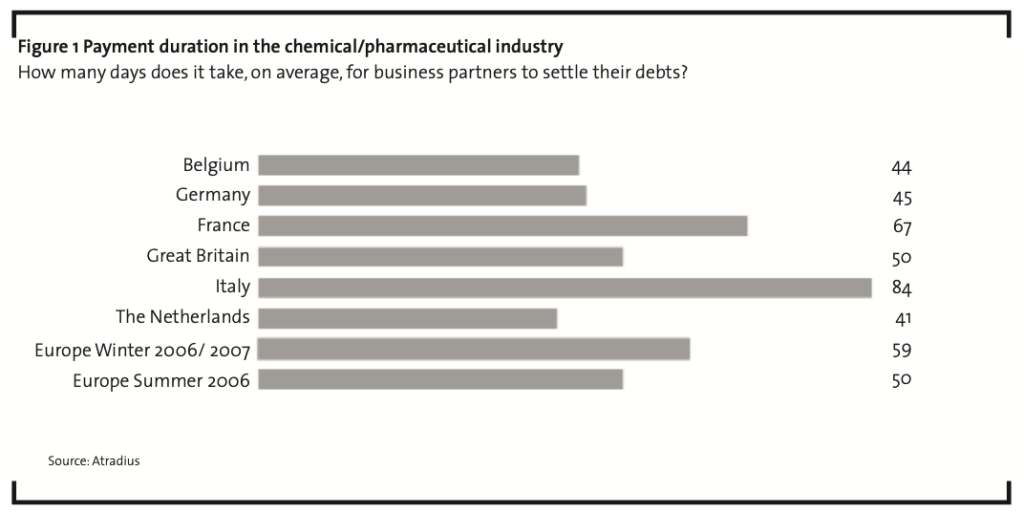

In summer 2007, Atradius carried out the first sector-based analysis of the two Payment Practices Barometers available at the time, summer 2006 and winter 2006/2007. The result showed that payment discipline deteriorated in most European business sectors within the space of nine months. This is also true of the chemical and pharmaceutical industries. The average time between receiving an invoice and payment increased from 50 to 59 days. Respondents also took a considerably more critical view of the sector in terms of late payments and complete non-payments.

The breakdown of the sector analysis by the individual countries surveyed provides a slightly more differentiated picture. In this comparison, the chemical and pharmaceutical sectors in Germany, for example, score much better. On average, payments were made within 45 days. However, companies exporting to other European countries waited significantly longer for their money. Chemical and pharmaceutical companies in the UK took an average of 50 days to pay invoices. French customers in the same sectors even waited 67 days before honouring their debts. Exporters supplying customers in the Italian chemical and pharmaceutical industries waited the longest, with invoices being paid after 84 days on average (Figure 1).

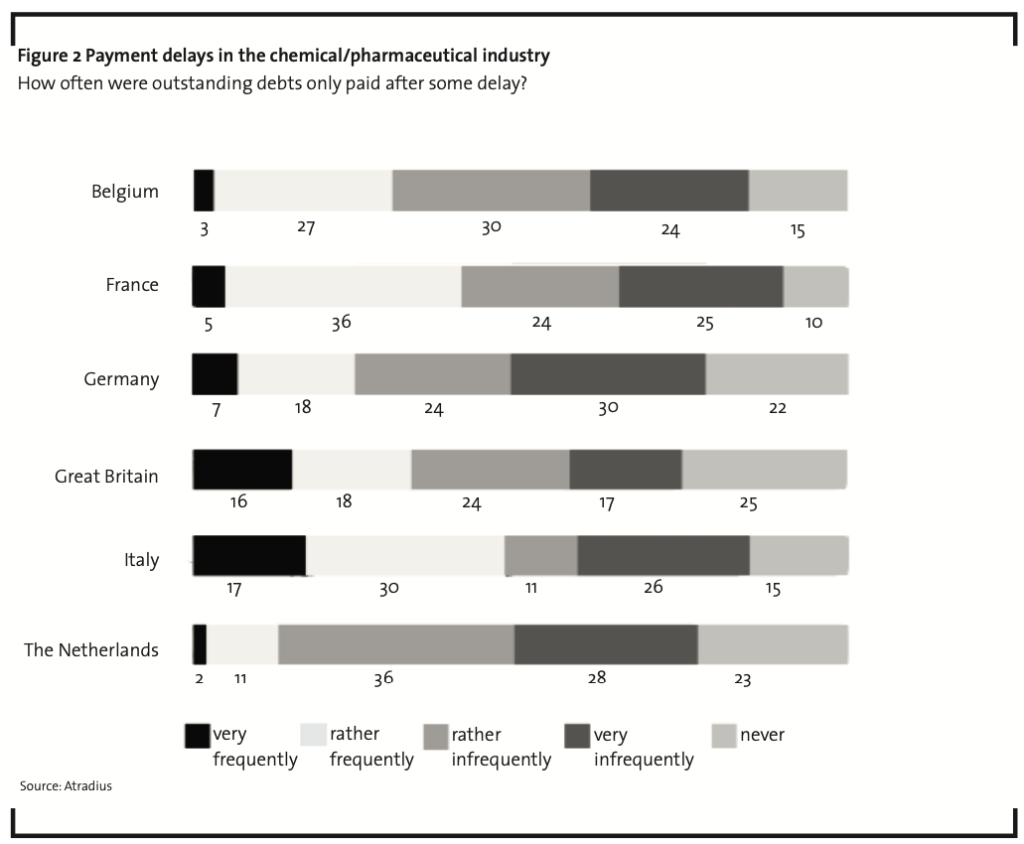

German chemical and pharmaceutical companies were given comparatively high scores by their business partners in Germany and abroad when these were asked about payment delays and complete non-payments. Payment delays occurred only in relation to one in four invoices. The situation is very different with regard to exports to other countries. Delays were most frequently experienced regarding deliveries to Italy, where almost half of the invoices (47%) were not paid within the agreed period of time. In France, this figure was similarly high (41%; see also Figure 2).

Caution advised regarding exports to other industries

The chemical and pharmaceutical sectors in Germany receive relatively good ratings for their payment practices. It is also worth consulting the Payment Practices Barometer to establish how long business partners in other sectors in Germany and abroad wait to pay invoices.

In Germany, the services, transport, technology, research and electronics sectors also achieve comparatively high scores. On average, suppliers waited 39 days to have their invoices paid. The food industry took 3 days longer to pay. The manufacturing industry scored average (44 days), along with the automotive sector (45 days). The clothing industry (48 days) and furniture industry (58 days) are towards the bottom of the league table, with the public sector in last place after a marked gap – government offices and local authorities took almost ten weeks to pay invoices. Incidentally, this is by no means the maximum in a European comparison. Companies supplying the public sector in Italy waited approximately 3 months (104 days) to receive payments. Suppliers to the following sectors in European countries also had to wait patiently for payment of their invoices: automotive (94 days) and clothing (91 days) in Italy, trade/wholesale (70 days) and retail (69 days) in France and the public sector in the UK (66 days). Comparing the times recorded in the two Payment Practices Barometer surveys conducted in summer 2006 and winter 2006/2007, it is evident that the average time for the payment of outstanding invoices recorded in the later survey was longer for almost all of the sectors.

High risk of non-payment

While allowing long periods for payments is common practice in some sectors and also accepted in some cases, actual non-payment of receivables is more than just annoying and in the worst case may jeopardise the existence of a company. A simple calculation illustrates this fact. If a supplier is left with one invoice worth € 50,000 unpaid, assuming a sales return of 5%, he would have to generate an additional € 1 m to absorb the non-payment of this one invoice. For small and medium-sized companies, in particular, one unpaid invoice can impact heavily on the income statement of the relevant financial year. German companies supplying the following sectors in other European countries should analyse business partners carefully and obtain comprehensive information about their creditworthiness:

- manufacturing industry in France: 11% of respondents indicated that payment problems with representatives from the sector occurred “very frequently” or “relatively frequently”;

- technology, research and electronics in Italy: payment delays occurred “very frequently” in 6% of cases and “relatively frequently” in 3%;

- pharmacies and hospitals in the UK: an average of 7% defaulted on payments “very frequently”.

Credit insurance provides instant liquidity

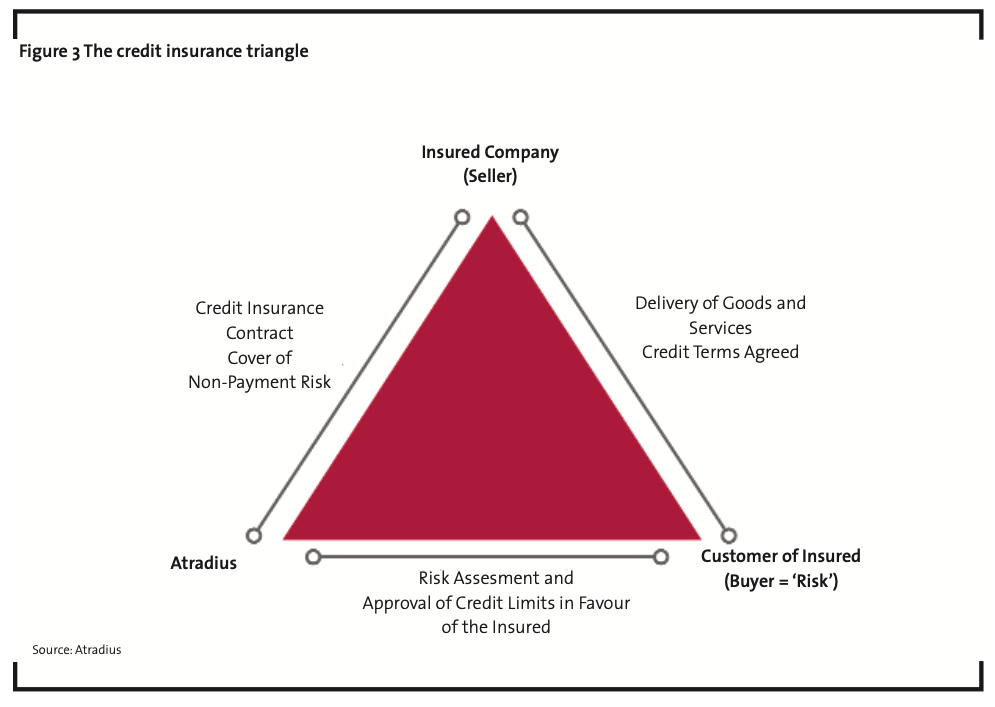

Credit insurers regularly check the creditworthiness of customers on behalf of their clients and hedge against specific risks or the complete portfolio of receivables. These risks include customers’ inability to pay, exchange rate fluctuations and political risks in the export business. The credit specialists have the required expertise and can rely on a worldwide network of sector experts to assess the financial strength of customers as accurately as possible.

Hedging the portfolio of accounts receivable is often a prerequisite for obtaining a loan from the main bank, particularly in connection with major projects where companies require sales financing. The bank will only give the green light for the financing of imminent orders once a credit insurance policy with a cover note is in place. If one party is unable to meet its liabilities, or unable to meet these on time, the credit insurance kicks in, preventing any negative impact on the liquid funds and earnings of the company by providing compensation promptly (please refer to Figure 3 regarding the tripartite relationship in credit insurance).

Summary

In an increasingly competitive market environment, which is coupled with the intensifying international credit crisis, it is virtually impossible for companies to avoid granting trade credit and allowing long periods of time for payments to be made. However, this is risky since non-payment will occur time and again. In addition, payment practices in some sectors and countries are far from ideal, with invoices remaining unpaid for weeks. These days, the traditional means for companies to protect themselves against nonpayment by customers, such as delivery upon advance payment or granting guarantees, are accepted only by a minority of business partners. This makes it all the more important for companies to hedge their complete portfolio of receivables where possible. Credit insurance companies have developed sector-specific solutions to prevent the worst case scenario of a financial collapse of companies through no fault of their own but caused by their customers’ inability to pay.

Atradius Credit Insurance has published three Payment Practices Barometers for the B2B segment to date. In each of the surveys carried out in summer 2006, winter 2006/2007 and winter 2007, a total of 1,200 participants, who are responsible for the receivables management in their companies, were questioned about the payment behaviour of their business partners in Germany, Belgium, France, the UK, Italy and the Netherlands. An interim evaluation of the 15 major economic sectors in Europe was published in July 2007. The surveys were conducted by Psychonomics AG in Cologne (summer 2006, winter 2006/2007 and sector evaluation in July 2007) and Heliview Research in Breda (winter 2007) respectively.

Atradius is a leading credit insurer with total sales of € 1.3 bn and a 24% share of the global credit insurance market. The company insures trade transactions worth € 400 bn a year against the risk of non-payment and offers products and services relating to risk transfer and receivables management. With 3,500 staff and more than 90 offices based in 40 countries, Atradius has access to information about the credit quality of 45 million companies across the globe and makes more than 12,000 credit limit decisions every day. Atradius has an A rating from Standard & Poor’s (outlook stable) and an A2 rating from Moody’s (outlook stable).